Geopolitics

Highlights So What? The Trump administration’s decision to apply maximum pressure to Iran fundamentally changes the investment landscape in 2019-20. Why? The impact of the Iran sanctions on a stand-alone basis can easily be handled given OPEC 2.0’s current spare capacity. However, not only Iranian and Venezuelan oil but also Iraqi oil could be pulled off the market in a full-fledged conflict. Policy-induced volatility and the oil risk premium will rise. Geopolitical tail risks have gotten fatter and the odds of a recession have also increased. Feature What are the Trump administration’s foreign policy objectives? First, to confront the U.S.’s greatest long-term competitor, China, by demanding economic reforms and greater market access. Second, to force a decision-point upon rogue regimes with significant ballistic missile programs and nuclear-weapon aspirations: North Korea and Iran. Third, to maintain credible deterrence in Russia’s periphery. Fourth, to reassert the Monroe Doctrine through regime change in Venezuela. The common thread, even with Russia, is confrontation. It is not necessary for President Trump to pursue all of these objectives at once. So his decision last November to issue waivers for eight importers of Iranian oil suggested to us that he was prioritizing – and becoming more risk averse ahead of the 2020 election. Full enforcement of the oil sanctions at that time threatened to push oil prices up at the same time as the Fed was raising rates, a pernicious combination late in the cycle (Chart 1). Thus, after walking away from the 2015 nuclear accord with Iran, it made sense for Trump to delay any confrontation with Iran until his hoped-for second term in office. He could focus on building the border wall, resolving trade tensions with China, and making peace with North Korea instead. Chart 1Full Sanctions Enforcement Was Too Risky Last November

Full Sanctions Enforcement Was Too Risky Last November

Full Sanctions Enforcement Was Too Risky Last November

Chart 2Sanctions Will Raise Risk

Sanctions Will Raise Risk

Sanctions Will Raise Risk

This view has now been proved wrong. The oil waivers apparently represented only a temporary delay in the administration’s hawkish Iran policy. Now that financial conditions have eased and growth has stabilized, Trump has declared the Iranian Revolutionary Guard Corps a foreign terrorist organization and announced that he will discontinue the waivers, demanding full compliance on energy sanctions from all states by the end of May. Volatility will move higher (Chart 2). Trump is emboldened by America’s newfound energy independence (Chart 3). While the shale boom can be used to reduce U.S. strategic commitments in the Middle East, it can also encourage Washington to believe it is invulnerable to traditional Middle Eastern risks. Trump’s advisers, Secretary of State Mike Pompeo and National Security Adviser John Bolton, apparently have won the Iran policy debate on this basis. Since Trump’s reelection is far from guaranteed, it would appear his advisers view re-imposing sanctions against Iran as a rare opportunity to achieve long-term strategic objectives. They may not have the chance in 2021. Chart 3The U.S. Is Energy Independent

The U.S. Is Energy Independent

The U.S. Is Energy Independent

Chart 4Trump's Reelection At Risk If Oil Spikes

Trump's Reelection At Risk If Oil Spikes

Trump's Reelection At Risk If Oil Spikes

All the same, the problem for Trump is that, while the U.S. will survive any chaos ensuing from an Iran confrontation, his presidency may not. Full enforcement of the sanctions could spiral out of control and, through the oil price channel, come back to hurt Trump’s economy – and hence his re-election odds (Chart 4). The implication is that Trump has either been misled about the risks of his Iran policy, or he does not care as much about his re-election odds as we believed. Either way, the result is aggressive policy, which increases the geopolitical risk premium in oil prices. We can see this in our simulations (below), which are based entirely on spare capacity and compliance by consumers to the sanctions. We did not include an Iran-retaliation scenario in this modeling. Therefore, any threat to Iraqi supplies, or talks of disrupting the Strait of Hormuz will add to our prices forecasts. U.S. Administration Sailing Close To The Wind From their public comments, it would appear the U.S. administration has convinced itself the global oil market can absorb a disruption from the loss of production in Iran and Venezuela. For the Trump administration, this view is supported by growing U.S. shale-oil supplies, and the administration’s belief the Kingdom of Saudi Arabia (KSA) and its Gulf allies stand ready to increase production to cover any losses arising from the re-imposition of Iranian oil-export sanctions by the U.S. This belief supports the administration’s end-game, which appears to be regime change in Iran, a position long favored by Trump’s national security advisor John Bolton. Frank Fannon, U.S. Assistant Secretary of State for Energy Resources, succinctly captured the administration’s view when he declared, “We are doing this ... in a favorable market condition with full commitment from producing countries.” He further stated, “We think this is the right time.”1 We believe the Trump administration is sailing close to the wind here. The U.S. administration has convinced itself the global oil market can absorb a disruption from the loss of oil production in Iran and Venezuela. While increasing U.S. shale output does provide something of a cushion to global oil markets, it is not a substitute for the heavy-sour crude produced by Iran and Venezuela (and others), which is favored by refiners with complex units. The loss of Iranian exports hits these refiners harder than those able to process lighter, sweeter crude of the sort exported by the U.S. (Chart 5).2 As Iranian and Venezuelan barrels are lost to the market, these heavier crudes are getting more scarce relative to the crude produced in U.S. shales – typically classified as West Texas Intermediate (WTI) crude oil. This can be seen in tighter light-versus-heavy crude oil spreads, and the wider Brent-WTI spreads, which indicate WTI is relatively more plentiful (Charts 6A & 6B).

Chart 5

Chart 6AWTI Relatively More Plentiful…

WTI Relatively More Plentiful...

WTI Relatively More Plentiful...

Chart 6B…As Heavier Crudes Become More Scarce

...As Heavier Crudes Become More Scarce

...As Heavier Crudes Become More Scarce

It is true U.S. production continues to grow, which is causing crude oil inventories to increase as sanctions on Iran are being re-imposed. We expect U.S. shale-oil output to grow 1.2mm b/d this year – taking it to a record 8.4mm b/d on average – and 800k b/d next year. Caution is required regarding inventories, however: U.S. refiners are in the thick of their plant maintenance – known as turn-around season – and have loaded a lot of the maintenance they would normally have done in the Fall into Spring. As a result, U.S. refiners are running at reduced rates preparing for the Northern Hemisphere’s summer driving season and the January 1, 2020, implementation of the U.N. IMO 2020 regulations, which will require shippers to use lower-sulfur fuel to power their vessels worldwide.3 OPEC 2.0 Gains Control Of Brent Forward Curve Growing U.S. production and inventories might give the Trump administration comfort the market can absorb the loss of Iran’s exports – some 1.3mm b/d at present. However, our base case holds that Iran’s exports will stabilize at ~ 600k b/d after sanctions fully kick in. In most of the scenarios we run (Table 1), the impact of Iran sanctions on a stand-alone basis can easily be handled given OPEC 2.0’s current spare capacity (Chart 7).4 Indeed, many of the low-probability scenarios we run – including the “maximum pressure” scenario, in which the Trump administration succeeds in removing all of Iran’s exports – can be accommodated by current supply and spare capacity without sending Brent prices through $100/bbl (Chart 8). OPEC 2.0 holds ~ 1.5mm b/d of what we would describe as readily available spare capacity – mostly in KSA – that can be brought to market fairly quickly, as the ramp-up last year ahead of the first round of sanctions in November amply demonstrated. Another 1.5mm b/d or so is held by the Kingdom and its GCC allies, but it would take longer to bring on line. Table 1BCA Oil Market Scenarios

U.S.-Iran: This Means War?

U.S.-Iran: This Means War?

Chart 7OPEC 2.0 Can Handle Iranian Losses

OPEC 2.0 Can Handle Iranian Losses

OPEC 2.0 Can Handle Iranian Losses

Chart 8Brent Unlikely To Surpass $100

Brent Unlikely To Surpass $100

Brent Unlikely To Surpass $100

In reality, once refiners are up and running at max capacity in the U.S. in a few weeks, U.S. inventories will begin to draw hard. This will support what we believe to be OPEC 2.0’s goal of backwardating the Brent curve – perhaps sharply. This will allow it some breathing space to gradually add barrels to the market in 2H19 as needed, as our balances and forecasts assume. It is important to remember OPEC 2.0 was formed to drain the massive storage overhang that resulted from the 2014-16 market-share war launched by KSA. The Kingdom’s energy minister, Khalid al-Falih, is in no hurry to reverse OPEC 2.0’s strategy now. Throughout the ramp to renewed sanctions, he has steadfastly maintained the Kingdom will provide oil as Aramco’s customers need it, following the blind-side hit KSA took from the Trump administration in November when it granted Iran’s largest customers waivers on its export sanctions. U.S. Pressure On OPEC To Raise Output Will Grow We expect the Trump administration to continue to pressure OPEC – the old cartel, not OPEC 2.0 – to boost production post-sanctions. However, it is not entirely clear that this time OPEC’s – particularly KSA’s – interests are 100% aligned with President Trump’s. KSA and other producers were shocked by the administration’s decision to grant waivers after lifting supply sharply in response to Trump’s demands. This time around, we believe OPEC – KSA in particular – will be more cautious lifting output, even as the U.S. Navy very publicly displays its ability to project and sustain force in the Mediterranean and Persian Gulf regions (Map 1). With good reason: The U.S. holds ~ 650mm barrels of oil in its Strategic Petroleum Reserve (SPR), which can be released at a rate of 1mm to 1.3mm b/d for a year or so. Realistically, it is probably more like six to nine months, since, by the time much of the oil has been released to the market the reserves that are left likely will have higher concentrations of contaminants (e.g., metals and solids that migrated to the bottom of the storage while it was sitting idle), making buyers way more leery of using it.

