Equities

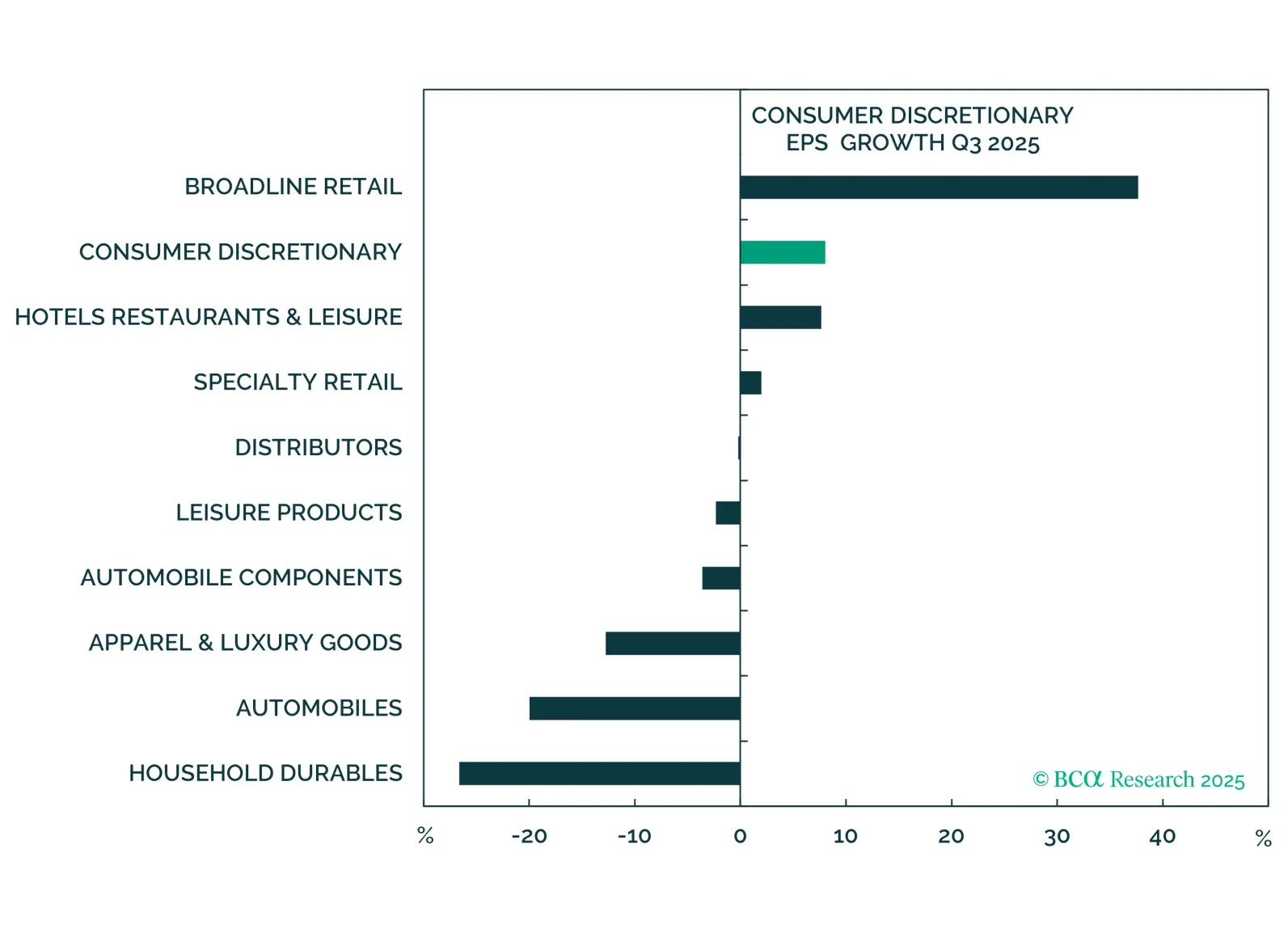

Q3 results were strong but failed to impress investors, and Q4 will likely prove more challenging. Beneath the surface, earnings diverged sharply: Firms catering to affluent consumers maintained solid momentum, while those reliant on the mass market lagged. We remain equal weight Consumer Services and underweight Consumer Staples.

