Equities

In Section I, we audit the market’s “soft landing” narrative in response to a meaningful challenge to our cautious stance from recent financial market developments. We acknowledge that US economic growth was stronger in the first half of the year than many investors expected, but we are unmoved by the recent uptick in “soft landing” hopes. A “soft landing” outcome very likely necessitates interest rate cuts before recessionary dynamics emerge, and it is far from clear that rate cuts or (especially) an easy monetary policy stance are likely to materialize over the coming year. As such, we continue to believe that conservative portfolio positioning is appropriate. In Section II, we discuss some simple approaches that we use when valuing the major asset classes that we cover. We conclude that global ex-US equities and ex-US developed market currencies are the main assets that can be considered “cheap” today.

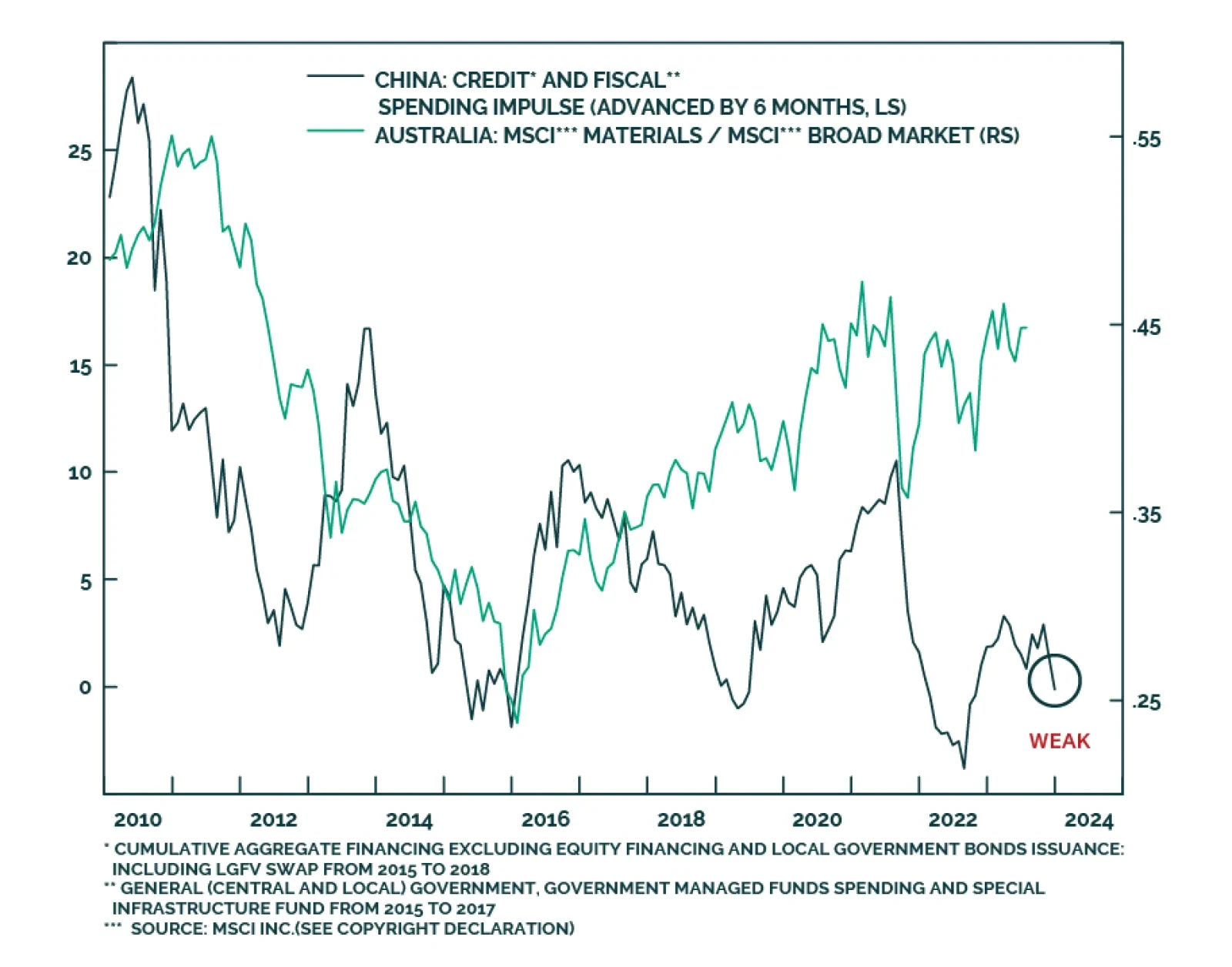

Stay cautious on Chinese stocks. Equity investors should use any rebound in onshore stock prices to downgrade A-shares from overweight to neutral within global and EM equity portfolios. Remain underweight Chinese investable/offshore stocks. Onshore bond yields will drop to all-time lows. Continue receiving 10-year swap rates. The currency will continue depreciating versus the US dollar in the coming months.