Chart

After the shock of the waivers, KSA likely will minimize its exposure to another surprise from the U.S. as sanctions take hold. The risk to OPEC – KSA in particular – is that Trump again will pull a fast one as the U.S. general election approaches. Given Trump’s demonstrated sensitivity to U.S. gasoline prices approaching elections, it is not unlikely that he would hold on to the SPR barrels until mid to late summer 2020, then release them in time to reduce prices further. If, in the run-up to U.S. elections, OPEC has steadily increased production to build precautionary inventories then it runs a non-trivial risk the crude oil price would once again crash as SPR barrels are released. The Kingdom of Saudi Arabia’s energy minister, Khalid al-Falih, is in no hurry to reverse OPEC 2.0’s strategy now. In this iteration of Iranian export sanctions, we expect KSA to adopt a just-in-time inventory management strategy, so that it is not caught out once again over-supplying the market ahead of a U.S. surprise. U.S. Shales Will Figure Into OPEC 2.0’s Calculus Chart 9U.S. Export Capacity Is Constrained

U.S. Export Capacity Is Constrained

U.S. Export Capacity Is Constrained

The other big fundamental OPEC 2.0 will be considering is the rate at which U.S. shale oil can be exported. Export capacity still is constrained by the shortage of deep-water harbor facilities in the U.S. Gulf. This is being addressed, but it has been slowed by additional requests for environmental impact statements from the federal and state governments. If prices start moving higher because KSA and OPEC 2.0 are responding to tightening markets with caution (and slowly), we’d likely see WTI production increase – it’ll have 2mm b/d of new pipe in the Permian to fill by end-2019 – but that crude could start backing up as storage in the U.S. Gulf fills. This would again widen the Brent vs. WTI - Houston spread, which will benefit refiners in the U.S. Gulf, but will lower prices received by U.S. shale producers (again) (Chart 9). Bottom Line: Trump’s decision not to extend the Iranian oil waivers suggests that he has plenty of risk appetite ahead of the 2020 election. His Iran policy is now the biggest geopolitical risk to the late-cycle bull market. It also risks tightening the oil market considerably as the election approaches. Can Iran’s Regime Withstand The Sanctions? Iran’s economic weakness was an added inducement for the Trump administration to take an aggressive turn. The sanctions against Iran’s crude oil exports have not yet been implemented in full force, but the economy is already showing signs of distress. For one, inflation is back near 40% – levels only reached during the previous round of sanctions (Chart 10). Given that food, beverages, and transportation are among the sectors experiencing the fastest growing prices, lower income groups – which the World Bank estimates spend almost half their income on food alone – will suffer disproportionately. Economic dissatisfaction has catalyzed protests in Iran in the past, and the squeeze from the U.S. sanctions could propel further unrest. Chart 10Iran's Economy Already Showing Signs Of Distress

Iran's Economy Already Showing Signs Of Distress

Iran's Economy Already Showing Signs Of Distress

Chart 11

Moreover, soaring prices are coinciding with a slowdown in activity and consumption. On the surface Iran appears relatively well protected given that its economy is not as directly correlated with oil exports as some of its peers (Chart 11). However, Iran’s oil and non-oil sectors are actually closely intertwined. This is evident from weakness in the non-oil sector during the previous round of sanctions (Chart 12). The IMF expects the economy to contract by 6% this year – faster than its 3.9% estimate for last year – leaving Iranians to face a period of deepening stagflation.

Chart 12

The jump in consumer prices is a reflection of the ongoing collapse of the currency. Despite the government’s best efforts to stabilize the foreign exchange market, heightened demand for foreign currencies caused a nearly 30% depreciation in the unofficial exchange rate vis-à-vis the U.S. dollar since the beginning of the year (Chart 13). Chart 13Unofficial Exchange Rate Continues To Weaken

Unofficial Exchange Rate Continues To Weaken

Unofficial Exchange Rate Continues To Weaken

Chart 14Debt Burden Is Manageable

Debt Burden Is Manageable

Debt Burden Is Manageable

To soften the impact of the weaker currency and the potential shortage of essential goods, authorities have introduced a three-tier exchange rate system, and banned the export of several products including grains and seeds, powdered milk, butter, and tea. Since the level of external debt remains manageable (Chart 14) the weak currency will pressure the economy through its impact on prices (highlighted above), with imported inflation eroding purchasing power. Furthermore, Iran will not benefit from any additional export competitiveness due to currency depreciation. The current account surplus is expected to deteriorate and eventually flip to a deficit amidst weak exports, and despite declining imports (Chart 15). The fact that Iran runs a non-energy trade deficit does not help. Chart 15Trade Surplus At Risk

Trade Surplus At Risk

Trade Surplus At Risk

Chart 16Rising Budget Deficit Is A Constraint

Rising Budget Deficit Is A Constraint

Rising Budget Deficit Is A Constraint

In terms of the fiscal purse, under normal circumstances, a weaker rial would raise government revenue from oil exports. However, given the restrictions on oil exports, the fiscal budget will not benefit from this relationship. Instead, the dominant impact will be greater government spending. Historically, expenditures tend to be countercyclical, aiming to mitigate the impact of the deteriorating economic environment on Iranian households (Chart 16). In the past, the Iranian government’s healthy fiscal balance allowed policymakers to implement social protection schemes to combat poverty and revitalize the economy. Now, however, the fiscal coffers are no longer so well-cushioned and the deficit will constrain this option. Stimulative fiscal policy in this environment would only raise inflation further. Furthermore, given that the lion’s share of Iran’s imports are capital and intermediate goods, the currency depreciation will spill over into the domestic industry and weaken demand, even for domestically produced goods. Investments have been lacking in many of the most essential services. The electricity sector is a prime example: while demand is rising, spare capacity is dwindling and causing recurring outages. Similarly, foreign direct investment will likely fall in this uncertain political environment. With the economy on the brink, Iran is not in a position to confront the United States directly. It must take total sanctions enforcement as a very grave risk and seek delaying actions and negotiations. However, this vulnerability will turn into desperation if the Trump administration proceeds with a full embargo without any “off ramp” for negotiations. Bottom Line: Full enforcement of sanctions threatens to destabilize Iran’s already vulnerable economy. Inflation is soaring, the currency is plunging, and the economy will likely be plagued by a twin deficit going forward. The implication is that Iran will eschew direct confrontation unless forced. Will Iran Retaliate In Iraq? Iran is also at risk of losing one of its great sources of leverage: Iraqi stability. Given its gloomy economic outlook, Iran is looking to expand ties with its neighbors in an attempt to soften the blow from the sanctions. Earlier this year president Hassan Rouhani and Iraqi prime minister Adel Abdul Mahdi signed several preliminary trade deals, with the ultimate aim to boost bilateral trade to $20 billion from its current ~$12 billion. However, natural gas exports to Iraq – a major traded good – are covered by the sanctions, so this target is probably unattainable. Although Iran is currently the only foreign supplier of natural gas and electricity to Iraq, the temporary halt in electricity supplies last summer coincided with violent protests in Southern Iraq.5 Growing anger over Iran’s inability to satisfy its commitments to Iraq highlights the tensions in the Iraq-Iran relationship. What’s more, the U.S. is pressuring Iraq to turn to other neighbors such as Saudi Arabia, Jordan, and Kuwait for its electricity needs.6 In March, it renewed a three-month waiver allowing Iraq to import Iranian gas. Then Saudi Arabia promised to connect Iraq to the Saudi electricity grid during a visit by its economic delegation to Baghdad on April 4.7 At that meeting, the Saudi delegation also agreed to provide Iraq with $1 billion in loans, $500 million to boost exports, and a sporting complex as a gift. Additionally, the Saudi consulate in Baghdad – which had been closed for almost 3 decades – reopened last month. Saudi Arabia and Iraq are starting to cooperate. Iraq’s new government is clearly taking a pragmatic approach to its regional relationships. This is also largely in line with growing domestic opposition to Iranian interference within Iraq. Influential Shia leaders such as Muqtada al-Sadr and Ayatollah Ali al-Sistani have been voicing concerns about Iran’s influence in Iraqi politics. As such, the new Iraqi government is attempting to walk a tight rope between placating Iran and taking advantage of new opportunities with its Arab neighbors to rebuild its economy. This trend raises the risk that Iran will strike rapidly in Iraq if it believes Trump’s maximum pressure strategy is succeeding in bringing oil exports to zero. Iraq is the logical target as Iran has great political and sectarian influence there, it is the geographic buffer with Saudi Arabia, and it is the necessary launchpad for Iran’s strategic opponents to undermine or attack the Iranian regime (Map 2).

