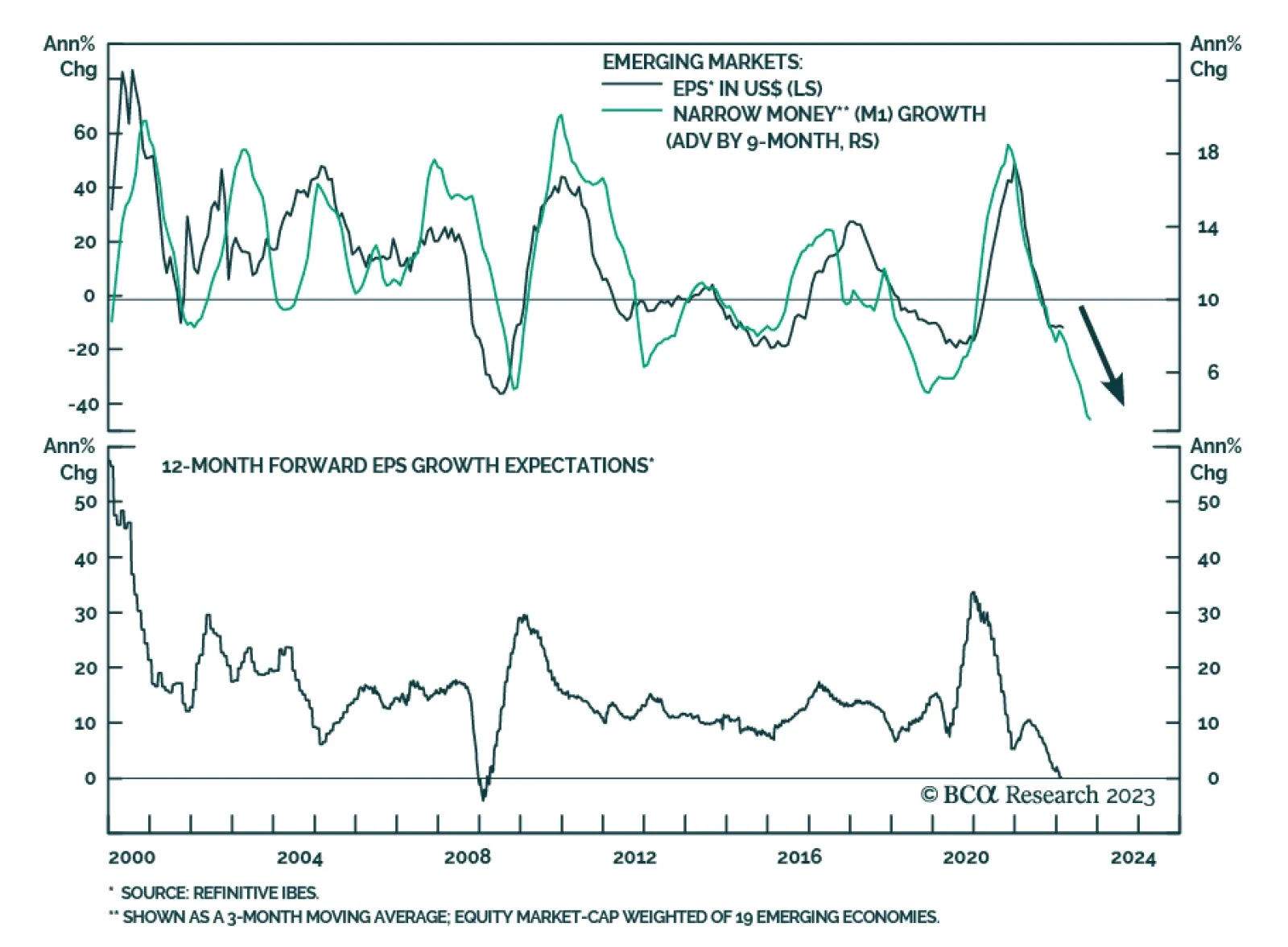

Emerging Markets

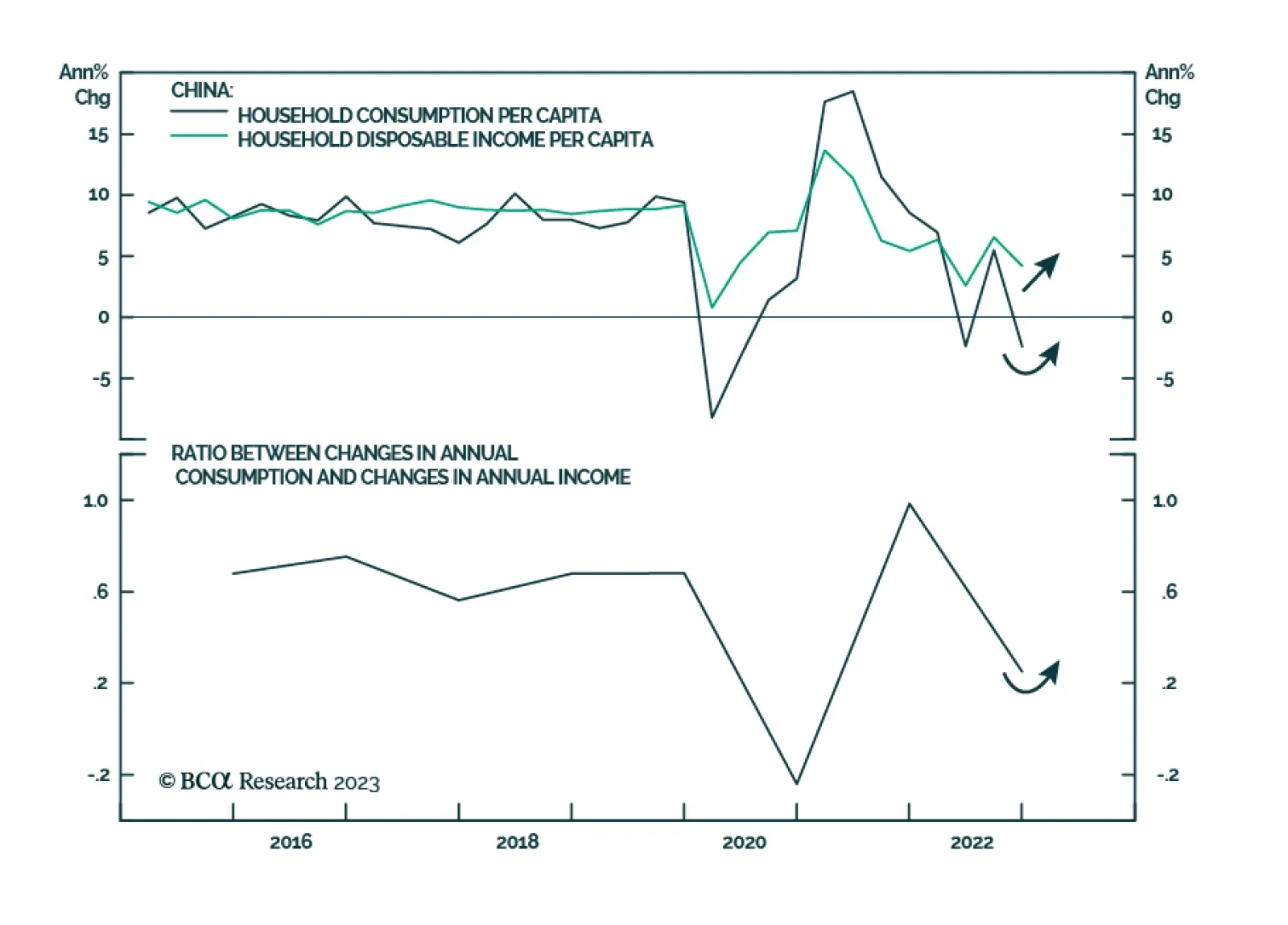

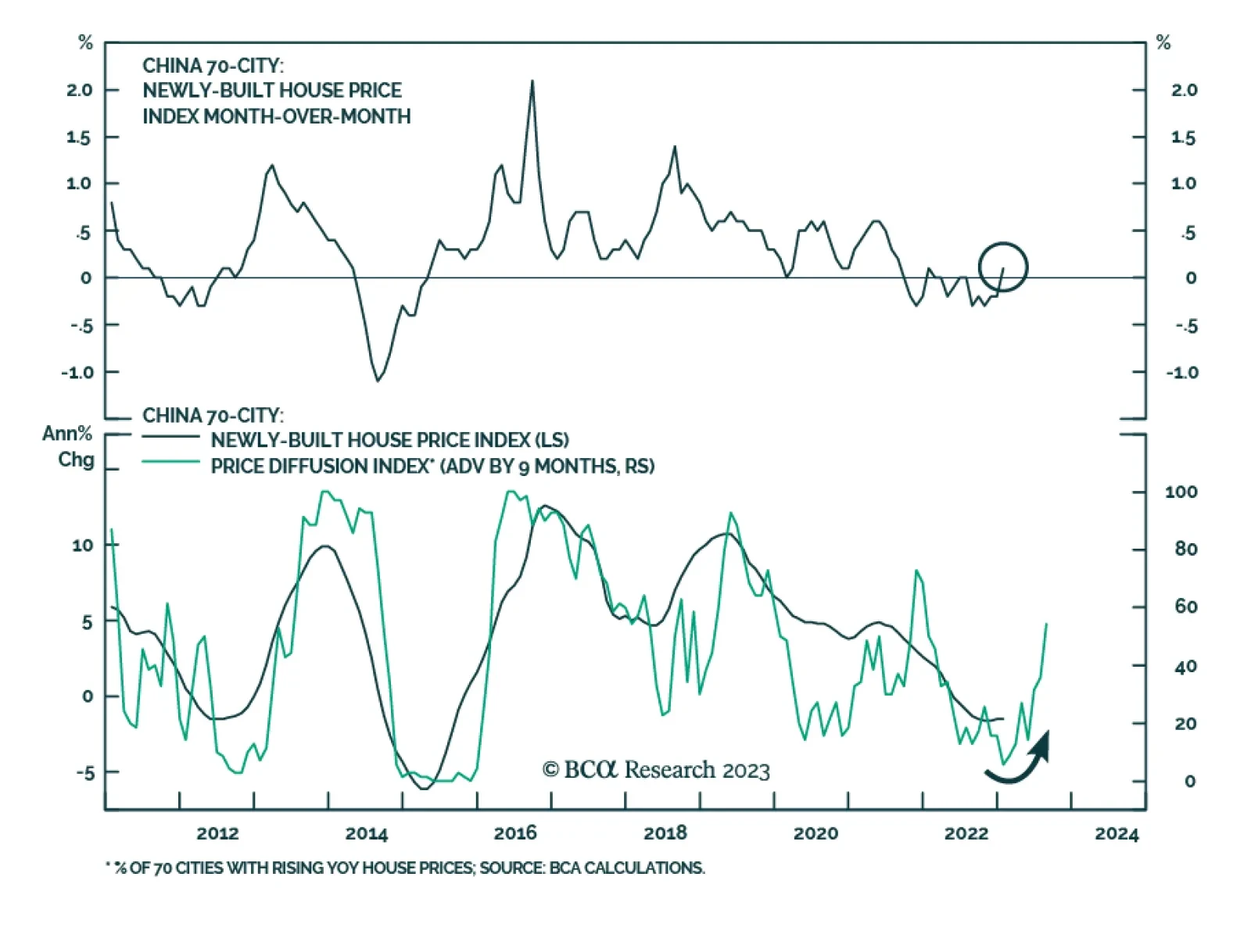

Pent-up demand for consumer goods and services will boost Chinese household spending this year. Beyond the next 12 to 18 months, however, structural forces will likely drive Chinese household consumption growth lower than in the pre-pandemic era.

