Commodities & Energy Sector

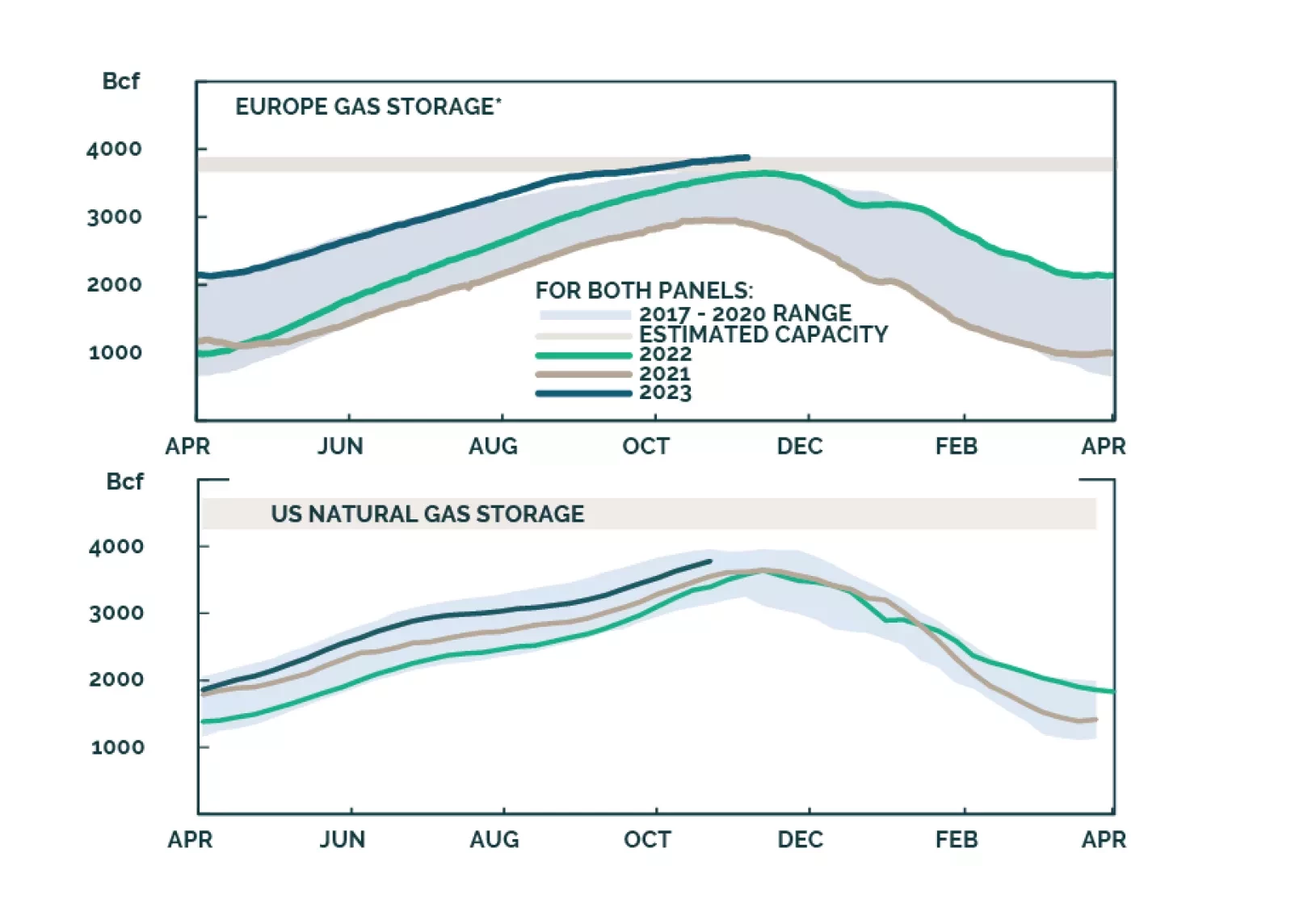

Natural gas storage levels in the US and EU are sufficient to balance flowing supply and demand this winter, assuming normal weather. China continues to invest in domestic production, and to diversify supply sources to compensate for a lack of storage. Longer-term Qatari contracts are giving higher weight to natgas trading hub prices. We remain long the XOP ETF to retain exposure to fossil-fuel producers supplying DM and EM economies with natgas beyond the 2050 net-zero-emissions goals advanced by the IEA.

