Equities

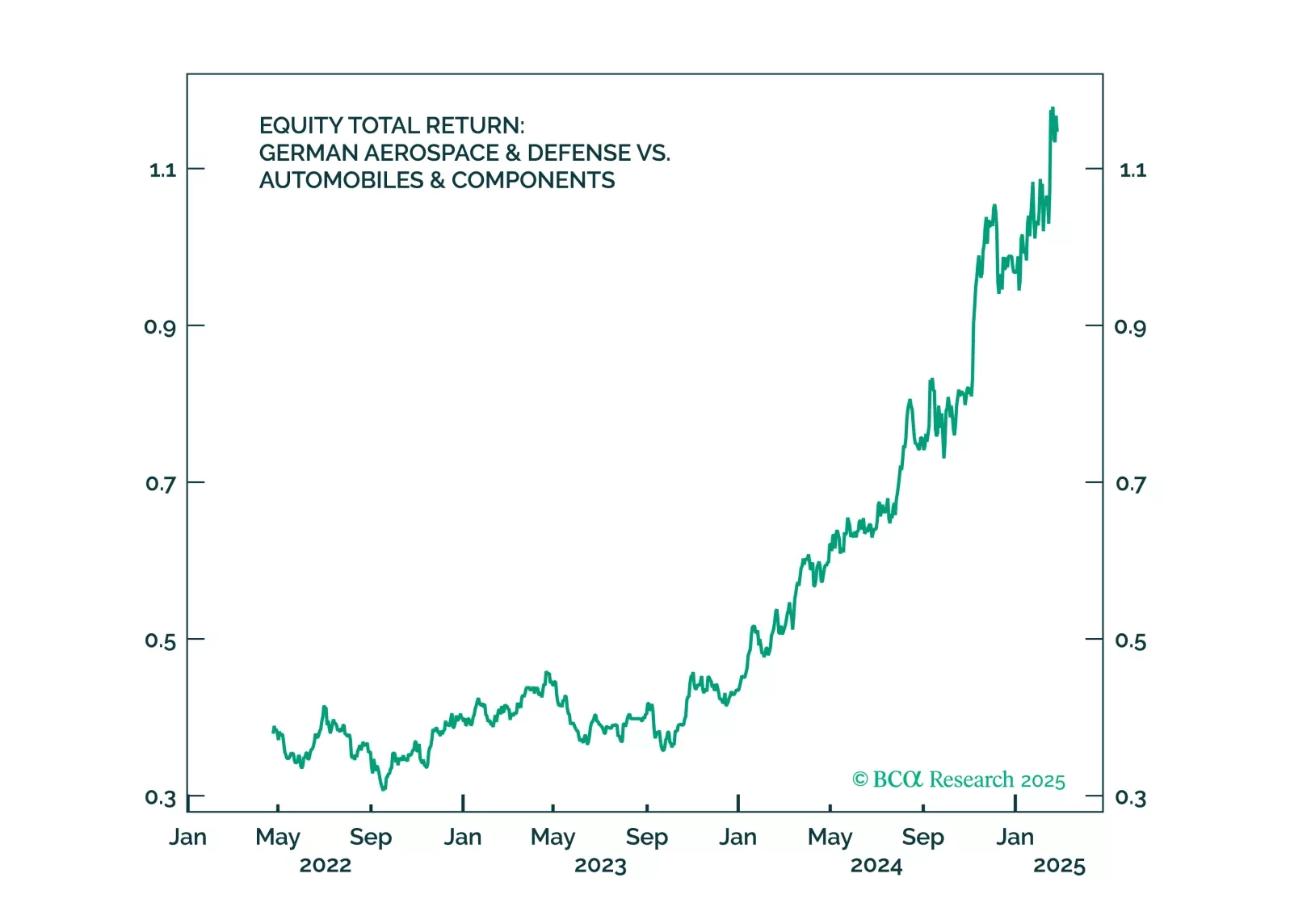

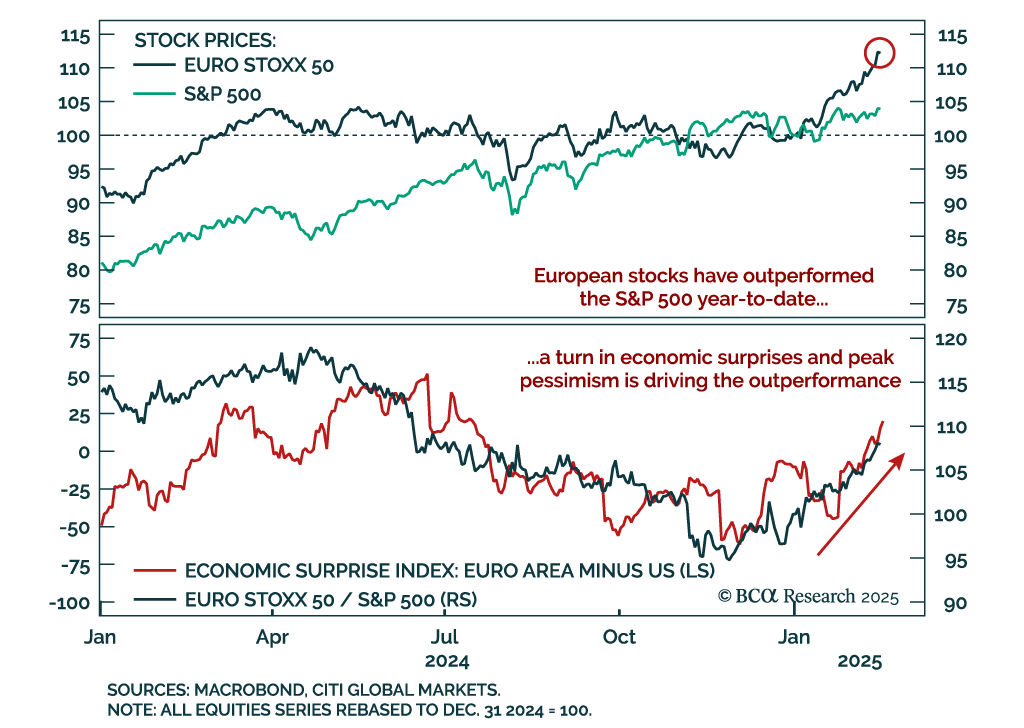

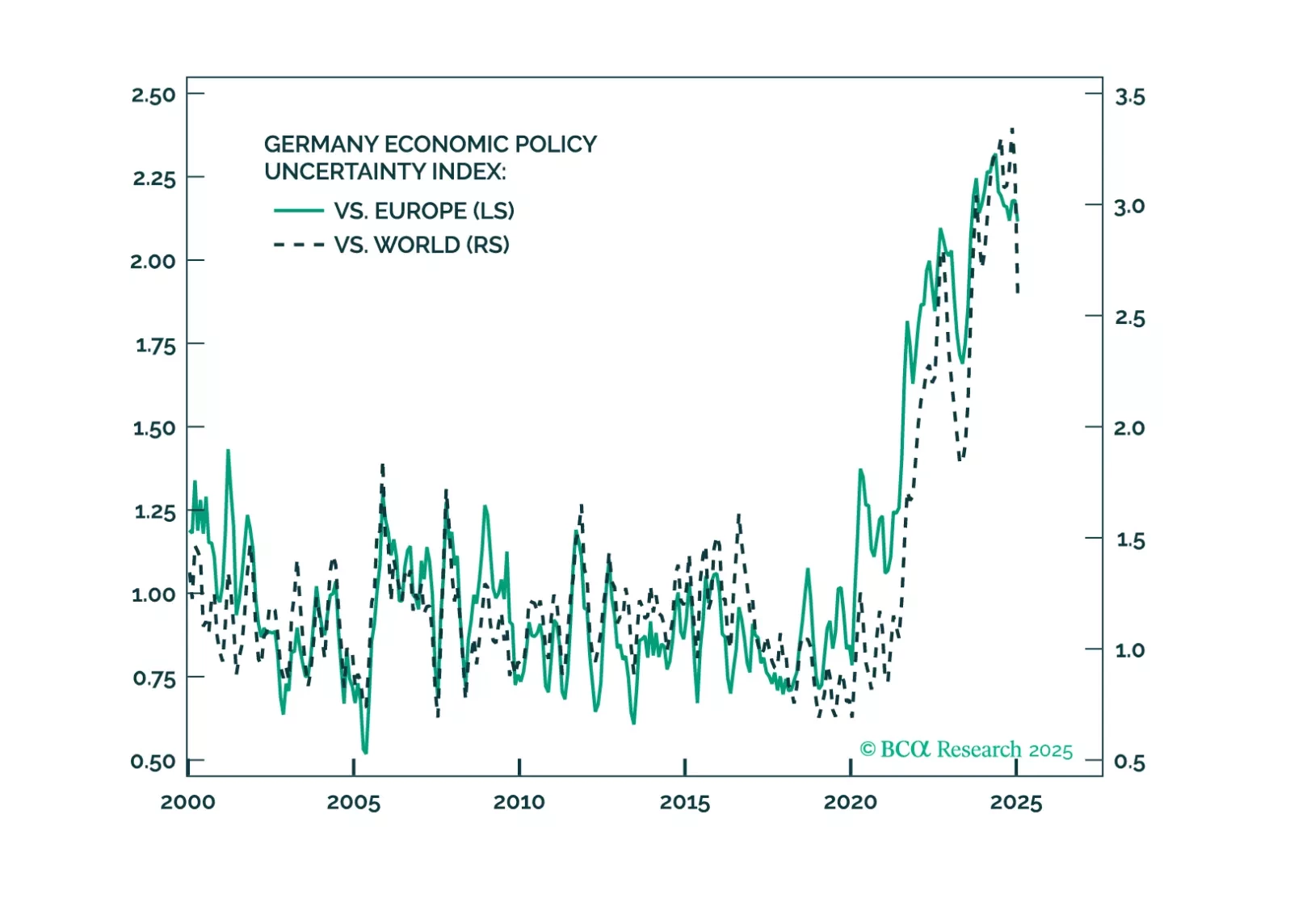

Trump’s ceasefire talks are positive for Germany – and so was the German election result. But Trump’s tariffs will hit Germany soon. Investors should use near-term volatility to increase exposure to Germany.