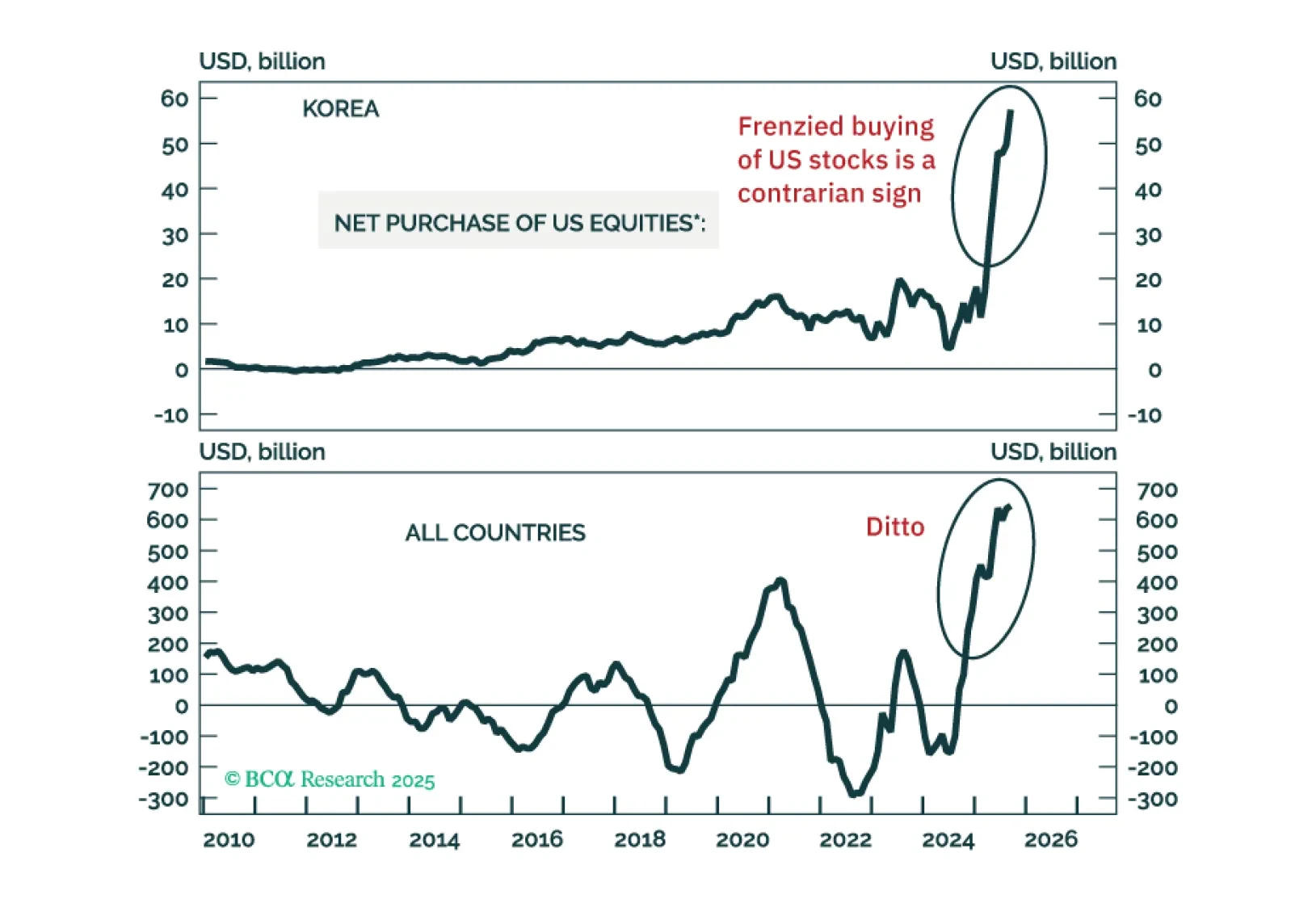

Many key equity indexes have failed to break above major resistance levels, while risky segments have begun to crack. Altogether, this suggests that a major peak in risk assets has probably been made. Short the MSCI EM stock index with a stop loss at 1470.