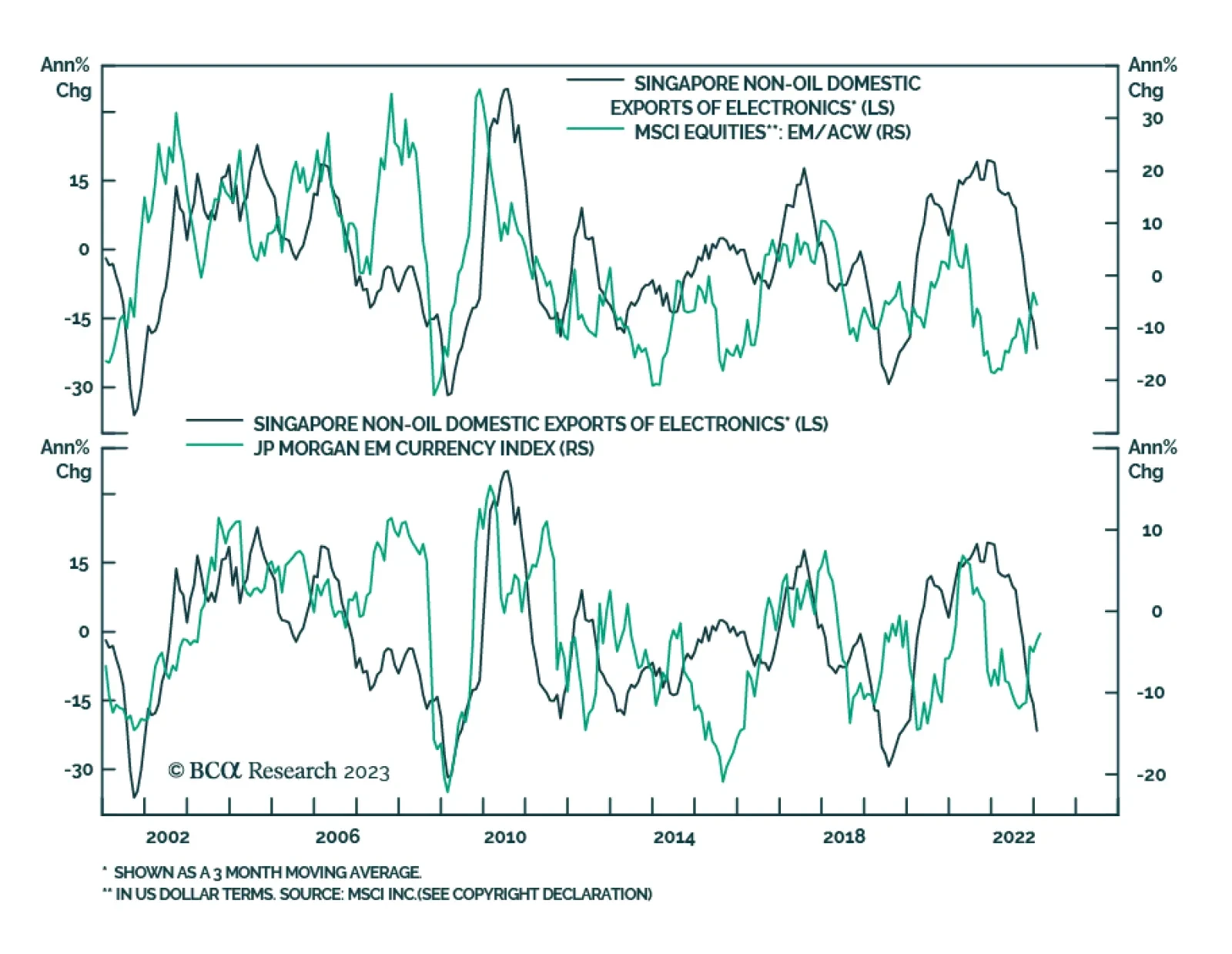

Investor sentiment on China and EM has become bullish. Meanwhile, the reflation plays have begun fraying on the edges. Cracks always appear first in the most sensitive reflation plays and then spread to the core. The narratives of the Fed's imminent pivot and China's recovery will be questioned in the coming months. Thus, China/EM assets and related plays will sell off, and the US dollar will rebound.

