Equities

Long-term drivers, including the growing ability of banks to returns cash to shareholders, point toward a strong structural performance for European financials. However, the ECB’s aggressive tightening campaign could still spoil the party.

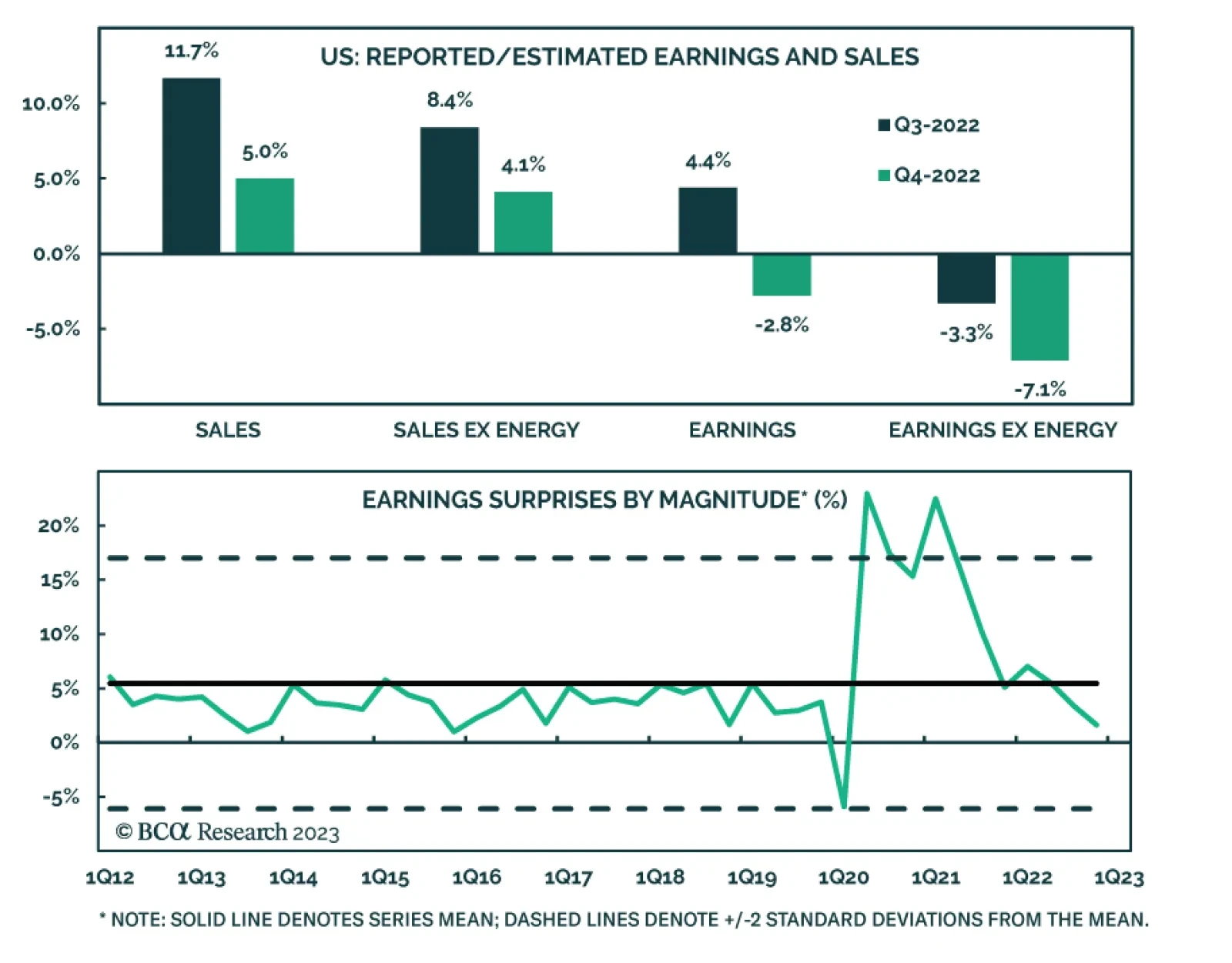

The US equity market is in the midst of an earnings contraction driven by slowing sales growth – a manifestation of the weakening economic demand and loss of corporate pricing power that accompany disinflation. The telecommunications industry is a defensive industry that faces many challenges: Low growth, cut-throat competition, and incessant demands for capital investment.

We refresh our 2023 plan of attack to reflect the latest data and several rounds of discussions with clients in virtual and face-to-face meetings. We continue to expect a meaningful first-half rally in the S&P 500, despite revising our expected terminal fed funds rate 25 basis points higher.

The risk of a recession in 2023 is being supplanted by the risk of another inflation wave. We will turn more defensive on equities if it continues to look like inflation is making a comeback.

Investor sentiment on China and EM has become bullish. Meanwhile, the reflation plays have begun fraying on the edges. Cracks always appear first in the most sensitive reflation plays and then spread to the core. The narratives of the Fed's imminent pivot and China's recovery will be questioned in the coming months. Thus, China/EM assets and related plays will sell off, and the US dollar will rebound.

Thai stocks and currency will weaken over the short term. And yet EM equity portfolios should overweight Thailand as tourism revivals will rejuvenate this economy.