The snap election which took place on Sunday resulted in a political deadlock in Spain. No single party has won enough seats to form a government. More importantly, both the left-wing bloc and the right-bloc fell short of the 176-seat majority needed in the 350-seat lower house. Negotiations are taking place as we publish, but neither side can see a clear and straightforward path to form a working government. Spain is heading into a political deadlock.

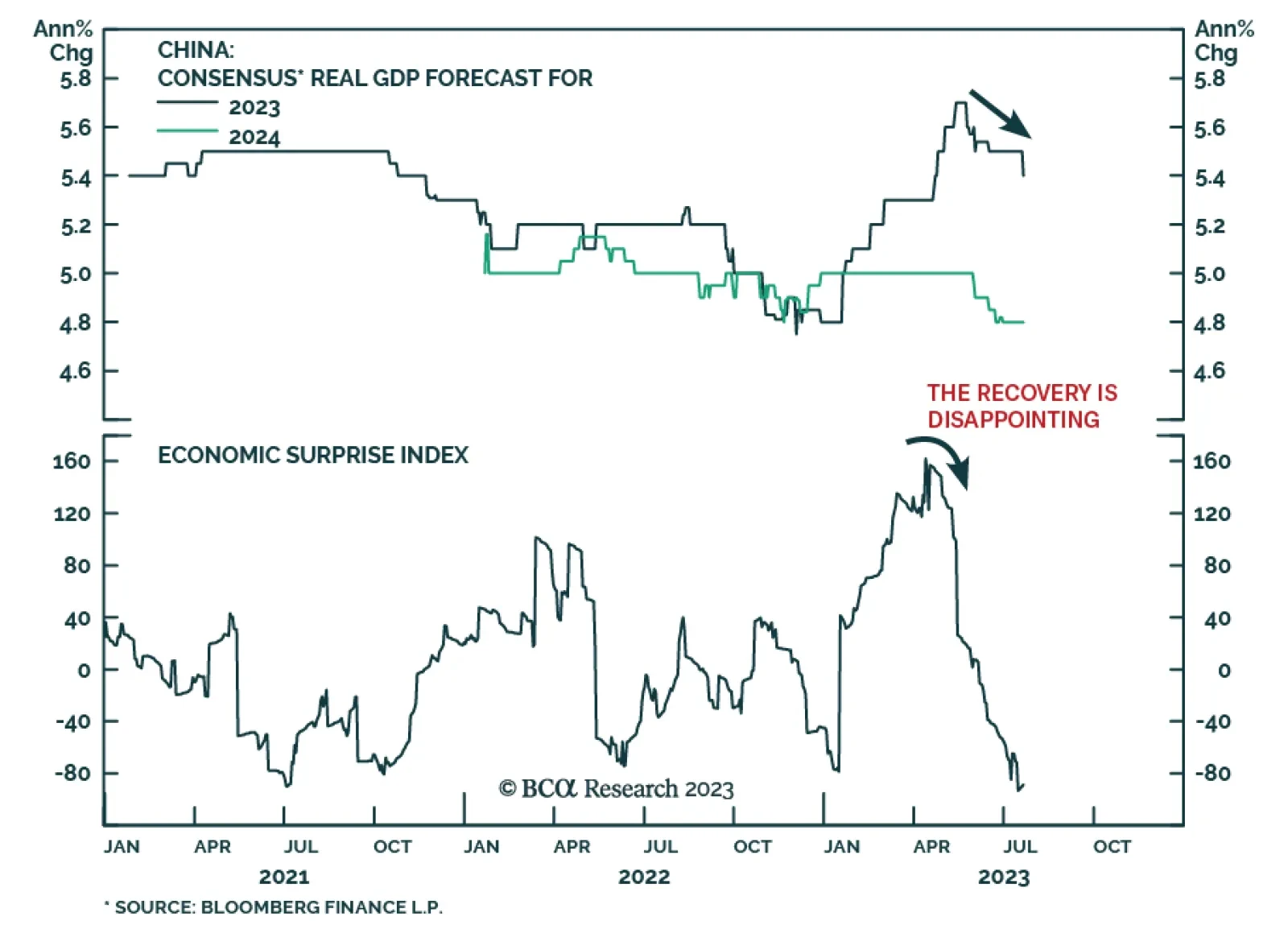

China’s economy is cruising at a very low altitude where gravity forces are intense. Downbeat consumer and business sentiment will reduce the effectiveness of stimulus. Anything short of “irrigation-style” stimulus will be insufficient to boost growth. We remain cautious on Chinese stocks. Onshore bond yields will drop to an all-time low. The RMB is still vulnerable against the USD in the next few months.