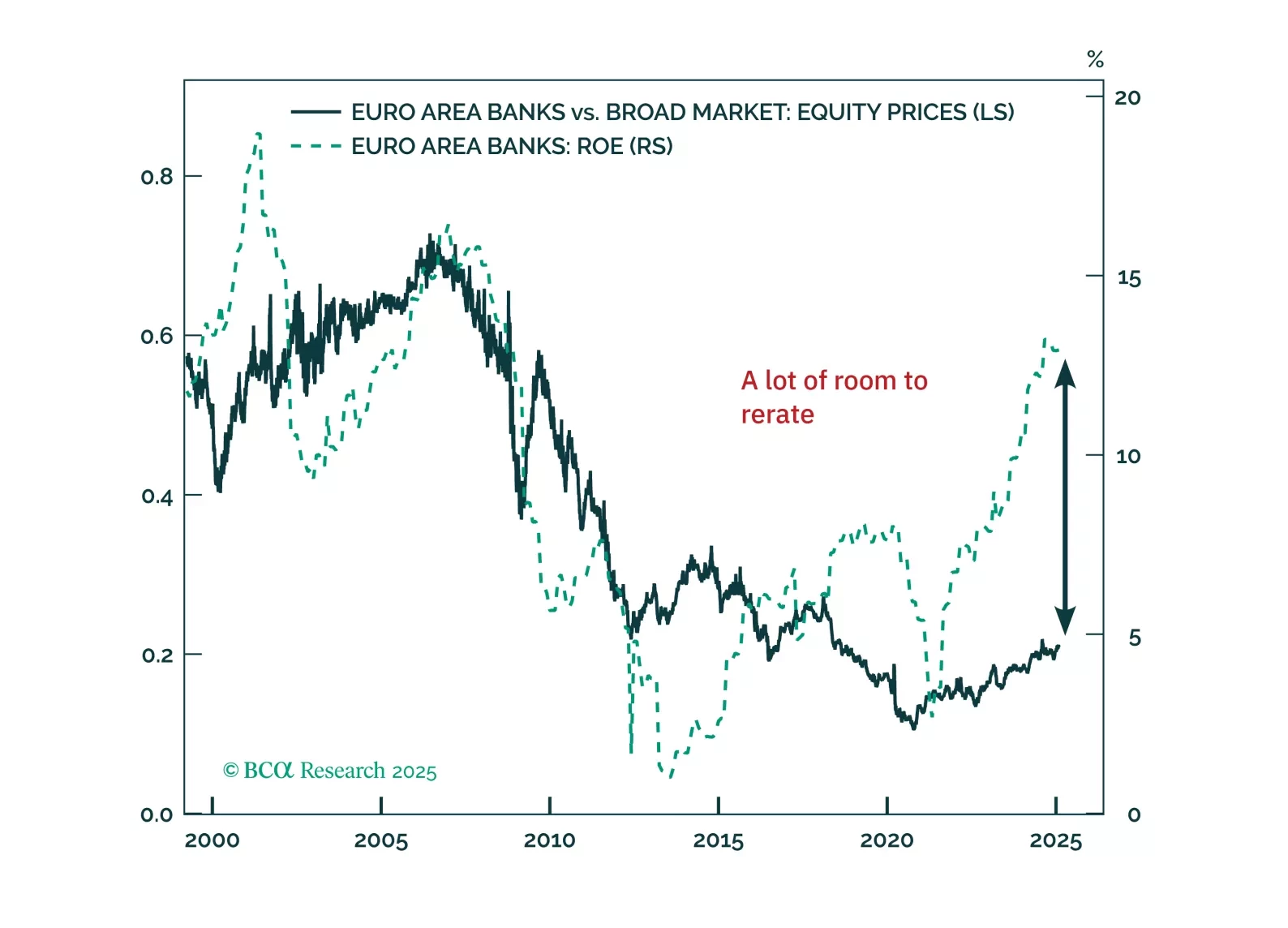

Eurozone banks have quietly outpaced the Magnificent 7—can they keep winning? With strong balance sheets, rising profitability, and structural tailwinds, European lenders still offer value despite short-term risks. Meanwhile, German equities continue to defy expectations, but is a near-term pullback on the horizon?

