Emerging Markets

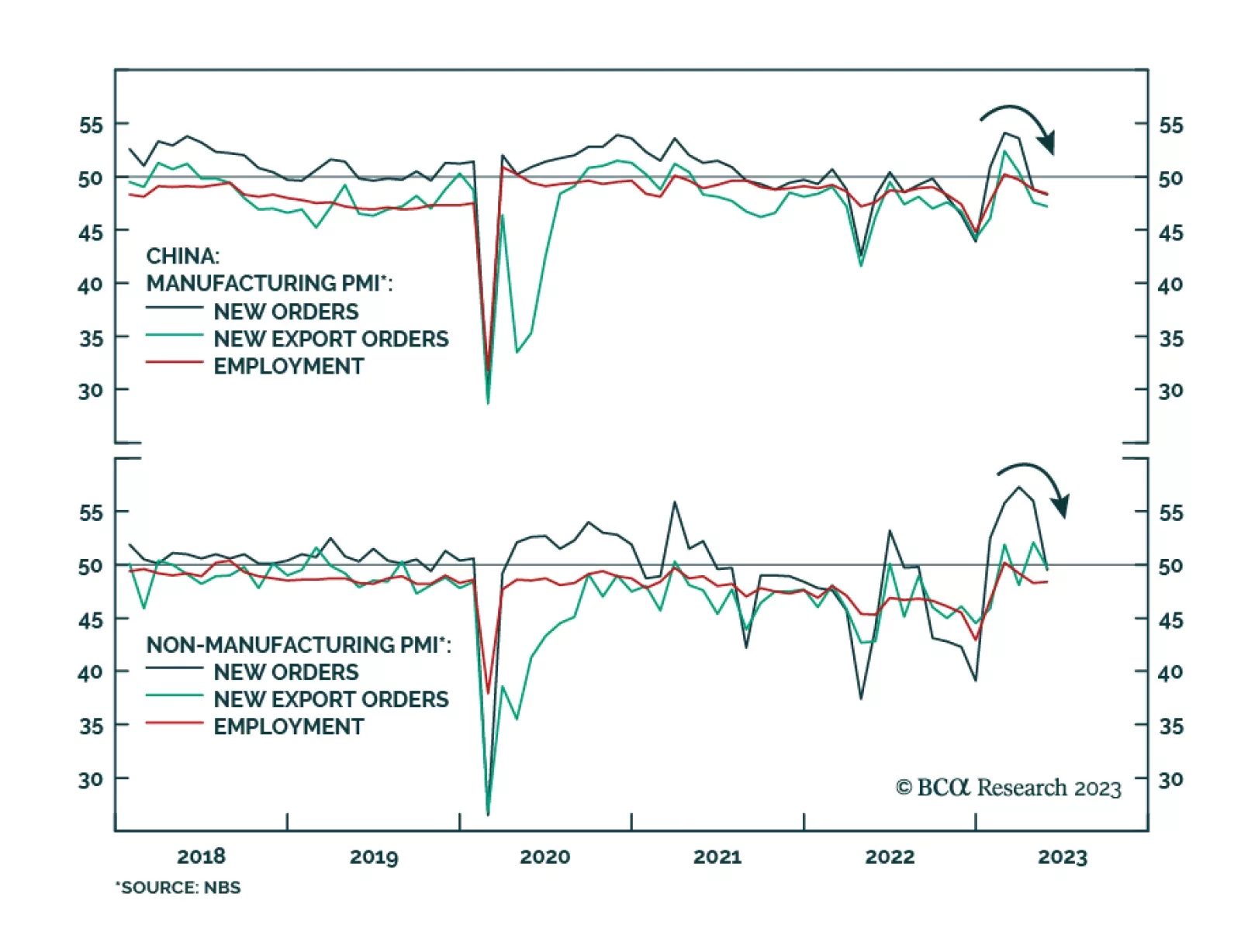

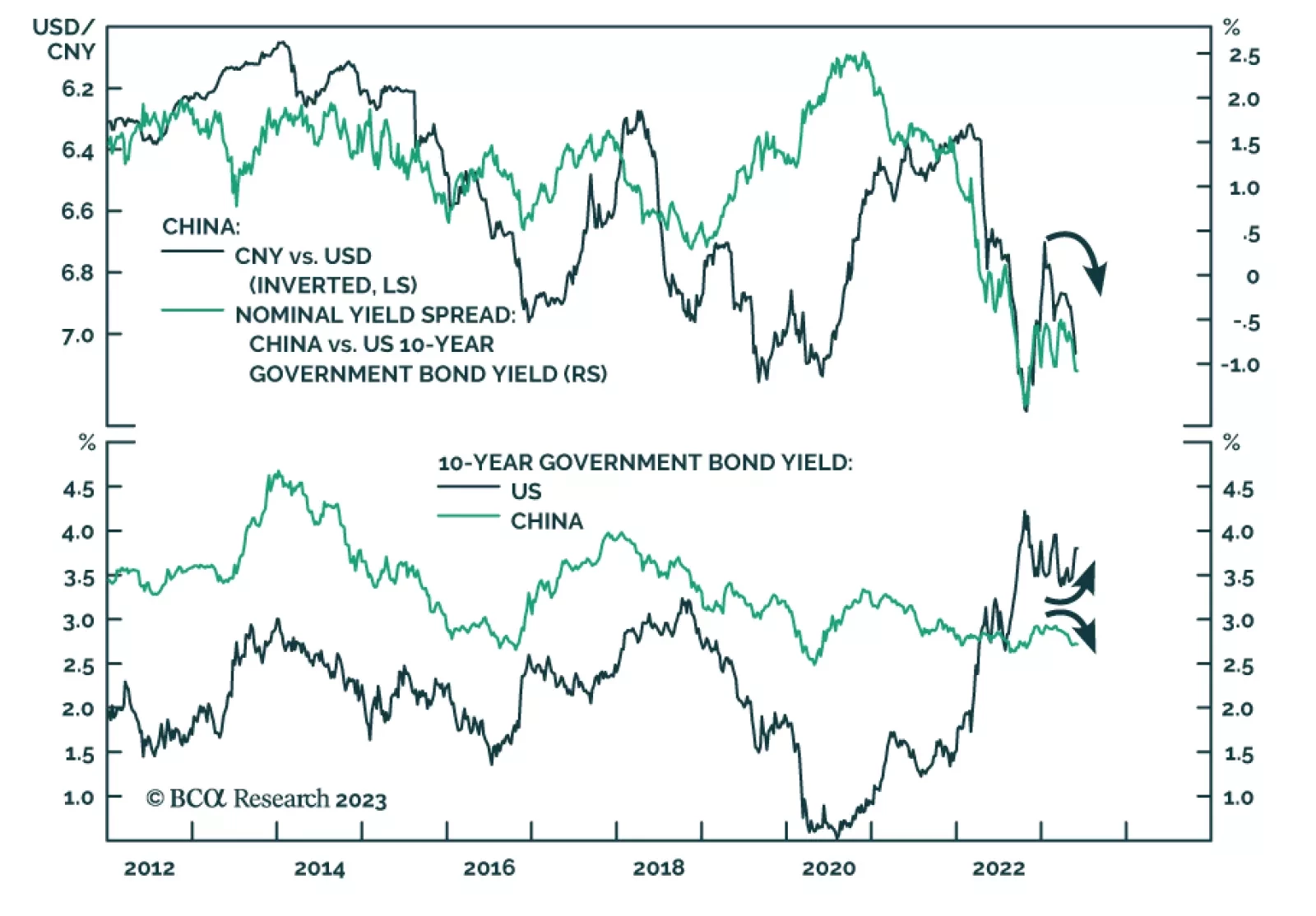

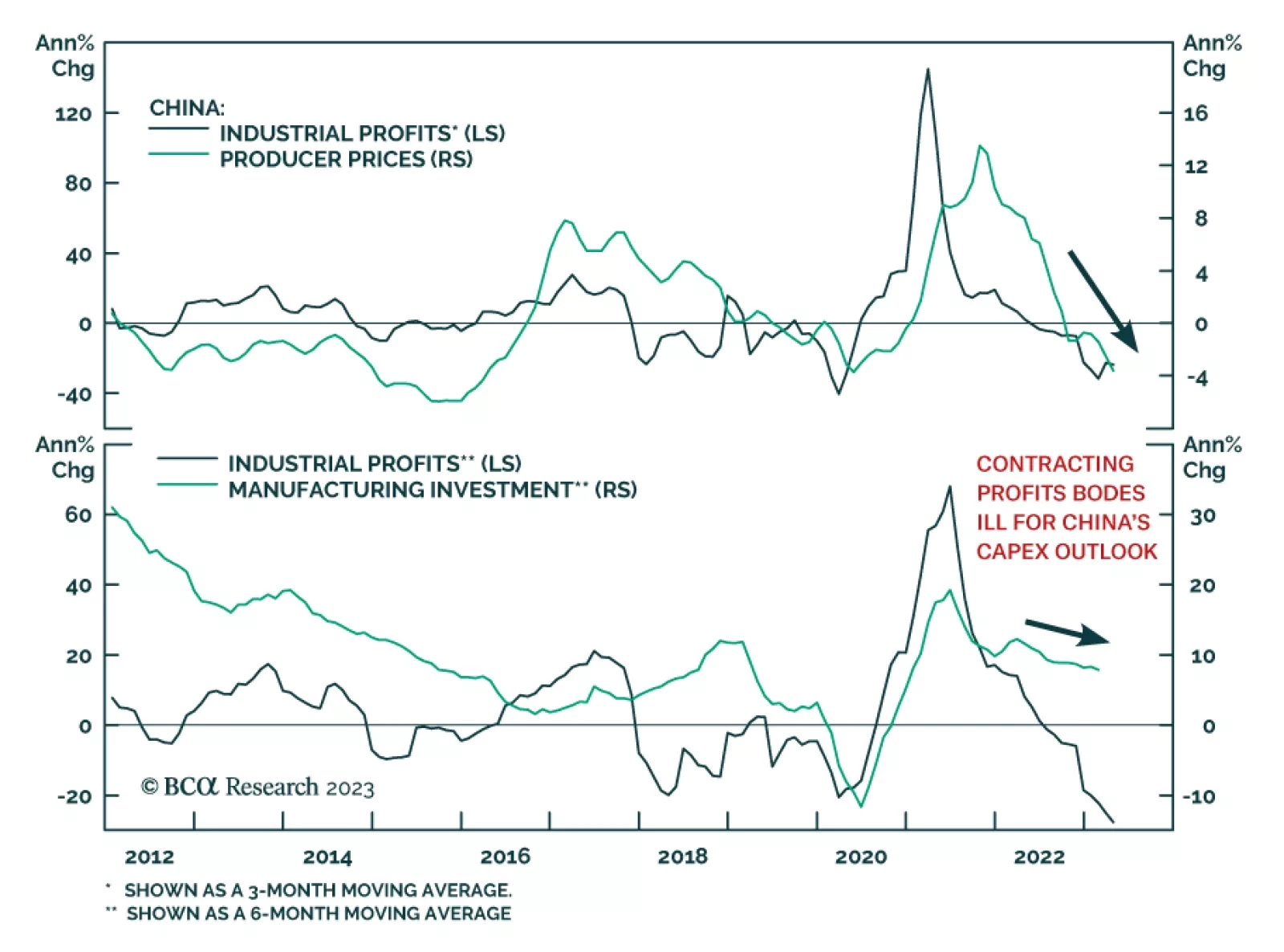

Symptoms of a liquidity trap for Chinese households are appearing. Our proprietary indicators for the marginal propensity to spend among households and enterprises continue falling. There has been a paradigm shift in Beijing’s approach to policy stimulus. Authorities will be slow to introduce large stimulus. Hence, China-related financial markets are set to fall further.

Risk assets would perform well over 12 months only if inflation falls to 2% without triggering a recession. That would be unprecedented. We recommend investors stay defensive.

The CCP is poised to roll out a re-boot of China’s economy that will focus on its comparative advantage in the processing of base metals – particularly copper – and the export of metals-intensive products like EVs. The re-boot will emphasize deeper policy coordination to revive construction, manufacturing, exports and renewed efforts to attract and retain FDI. This will be bullish for commodities – particularly conventional energy and metals – as funding flows to SOEs.

Expectations for oil demand growth through 2023-24 are way too optimistic. Until these expectations fall to -0.5-1 percent, the oil price has further downside. Plus: collapsed complexity confirms that AI is in a mania, while basic materials stocks and ZAR/EUR are rebound candidates.