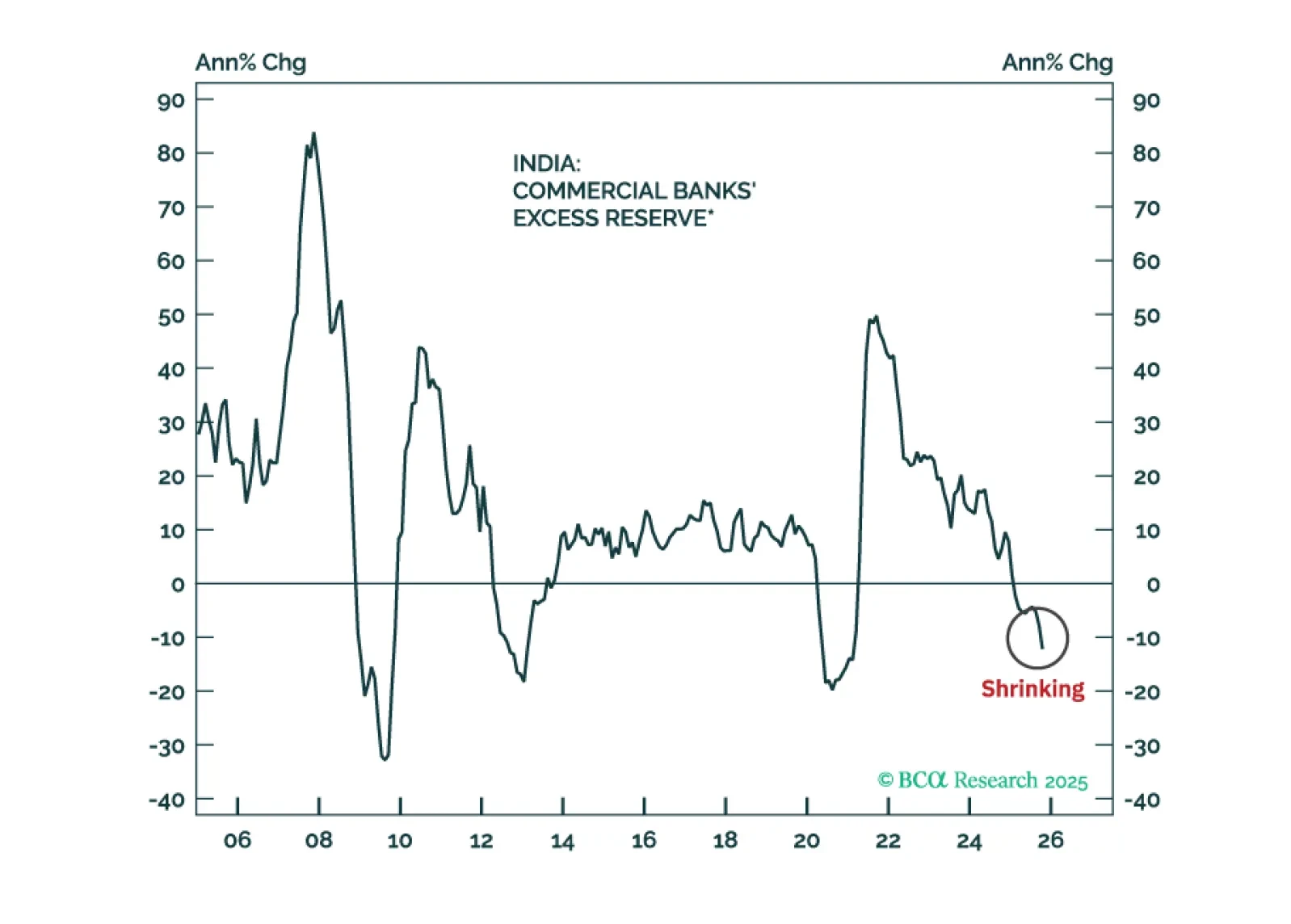

Indian stocks have further downside in absolute terms as profits disappoint. Their underperformance versus the EM equity benchmark, however, is late, which warrants a shift from underweight to neutral allocation.