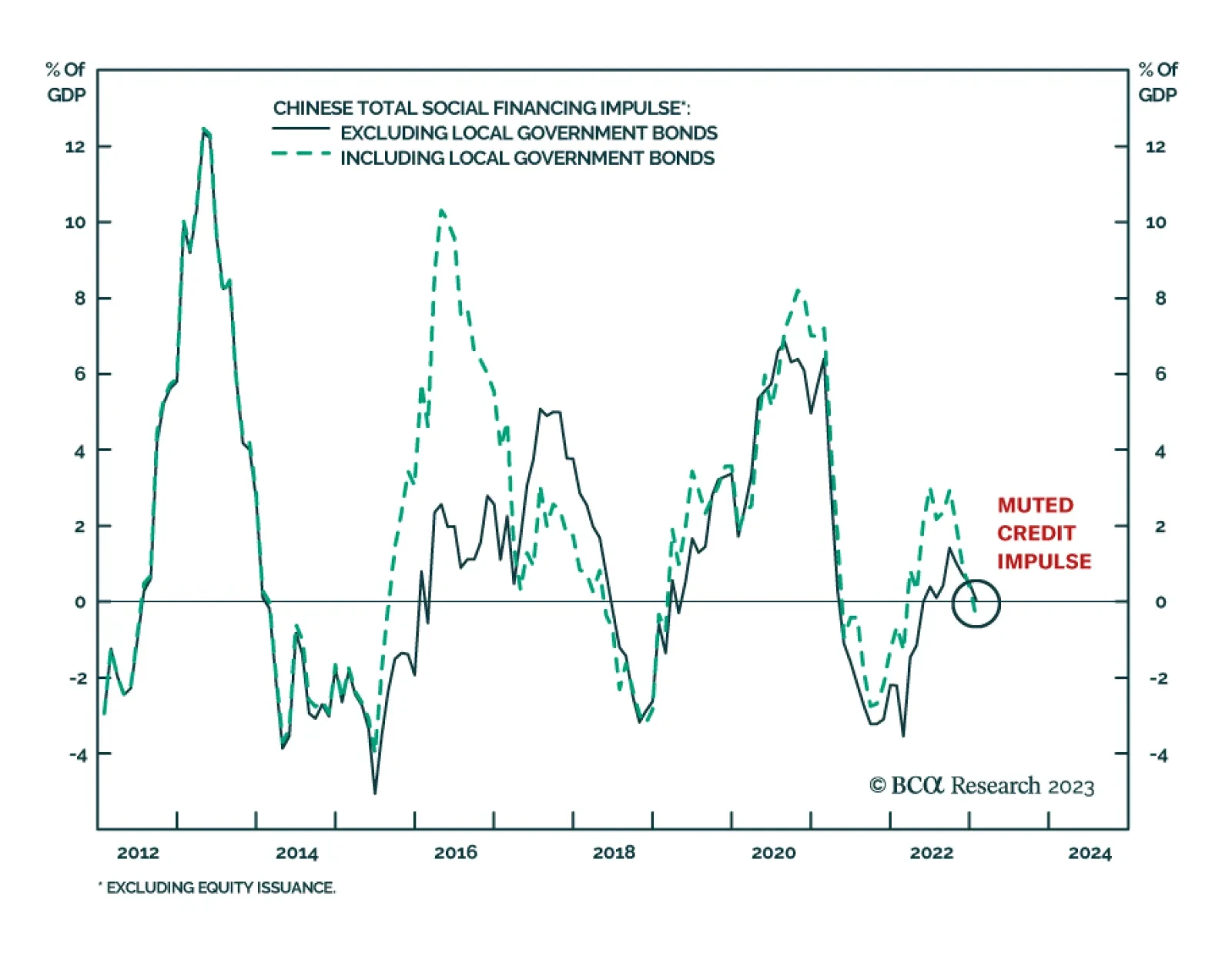

Two developments this week reinforce our key views for 2023. First, Russia’s threat to reduce oil production by 500,000 barrels per day, while escalating the war in Ukraine, confirms that geopolitical risk will rebound and new oil supply shocks are likely. Second, China’s credit numbers for January confirm that the country is trying to stabilize the economy but also that stabilization will not come quickly. Moreover, stimulus does not resolve structural problems over the long run. We remain defensively positioned overall and underweight Chinese assets.