Emerging Markets

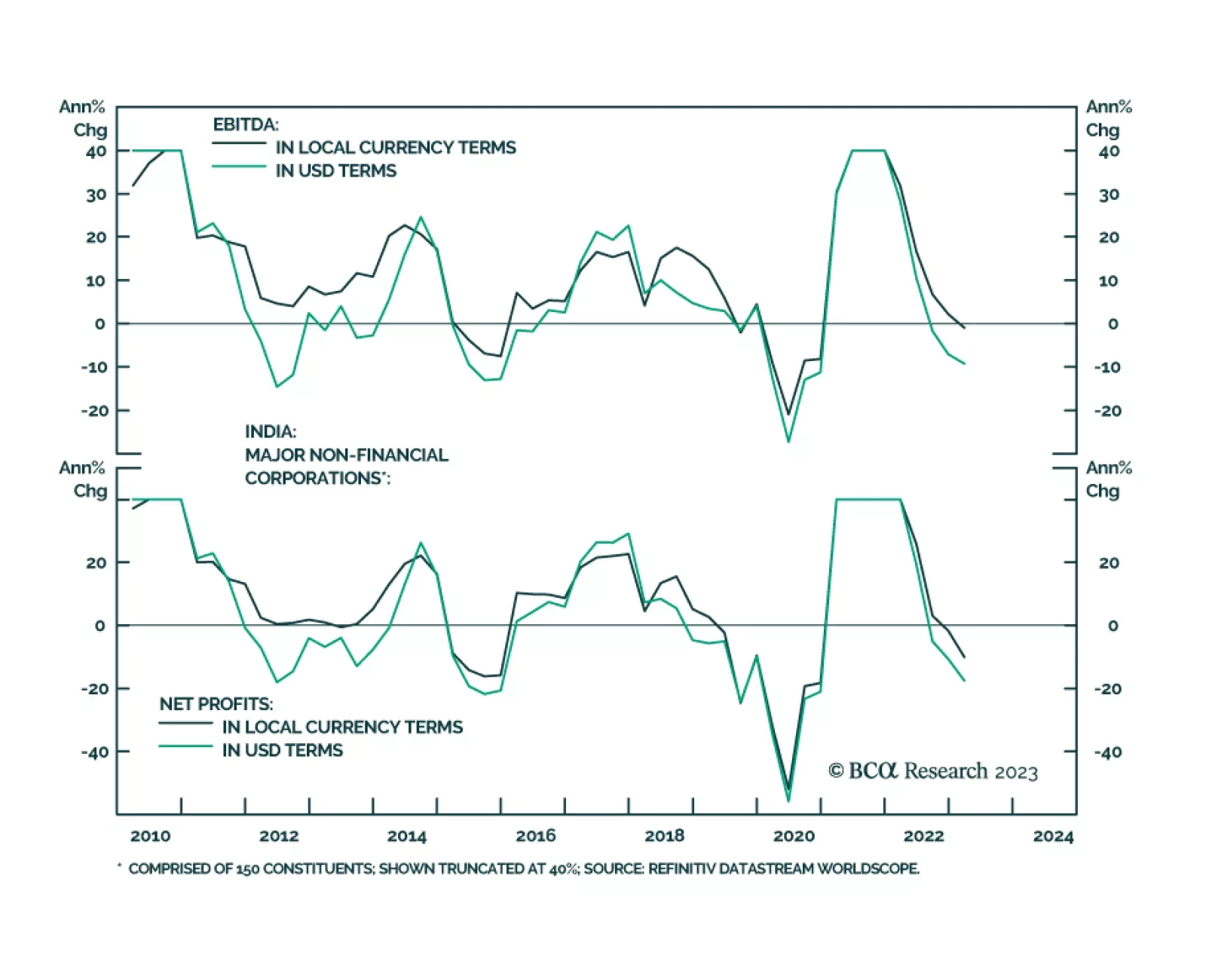

Indian EPS growth is set for major disappointments vis-à-vis the lofty expectations. Weak domestic demand amid tight fiscal and monetary policy entails more downside in stock prices. Stay underweight.