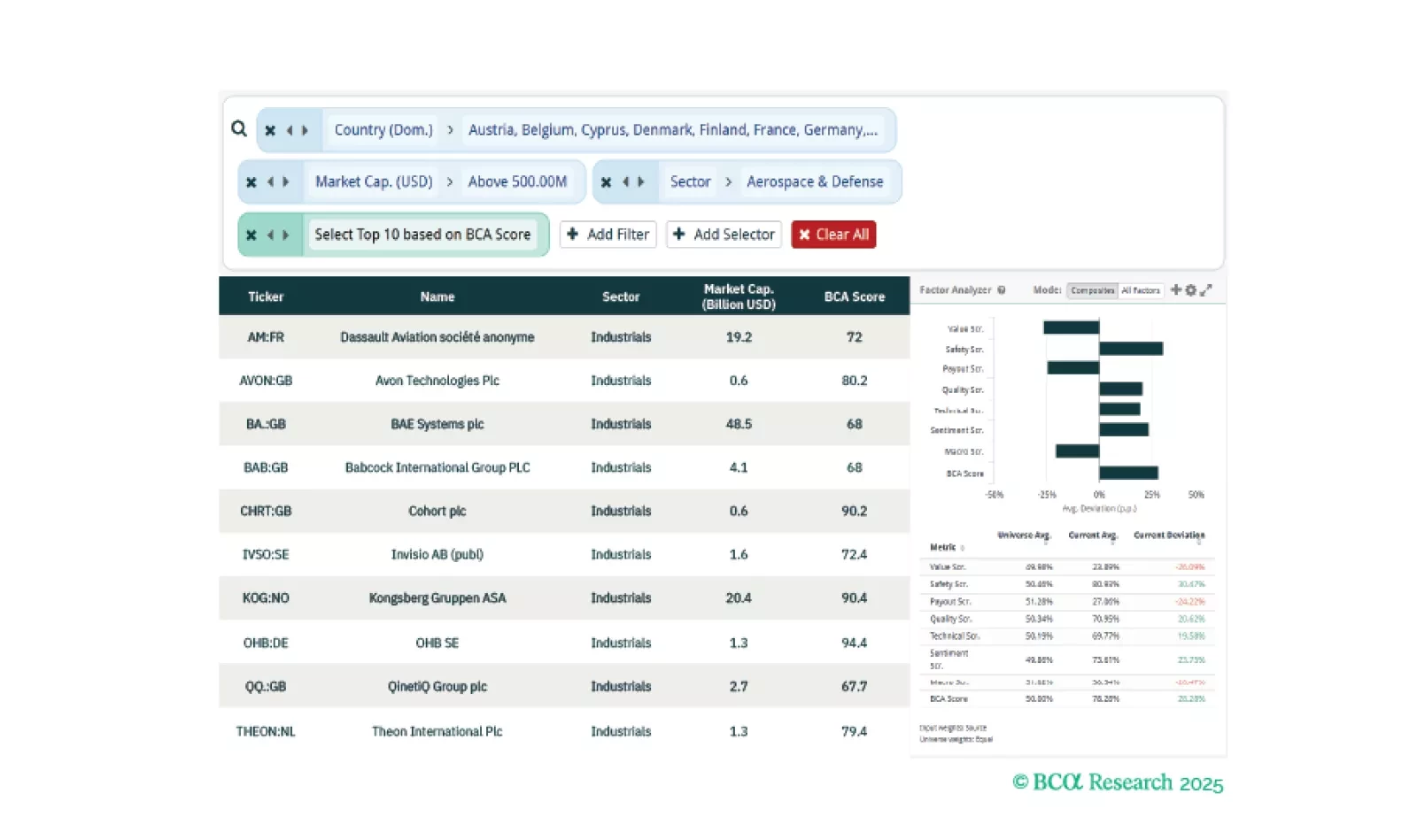

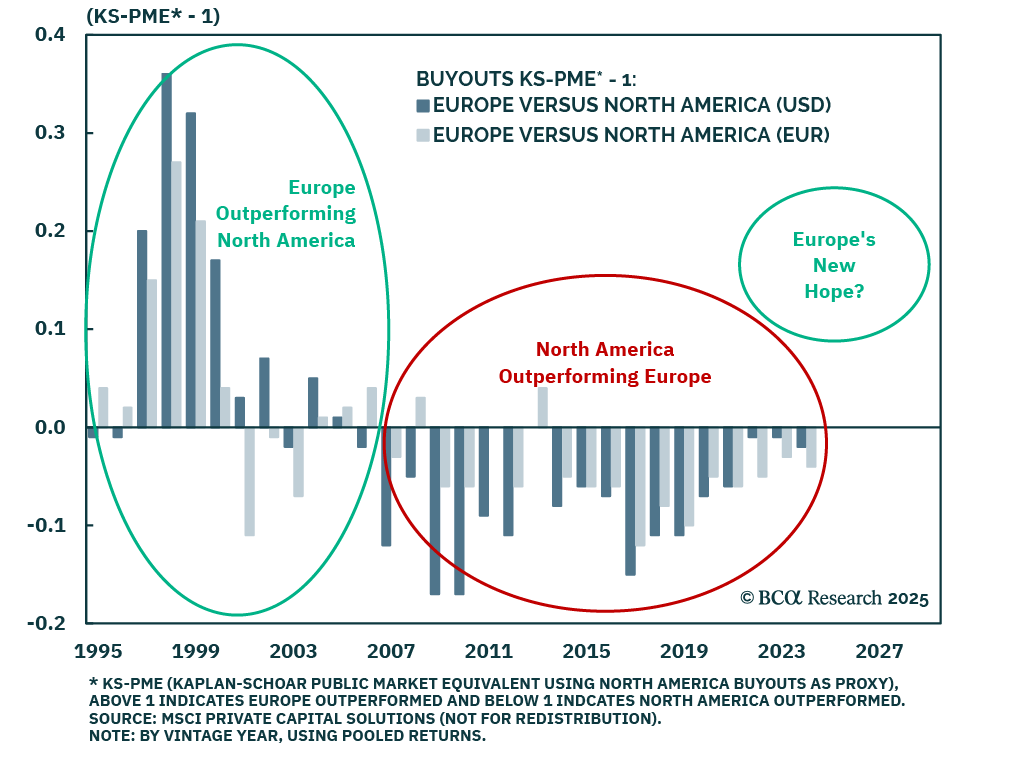

