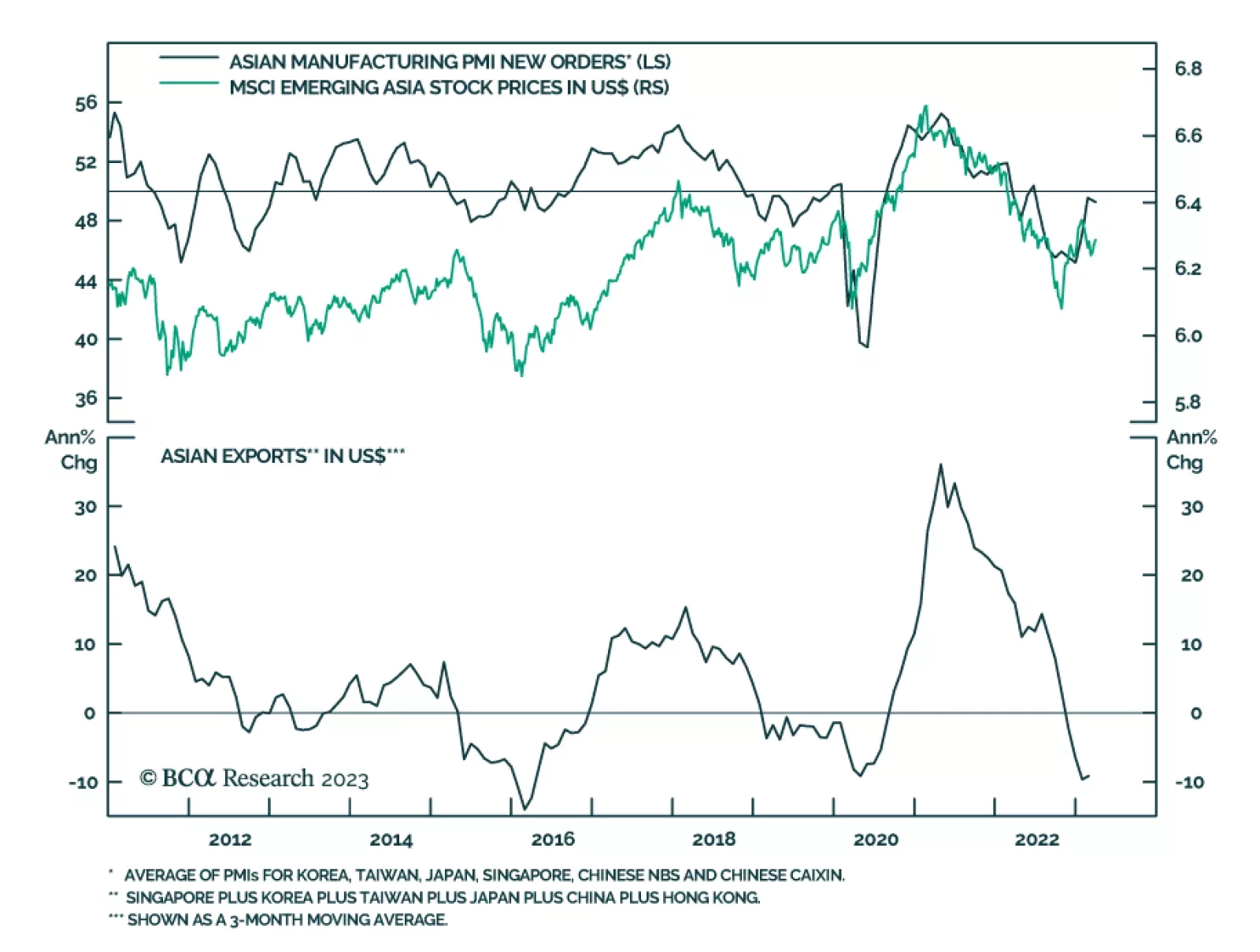

Emerging Markets

This week we present our Portfolio Allocation Summary for April 2023.

Stay defensive in the second quarter. We can see a narrow window for risky assets to outperform but we recommend investors stay wary amid high rates, supply risks, extreme uncertainty, peak polarization, and structurally rising geopolitical risk.

In Section I, we discuss the implications of the banking crisis that emerged in March. We do not expect what happened in the US or Europe to morph into a full-blown meltdown of the financial system, but this month’s events will likely lead to a further tightening in bank lending standards, raising further the odds of a US recession over the coming year. We continue to recommend an underweight stance toward risky assets versus government bonds over the coming 6-12 months, and defensive positioning within a global equity portfolio. In Section II, we estimate the impact of recently-passed US legislation on US business investment over the structural horizon and conclude that it will indeed boost capex growth over the coming several years. Assets poised to benefit from this trend will likely underperform over the coming year but should be bottom-fished following the next recession.

