Equities

Bulls and bears are perplexed because they suffer from recency bias. The investment roadmap and framework of the past 15 to 20 years should not be used to analyze current US financial markets. US corporate earnings will likely plunge substantially even in the case of a mild recession.

It is easy to conclude that European equities are attractively valued by looking at multiples; however, a method rooted in fundamentals is essential to find out which bourses are genuinely cheap.

Investors should avoid / stay underweight Turkish stocks and local currency bonds versus their respective EM benchmarks. Stay underweight Turkish sovereign credit.

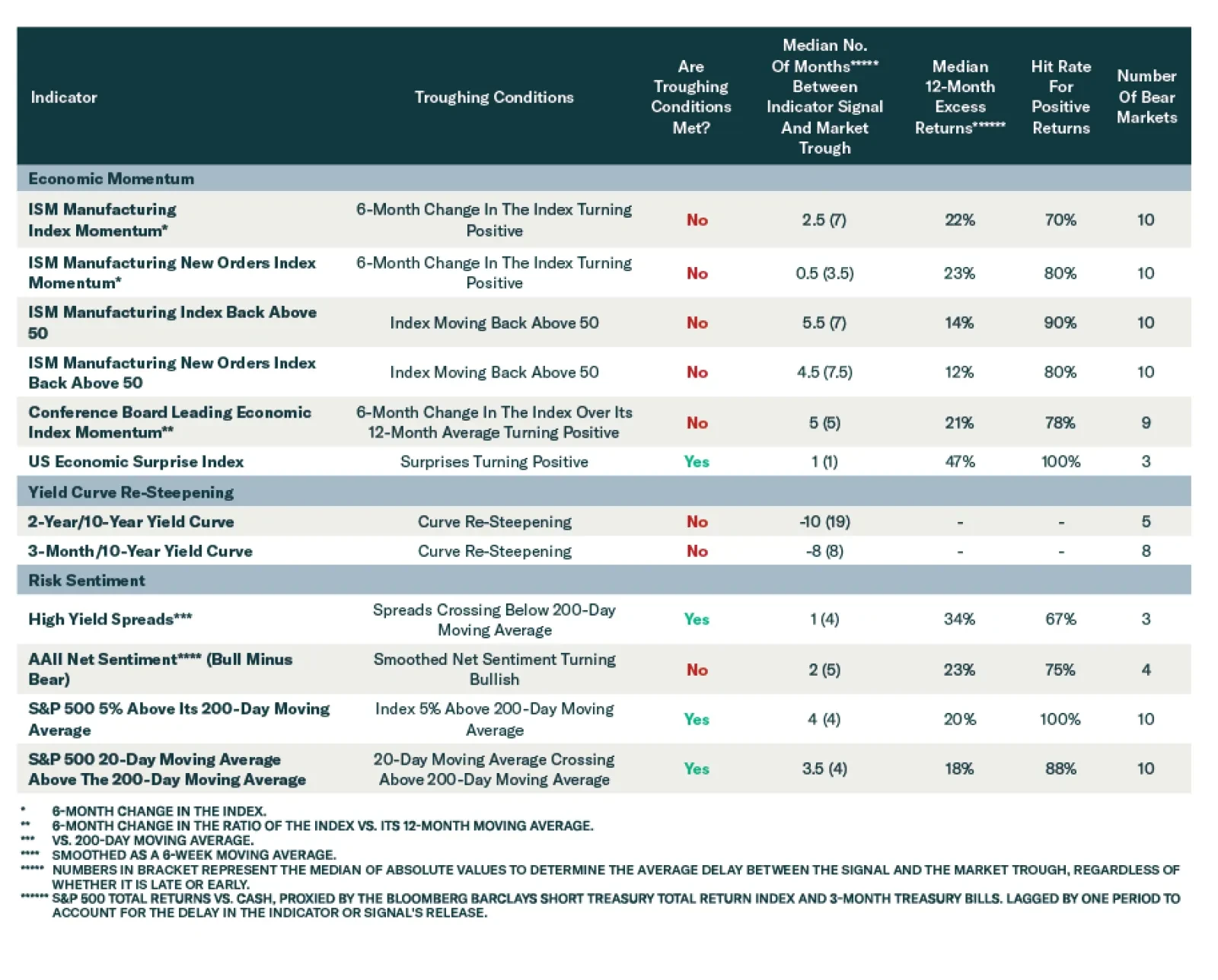

We analyzed US bear markets since 1954 to identify reliable indicators for distinguishing new equity bull markets from bear market rallies. Our checklist of indicators does not suggest it is time to overweight equities in a multi-asset portfolio. Remain underweight on equities, overweight on fixed income, and neutral on cash.

Great Power Rivalry is taking another leg up as Russia and China further align their geopolitical interests. Investors should stay long USD-CNY, favor defensives over cyclicals, and markets like North America and DM Europe that have less exposure to geopolitical risk.

In Section I, we address the recent improvement in several data releases over the past three months, and explain why we do not believe that these developments have increased the odds of a soft landing. US monetary policy likely became tight in November, which has started the recessionary clock. We continue to recommend a conservative investment stance over the coming 6-12 months that anticipates eventually lower long-maturity bond yields. In Section II, we explain why the Fed’s unreasonably low neutral rate forecast is the main risk to a conservative investment stance over the coming year, as it could lead to interest rates falling back into easy territory before a recession begins. For now, this remains a possible but not probable outcome.

Since 1970, the track record of US housing recessions as the ‘canary in the coal mine’ for economic recessions is a perfect four out of four: 1974; 1980; 1990; and 2007. If this perfect track record continues, the current US housing recession presages an economic recession that starts in 2023. We discuss the investment implications.