Chart

Thus, not only Iranian and Venezuelan oil but also Iraqi oil could be pulled off the market in a fullfledged conflict.

Chart 17

Thus, not only Iranian and Venezuelan oil but also Iraqi oil could be pulled off the market in a full-fledged conflict. About 85% of Iraq’s crude exports flow through the southern port city of Basra (Chart 17). It is already home to recurrent protests and any disruptions there threaten around 3.5mm bbl shipping to international markets daily. Bottom Line: Iraq is caught in the strategic tug-of-war between Iran and Saudi Arabia, with the latter gaining influence at present. Sanctions could compel Iran to retaliate in Iraq, jeopardizing up to 3.5mm b/d of supply. What Comes Next? The latest data suggest that Japan is in full compliance with the U.S. sanctions against Iran as of April and that China has been front-running the sanctions and is now reducing imports, as it was at the time the waivers were first introduced. China may not go to zero, but it is apparently complying. This is important given that the Trump administration has essentially introduced a bold new demand – cut off all energy imports from Iran – at the eleventh hour of the U.S.-China trade negotiations. Our projections of spare capacity suggest that the Trump administration will believe it has room to enforce the sanctions fully (Chart 18). This is a risky approach, as a fairly standard unplanned outage anywhere else in the world could bring spare capacity much lower, but the data suggest that Trump’s team will not see it as a hard constraint. If necessary, the administration can later choose to soft-pedal enforcement on black market activity so as to calibrate the global impact.

Chart 18

The Iranians, for their part, are unlikely to leap to the most aggressive forms of retaliation immediately – such as fomenting unrest in Iraq – because of their economic vulnerability. Small acts of sabotage or subversion are a way to send the U.S. a warning signal, but generally Iran will want to signal defiance while shifting the emphasis to negotiations. Hence it will primarily retaliate through diplomatic actions and calculated displays of force. A limited response enables Iran to appear innocent, divide the U.S. and EU, and thus isolate the U.S. over its belligerent policies. Previously, Trump has sought to negotiate with Iranian President Hassan Rouhani. The Iranians have so far rebuffed him, but Foreign Minister Mohammad Zarif’s initial response to the waiver announcement was to blame Trump’s advisers, instead of Trump himself, and offer an exchange of prisoners (And release of detained Americans happen to be one of the Trump administration’s key demands – see Table 2.) Negotiations could begin through back channels and an uneasy period of tensions could thus ensue without a full-blown war. Table 2Trump Administration’s 12 Demands On Iran

U.S.-Iran: This Means War?

U.S.-Iran: This Means War?

The problem is that negotiations cannot work if Trump fully and immediately enforces the sanctions without offering Iran an “off ramp.” If the administration backs Iran into a corner it will have no option but to strike out forcefully. Negotiations also cannot work if Iran joins the U.S. in withdrawing from the 2015 deal and reactivating its nuclear program, specifically the suspected military dimensions of that program. This would force Trump to respond (Diagram 1). Diagram 1Iran-U.S. Tensions Decision Tree

U.S.-Iran: This Means War?

U.S.-Iran: This Means War?

In short, a period of “fire and fury” is about to ensue between Trump and Rouhani. It will be even more uncertain and disruptive than the summer 2017 showdown between Trump and Kim Jong Un of North Korea (Chart 19), which drove a 35 bps decline in the 10-year Treasury yield. Chart 19Upcoming "Fire And Fury" Will Be More Disruptive Than 2017 Trump-Kim Showdown

Upcoming "Fire And Fury" Will Be More Disruptive Than 2017 Trump-Jong Un Showdown

Upcoming "Fire And Fury" Will Be More Disruptive Than 2017 Trump-Jong Un Showdown

There is a pathway for Trump’s pressure tactics to succeed: Iran is vulnerable and the United States and its allies are in a position of relative strength in terms of global oil supply. Therefore, it is possible that Trump could fully enforce the sanctions and yet avoid any uncontrollable crisis or oil shock. However, this pathway, at a subjective 26% probability, is less likely than the combined 48% probability of the alternatives: either escalation short of war, or ultimatums leading to Middle Eastern instability and much higher odds of war. Bottom Line: The geopolitical risk of U.S.-Iran confrontation is not contained. But we do not expect Iran to overreact unless Trump plows forward with full and immediate sanctions enforcement and offers no realistic “off ramp” for negotiations. At that point Iranian retaliation will be concrete and escalation could spiral out of control. Investors should keep in mind that Iran is not North Korea. Unlike the hermit kingdom, Iran has the ability to retaliate with a number of different levers. Indeed, it has threatened to shut the Strait of Hormuz in the past, and could, at the limit, be backed into that corner. While the risk of this is extremely low, should it occur the consequences would be huge – close to 20% of the world’s daily oil supply passes through the Strait daily. Indeed, just this week Iran’s Oil Minister Bijan Zanganeh again threatened to take action against any OPEC member working against its interests. Following a meeting with the Cartel’s president, he is reported to have said, “Iran is a member of OPEC because of its interests, and if other members of OPEC seek to threaten Iran or endanger its interests, Iran will not remain silent.”8 Investment Conclusions The Trump administration’s decision to apply maximum pressure to Iran is a significant and unexpected injection of geopolitical risk that we believe fundamentally changes the investment landscape in 2019-20. While our base case is that the U.S. will enforce the oil sanctions gradually and in such a way as to avoid causing an oil shock, policy-induced volatility and the oil risk premium will rise. Geopolitical tail risks have gotten fatter and the odds of a recession have also increased. Robert P. Ryan, Chief Commodity & Energy Strategist rryan@bcaresearch.com Matt Gertken, Geopolitical Strategist mattg@bcaresearch.com Roukaya Ibrahim, Editor/Strategist roukayai@bcaresearch.com Footnotes 1 Please see Humeyra Pamuk and Timothy Gardner, “How Trump’s hawkish advisors won debate on Iran oil sanctions,” Reuters, May 1, 2019, available at reuters.com. 2 Heavy-sour crudes are those with low API gravity (a measure of how easily a crude flows) and higher sulfur content. Light-sweet crudes have higher API gravity and lower sulfur content. 3 Please see BCA Commodity & Energy Strategy Weekly Report, “IMO 2020: The Greening Of The Ship-Fuel Market,” February 28, 2019, available at ces.bcaresearch.com. 4 OPEC 2.0 is the name we coined for the producer coalition led by KSA and Russia, which was formed in 2016 to manage global crude oil output. Its goal is to drain the massive storage overhang caused by the market-share war launched by KSA in 2014. 5 Iran cited dissatisfaction with Iraq over the accumulation of unpaid bills as the cause of the halt in electricity exports to Iraq. This prompted Iraqi authorities – under pressure from domestic unrest – to send a delegation to Saudi Arabia in attempt to negotiate an electricity agreement. 6 Please see Edward Wong, “Trump Pushes Iraq to Stop Buying Energy From Iran,” The New York Times, February 11, 2019, available at nytimes.com. 7 Please see Geneive Abdo and Firas Maksad, “Iraq’s Place in the Saudi Arabian-Iranian Rivalry,” The National Interest, April 15, 2019, available at nationalinterest.org. 8 Please see Babk Dehghanpisheh, “Iran will respond if OPEC members threaten its interests: oil minister,” Reuters, May 2, 2019, available at reuters.com. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades TRADE RECOMMENDATION PERFORMANCE IN 2019 Q1

Image

Commodity Prices and Plays Reference Table Trades Closed in 2019 Summary of Closed Trades

Image

Investor surveys show that the majority of investors’ top concerns are political or geopolitical in nature. Yet there is limited research devoted to quantifying these risks. The most prominent techniques involve tallying word counts of key terms that appear…