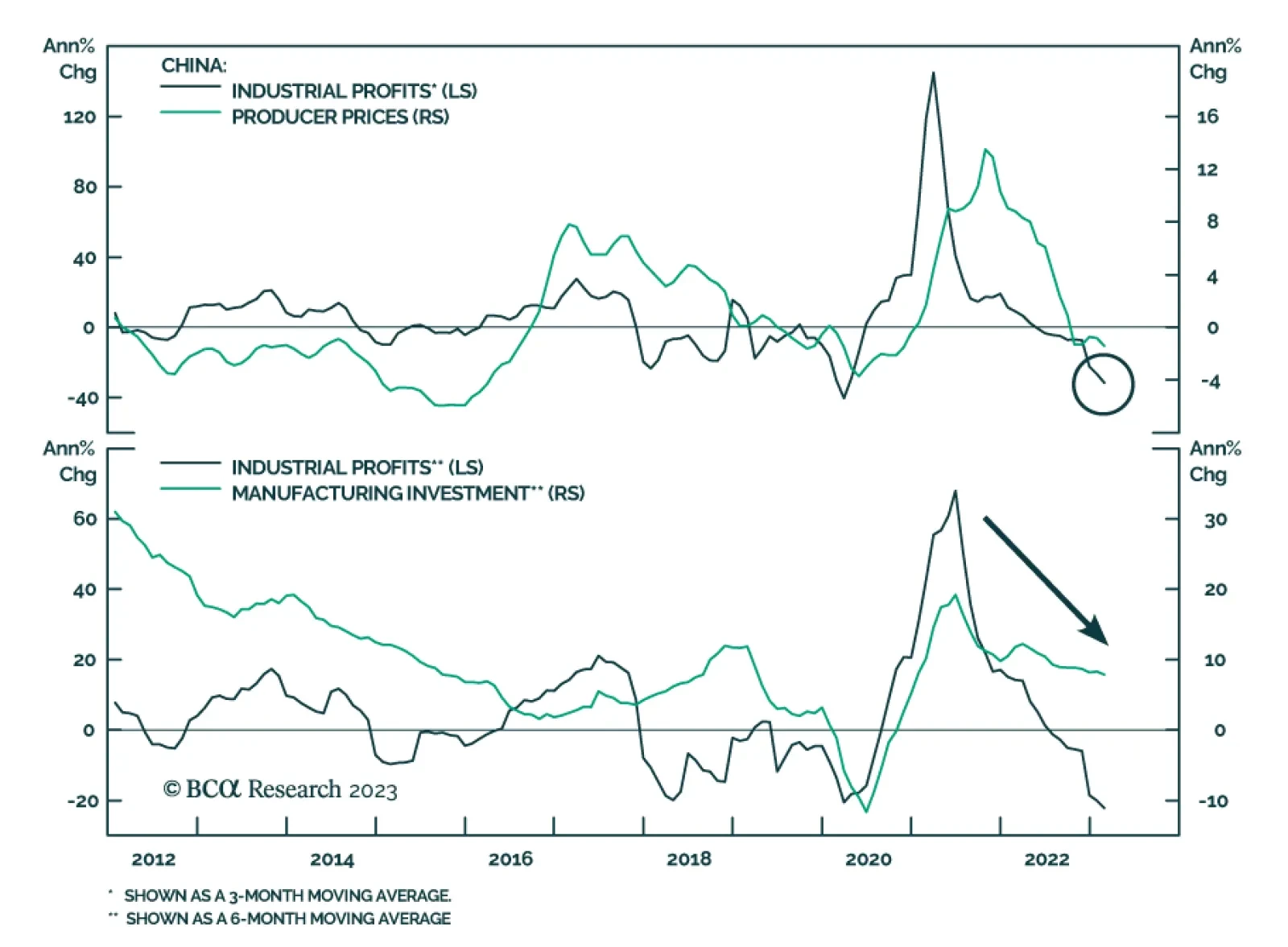

CCP officials are discussing policy options for breaking out of a deepening liquidity trap. Anything policymakers come up with will be additive to existing spending and to the multi-trillion-dollar fiscal-stimulus packages being rolled out by the EU and US. Inflationary pressures in the real economy will become embedded as increasing demand for industrial commodities meets constrained supply. Stagflation likely follows.