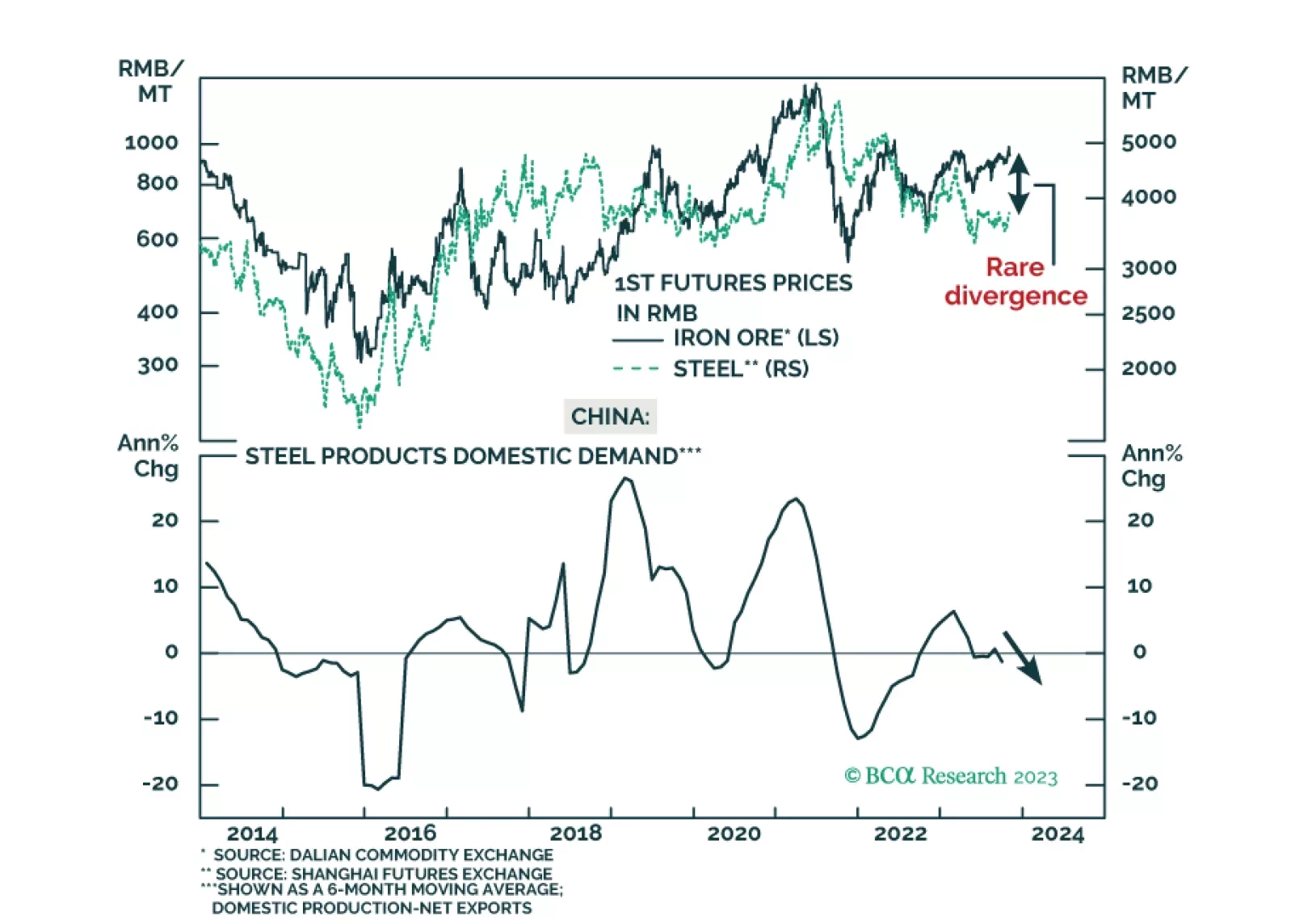

Increasing iron ore prices coupled with declining steel prices represent an unsustainable disparity. Iron ore prices will pivot downward in the next six months. A sizeable reduction in China’s steel production will likely occur, reducing global iron ore demand. Meanwhile, global iron ore supply will increase moderately.