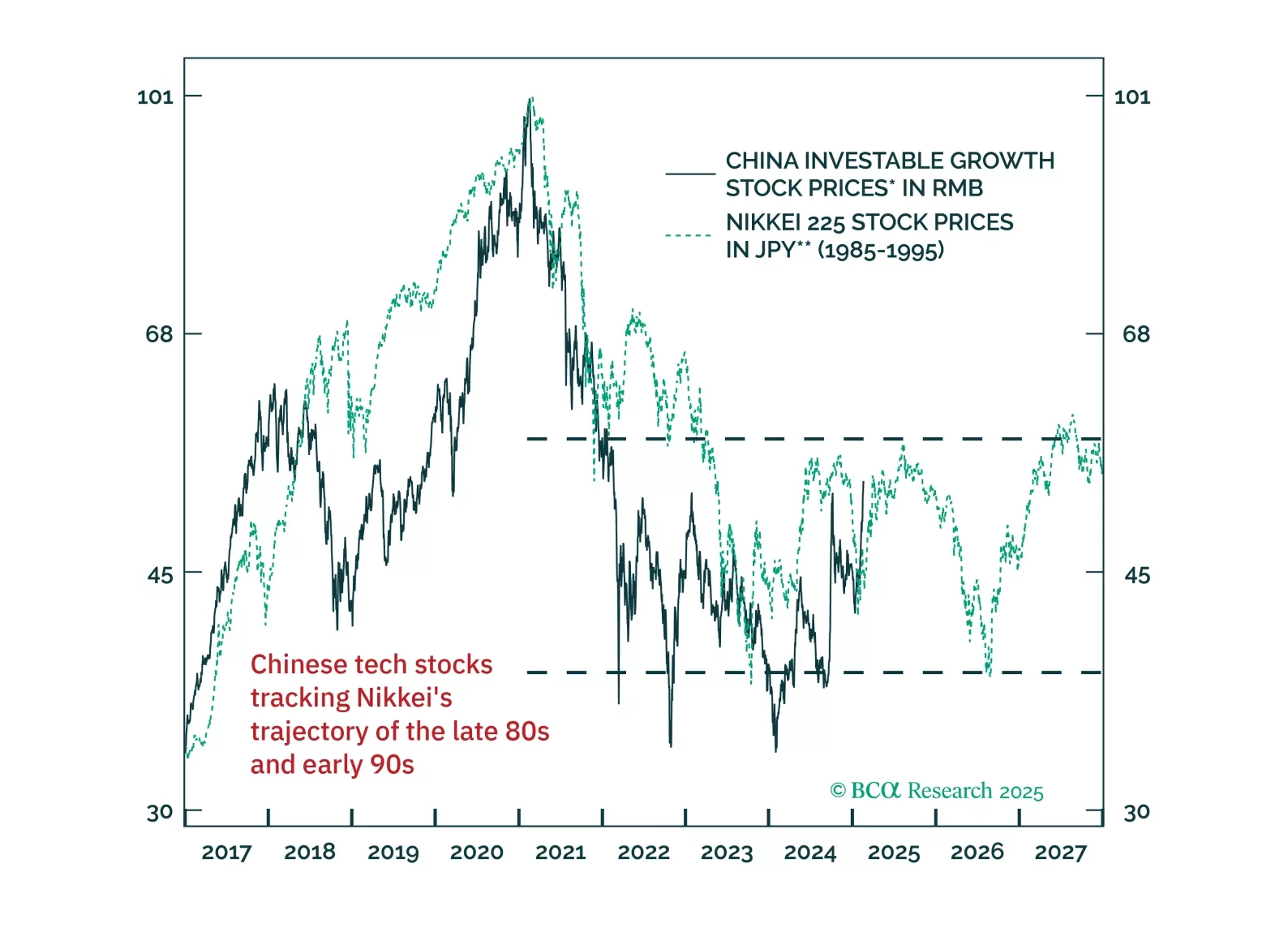

This week, our three screeners cover equity plays in European Defense, Chinese Tech, and “Boring Stocks”.

