Emerging Markets

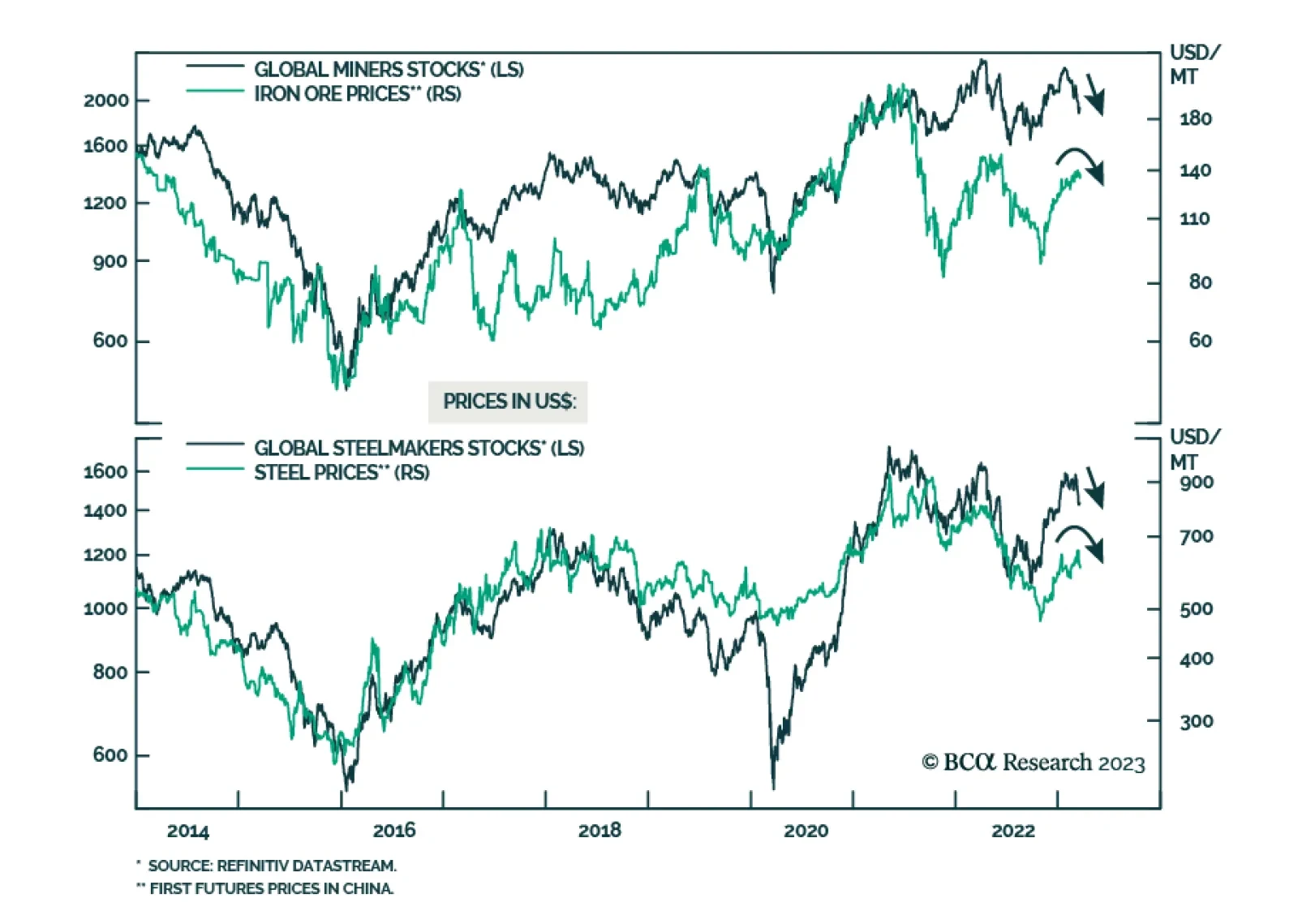

Both iron ore and steel will have oversupplied markets in 2023. The path of least resistance for iron ore and steel prices will be down in the coming months. We expect both iron ore and steel prices to drop by 15%-20% from their current levels. We recommend that investors short stocks for global steelmakers and global mining companies.

China’s victory in getting KSA and Iran to restore diplomatic relations is of far greater consequence to commodity markets than the past weeks’ bank failures in the US. For China, further success in sorting long-standing security issues in the Middle East could incentivize oil and gas capex and affect oil flows. With short- to medium-term fundamentals largely unchanged, we are keeping our 2023 and 2024 Brent forecasts similar to last month, at $95/bbl and $110/bbl, respectively.