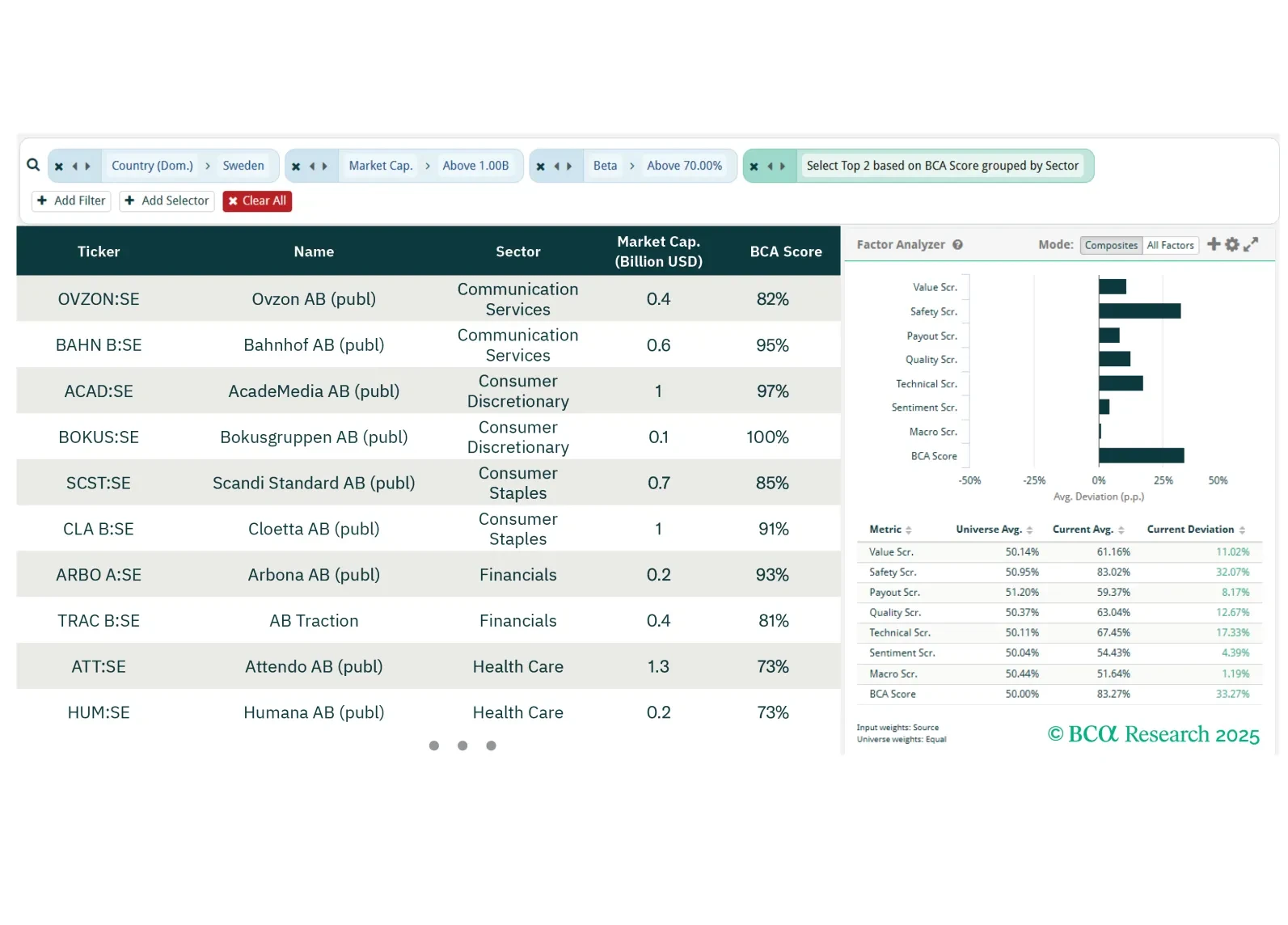

This week, our screeners explore opportunities in the Swedish stock market, Canadian gold-exposed and domestic-focused sectors, and ex-tech GenAI names.

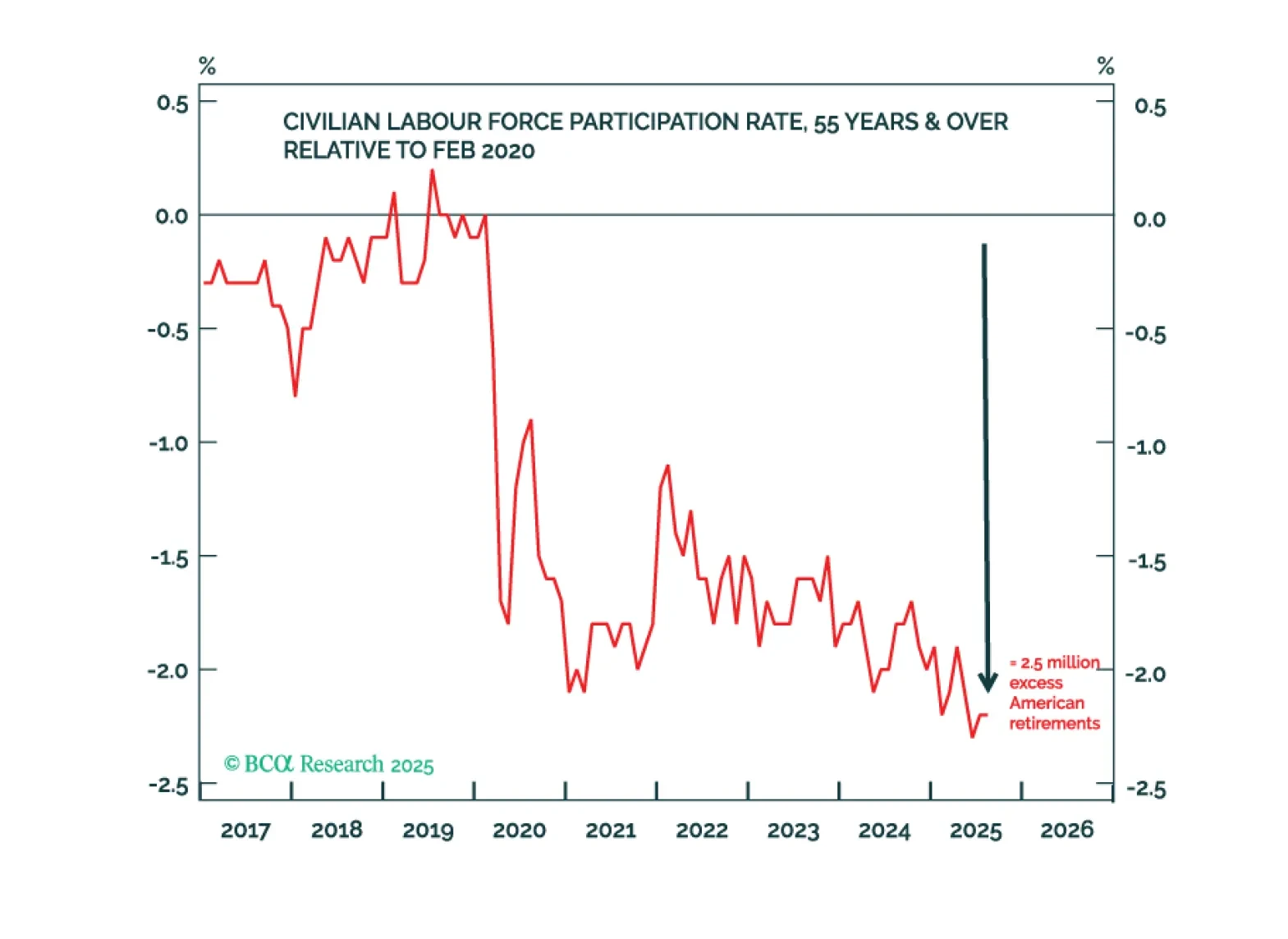

The greater risk to the world economy in 2026-27 is not that a recession triggers a market crash, but that a market crash triggers a recession. This is because a market crash will destroy the wealth that is funding the crucial marginal spending of 2.5 million excess American retirees. Plus, a new tactical trade is: Overweight Switzerland (SMI) versus UK (FTSE 100).

