Fixed Income

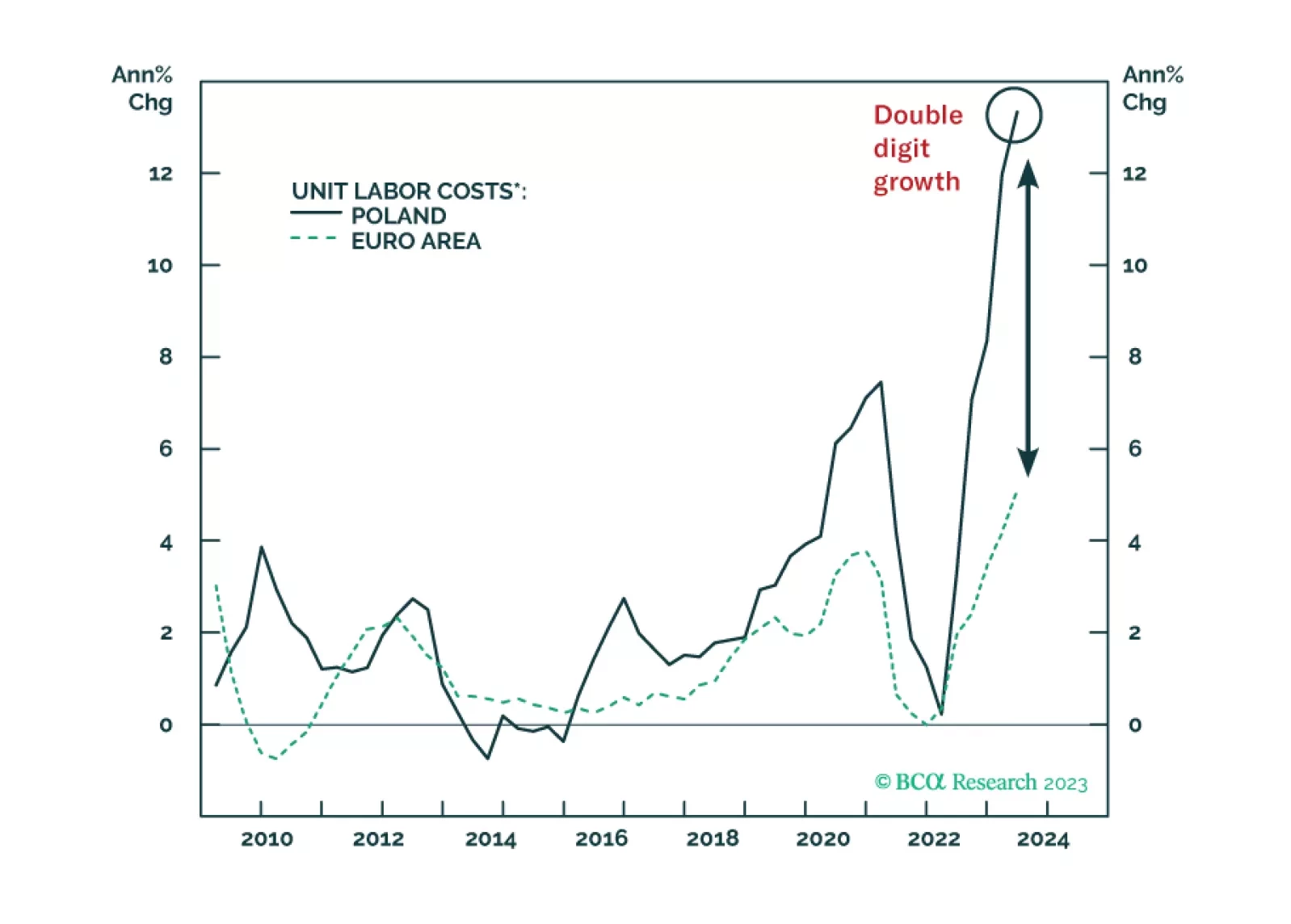

Poland’s inflation will stay elevated. And yet, its return to the European mainstream has improved its financial market outlook. Accordingly, we are recommending new trades on Polish equity, fixed income, and currency.