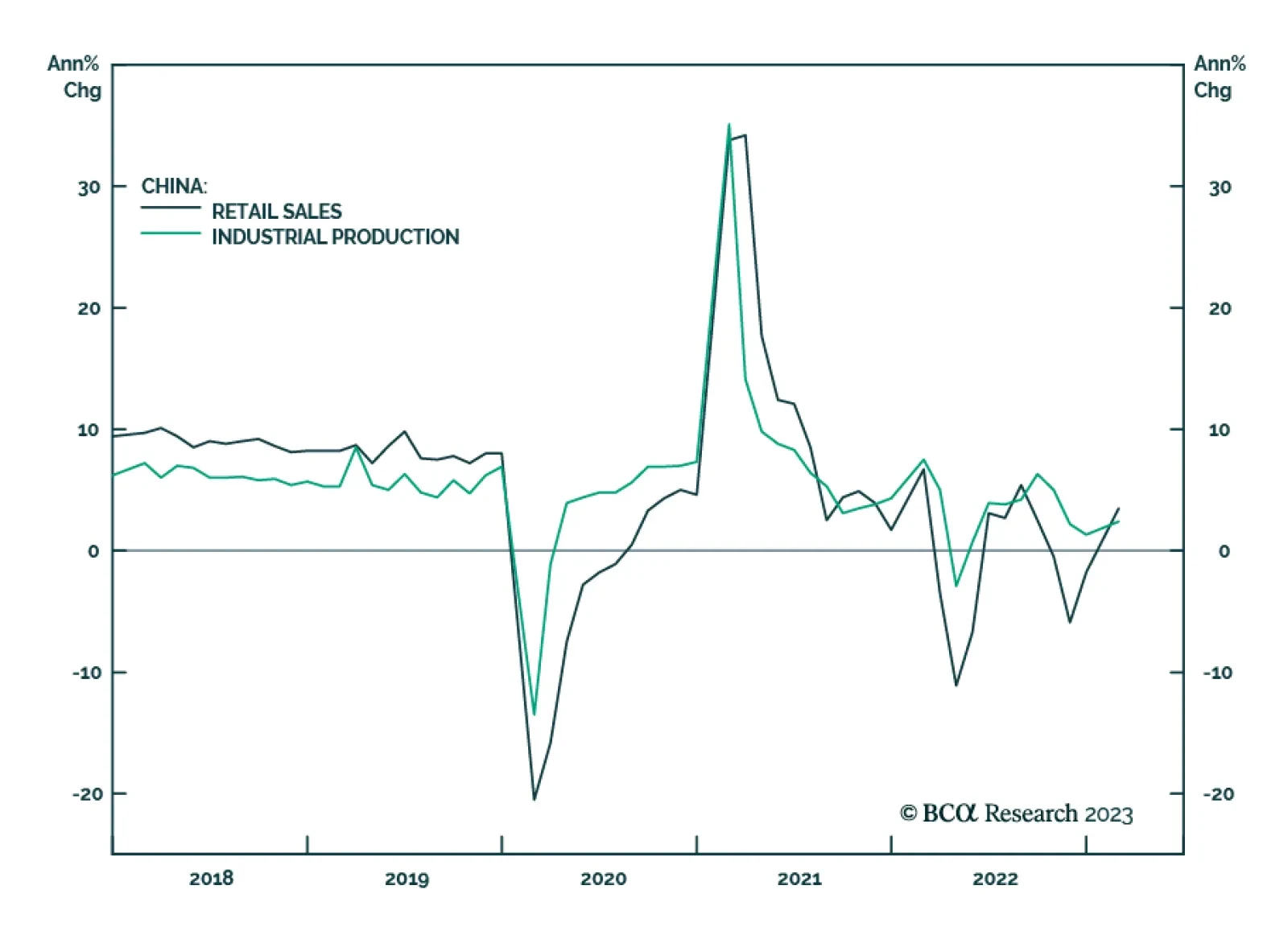

The odds of achieving a goldilocks scenario in the US where inflation drops amidst robust growth are low. If US bank woes do not escalate, the Fed will continue hiking amid a contraction in US corporate profits and global trade. The recovery in China’s industrial economy will disappoint. Commodity prices are breaking down.

The growth and inflation profiles of the three central European countries are set to diverge. The outlook for Polish and Hungarian Bonds are not attractive anymore. Book profits on them. Instead, initiate a new trade: pay Polish / receive Czech 10-year swap rates.

Generative AI is a major technological breakthrough that holds tremendous economic and investment promise and will have sweeping effects on wide swaths of the economy. We are bullish on generative AI as a long-term investment theme. However, at the moment we observe hallmarks of an investment frenzy. We believe that there will be a more attractive entry point for patient investors.