Emerging Markets

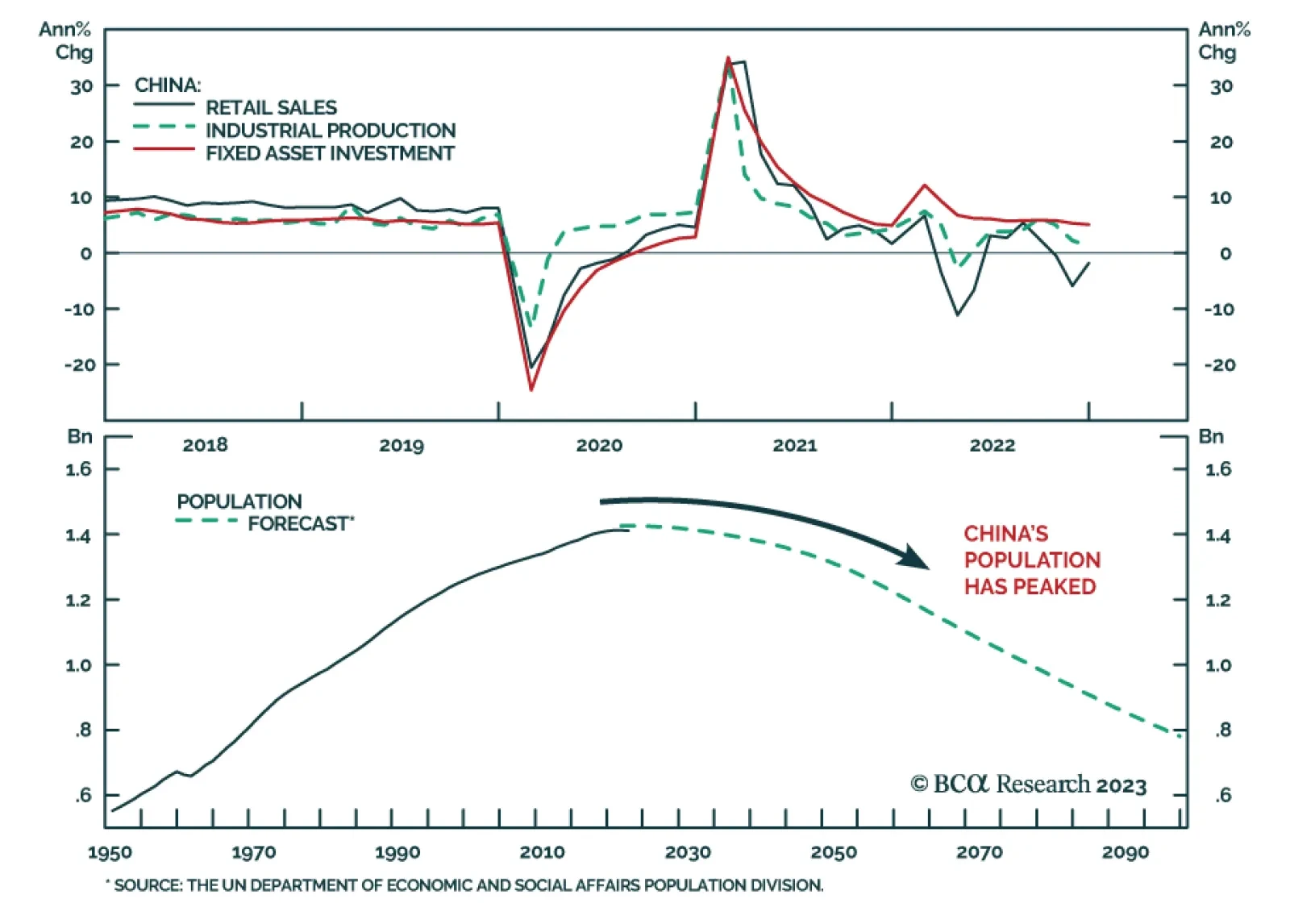

China's reopening is much more positive for the Chinese economy than it is for the rest of the world, as it will boost its domestic service sector activity and consumer spending much more than the industrial economy. A slowdown in Chinese industrial activity will put downward pressure on its demand for raw materials and energy, helping the world avoid another spike in inflation. Upgrade Macau casinos to overweight as the key beneficiaries of reopening. Off-shore TMT and bank shares face structural headwinds.

Investors should bet against the global rally in risk assets and maintain a defensive positioning until recession risks verifiably abate.

Investors should bet against the global rally in risk assets and maintain a defensive positioning until recession risks verifiably abate.

In response to lower energy prices and China’s reopening, European assets prices are outperforming. Will the ECB spoil the party?

CCP policy stimulus will boost growth in China this year. Copper prices breached $4.00/lb on COMEX this week, as expected. We continue to forecast $4.50/lb this year, with upside price risk dominating. Iron ore also will rise, but economic and regulatory policy uncertainty clouds the outlook. We remain long the COMT and XME ETFs. We are getting tactically long BRL/USD and AUS/USD on the back of our metals view, which is constrained by China’s reversion to absolute autocracy and ability to reverse policy suddenly and unpredictably.

Why will Chinese consumer spending recover but not its industrial sectors? Will China's reopening boost the global business cycle and inflation? How fast will US core inflation fall and what are the implications for corporate profits? Are global equities pricing in enough bad news/profit contraction?