Currencies

Markets keep buying the dip because liquidity remains plentiful. That buffer lasts through 2026; the bigger question is what happens when it thins in 2027.

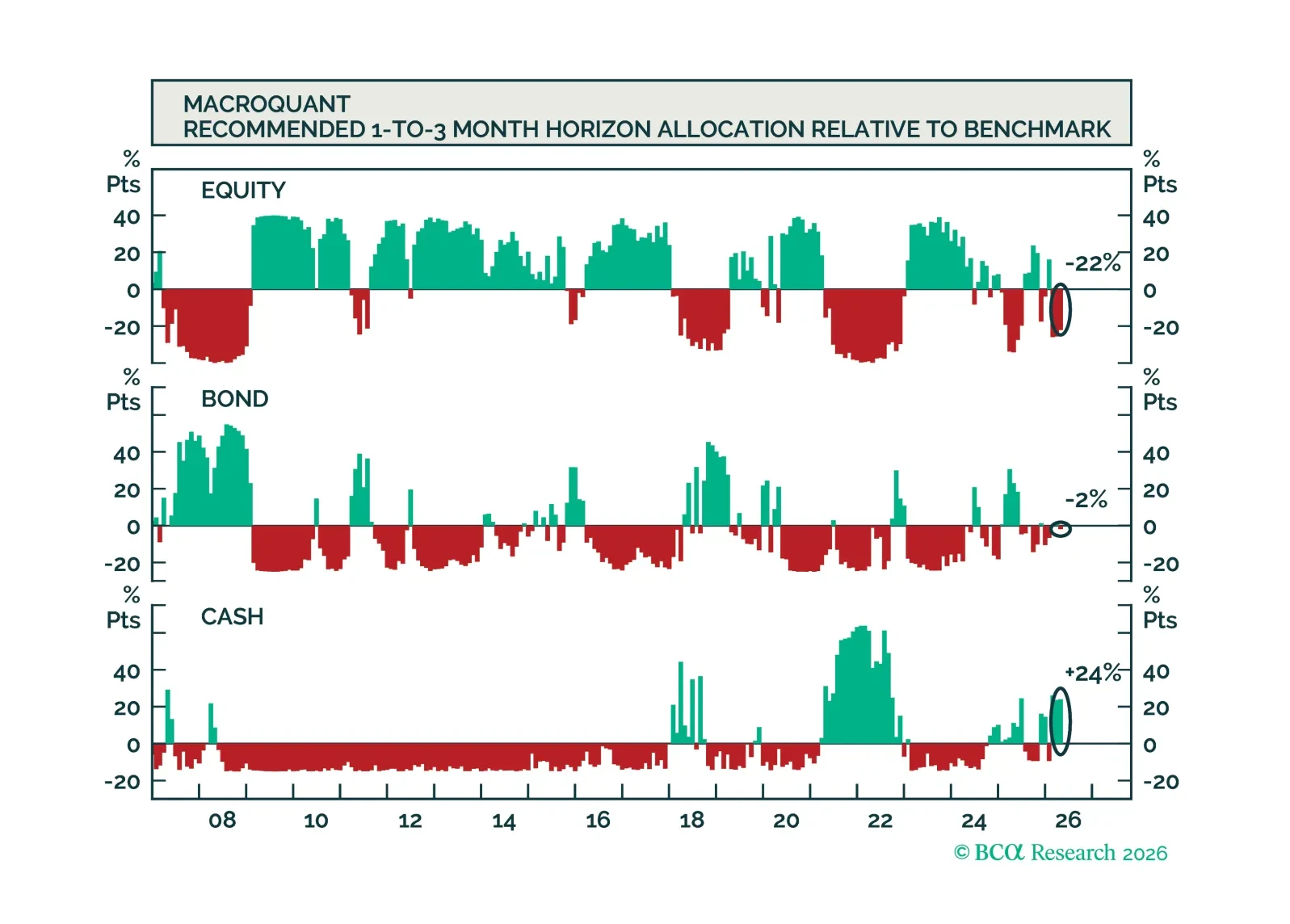

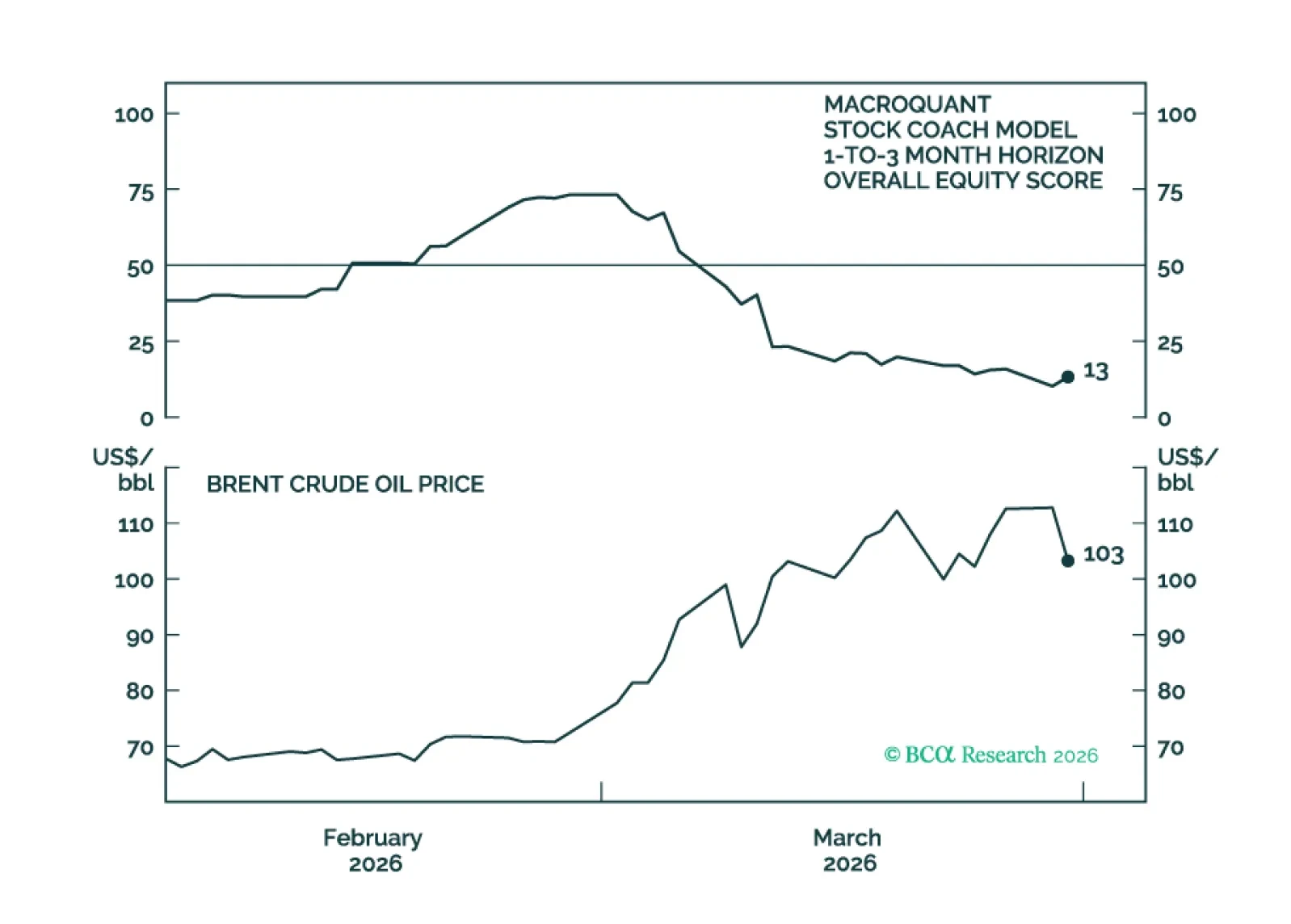

MacroQuant recommends a slight underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is very positive on the US dollar, downgrades gold to underweight, upgrades copper to overweight, and remains very bullish on oil.