Highlights So what? Quantifying geopolitical risk just got easier. Why? In this report we introduce 10 proprietary, market-based indicators of country-level political and geopolitical risk. Featured countries include France, U.K., Germany, Italy, Spain, Russia, South Korea, Taiwan, Turkey, and Brazil. Other countries, and refinements to these beta-version indicators, will come in due time. We remain committed to qualitative, constraint-based analysis. Our GeoRisk Indicators will help us determine how the market is pricing key risks, so we can decide whether they are understated or overstated. Feature For the past three months we have been tracking a “Witches’ Brew” of political risks that threaten the late-cycle bull market. Some of these risks have abated for the time being: the Fed is on pause, China’s stimulus has surprised to the upside, and Brexit has been delayed. Other risks we have flagged, however, are heating up: Iran And Oil Market Volatility: Surprisingly the Trump administration has chosen not to extend oil sanction waivers on Iran from May 2, putting 1.3 million barrels per day of oil on schedule to be removed from international markets by an unspecified time. It remains to be seen how rapidly and resolutely the administration will enforce the sanctions on specific allies and partners (Japan, India, Turkey) as well as rivals (China, others). Because the decision coincides with rising production risks from renewed fighting in Libya and regime failure in Venezuela, we expect President Trump to phase in the new enforcement over a period of months, particularly on China and India. But official rhetoric is draconian. Hence the potential for full and immediate enforcement is greater than we thought. In the short term, individual political leaders, and very powerful nations like the United States, can ignore material economic and political constraints. Since the Trump administration’s decision exemplifies this point, geopolitical tail risks will get fatter this year and next. Global oil price volatility and equity market volatility will increase with sanction enforcement actions and retaliation. We would think that Trump’s odds of reelection will marginally suffer, though for now still above 50%, as any full-fledged confrontation with Iran will raise the chances of an oil price-induced recession. U.S.-EU Trade War: Neither the Trump administration nor the U.S. has a compelling interest in imposing Section 232 tariffs on imports of autos and auto parts. Nevertheless the risk of some tariffs remains high – we put it at 35% – because President Trump is legally unconstrained. The decision is technically due by May 18 but Economic Council Director Larry Kudlow has said Trump may adjust the deadline and decide later. Later would make sense given the economic and financial risks of the administration’s decision to ramp up the pressure on Iran.1 But the risk that tariffs will pile onto a weak German and European economy will hang over investors’ heads. U.S.-China Talks Not A Game Changer: The ostensible demand that China cease Iranian oil imports immediately and the stalling of U.S. diplomacy with North Korea are not conducive to concluding a trade deal in May. We have highlighted many times that strategic tensions will persist even if Beijing and Washington quarantine these issues to agree to a short-term trade truce. The June 28-29 G20 meeting in Japan remains the likeliest date for a summit between Presidents Trump and Xi Jinping, but even this timeframe could be too optimistic. Continued uncertainty or a weak deal will fail to satisfy financial markets expecting a very positive outcome. With a 70% chance that U.S. tariffs on China will not increase this year and, contingent on a U.S.-China deal, only a 35% chance that the U.S. slaps tariffs on German cars, we sound optimistic to some clients. But the Trump administration’s decision on Iran is highly market-relevant and portends greater volatility. We expect to see a geopolitical risk premium creep higher into oil markets as well as a greater risk of “Black Swan” events in strategically critical or oil-producing parts of the Middle East. There is limited research devoted to quantifying geopolitical risk. We are late in the business cycle and President Trump has emphatically decided to increase rather than decrease geopolitical risk. Quantifying Geopolitical Risk Geopolitical analysis has taken a bigger role in investors’ decision-making over the last decade. Surveys show that geopolitical risks rank among global investors’ top concerns overall. In the oft-cited Bank of America Merrill Lynch survey, geopolitical and related issues have dominated the “top tail risk” responses for the past half-decade (Chart 1). In other surveys, the most worrisome short-term risks are mostly political or geopolitical in nature, ranking above socio-economic and environmental risks (Chart 2).

Chart 1

Chart 2

Despite this high level of concern, there is limited research devoted to quantifying geopolitical risk. Isolating and measuring the range of risks under this umbrella term remains a challenge. As such, for many investors, geopolitics remains an ad hoc, exogenous factor that is often mentioned but rarely incorporated into portfolio construction. For the past four decades the predominant ways of measuring political or geopolitical risk have been qualitative or semi-qualitative. The Delphi technique, developed on the basis of low-quality data sets in social sciences, relies on pooled expert opinions.2 Independently selected experts are asked to provide risk assessments and their responses are then interpreted by analysts to create a measure of risk. Another semi-qualitative method of measuring geopolitical risk ranks countries according to a set of political and socio-economic variables. These variables – such as governance, political and social stability, corruption, law and order, or formal and informal policies – are extremely important but inherently difficult to quantify.3 These results are useful but suffer from dependency on expert opinion, data quality, and institutional biases. More importantly, these methods are slow to react to breaking events in a rapidly changing world. The same goes for bottom-up assessments using political intelligence. The weakness of these methods is that it is highly unlikely that they will produce statistically significant estimates of risk. The odds of getting a “silver bullet” insight from a “key insider” are decent for simple political systems, but not in the complex jurisdictions that host the vast majority of global, liquid investments. Quantitative approaches to measuring geopolitical risk have since become more widespread. The most prominent method is based on quantifying the occurrence of words related to political and geopolitical tensions that appear in international newspapers. These word-counts typically include terms like “terrorism,” “crisis,” “war,” “military action,” etc. As a result, the indices reflect incidents of physical violence or other “Black Swan” events that may not have direct relevance to financial markets. Moreover, while news-based indices accurately capture dramatic one-time peaks at the time of a crisis, they are largely flat aside from these, as they rely on popular topics rather than underlying structural trends (Chart 3). They fail to capture geopolitical developments associated with electoral cycles, protest movements, paradigm shifts in economic policy, or other policy changes.4 Notice, for instance, that the fall of the Soviet Union in late 1991 and the resulting chaos in Russia and many other parts of the emerging world hardly register in Chart 3. Chart 3News-Based Indices Only Capture Crisis Peaks, Not Geopolitical Developments

News-Based Indices Only Capture Crisis Peaks, Not Geopolitical Developments

News-Based Indices Only Capture Crisis Peaks, Not Geopolitical Developments

Introducing BCA’s GeoRisk Indicators The past 70 years have taught BCA Research to listen and respect the market. Why would we suddenly follow the media instead? Most quantitative geopolitical indicators begin with the premise that journalists and the news-reading public have accurately emphasized the most relevant risks and uncertainties. They proceed to quantify the terms of these assessments with increasingly sophisticated methods. This approach solves only part of the puzzle. News-based indices ... fail to capture geopolitical developments associated with underlying policy changes. At BCA Geopolitical Strategy, we aim to generate geopolitical alpha.5 This means identifying where financial media and markets overstate or understate geopolitical risks. We do not primarily aim to predict events or crises. As such, traditional news-based indicators that capture only major events, even those ex post facto, are of little relevance to our analysis. What is needed is a better way to quantify how the market is calculating risks. We start with a simple premise: the market is the greatest machine ever created for gauging the wisdom of the crowd. Furthermore, it puts its money where its predictions are, unlike other methods of geopolitical risk quantification which have no “value at risk.” Chart 4USD/RUB Captures Geopolitical Risk In Russia...

USD/RUB Captures Geopolitical Risk In Russia...

USD/RUB Captures Geopolitical Risk In Russia...

To this end, we have introduced market-based indicators over the years that rely on currency movements, which are often the simplest and most immediate means of capturing the process of pricing risk. In 2015, for instance, we introduced an indicator that measures Russia’s geopolitical risk premium (Chart 4). It is constructed using the de-trended residual from a regression of USD/RUB against USD/NOK and Russian CPI relative to U.S. CPI. We can show empirically that it captures geopolitical risk priced into the ruble, as the indicator increases following critical incidents. These include the downing of Malaysian Airlines Flight 17 over eastern Ukraine in 2014; the warnings that Russia aimed to stage a “spring offensive” in Ukraine in 2015; Russian military intervention in the Syrian Civil War later that year; and the poisoning of former intelligence agent Sergei Skripal in the U.K. in 2018 and subsequent tensions. Using similar methods, we created a proxy to capture geopolitical risk in Taiwan, based on USD/JPY and USD/KRW exchange rates and relative Taiwanese/American inflation (Chart 5). The indicator tracks well with previous cross-strait crises. It jumped upon Taiwan’s election of President Tsai Ing-wen and her pro-independence government in January 2016 – and this was well before any tensions actually flared. It even registered a small increase upon her controversial phone call congratulating Donald Trump upon winning the U.S. election. Chart 5...And USD/TWD Captures Geopolitical Risk In Taiwan