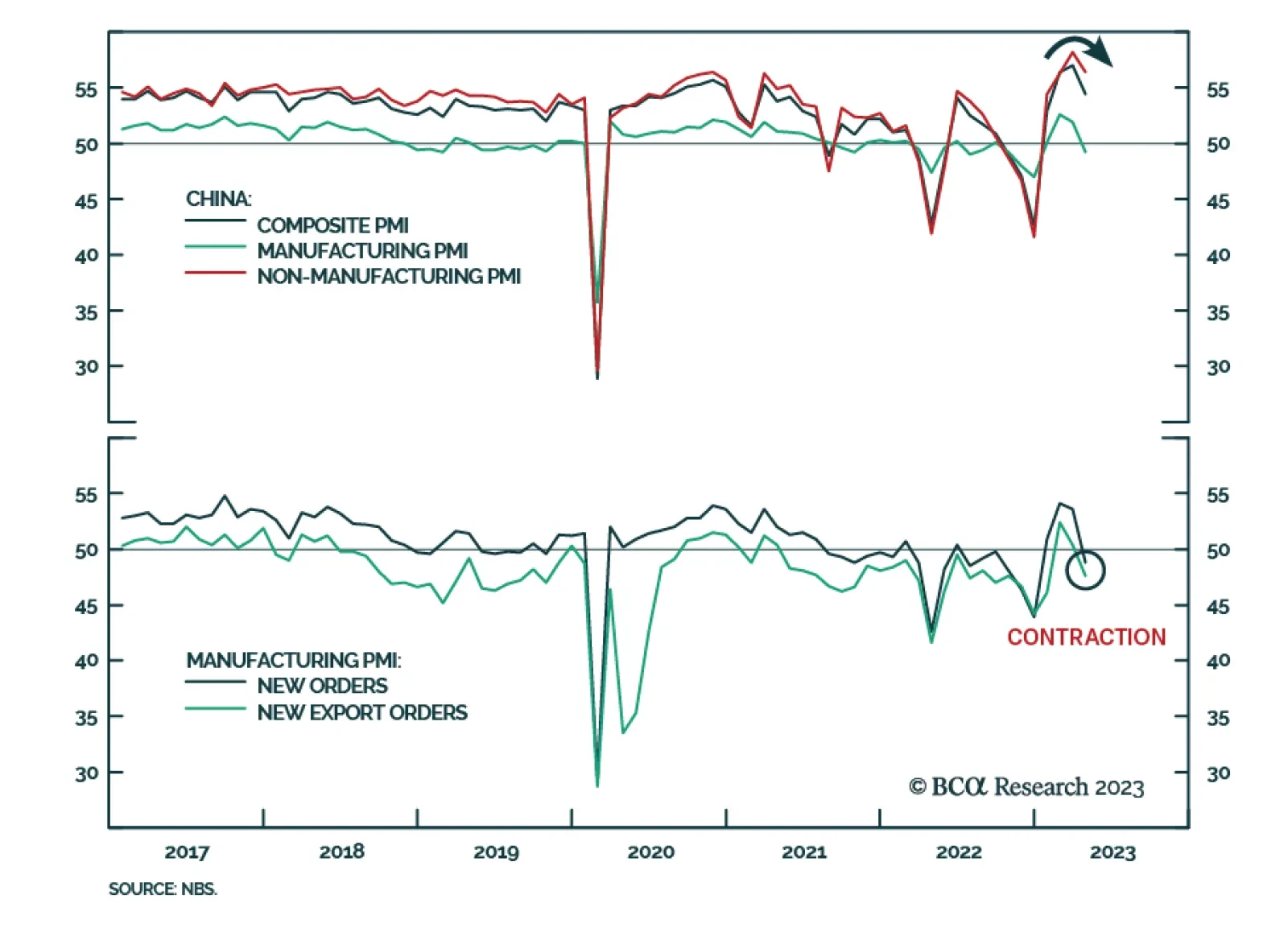

China’s reopening, combined with a slew of pro-consumption policy stimuli, will likely boost household consumption by 10% in nominal terms in 2023 from a year ago. Some of the hardest hit service sectors during the pandemic will experience a strong recovery. Within the A-share market, investors should overweight the consumer discretionary sector versus the Chinese CSI300 benchmark.