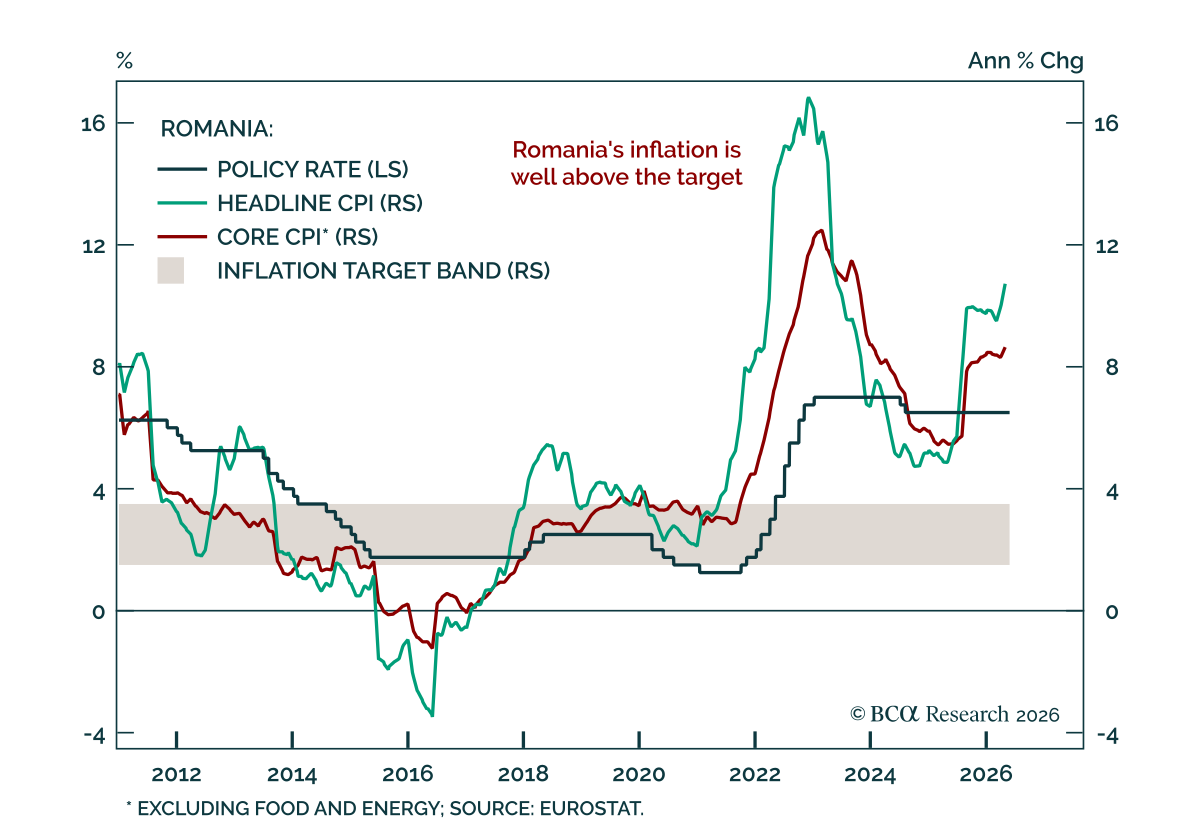

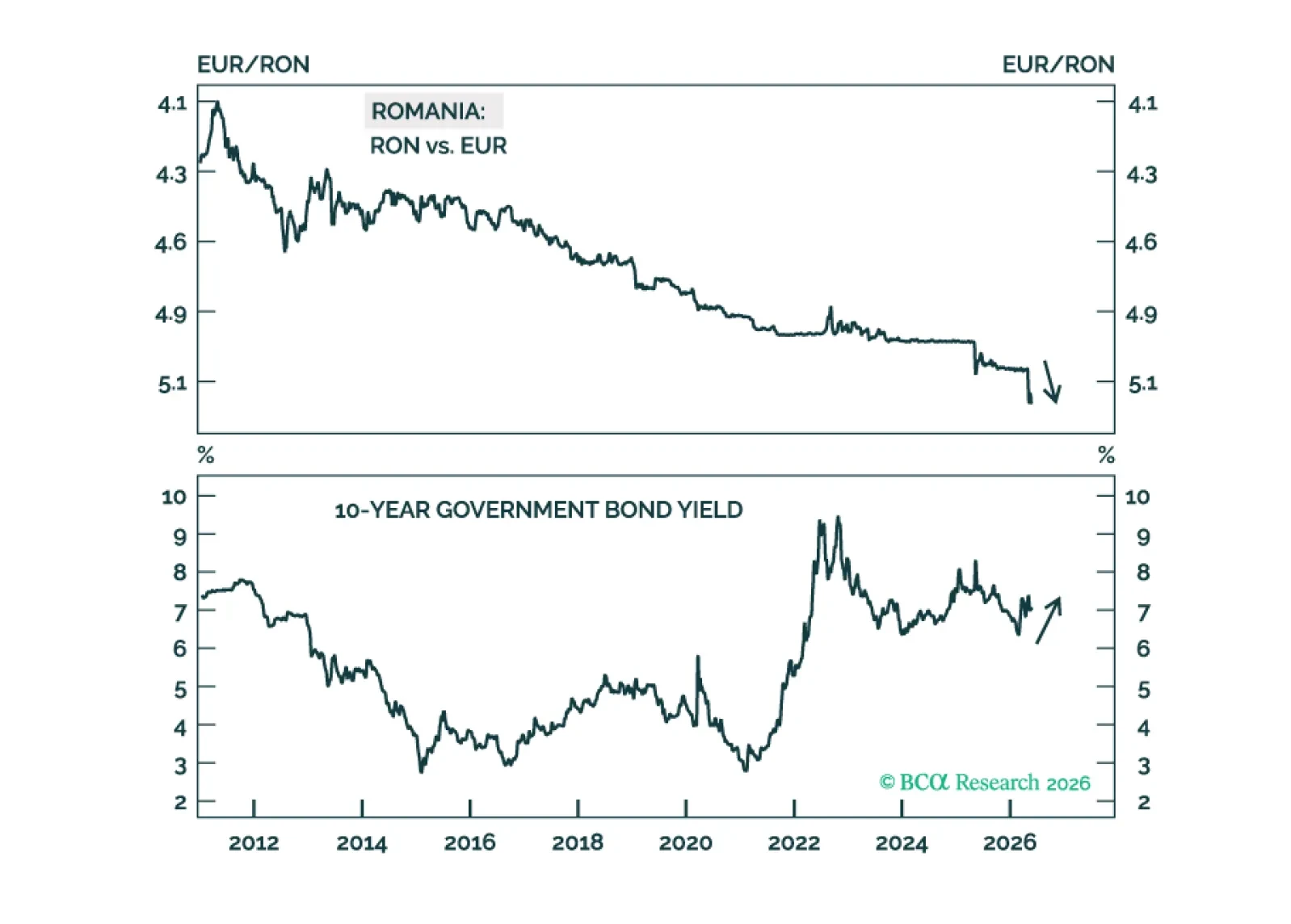

In Romania, large fiscal and current account deficits, high inflation, negative real rates, an overvalued exchange rate, and deteriorating growth point to budding currency devaluation. Investors should short the Romanian currency versus the euro and underweight Romanian local bonds, equities, and sovereign credit.

MacroQuant recommends an underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is neutral-to-slightly positive on the US dollar, remains neutral on gold, upgrades copper to neutral, and is very bullish on oil.