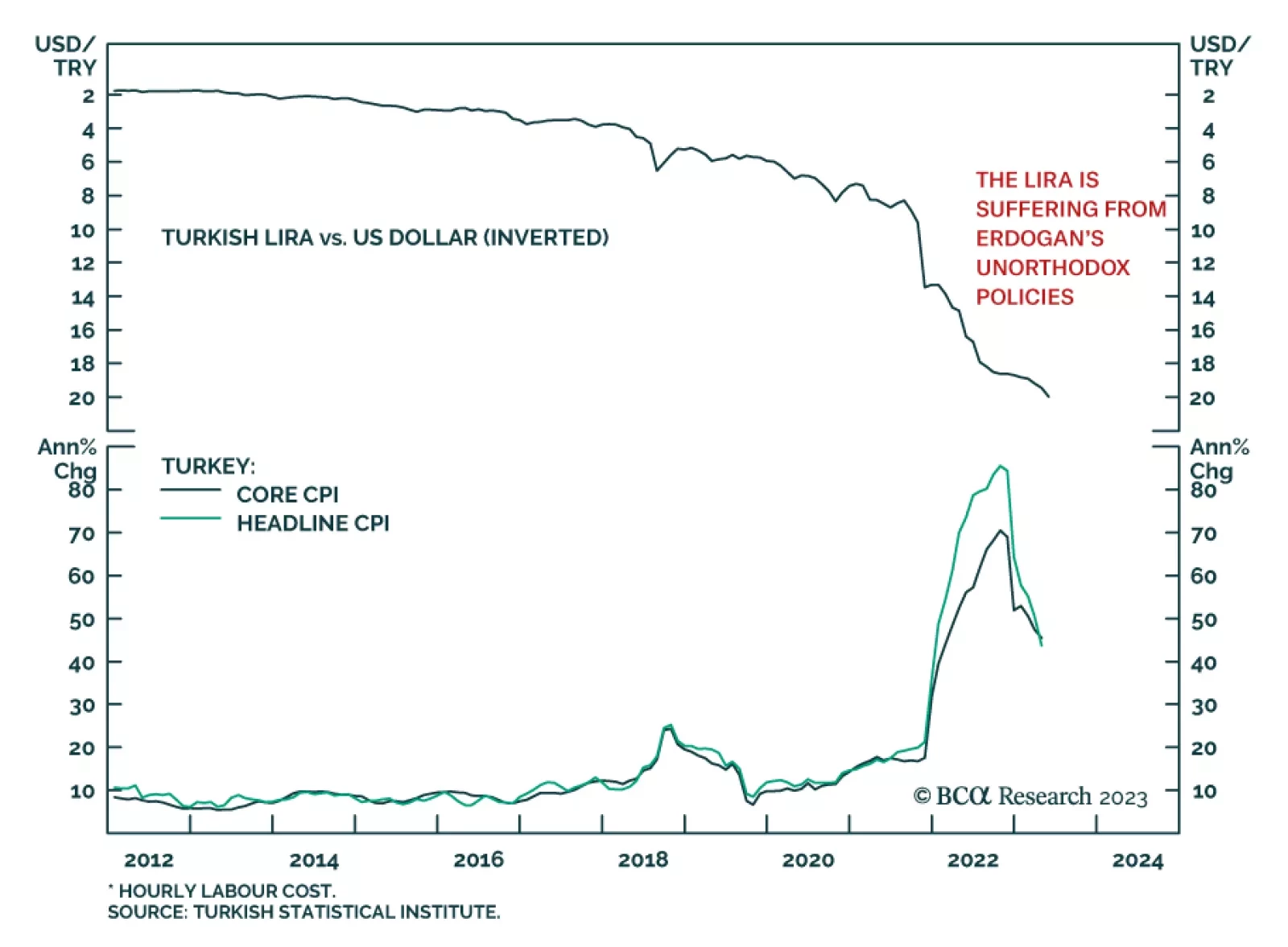

President Erdogan and the Justice and Development Party emerged as the winner of the Turkish general election which was concluded yesterday. This victory means that their expansive policies of the past decade will continue, and Turkish assets will suffer. Across the Aegean, the Greeks voted to reelect the New Democrats under the leadership of Prime Minister Mitsotakis. Their fiscal prudence and structural reforms will be continued as voters had rewarded them with another term in office. Go long Greek versus Turkish equities.

We expect the CCP to pivot toward more fiscal stimulus – and less credit stimulus – this year, which will put a bid under energy and metals prices. On the back of this view, at tonight’s close we are getting long 4Q23 Brent futures vs short 4Q24 futures, and re-establishing our XME and PICK ETF positions expecting higher prices and steeper backwardations in metals markets. We also are getting long 4Q23 COMEX copper vs short 4Q24 futures.