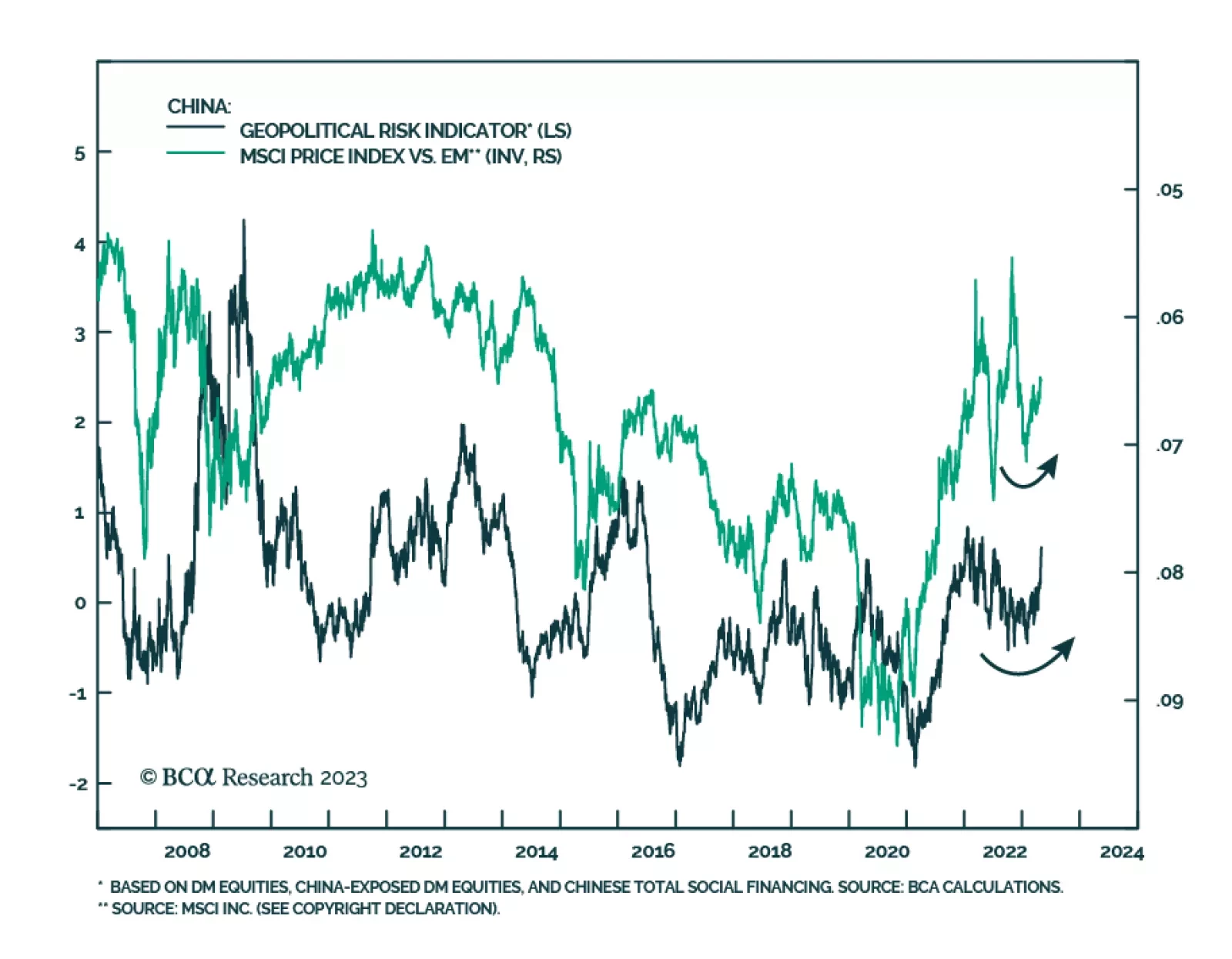

Macro and geopolitical risks may spoil the narrow window for a stock market rally before recessionary trends rise to the fore.

The risk-reward of the US dollar is currently positive. If a US recession is not imminent, then US bond yields will move higher, thus supporting the greenback. If the US enters a recession soon, the US dollar will benefit because it is counter-cyclical. Besides, the US dollar has not been as weak as the DXY index suggests.

This week we present our Portfolio Allocation Summary for May 2023.