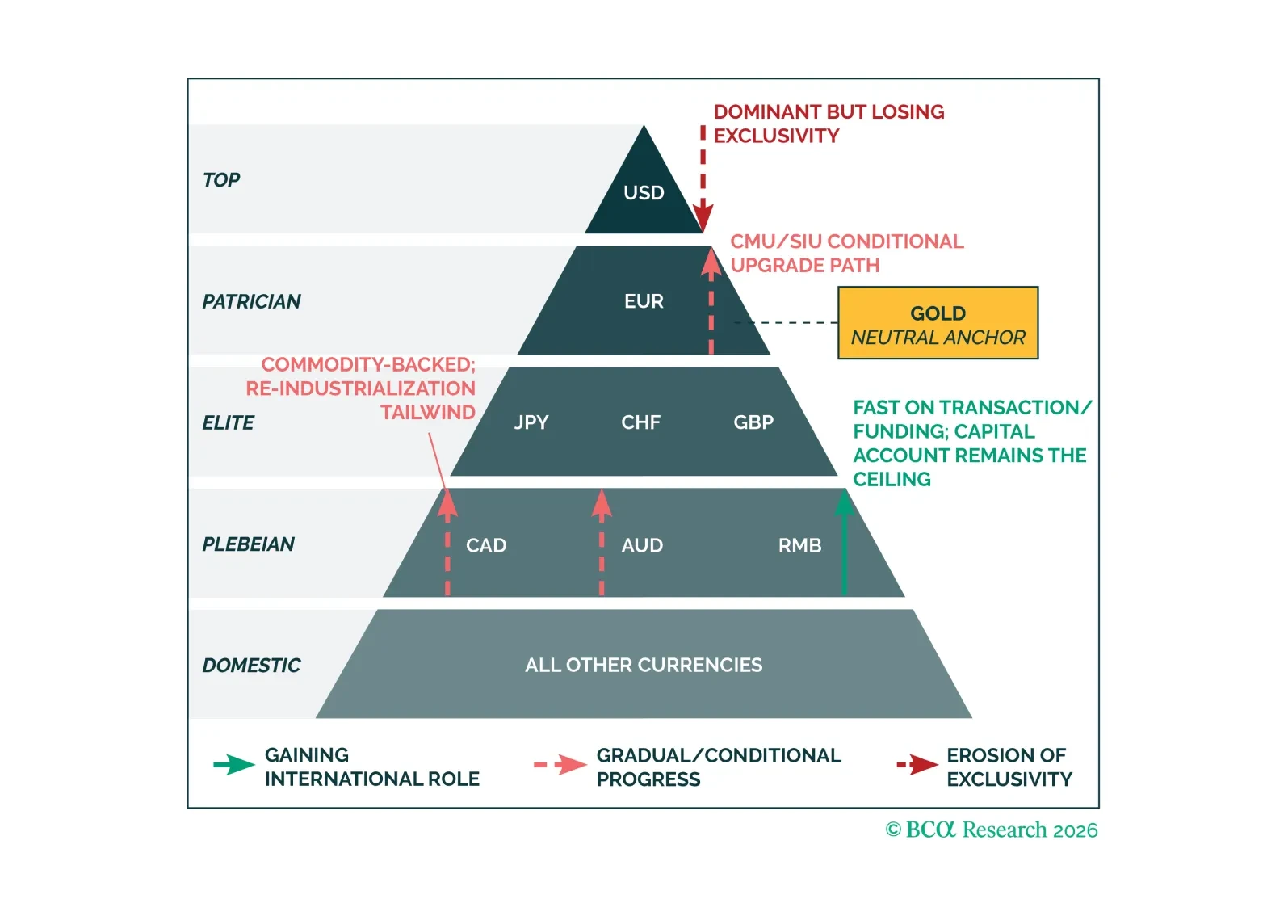

The debate over “what replaces the dollar” is misguided. The real shift is toward a multi-anchor system where reserve functions fragment. That changes everything from term premia to cross-asset correlations. The implication: portfolios built for the old regime are already behind the curve.

MacroQuant recommends a strong underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, has become neutral-to-slightly positive on the US dollar, has downgraded gold to neutral and copper to a strong underweight, and is bullish on oil.