Emerging Markets

In this Special Report, BCA Strategist Ritika Mankar highlights that India may prove to be a sanctuary of safety in what promises to be a volatile 2023. Indian equity outperformance could continue, as India ends up offering relatively high growth at a time when EMs at large must contend with the effects of declining exports, high global interest rates, and exhausted fiscal stimulation capabilities.

Remain cautious and defensive overall. Stay long DM Europe over EM Europe. Look for EM opportunities in Southeast Asia and Latin America over Greater China.

In Section I, we explain why we do not see the deceleration in US inflation, the likely near-term pickup in European growth, and the end of China’s dynamic zero-COVID policy as signs of a sustainable rebound in global economic activity over the coming 6-12 months. The key question is not whether inflation will fall back to central bank targets, but rather how quickly this will occur. For now, our indicators point to slower but still elevated inflation this year. In Section II, we explore what it will take for the Fed to cut interest rates, and note that nonrecessionary rate cuts are possible but not especially likely.

It is not unusual for a period of rebounding share prices to occur between an inflation-driven selloff and a growth scare. Initially, stocks rally on falling inflation and prospects of lower interest rates. Then, worries about corporate profits intensify, and equity prices deflate along with falling Treasury yields. This is what happened in the US in 2000-2001 and is likely to occur in the coming months.