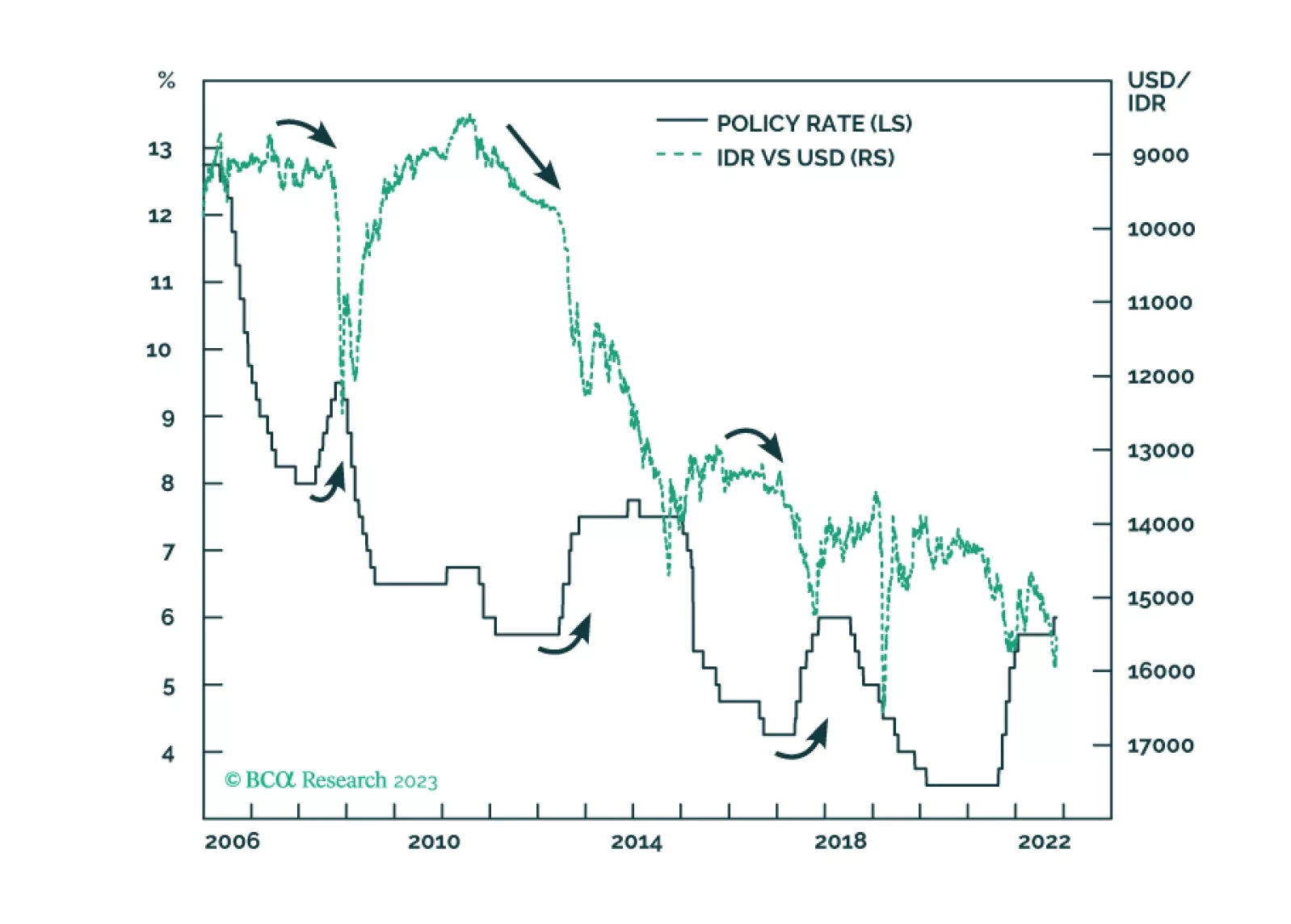

Despite very low inflation, Bank Indonesia raised its policy rates last month to support the currency. The strategy did not work before and will not work now. Stay short the rupiah.