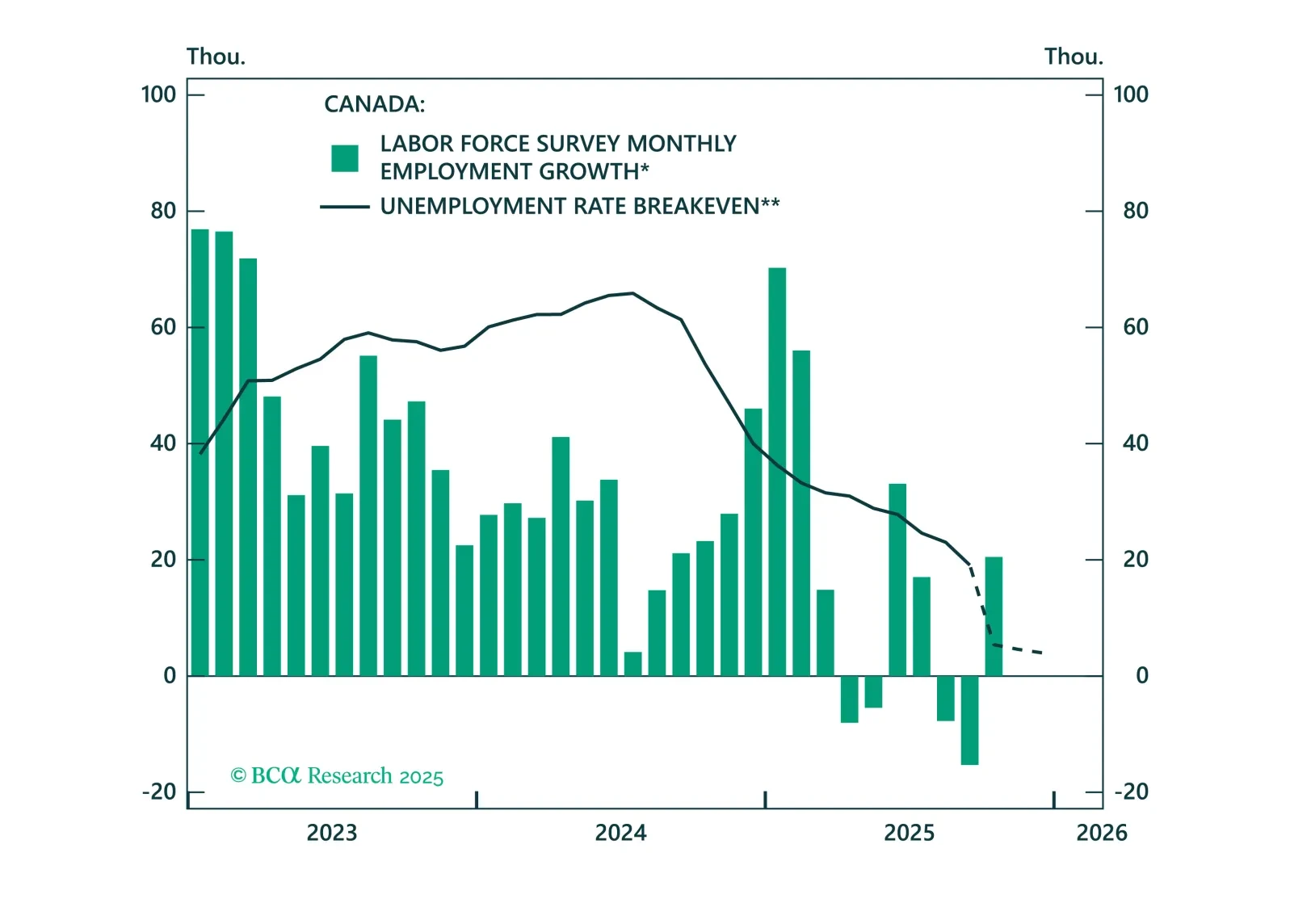

The trade war hit Canada’s economy hard, but the worst is over. In our latest update on Canada, we assess the aftermath of the trade shock, the new budget, and the effects of BoC easing. We outline what this means for duration, the Loonie, and Canadian stocks heading into 2026.