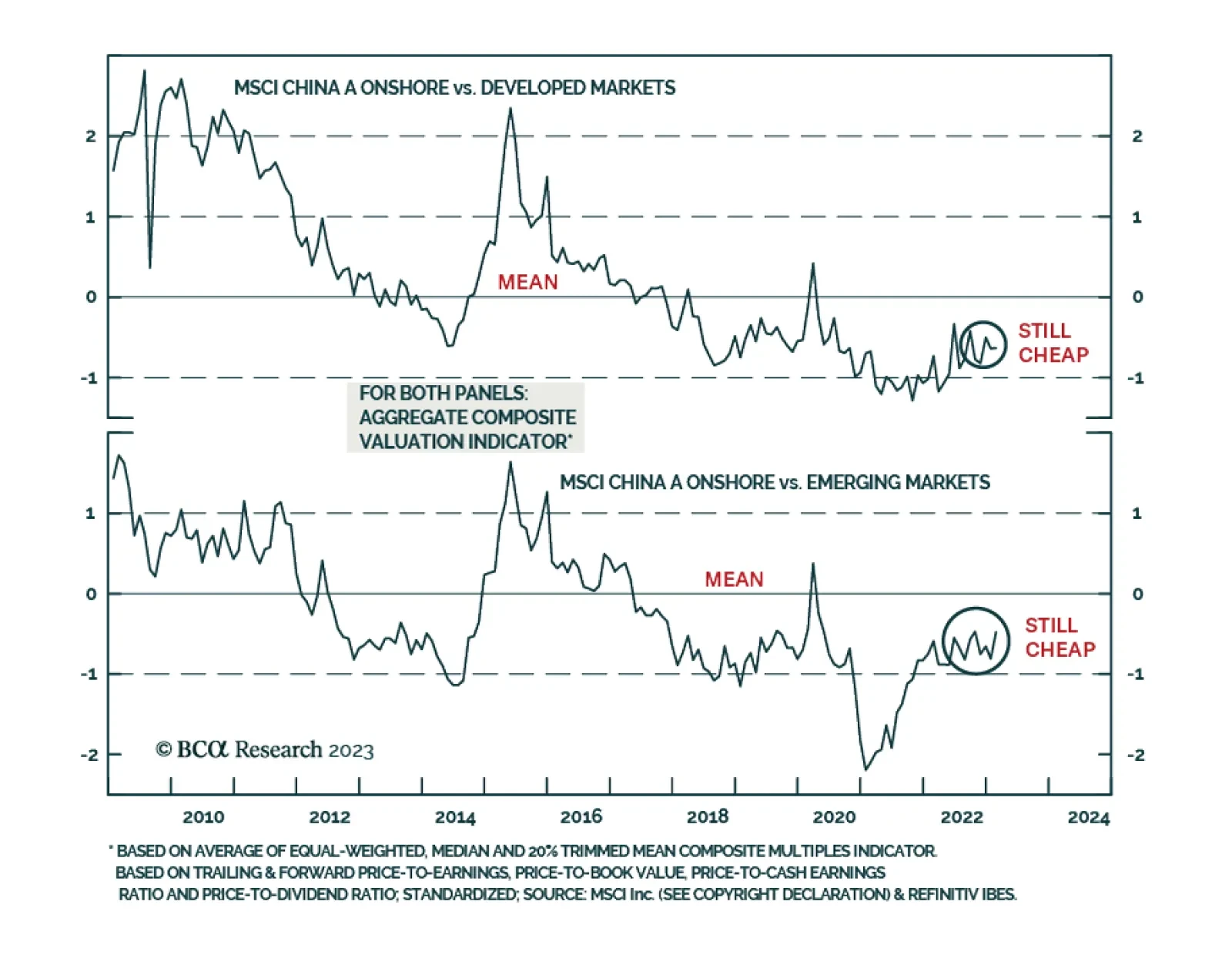

Chinese onshore stocks are attractive on a risk-reward basis relative to their global counterparts. If the global equity bear market continues, our bias is that Chinese onshore stock prices will also drop, but they will likely fall by less than their global peers.

China is launching a diplomatic charm offensive to improve relations with the world excluding the United States. But China’s proposals in Ukraine and the Middle East are overrated in their ability to restore global stability and reduce geopolitical risk.

Have global equity markets reached a riot point? Is the Fed going on hold a sufficient condition for stocks to stage a cyclical rally? If not, what would be needed to produce such a rally? Does the Fed’s recent balance sheet expansion foreshadow a rise in the US money supply? This report provides answers to all these questions.