The soft-landing narrative has gotten nowhere at BCA but appears to be making some headway with broker-dealers and investors. We are preparing to lean against it once it pushes equity prices a little higher.

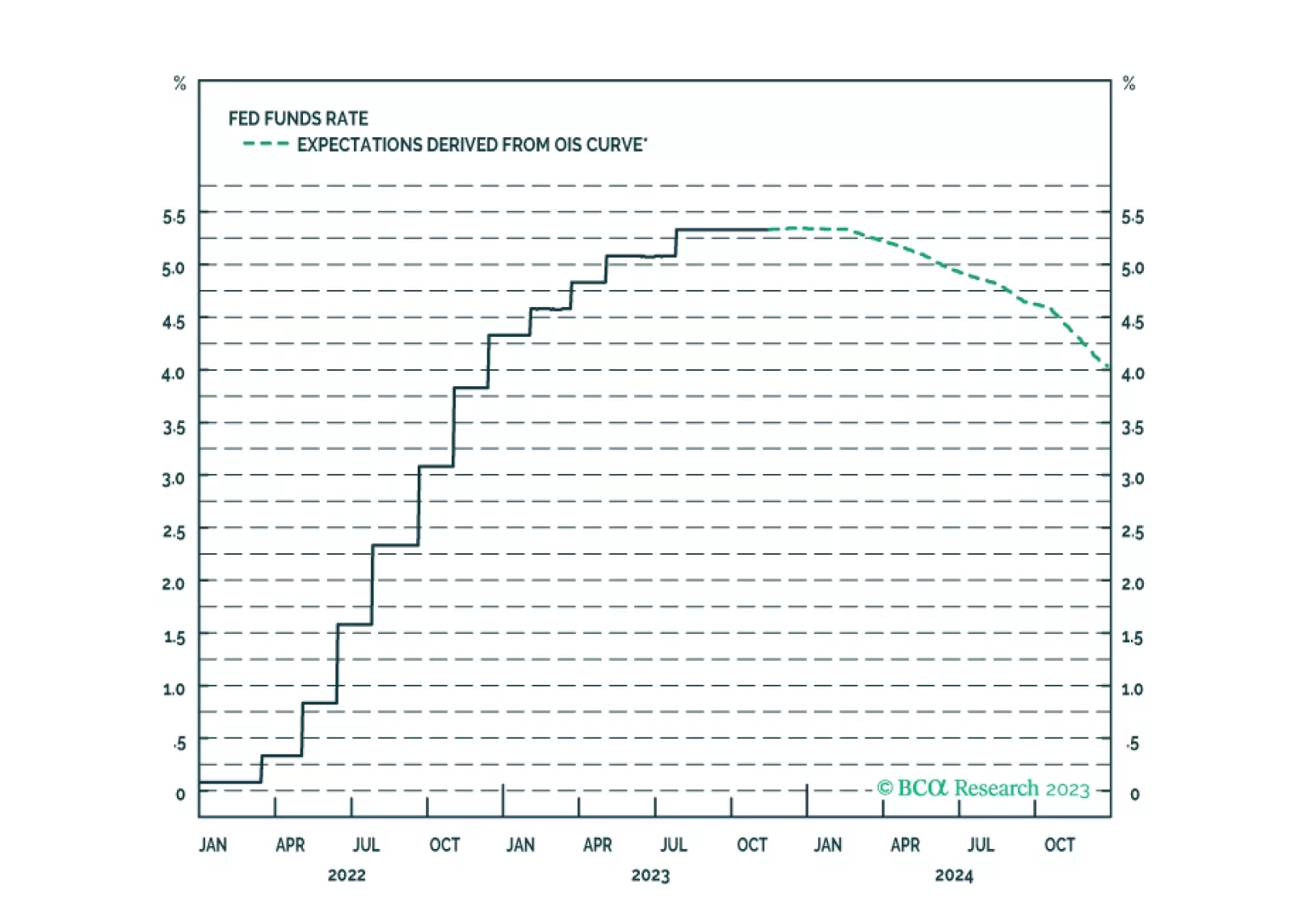

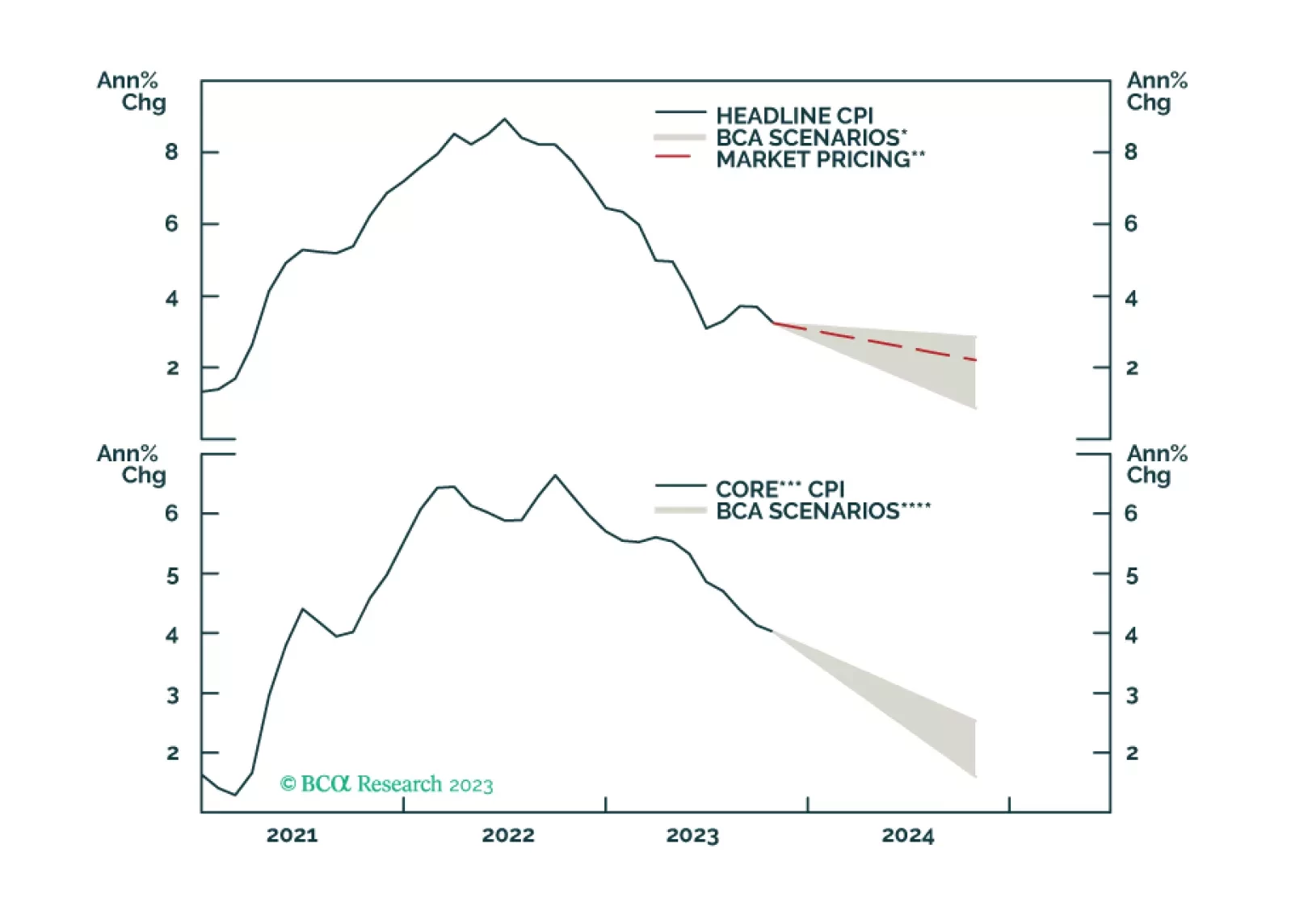

This week’s Special report revisits our TIPS Golden Rule. We provide a 12-month inflation forecast and discuss how it impacts our TIPS view.

