Emerging Markets

This week we present our Portfolio Allocation Summary for March 2023.

The Chilean economy is entering a recession. Inflation will drop rapidly and the central bank will cut rates meaningfully in H2 2023. We continue to recommend a structural overweight across Chilean risk assets on the basis of falling inflation and local yields, record cheap valuations, and dissipated political volatility.

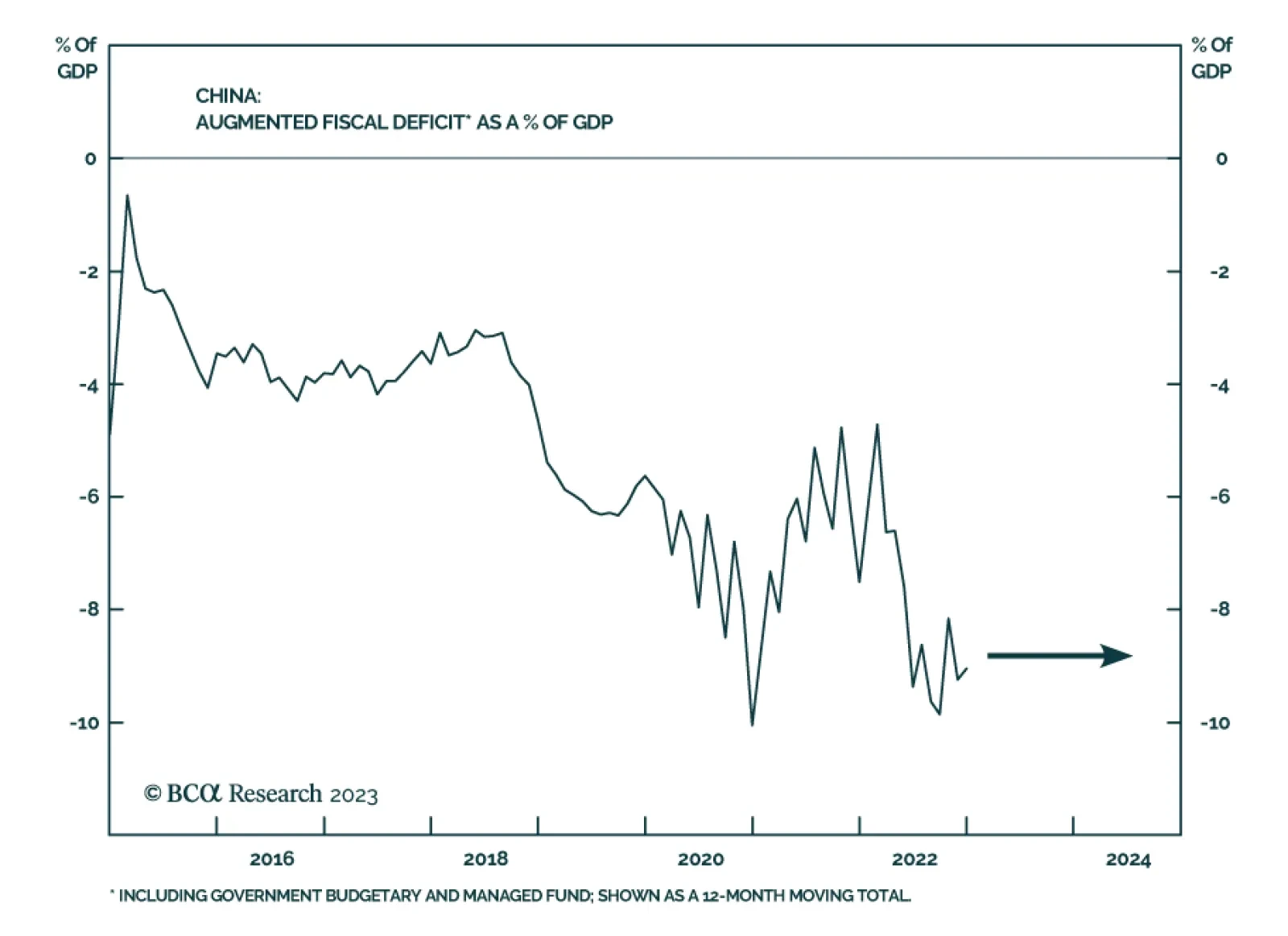

China’s housing market adjustment will be protracted, causing several years of sub-par growth in the world’s second largest economy. We go through the major investment implications.

Global demand for new energy vehicles (NEVs) remains in a long-term uptrend, propelled by falling battery prices, improved driving range and an upgraded charging infrastructure. That said, diminishing policy support in China and Europe will spark a drop in the growth rate of global NEV sales to about 35% this year, down from about 60% last year. Global NEV-related stocks are likely to rise on a structural basis, but we recommend that investors wait for a better entry point given that valuations remain high.

Investors should avoid / stay underweight Turkish stocks and local currency bonds versus their respective EM benchmarks. Stay underweight Turkish sovereign credit.

Great Power Rivalry is taking another leg up as Russia and China further align their geopolitical interests. Investors should stay long USD-CNY, favor defensives over cyclicals, and markets like North America and DM Europe that have less exposure to geopolitical risk.