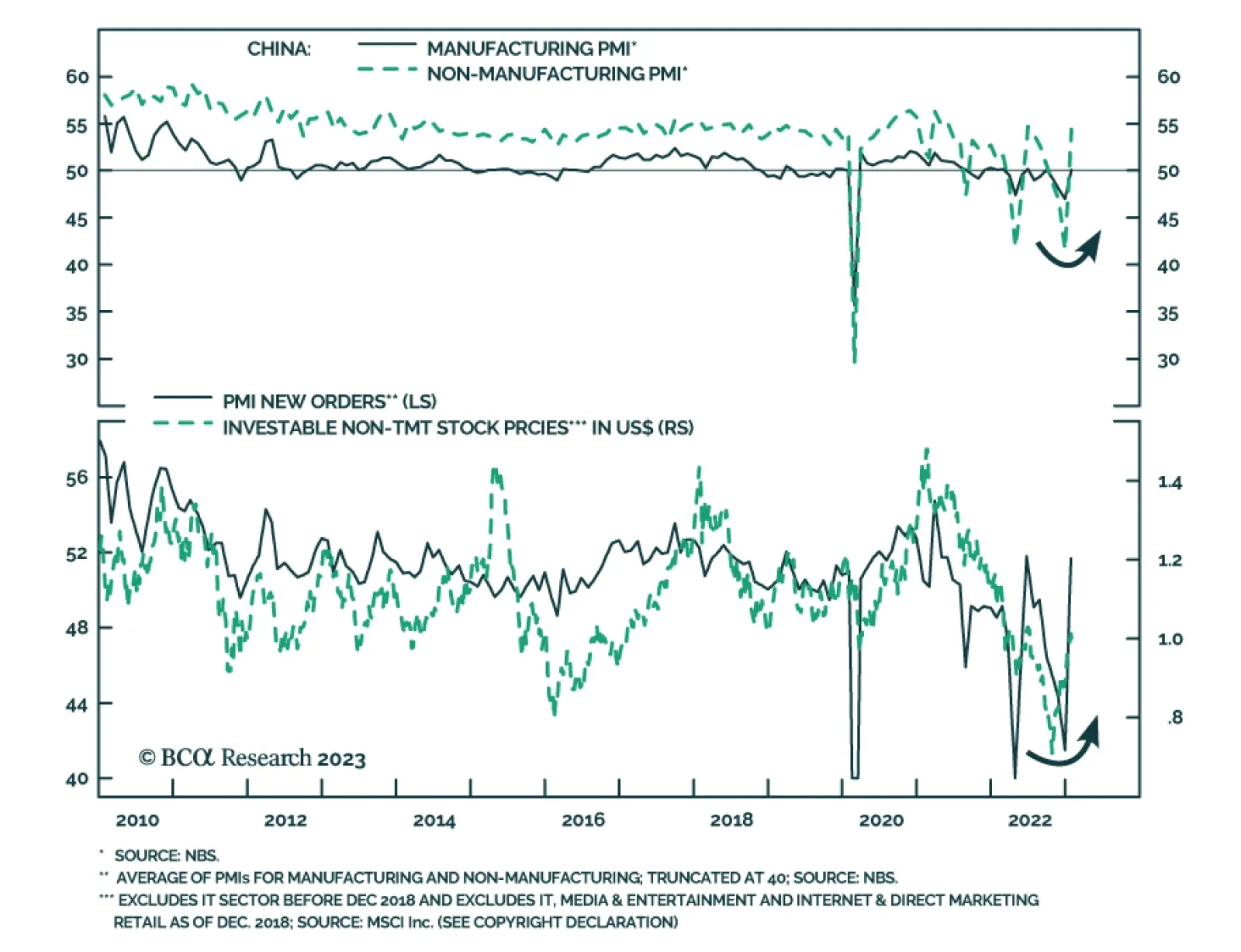

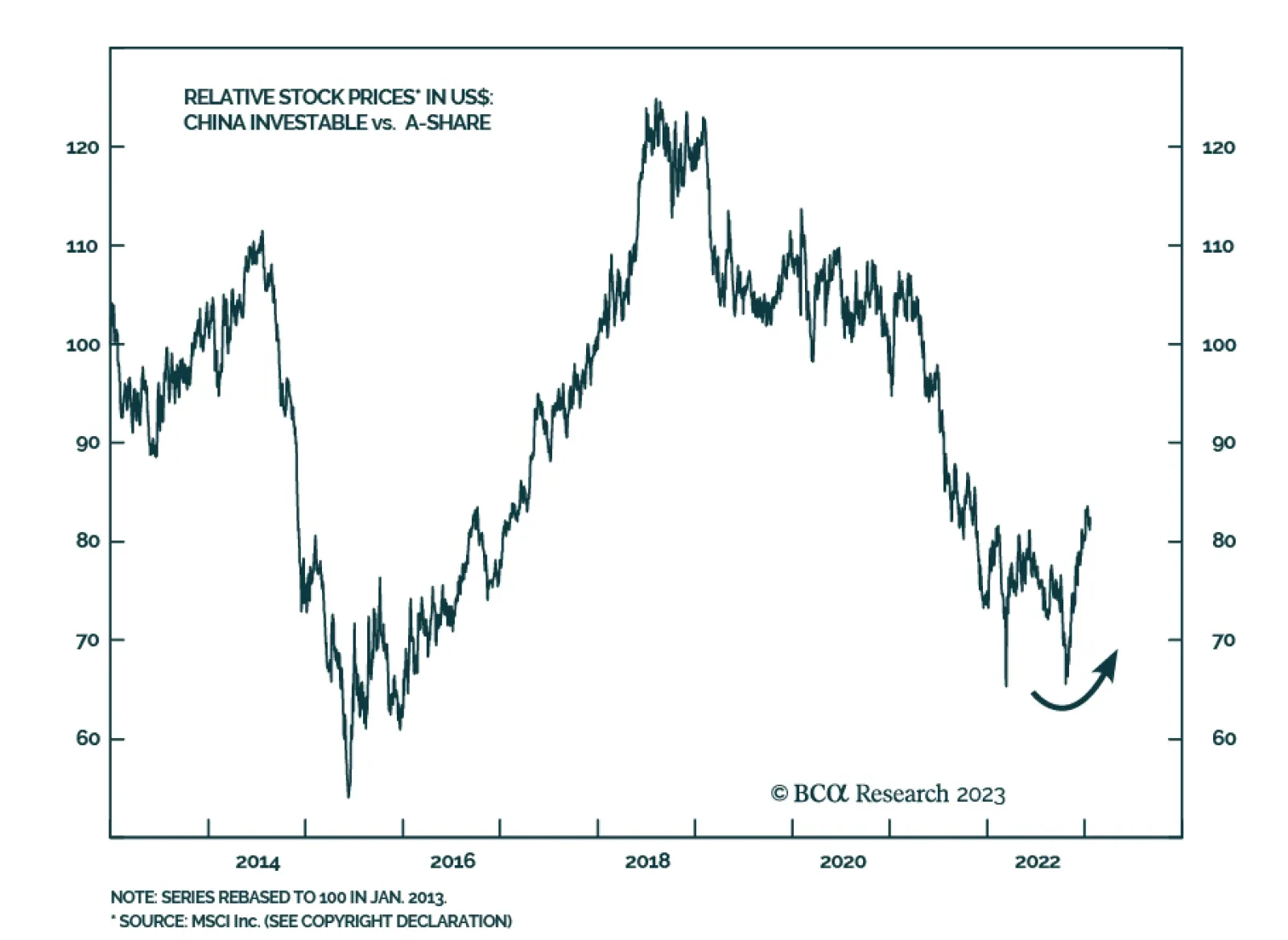

Global investors should sell Chinese assets on strength this year and diversify into other emerging markets. American investors should limit China exposure. Short CNY-USD.

In EM ex-China, growth will continue decelerating. Some economies will experience an outright recession, while most will have a growth recession. Nearly every single economy will experience a cyclical drop in inflation (with the exception of Turkey).

China’s re-opening – powered by the fiscal and monetary stimulus required to achieve at least 5% real GDP growth after flattish 2022 growth – and a weaker USD will catalyze demand growth this year and next, lifting global oil consumption by close to 2mm and 1.7mm b/d in 2023 and 2024. We lowered our Brent forecast slightly for this year to $110/bbl, and expect 2024 prices to average $115/bbl. WTI will trade $4-$6/bbl lower.

This insight presents an outlook on USD-Denominated Emerging Market Bonds.