Fixed Income

The risk of a recession in 2023 is being supplanted by the risk of another inflation wave. We will turn more defensive on equities if it continues to look like inflation is making a comeback.

Core CPI rose sequentially in January compared to December, but we don’t see this as the beginning of a new trend. Disinflation is very much still in the cards for the US economy between now and the end of the year.

Thai stocks and currency will weaken over the short term. And yet EM equity portfolios should overweight Thailand as tourism revivals will rejuvenate this economy.

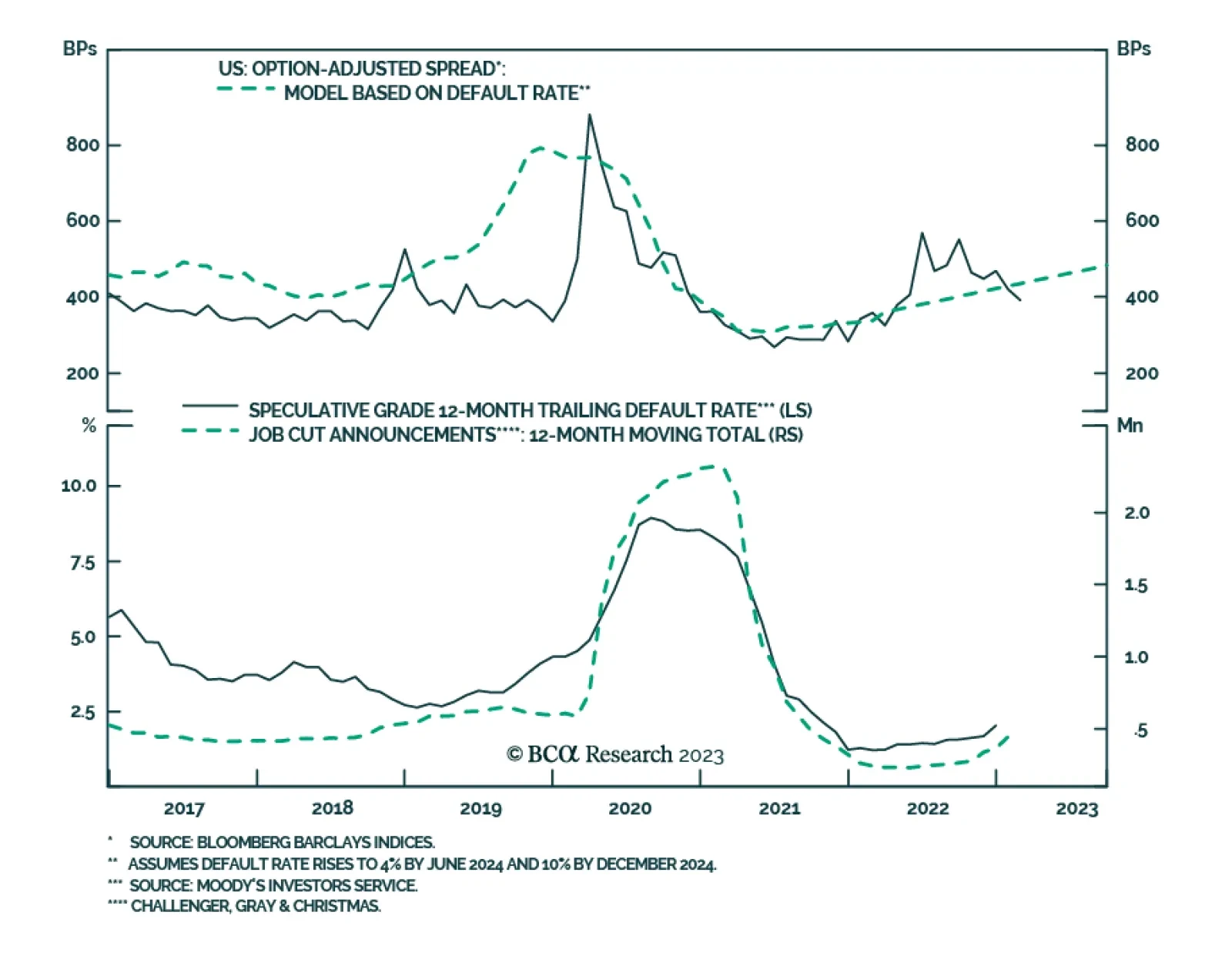

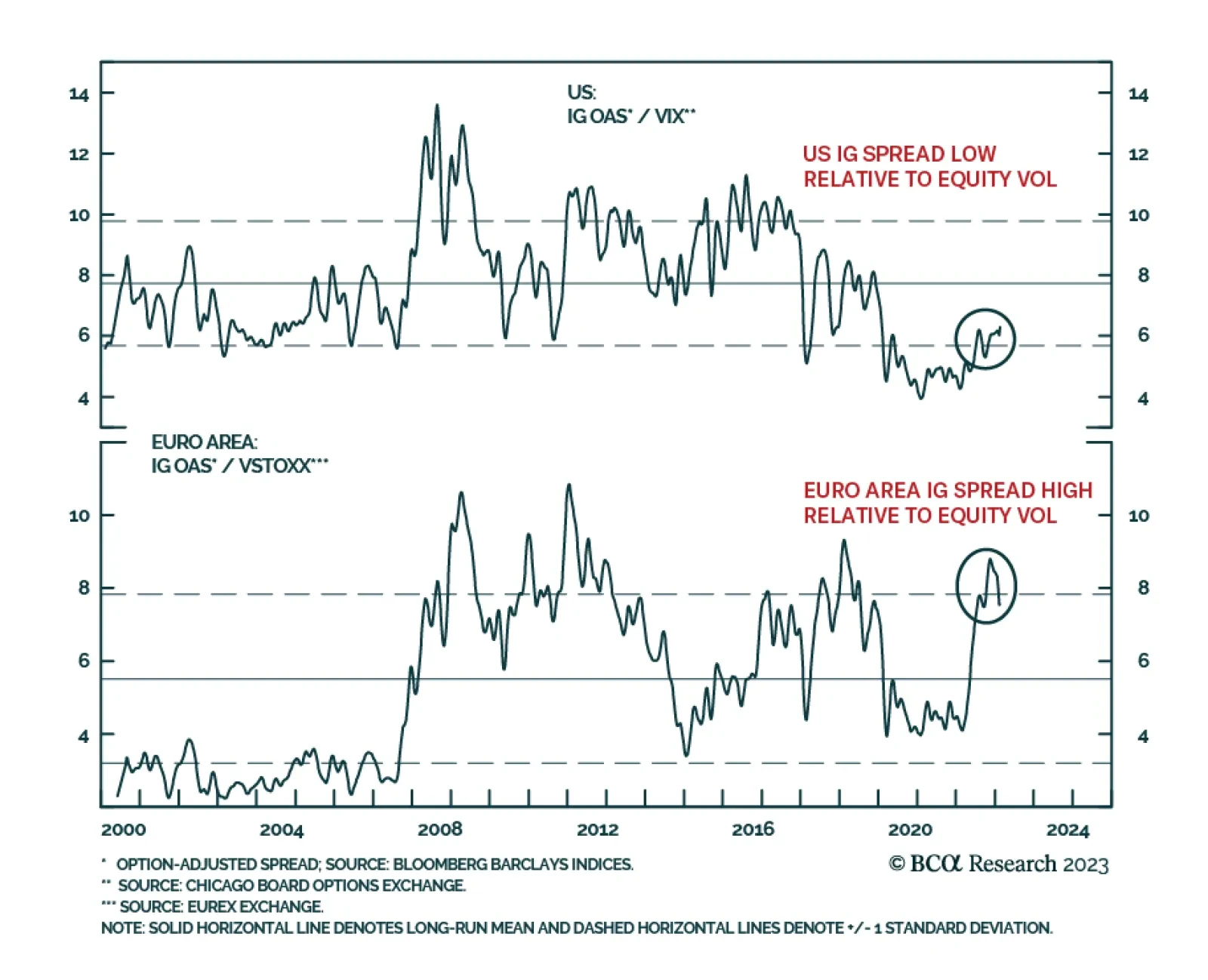

The backdrop for corporate bonds is turning more risky after the spread tightening seen over the past few months in the US and Europe. A tour of our favorite corporate spread valuation metrics on both sides of the Atlantic suggests a worsening cyclical risk/reward tradeoff for both investment grade and high-yield bonds, especially in the US.

We discuss the outlook for the Fed’s balance sheet and why QT is likely to continue for at least another year.

Our Central Bank Monitors support the recent shift in tone from central bankers in Europe. Find out what it means for European fixed-income portfolio allocation.

Ironically, increased confidence that the economy can withstand higher bond yields may be necessary to lift yields to a level that is actually detrimental to growth. Thus, until more investors are convinced that a recession will be averted, a recession will be averted. Remain tactically bullish on stocks for now. A more defensive posture will likely be necessary later this year.