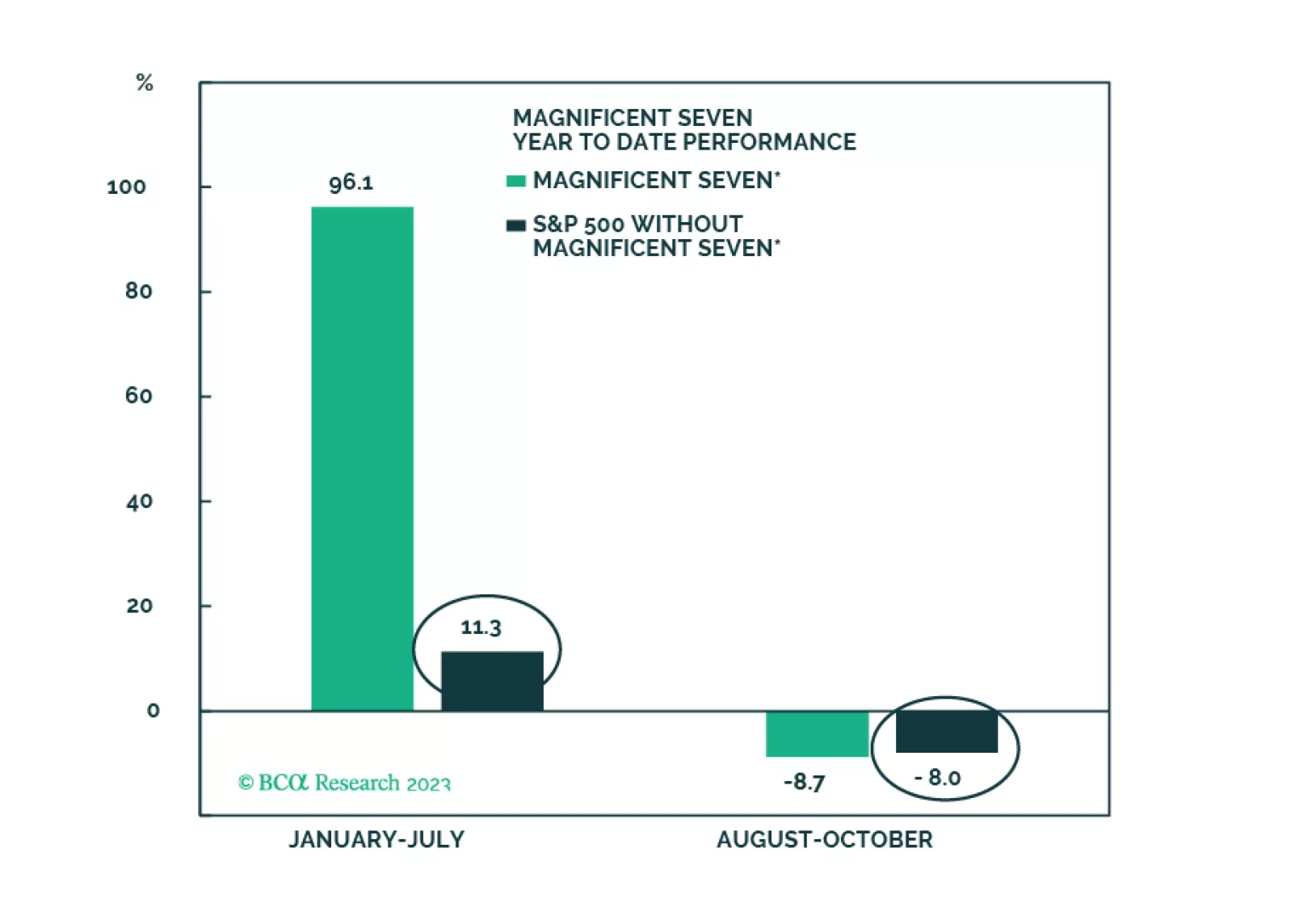

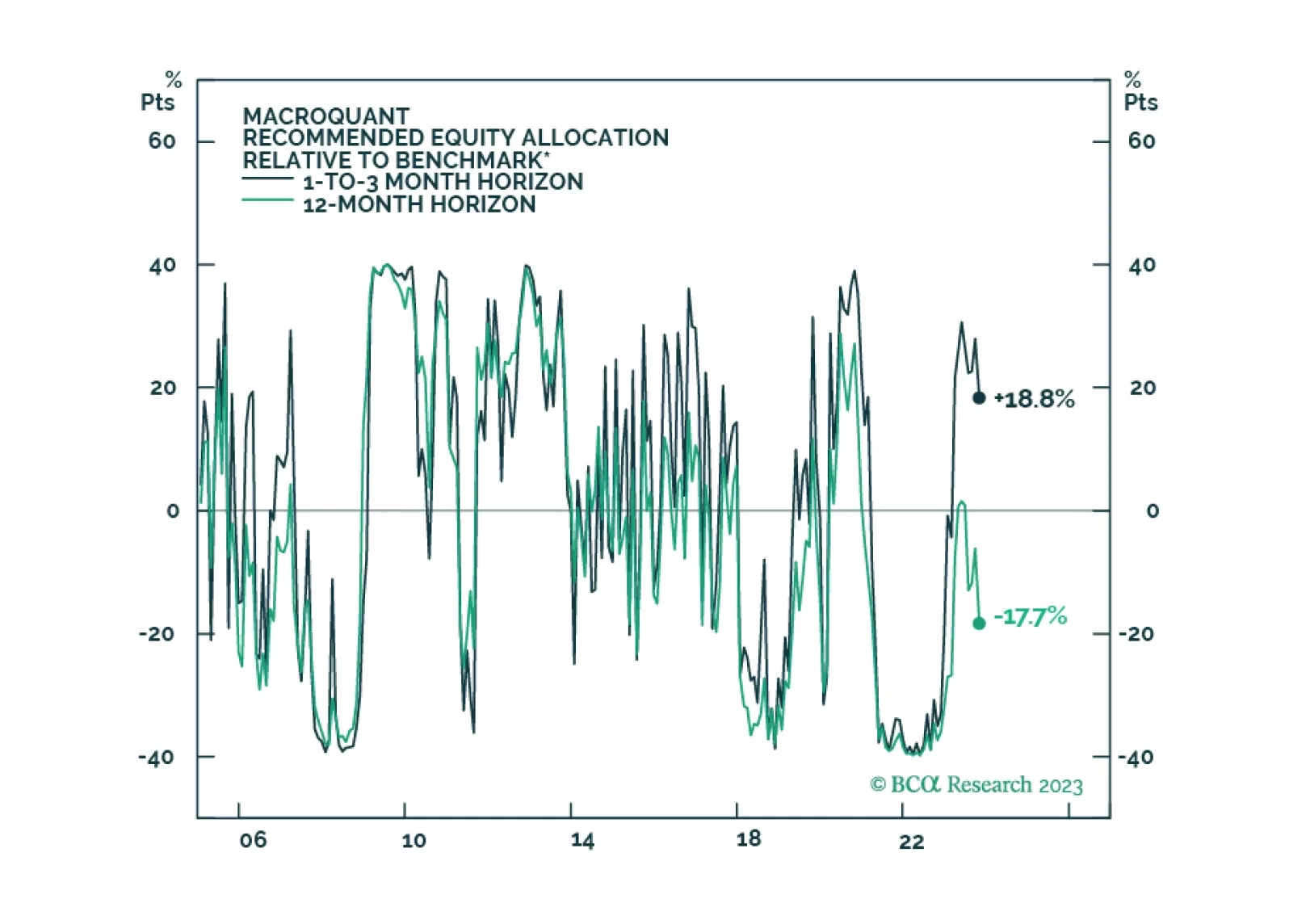

The Vicious Troika remains a long-term threat, but over the short term, rates will likely have another leg down on growth concerns, offering support to equities, which are now fairly valued and are no longer overbought. Longer-term outlook remains negative. The Magnificent Seven will likely lead a tactical rebound. Overweight Growth vs Value and FSemis.