...And USD/TWD Captures Geopolitical Risk In Taiwan

...And USD/TWD Captures Geopolitical Risk In Taiwan

This year we have expanded on this work, constructing a set of ten standardized GeoRisk Indicators for five developed economies and five emerging economies: U.K., France, Germany, Spain, Italy, Russia, Turkey, Brazil, Korea, and Taiwan. Indicators for the U.S., China, and others will be rolled out in a future report. These indicators attempt to capture risk premiums priced into the various currencies – except for Euro Area countries, where the risk is embedded in equity prices. In each case, we look at whether the relevant assets are decreasing in value at a faster rate than implied by key explanatory variables. The explanatory variables consist of (1) an asset that moves together with the dependent variable while not responding to domestic geopolitical risks, and (2) a variable to capture the state of the economy. This set of indicators differs from our earlier indicators in the following ways: We aim to create a simple methodology that we can apply consistently to all countries, both in the DM and EM universes. We therefore omitted using regression models that can prove to be quite whimsical. Instead, we simply looked at the deviation of the dependent variable from the explanatory variables, all in expanding standardized terms, to create the GeoRisk proxy. We wanted an indicator that would immediately respond to priced-in risks, so we opted for a daily frequency rather than the weekly frequency we used in our initial work. To get as accurate of a signal as possible, we use point-in-time data. Since economic data tends to be released with a one-to-two-month lag, we lagged the economic independent variable to correspond to its release date. All ten indicators are shown in the Appendix. Across all countries, they track well with both short-term events and long-term trends in geopolitical risk. In the case of France, for example, the indicator steadily climbs during the period of domestic tensions and protests in the early 2000s; as the European debt crisis flares up; again during the rise of the anti-establishment Front National and the Russian military intervention in Ukraine; and finally during the U.S. trade tariffs and Yellow Vest protests (Chart 6). Our GeoRisk indicators isolate risks that either originate internally or otherwise affect the country more so than others. Similarly, in Germany, there is a general increase in perceived risk as Chancellor Gerhard Schröder implements structural reforms in the early 2000s; another increase leading up to the leadership change as Angela Merkel is elected Chancellor; another during the global and European financial crises; another during the Ukraine invasion and refugee influx; and finally another with the U.S.-China trade war (Chart 7). Chart 6Our French Indicator Picks Up Domestic And European Unrest

Our French Indicator Picks Up Domestic And European Unrest

Our French Indicator Picks Up Domestic And European Unrest

Chart 7Greater German Risk Amid The Trade War

Greater German Risk Amid The Trade War

Greater German Risk Amid The Trade War

We have annotated each country’s GeoRisk indicator heavily in the appendix so that readers can see for themselves the correspondence with political events. The indicators are affected by international developments – like the Great Recession – but we have done our best to isolate risks that either originate internally or otherwise affect the country more than other countries. (As a consequence, the Great Recession is muted in some cases.) What are the indicators telling us now? Most obviously, they highlight the extreme risk we have witnessed in the U.K. over the now-delayed March 29 Brexit deadline. We would bet against this risk as the political reality has demonstrated that a “hard Brexit” is very low probability: the U.K. has the ability to back off unilaterally while the EU is willing to extend for the sake of regional stability. In this sense the pound is a tactical buy, which our foreign exchange strategist Chester Ntonifor has highlighted.6 Our U.K. risk indicator has been fairly well correlated with the GBP/USD since the global financial crisis and it suggests that the pound has more room to rally (Chart 8). Chart 8Betting Against A Hard Brexit, the GBP Is A Tactical Buy