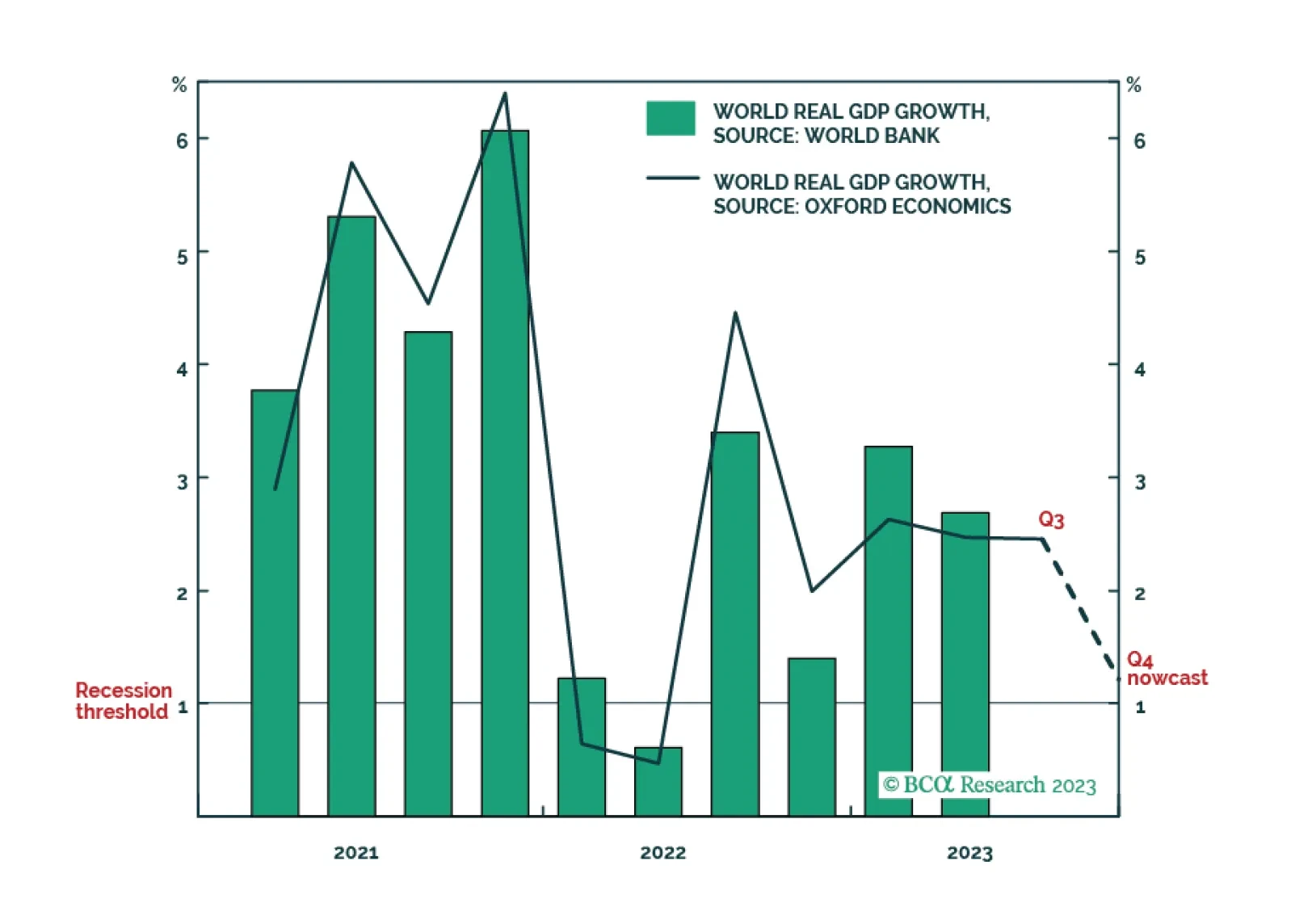

The latest ‘nowcast’ for world economic growth in the fourth quarter has plunged to just 1.2 percent, marking the cusp of another world recession. One important implication is that expectations for oil demand growth and industrial metal demand growth are way too optimistic.