We are approaching another phase transition from boom to bust. Stocks should rally into year-end, but investors should look to reduce equity exposure early next year while increasing bond exposure.

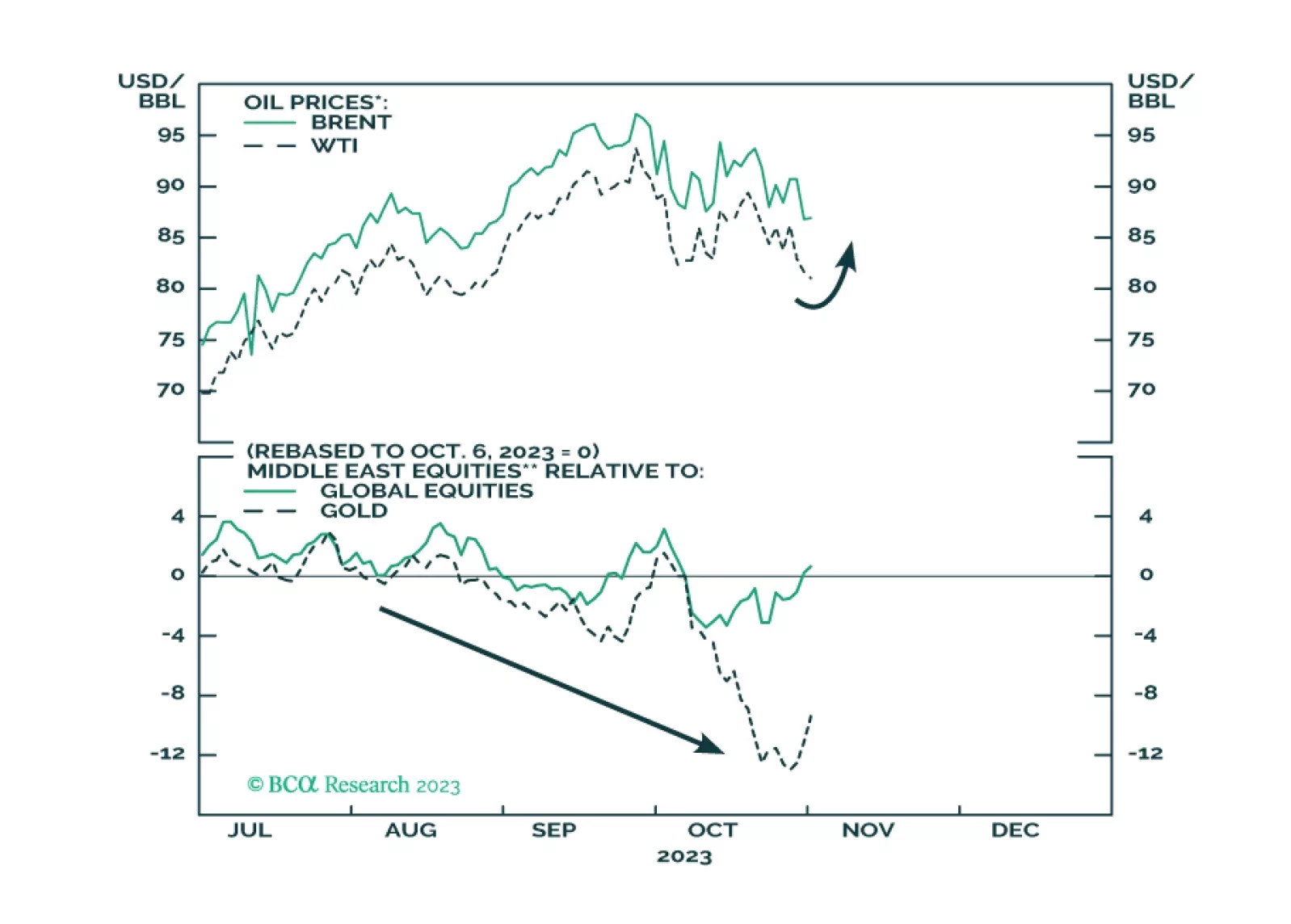

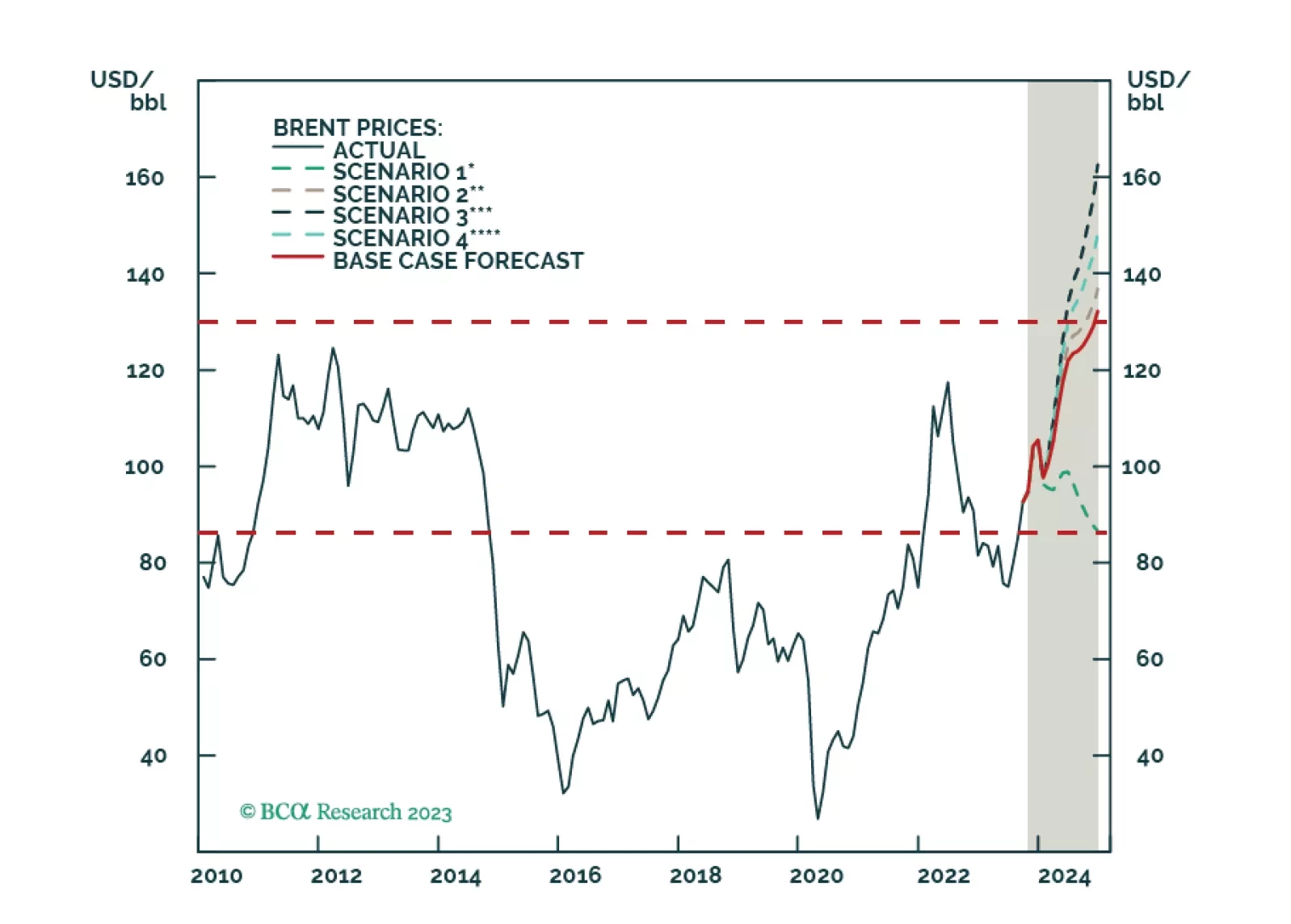

Investors should reduce risk, increase allocation to safe havens, and brace for oil price volatility and supply disruptions stemming from the Middle East over the next zero-to-12 months.

Economic fragmentation will accelerate in the wake of the Israel-Hamas and Russia-Ukraine wars. China’s fis-cal support for its economy; a still-strong US economy, and the preparation for a wider war in the Middle East involving Iran will elevate volatility and bias oil prices upward. We remain long equity and commodity exposure via the XOP, XME and COMT ETFs.