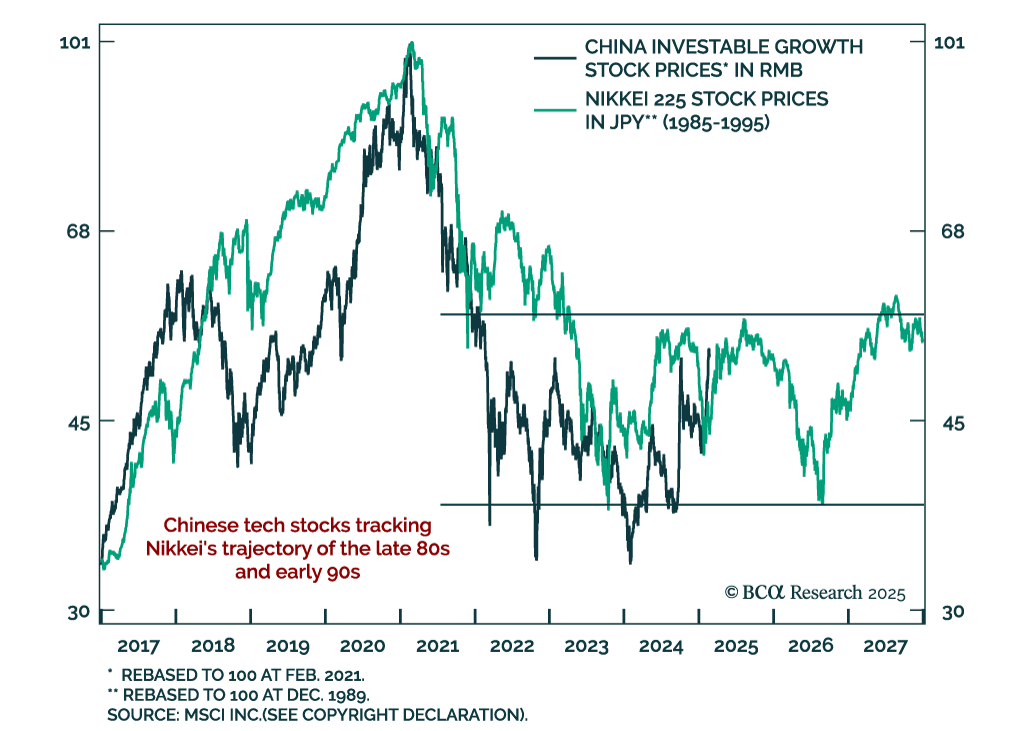

DeepSeek's AI breakthrough will likely enhance China’s productivity gains. But does it justify a re-valuation in Chinese tech stocks? Sustaining the Chinese tech rally will require corporate profits to overcome the pressures of China’s deflationary cycle. Meanwhile, DeepSeek’s innovations may fuel greater competition, intensifying price wars and putting further strain on Chinese tech companies’ profit margins.

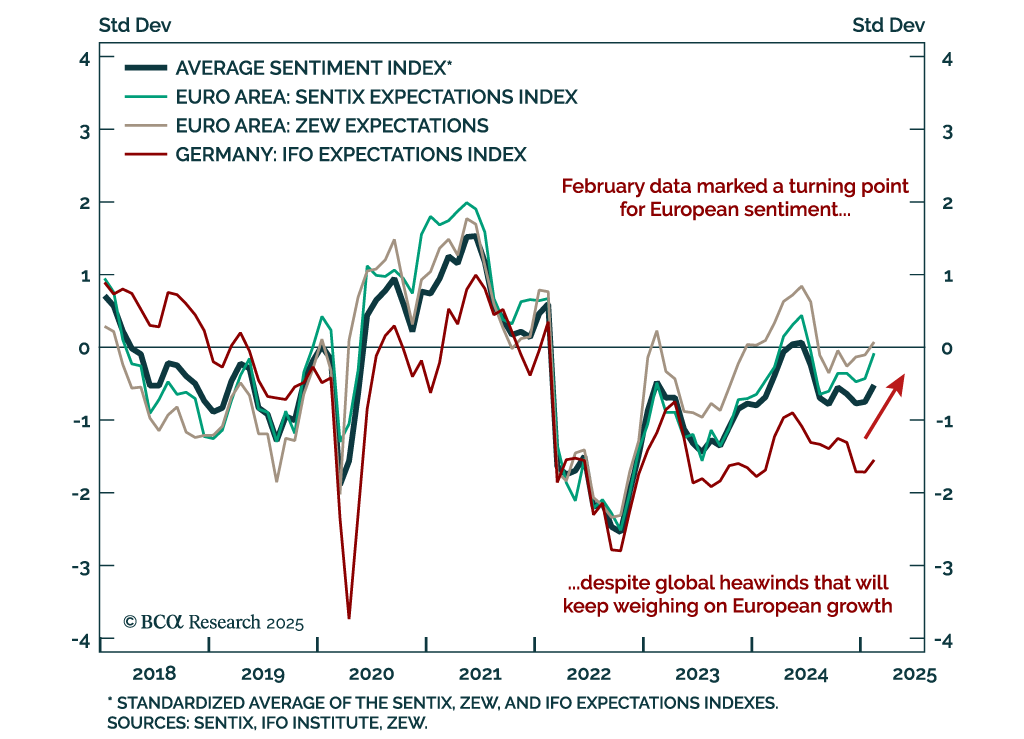

The rise of the far-right is challenging mainstream German politics. The CDU/CSU and SPD will govern Germany again after the election. A ceasefire in Ukraine will offer some relief, but Trump’s policies will keep tensions high.