Betting Against A Hard Brexit, the GBP Is A Tactical Buy

Betting Against A Hard Brexit, the GBP Is A Tactical Buy

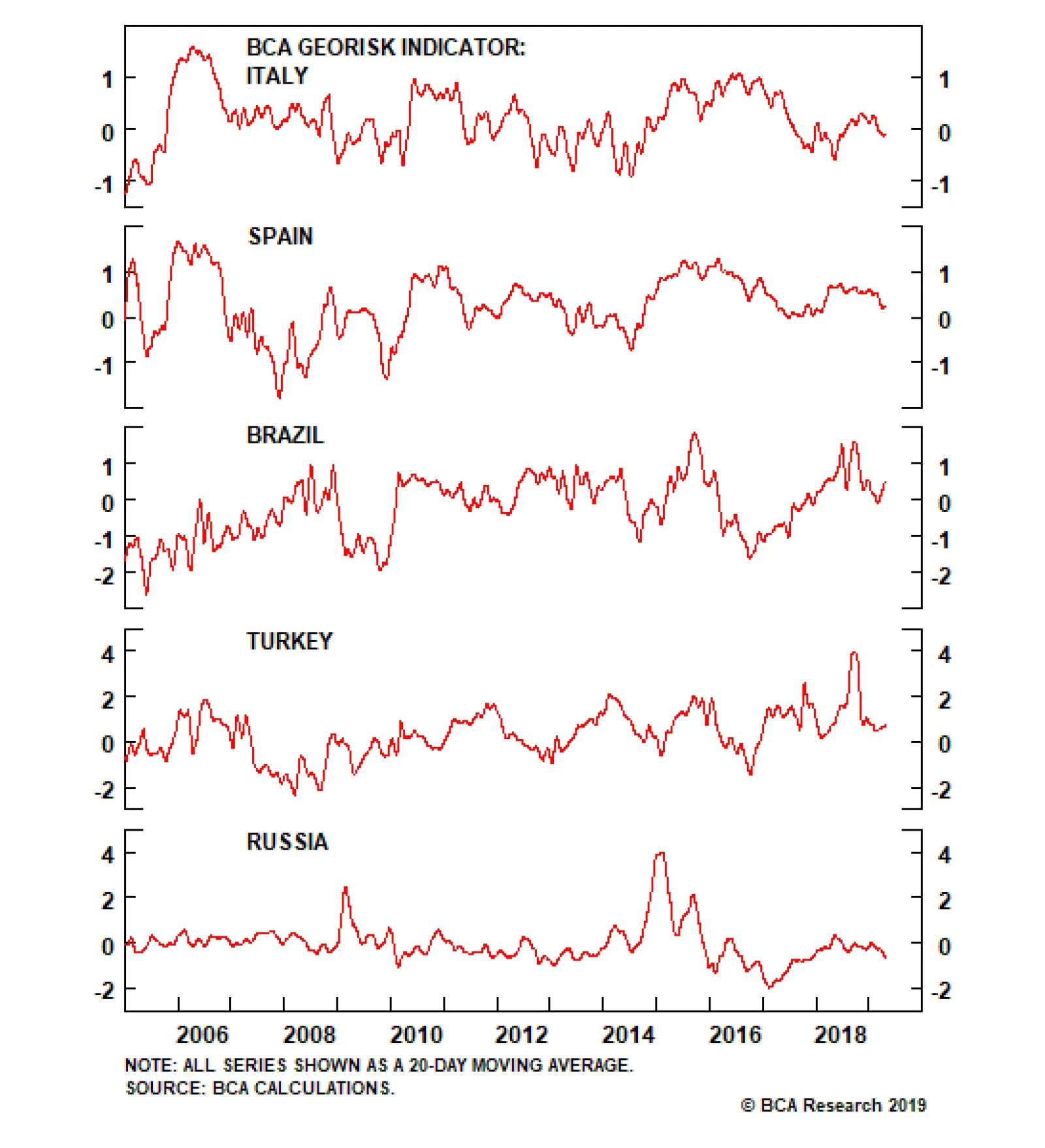

Meanwhile, Spanish risks are overstated while Italy’s are understated. As for the emerging world, Turkish risks should be expected to spike yet again, as divisions emerge within the ruling coalition in the wake of critical losses in local elections and a failure to reassure investors over monetary policy and the currency. Brazilian risks will probably not match the crisis points of the impeachment and the 2018 election, at least not until controversial pension reforms reach a period of peak uncertainty over legislative passage. Both our new Russian indicator and its prototype are collapsing (see Chart 4 above). This captures the fact that we stand at a critical juncture in Russian affairs, where President Putin is attempting to shift focus to domestic stability even as the U.S. and the West maintain pressure on the economy to deter Russia from its aggressive foreign policy. Given that both Putin’s and the government’s approval ratings are low amid rising oil prices, the stage is set for Russia to take a provocative foreign policy action meant to distract the populace from its poor living conditions. Venezuela is the obvious candidate, but there are others. Moscow will want to test Ukraine’s newly elected, inexperienced president; it may also make a show of support for Iran. With Russia equities having rallied on a relative basis over the past year and a half, and with the Iranian waiver decision already boosting oil prices as we go to press, the window of opportunity to buy Russian stocks is starting to close. (We remain overweight relative to EM on a tactical horizon; our Emerging Markets Strategy is also overweight.) Going forward, we will update these risk indicators regularly as needed and publish the full appendix at the end of every month along with our long-running Geopolitical Calendar. We will also fine-tune the indicators as new information comes to light. In other words, here we present only the beta version. We hope that these indicators will help inform investors as to the direction, and even magnitude, of political risks as the market prices them. Our GeoRisk indicators are not predictive, as establishing a trend is not a prediction. The main purpose of this exercise is to answer the critical question, “What is already priced in?” How is the market currently calculating geopolitical risk for a country? After that, it is the geopolitical strategist’s job to unpack this question through qualitative, constraint-based analysis. It is when our qualitative assessments disagree with what is priced in that we can generate geopolitical alpha. Ekaterina Shtrevensky, Research Analyst ekaterinas@bcaresearch.com Matt Gertken, Vice President Geopolitical Strategist mattg@bcaresearch.com Marko Papic Consulting Editor marko@bcaresearch.com Footnotes 1 See Sean Higgins, “Auto tariffs decision could be delayed, Kudlow says,” Washington Examiner, April 3, 2019, www.washingtonexaminer.com. 2 Norman C. Dalkey and Olaf Helmer-Hirschberg, “An Experimental Application of the Delphi Method to the Use of Experts,” Management Science, Vol. 9, Issue: 3 (April 1963) pp. 458- 467. 3 Darryl S. L. Jarvis, “Conceptualizing, Analyzing and Measuring Political Risk: The Evolution of Theory and Method,” Lee Kuan Yew School of Public Policy Research Paper No. LKYSPP08-004 (July 2008). William D. Coplin and Michael K. O'Leary, "Political Forecast For International Business," Planning Review, Vol. 11 Issue: 3 (1983) pp.14-23. The PRS Group, “Political Risk Services”™ (PRS) or the “Coplin-O’Leary Country Risk Rating System”™ Methodology. Daniel Kaufmann, Aart Kraay, and Massimo Mastruzzi, “The Worldwide Governance Indicators: Methodology and Analytical Issues,” World Bank Policy Research Working Paper No. 5430 (September 2010). 4 Scott R. Baker, Nicholas Bloom, and Steven J. Davis, “Measuring Economic Policy Uncertainty,” The Quarterly Journal of Economics, Volume 131, Issue 4, November 2016 (July 2016) pp.1593–1636. Dario Caldara and Matteo Iacoviello, “Measuring Geopolitical Risk,” Board of Governors of the Federal Reserve Board, Working Paper (January 2018). 5 Please see BCA Research Geopolitical Strategy Special Report, “Five Myths On Geopolitical Forecasting,” dated July 9, 2018, available at gps.bcaresearch.com. 6 Please see BCA Foreign Exchange Strategy Weekly Report, “Not Out Of The Woods Yet,” April 5, 2019, available at www.bcaresearch.com. Appendix Appendix France

France: GeoRisk Indicator

France: GeoRisk Indicator

Appendix U.K.

U.K.: GeoRisk Indicator

U.K.: GeoRisk Indicator

Appendix Germany

Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

Appendix Italy

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Appendix Spain

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Appendix Russia

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

Appendix Korea

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Appendix Taiwan

Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Appendix Turkey

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Appendix Brazil

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

What’s On The Geopolitical Radar?

Chart 19

Geopolitical Calendar

Highlights So what? Egyptian assets will benefit from improving fundamentals. Why? March credit data confirm China’s stimulus, supporting the commodity/EM complex. Oil price risks are also to the upside. In Egypt, investors will welcome constitutional changes that reinforce the regime and overall stability. Egypt is beginning to reap the rewards of painful IMF reforms enacted in late 2016. A large, under-invested labor market is a key structural risk that will weigh on Egypt’s long-term investment potential. We recommend an overweight stance in Egyptian sovereign (USD) bonds relative to EM. Feature Egypt is the world’s most populous Arab country and a geopolitical fulcrum at the critical juncture between Africa, Europe, and Asia. Its stability is particularly important at a time of rapid geopolitical change. The U.S. is deleveraging from the Middle East and regional powers are scrambling to fill the void. Popular discontent is toppling rigid authoritarian leaders, most recently in Algeria and Sudan. Displaced peoples have spilled into Europe in the recent past and could do so again if more regimes fail (Chart 1). In this week’s Special Report we take a close look at Egypt and show how its continued stabilization is a rare positive trend for the region and one that presents an investment opportunity in its own right. China’s March Credit data confirm that stimulus is surprising to the upside this year. Before proceeding, however, we make note of some key developments on the global front, especially our oil view: China’s Stimulus: China’s March credit data confirm that stimulus is surprising to the upside this year (Chart 2). The data will help galvanize expectations of firming global growth, supporting commodity prices and EM risk assets. We are long Chinese equities, Indonesian and Thai equities, and EM energy producer equities relative to the EM benchmark. Chart 1Asylum Seekers May Rise Amid Mideast Instability

Asylum Seekers May Rise Amid Mideast Instability

Asylum Seekers May Rise Amid Mideast Instability

Chart 2Chinese Credit Supports Economic Outlook

Chinese Credit Supports Economic Outlook

Chinese Credit Supports Economic Outlook

Iranian Sanctions: The Trump administration is increasing the pressure on Iran again and threatening to enforce sanctions strictly on oil exports. Exports have recovered somewhat since Trump issued waivers for key importers last fall and this means that 1.3mm bpd are still at risk if enforcement intensifies (Chart 3).

Chart 3

Libyan War: Libyan National Army leader, General Khalifa Haftar, has made a move for Tripoli after sweeping across the country’s south, jeopardizing the roughly 300,000 barrels per day exported from Zawiya, west of Tripoli. Egypt is one of Haftar’s geopolitical backers, along with the UAE, so Egypt’s improving domestic situation, discussed below, is a factor supporting Haftar’s ability to extend his control across western Libya, which poses a risk of unplanned oil outages this year. The combination of these factors will put upward pressure on oil prices in an environment where supplies are already limited. As a result, Bob Ryan, the head of BCA’s Commodity & Energy Strategy, believes that OPEC 2.0 will eventually follow Russia’s preferred path at this juncture and increase production. Russia and Saudi Arabia are comfortable with Brent crude above $70 per barrel, but will get nervous once prices rise above $80 and threaten to kill demand in emerging markets. An alteration of slated production cuts has not yet been agreed and prices remain well supported in the meantime, with Brent on track to average $75 per barrel in 2019 and $80 in 2020.1 We do not expect President Trump to impose “maximum pressure” on Iran in this context. We have long assumed the worst of Venezuelan production, i.e. that it will at least be cut in half to 500,000 bpd by end of year, and possibly fall to zero. Libyan outages could theoretically rise to the full 900,000 bpd, though the likely cap is 300,000 bpd. The removal of 1.3mm bpd of Iranian barrels would bring the combined production losses close to OPEC 2.0’s spare capacity of around 2.1mm bpd. Moreover, the Iranians have the ability to retaliate, which jeopardizes other output across the Middle East. The United States has a valuable tool in the Strategic Petroleum Reserve.2 But President Trump would still be taking an enormous risk with the economy in advance of an election year to enforce the maximum sanctions on Iran. So we maintain that he will largely keep the waivers in place on May 2. The real danger, from our point of view, comes if Trump is re-elected, as then he will be less constrained both politically (no chance of reelection) and economically (U.S. production going up) in pursuing his hawkish foreign policy against Iran. But that is a story for 2021. With that, we turn to Egypt. A Dream Deferred Earlier this year, the Egyptian parliament voted in favor of a series of proposed constitutional amendments that will further consolidate President Abdel Fattah al-Sisi’s power. Among the changes are the extension of the president’s term, allowing him in principle to rule for another 15 years. The proposed amendments will also expand the role of the military, enshrining a political role for it, thus solidifying its already preeminent position in Egyptian politics.3 These proposed changes bring the de facto Egyptian political environment close to its pre-2011 state – that is, the state of affairs before an estimated two million Egyptians rose in protest at Tahrir Square and removed President Hosni Mubarak from power, setting in motion a tumultuous decade. Sisi supporters argue that these changes will guarantee much needed stability and policy continuity to the Egyptian economy, allowing it to regain its footing. With GDP growth expected to near 6% by the middle of next year – the strongest since the 2011 revolution – it is no surprise that the aspirations of Egypt’s revolutionaries have become a dream deferred. Chart 4Improving Fundamentals Bode Well For Egyptian Equities