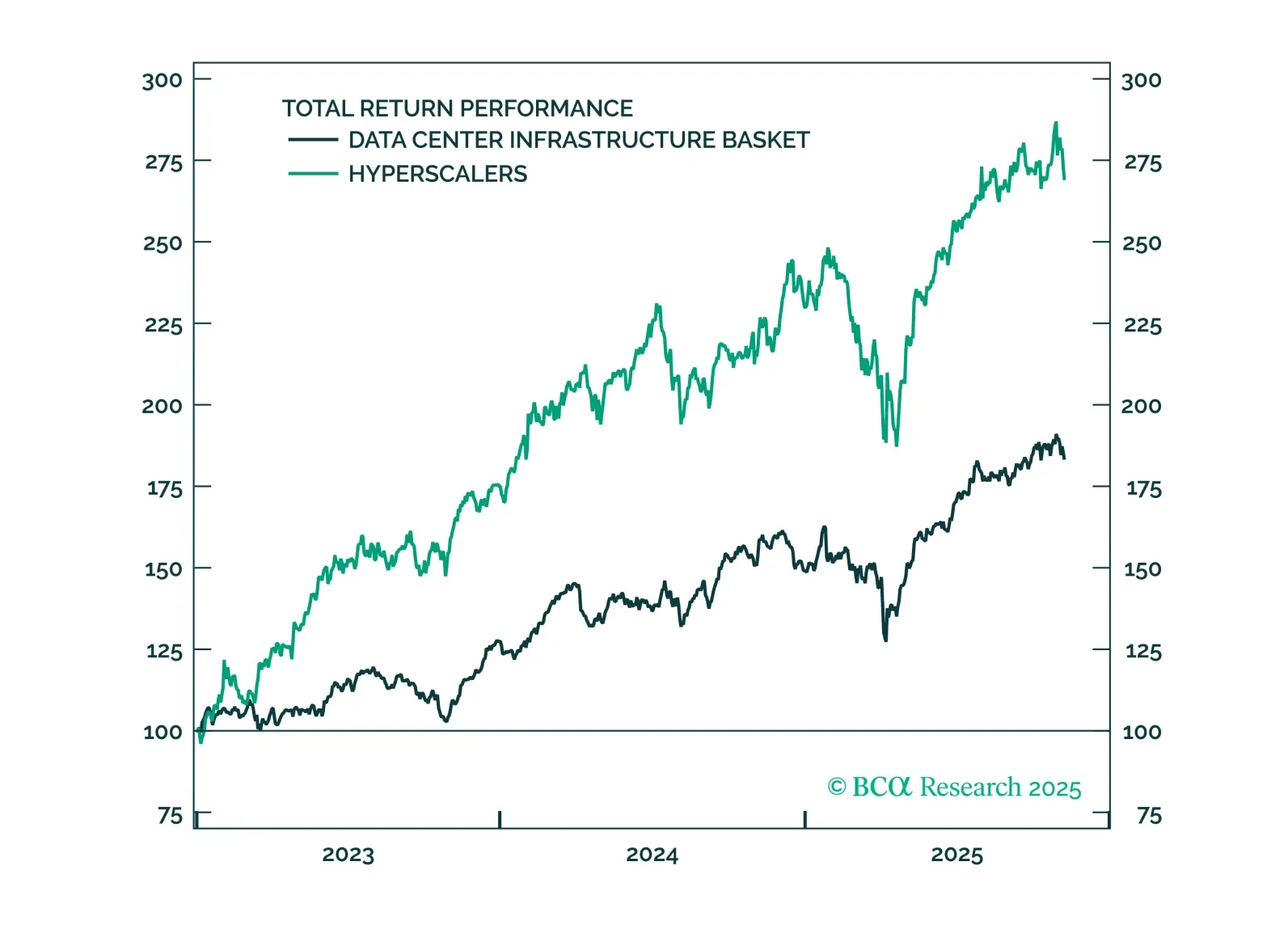

As hyperscalers expand global data center capacity, they are igniting a powerful industrial cycle. Capital Goods and Materials companies supplying turbines, grid components, cooling systems, and advanced connectivity materials for data center and energy infrastructure are emerging as key beneficiaries, positioned to capture structural growth as GenAI demand reshapes the economy.