Improving Fundamentals Bode Well For Egyptian Equities

Improving Fundamentals Bode Well For Egyptian Equities

Instead, policymakers and ordinary citizens alike have focused on making ends meet – both in terms of the fiscal purse and the household bank account. Policy continuity is what is required for Egypt at this point in time: It is finally beginning to reap the rewards of the painful reforms enacted in late 2016 as part of the IMF program. Sisi’s own position is reinforced by the fact that he oversaw this process and has come out on the other side. While the proposed constitutional amendments will pass, and will be characterized as a step back into authoritarian rule, the stability will be favorable for investors, as it will support a more predictable near-term trajectory for the Egyptian economy. Egyptian assets have already started to reflect this reality, signaling that Egypt is transitioning into a new era that portends a more attractive investment climate. As such, Egyptian equities have picked up and have outperformed the broader EM index since December (Chart 4). Bottom Line: “Stability” is the catch-phrase of the Sisi regime. Constitutional amendments allowing the Egyptian president and military to amass far-reaching powers are likely to pass. While they mark a return to Egypt’s traditional authoritarian system, this will be welcomed by foreign investors who were otherwise hesitant to re-enter the Egyptian market during the turbulent aftermath of 2011 Egypt’s 2016-2019 Policy Mantra: No Pain, No Gain Since the 2011 revolution, the Egyptian economy has been defined by years of turmoil. The popular uprising and ensuing loss of security drove away tourists and foreign investors – key sources of hard currency – causing the central bank to chew through its foreign exchange reserves as it scrambled to stabilize confidence and the currency. High rates of poverty, unemployment, and inequality amid a growing public sector wage bill, over reliance on food imports and an overvalued currency were a recipe for an economic disaster. Public debt ballooned while the black market for foreign exchange thrived. Thus, the structural reforms (Box 1) that accompanied the November 2016 $12bn IMF loan – while painful – were necessary to transition the economy onto a more sustainable trajectory. Box 1 Structural Reforms Implemented Since 2016 The reforms that accompanied the IMF program are designed to improve fiscal consolidation, liberalize the foreign exchange market, and create a more business friendly investment climate. They include the following measures: The floating of the currency in November 2016 which resulted in the Egyptian pound losing half its value relative to the dollar. Given that Egyptians rely on imports for a large chunk of their consumption, the impact on household budgets and consumer prices have been massive (Chart 5). However, the inflation rate has since slowed to 14.4%, with the Central Bank of Egypt (CBE) targeting single-digit inflation by the end of next year. Similarly, it has stabilized the EGP/USD.4 Reductions to fuel subsidies have weighed on consumer expenditures. The target is full-cost recovery by the end of 2018-19 for almost all fuel products (except LPG and fuel oil used in bakeries and electricity generation). The introduction of a value-added tax (VAT) of 13% in 2016, which subsequently rose to 14%. The VAT will help generate revenue, by replacing the distortionary sales tax and broadening the tax base. Basic goods and services are exempt from the VAT in order to shield the poor from rising living costs. A reduction in utility subsidies to reduce state spending and instead channel funds to more productive uses. Authorities target the full elimination of electricity subsidies by 2020-21. Similarly, water and sewage subsidies have been cut. As of December 2018, Egypt ended a discounted customs exchange rate for non-essential imports. The monthly fixed customs exchange rate was introduced in 2017, following the 2016 currency devaluation, offering a favorable exchange rate to importers. In the second half of last year, the customs exchange rate was set at 16 EGP/USD while the market rate was EGP/USD 17.82-17.96. The non-essential imports include tobacco products, alcohol, pet food, and cosmetics. Other goods that will also be subject to the market rate include mobile phones, computers, furniture, shoes, cars, and motorbikes. The elimination of the repatriation mechanism for new inflows. The repatriation mechanism guaranteed the availability of foreign exchange for capital repatriation to portfolio investors that chose to sell foreign exchange to the central bank. Its elimination means that cash inflows and outflows by foreign portfolio investors will now impact the supply and demand of foreign currencies in the market. A new investment law was enacted in July 2017, which aims to promote domestic foreign investments by offering incentives and reducing bureaucracy. A new bankruptcy law was enacted in January 2018. Egypt ranks 101 out of 168 in the “Resolving Insolvency Index” of the Doing Business report. The law simplifies post-bankruptcy procedures and aims to reduce the need for companies to resort to courts in the case of bankruptcy. It also removes investment risk by abolishing imprisonment in bankruptcy cases. Chart 5FX Reform Was Inflationary

FX Reform Was Inflationary

FX Reform Was Inflationary

To mitigate the impact of these changes, especially on the lower and lower-middle income brackets, social programs have been expanded and improved, including: Takaful and Karama: An expansion of the cash transfer program, which now targets more than 10 million people, or ~10% of the population. Forsa: A program that helps create job opportunities for underprivileged youth by focusing on employment training. Mastoura: A program that lifts living standards and provides economic empowerment for Egyptian women by supplying microloans to fund projects. Sakan Karim: A program that aims to improve housing conditions of the poor by promoting access to clean drinking water and sanitation. Together, the structural reforms and targeted social programs will support the Egyptian economy by strengthening the business climate, attracting investment, and increasing employment. Since the beginning of the program, the country’s fiscal arithmetic has improved, inflation has been contained, and foreign exchange is no longer scarce. As a result, investor confidence has picked up. With the final $2bn tranche of the loan expected to be dispersed in the middle of 2019, the onus now lies on Egyptian policymakers to keep up the momentum. Bottom Line: With the IMF program now winding down, the continuity of reform implementation is squarely on the back of policymakers. With further structural policies in the pipeline, we expect policymakers to build on the macroeconomic gains of the past few years. Reaping The Rewards The most evident improvement following the reforms is seen in the fiscal purse. For the first time in over a decade, the primary balance is in surplus (Chart 6). The improvement reflects lower government spending commitments on the back of fiscal consolidation (Chart 7). Nevertheless, revenues remain weak, despite the implementation of the VAT, implying a need to improve tax collection and boost aggregate demand to raise taxable revenues. Chart 6Improving In Fiscal Arithmetic...

Improving In Fiscal Arithmetic...

Improving In Fiscal Arithmetic...

Chart 7...On Back Of Fiscal Consolidation

...On Back Of Fiscal Consolidation

...On Back Of Fiscal Consolidation

As policymakers continue reforming budgetary allocations, we expect the primary surplus to remain intact. This will alleviate some of the pressure on the overall budget, which, while still in deficit, has improved substantially. With the final $2bn tranche of the loan expected to be dispersed in the middle of 2019, the onus now lies on Egyptian policymakers to keep up the momentum. Nevertheless, the stock of public debt – whilst declining – remains elevated and will continue weighing on the overall budget (Chart 8). This is especially problematic for fiscal arithmetic since domestic interest rates are in the double digits and interest payments will tie down roughly half of government revenues. A combination of improving potential GDP, falling domestic interest rates, and continued prudence on debt is needed to stabilize Egypt’s debt dynamics. In fact, with the decline in both headline and core inflation, the Central Bank of Egypt has already embarked on a monetary easing cycle, cutting rates by 300 basis points since the beginning of last year (Chart 9). Although interest rates remain extremely high, lower borrowing costs will not only improve debt dynamics on the margin, but also encourage private sector credit, thus raising aggregate output and revitalizing domestic investment. Chart 8Debt Remains A Burden

Debt Remains A Burden

Debt Remains A Burden

Chart 9Continued Easing Will Boost Outlook

Continued Easing Will Boost Outlook

Continued Easing Will Boost Outlook

While inflation may accelerate in the coming months – on the back of a seasonal uptick in food prices during the month of Ramadan and the further removal of subsidies – we expect further cuts by the CBE in 2H2019 and 2020. Falling real wages due to fiscal consolidation also point to lower inflationary pressures (Chart 10). Unless Egypt manages to stabilize its debt dynamics, it will once again be forced to resort to debt monetization, which bodes ill for the currency as well as for inflation. The evidence to date points to an improvement (Chart 11). Chart 10Inflationary Pressures Are Contained

Inflationary Pressures Are Contained

Inflationary Pressures Are Contained

Along with the improvement in the fiscal account, Egypt’s external deficit has also narrowed on the back of the improvement in the macroeconomic climate (Chart 12). The contraction in the current account deficit has been bolstered by an expansion in exports, which grew more than 10% in 2018. Chart 11Authorities Resisting Urge To Monetize Debt

Authorities Resisting Urge To Monetize Debt

Authorities Resisting Urge To Monetize Debt

Chart 12External Deficit Contracting

External Deficit Contracting

External Deficit Contracting

Chart 13Natural Gas Exports Will be Supportive

Natural Gas Exports Will be Supportive

Natural Gas Exports Will be Supportive

Notably, the energy trade balance has benefitted from an increase in Egypt’s natural gas potential (Chart 13). The giant Zohr field – the largest gas discovery ever made in the Mediterranean – came on stream in December 2017, and will support Egypt’s self-sufficiency in gas after falling domestic production forced Egypt to cut most LNG exports in 2014. The location of the gas field also presents opportunities for Egypt to become a natural gas export hub in the region. The Zohr field is close to other major fields in Israel and Cyprus, which means economies of scale can be utilized in developing regional export infrastructure. Egypt’s LNG export plants in Damietta and Idku have a capacity of 19 billion cubic meters (bcm) per year, which have been mostly idle in recent years. Already, an agreement between Egypt and Cyprus this past December committed to the construction of a pipeline connecting the Aphrodite gas field to Egypt’s LNG facilities. Similarly, a rebound in revenues from tourism to near-pre-crisis levels has helped improve the external account (Chart 14). Going forward, we expect the decline in terrorism to support the rebound of foreign inflows from tourism (Chart 15). This will be a non-negligible source of cash as tourism now accounts for roughly half of all service receipts, up from less than a quarter just three years ago. However, given that the security situation is unpredictable, this sector remains vulnerable to downside risks. Chart 14Rebound In Tourism...