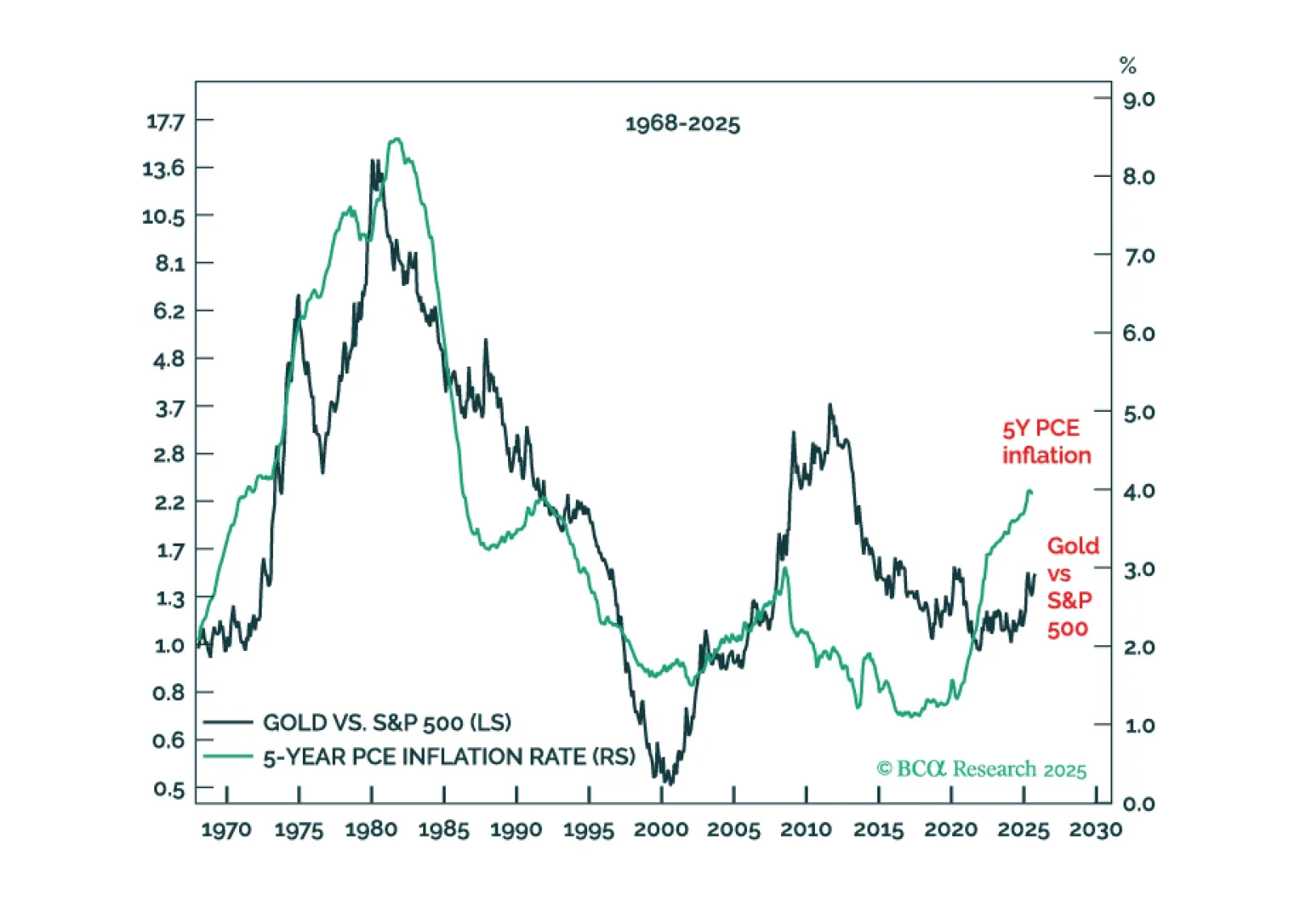

Long-term investors should own gold. The network effect that makes gold the physical ‘insurance asset’ of choice will generate long-term outperformance. But long-term investors should also own bitcoin. The network effect that makes bitcoin the digital ‘insurance asset’ of choice will generate long-term outperformance that betters even gold.