Rebound In Tourism...

Rebound In Tourism...

Chart 15

Another supportive source of inflows has been remittances from Egyptians living abroad. These continue to grow at a double-digit rate (Chart 16). Chart 16Recovery In Remittance Inflows

Recovery In Remittance Inflows

Recovery In Remittance Inflows

Chart 17Foreign Investment Will Be Supported...

Foreign Investment Will Be Supported...

Foreign Investment Will Be Supported...

However, the financial account has taken a hit recently as inflows from portfolio investments have come down quite sharply on the back of investor aversion to emerging markets last year (Chart 17). Given the Fed’s pause, China’s stimulus, and other factors, we expect a pickup in portfolio investment. What’s more, Egyptian authorities have been working on improving the business environment, reflected in Egypt’s rising rank in the ease of doing business and global competitiveness surveys (Chart 18). This should improve foreign direct investment, which remains relatively weak so far.

Chart 18

Chart 19Build Up In Central Bank Reserves

Build Up In Central Bank Reserves

Build Up In Central Bank Reserves

Of course, despite these improvements, Egypt still ranks relatively low on these measures. Thus continued efforts to improve the business environment will be necessary to make Egypt an attractive destination for businesses. Yet Egypt’s foreign reserves have picked up considerably, and more importantly its net reserves – which exclude the CBE’s foreign borrowings – have once again turned positive (Chart 19). Bottom Line: The rewards from Egypt’s structural reforms are evident in the improvements to its twin deficits. While continued policy prudence is necessary to maintain the momentum of these policies, we expect the EGP/USD to remain flattish for the remainder of the year. We expect continued policy easing as the CBE cuts rates at least one more time in the second half of the year on the back of slowing inflation. Ghosts Of Futures Past Political stability and an improvement in macroeconomic indicators will no doubt be supportive of the Egyptian economy and assets in the near term. However, several structural risks remain, and could derail its performance down the road. For one, Egypt remains heavily reliant on its external environment. This environment has been largely cooperative throughout Sisi’s term in office, but a global or EM downturn could cause investment to collapse. Meanwhile the cyclical rise in oil prices will weigh on the import bill and raise headline inflation. Improvements in the business environment should attract foreign directinvestment. Second, a rising dependency ratio will pose a burden on Egypt in the coming years (Chart 20). Furthermore, elevated female and youth unemployment keep the output gap wide. True, the current improvement in the overall labor market will help the country weather the demographic headwind. However, another chronic problem is the quality of the Egyptian labor market. The latest data from the World Bank shows that government spending on education is significantly lower than it is among EM peers (Chart 21). Similarly, health expenditure per capita has not picked up much in recent years and has actually fallen as a share of GDP. Chart 20Demographic Challenges Remain

Demographic Challenges Remain

Demographic Challenges Remain

Chart 21

This has manifested in relatively low labor productivity and highlights the need for investment in human capital to improve potential GDP and the necessity for funds to be channeled to these sectors. Fortunately, the reforms have freed up badly needed fiscal space for now. Another key concern is the bloated economic role of the state and military. This is a double whammy to the Egyptian economy as it reduces fiscal funds available for other uses, such as healthcare and education while constraining the private sector. The crowding out of the private sector is evident from the recipients of bank credit: loans to the government – beyond purchases of government securities – are growing at by nearly 50% y/y, while lending to other sectors is expanding at less than 15% y/y (Chart 22). Once again, however, there is evidence of improvement: bank investments in government securities have come down from their peak and now represent roughly a third of total bank assets (Chart 23). Accordingly, credit to the private sector has likely bottomed. Chart 22Private Sector Crowding Out Remains...

Private Sector Crowding Out Remains...

Private Sector Crowding Out Remains...

Chart 23...But Signs Of Improvement

...But Signs Of Improvement

...But Signs Of Improvement

One structural concern that is here to stay is the fact that the Egyptian military occupies an oversized share of the economy. Given that all companies of the Egyptian armed forces are exempt from taxes, they have an unfair advantage over the private sector. The military has an especially large presence in Egypt’s recent infrastructure mega-projects. These include $8.2 billion invested in an expansion of the Suez Canal as well as the construction of a new administrative capital, 45 km to the east of Cairo. The military budget is secret and connected industries are not subject to auditing. Preferential treatment in assigning government contracts and the ability to offer services at a cheaper rate have further expanded the military’s role in the economy. Bottom Line: Risks to our optimistic outlook on Egypt mostly come from any deterioration in the external environment. The Egyptian economy is also weakened by structural weaknesses such as a large, under-invested labor market. These structural risks are considerable and will weigh on the long term investment potential of Egypt. In the short term, however, Egypt appears to be a lucrative trade opportunity. Investment Implications Egyptian sovereign spreads will likely contract going forward on the back of an improvement in the economic outlook (Chart 24). Thus, we recommend an overweight stance in Egyptian sovereign bonds within the EM space. Chart 24Improved Fundamentals A Positive For Sovereign Bonds

Improved Fundamentals A Positive For Sovereign Bonds

Improved Fundamentals A Positive For Sovereign Bonds

Chart 25Equities Still Attractive

Equities Still Attractive

Equities Still Attractive

In the equities space, Egypt’s valuations look attractive relative to their Emerging Market and Frontier Market peers (Chart 25), despite the recent rally in recognition of the stability we outline here. Matt Gertken, Vice President Geopolitical Strategist mattg@bcaresearch.com Marko Papic Consulting Editor marko@bcaresearch.com Footnotes 1 Please see BCA Commodity & Energy Strategy Weekly Report, “Sussing Out OPEC 2.0’s Production Cuts, U.S. Waivers On Iran Sanctions,” April 11, 2019, available at www.bcaresearch.com. 2 The U.S. Strategic Petroleum Reserve (SPR) was created in 1975, in the wake of the Arab oil embargo, to protect the U.S. from supply disruptions. Faced with a “severe energy supply interruption” the U.S. president can authorize a maximum drawdown of 30 million barrels within a 60-day period, beginning 13 days after the decision. Notably, the SPR was tapped for 21 million barrels in 1990-91, during the Iraqi invasion of Kuwait, and for 30 million barrels in 2011, when Libyan production fell to zero amid the revolution. The current inventory is 649 million barrels of sweet and sour crude, which could last the U.S. 114 days of crude imports. As U.S. net oil imports decrease, the length of time that the SPR could substitute for net imports rises. 3 The Egyptian parliament voted in favor of the proposed changes on April 16. The changes will be put to a public referendum – as early as next week – before taking effect. The amendments seek to (1) extend presidential terms from four to six years, (2) permit President Sisi to run again after his current term ends in 2022 – as an exceptional case, (3) allow the president to select the heads of judicial bodies and to oversee a new council responsible for judicial affairs, and (4) enshrine in the constitution a political role for the army to preserve the constitution, democracy and – ironically – the civilian nature of the country. 4 The most recent appreciation this year raised fears that the CBE is once again intervening in the currency market through state-owned banks.

Highlights Evidence continues to mount that the Chinese economy is in a bottoming process. This suggests the path of least resistance for the RMB is up. Meanwhile, as the U.S. and China move closer to a trade deal, any geopolitical risk premium in the RMB will slowly erode. The ultimate catalyst for CNY longs will be depreciation in the U.S. dollar, which we believe is slowly underway. The ECB is turning more dovish at a time when euro area growth is hitting a nadir. This will be bullish for the euro beyond the near term. Our limit buy on the pound was triggered at 1.30. Target 1.45 with stops at 1.25. With the Aussie dollar close to the epicenter of Chinese stimulus, data down under is increasingly stabilizing. We are closing our short AUD/NOK position for a small profit. Feature Chart I-1The Chinese Yuan Is Pro-cyclical

The Chinese Yuan Is Pro-cyclical

The Chinese Yuan Is Pro-cyclical