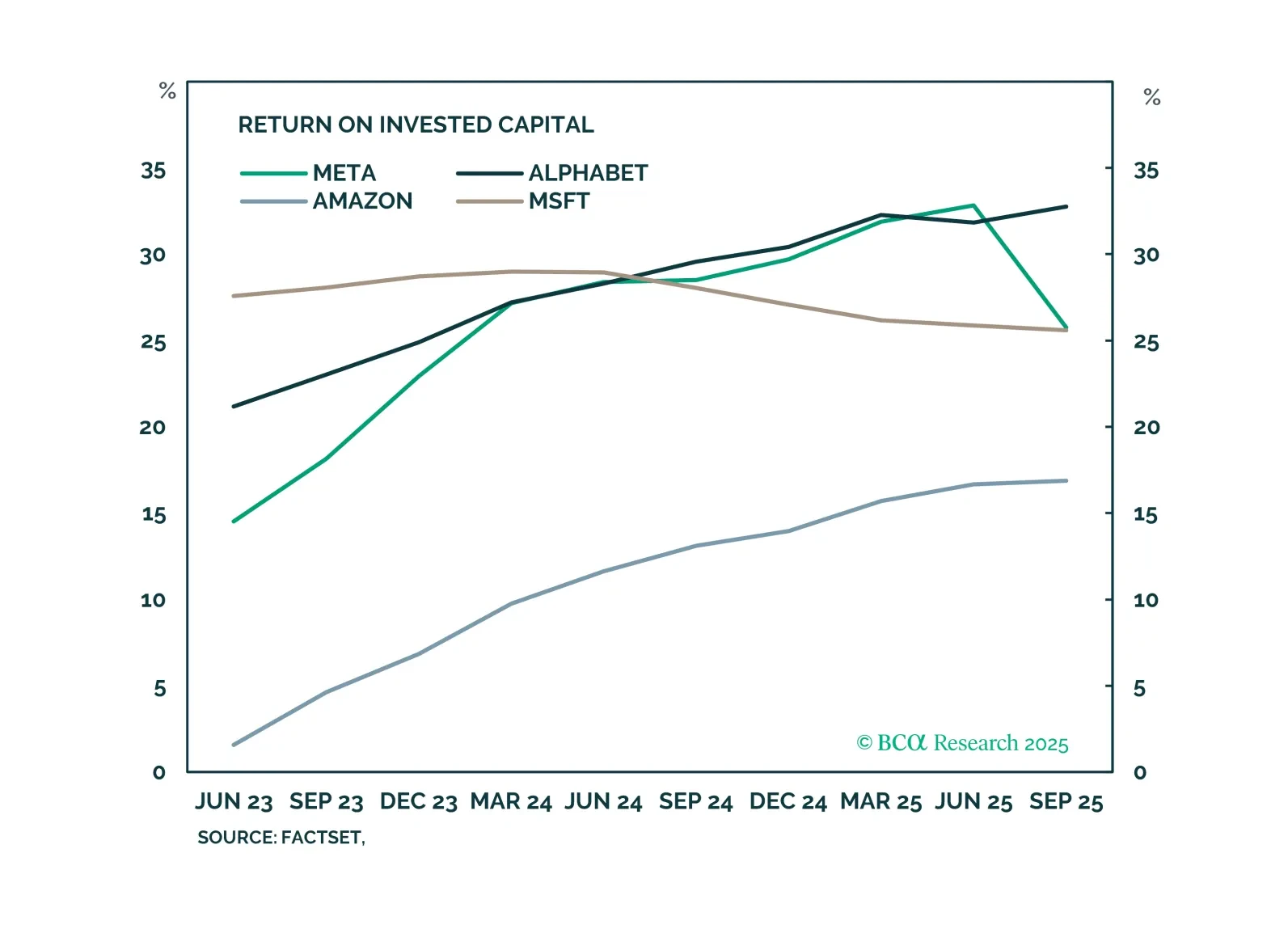

Investor reaction to Meta’s GenAI is an admonition against overspending, rather than a sign of a fraying GenAI rally. Other hyperscalers’ investments are driven by buoyant demand and remain profitable. With valuations stretched and many of the positives priced in, market consolidation is likely. We are decreasing portfolio beta.

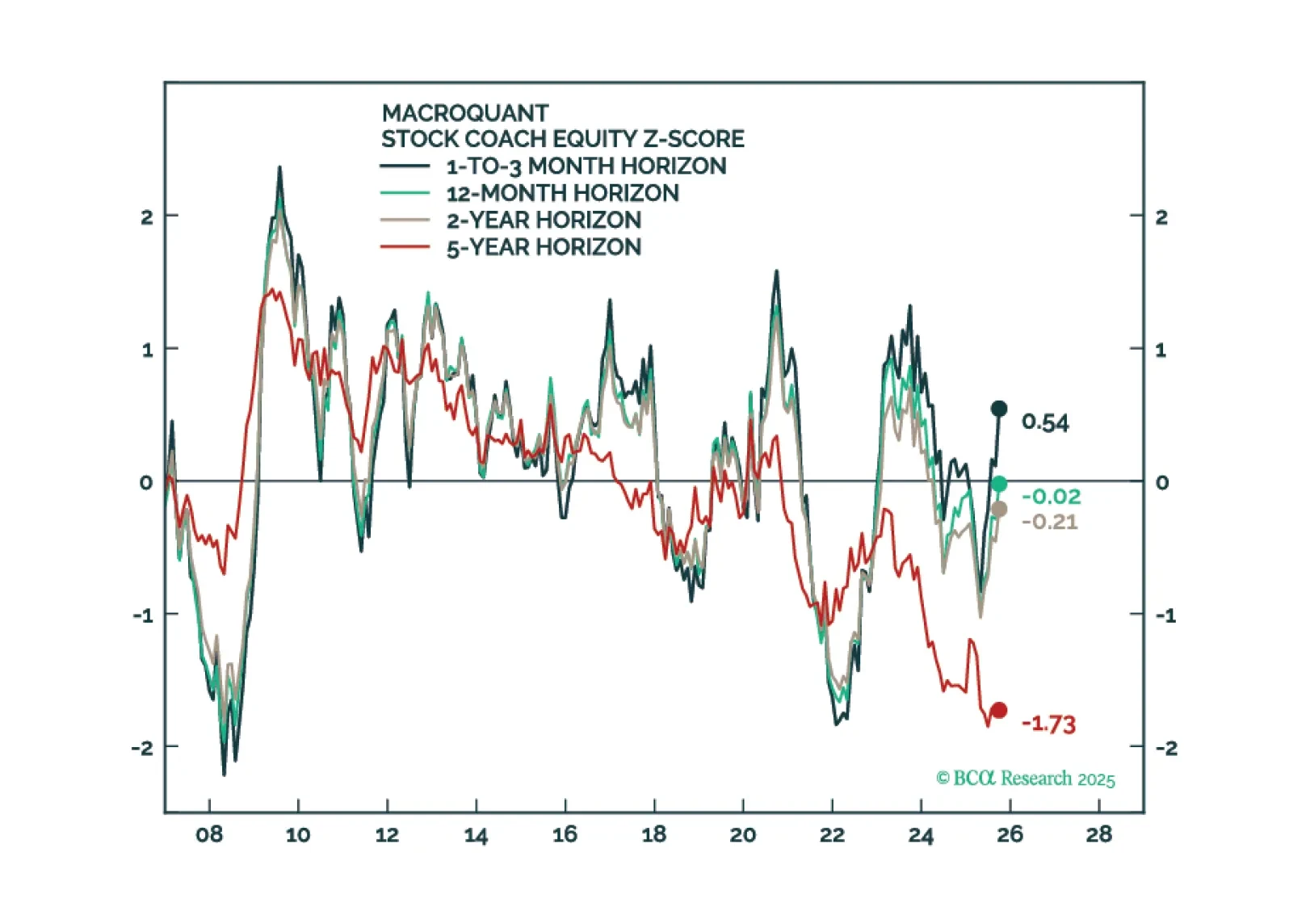

MacroQuant is tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold and copper.