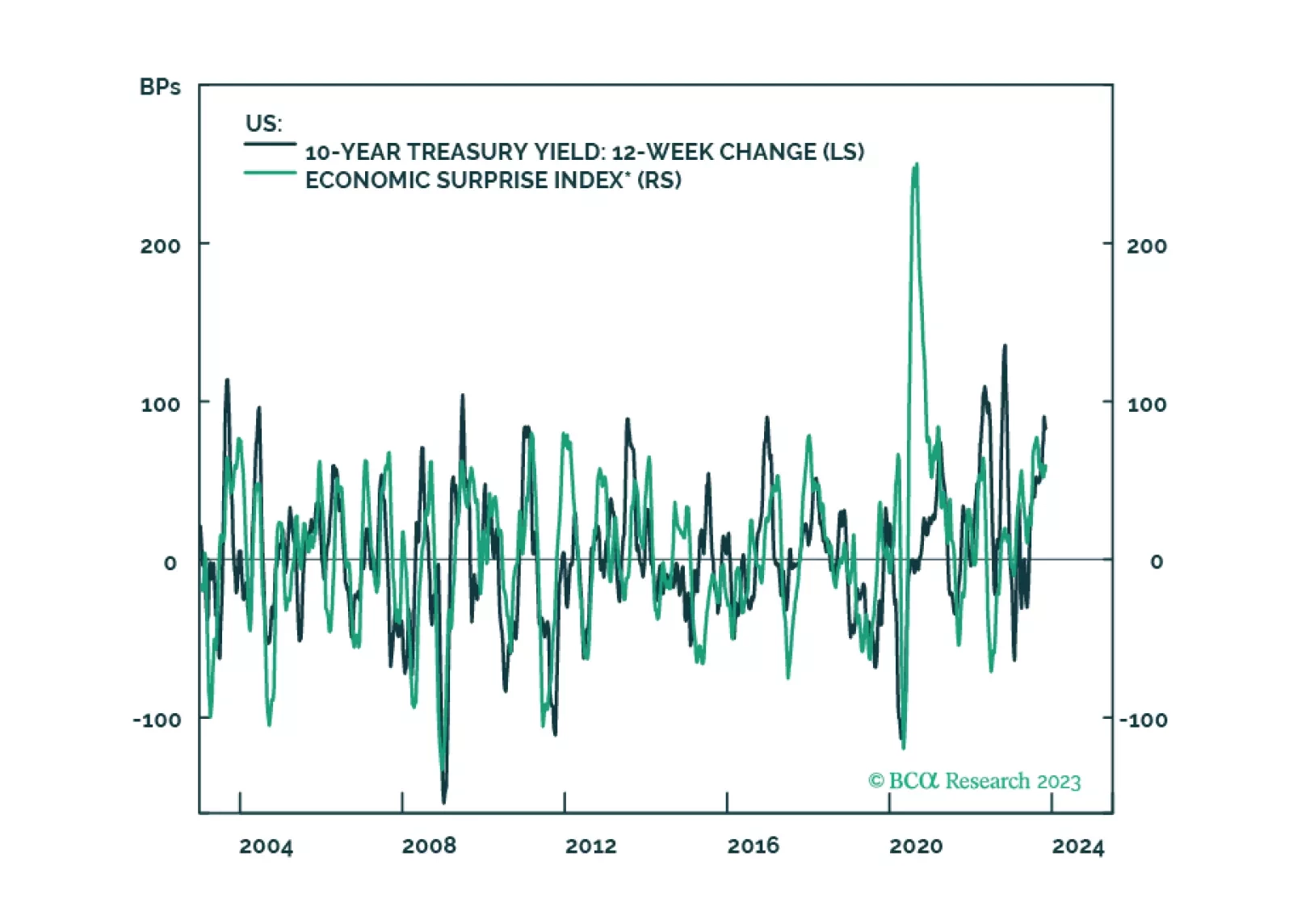

High interest rates will eventually cause growth to slow. Signs of stress are already starting to show. Stay cautiously positioned.

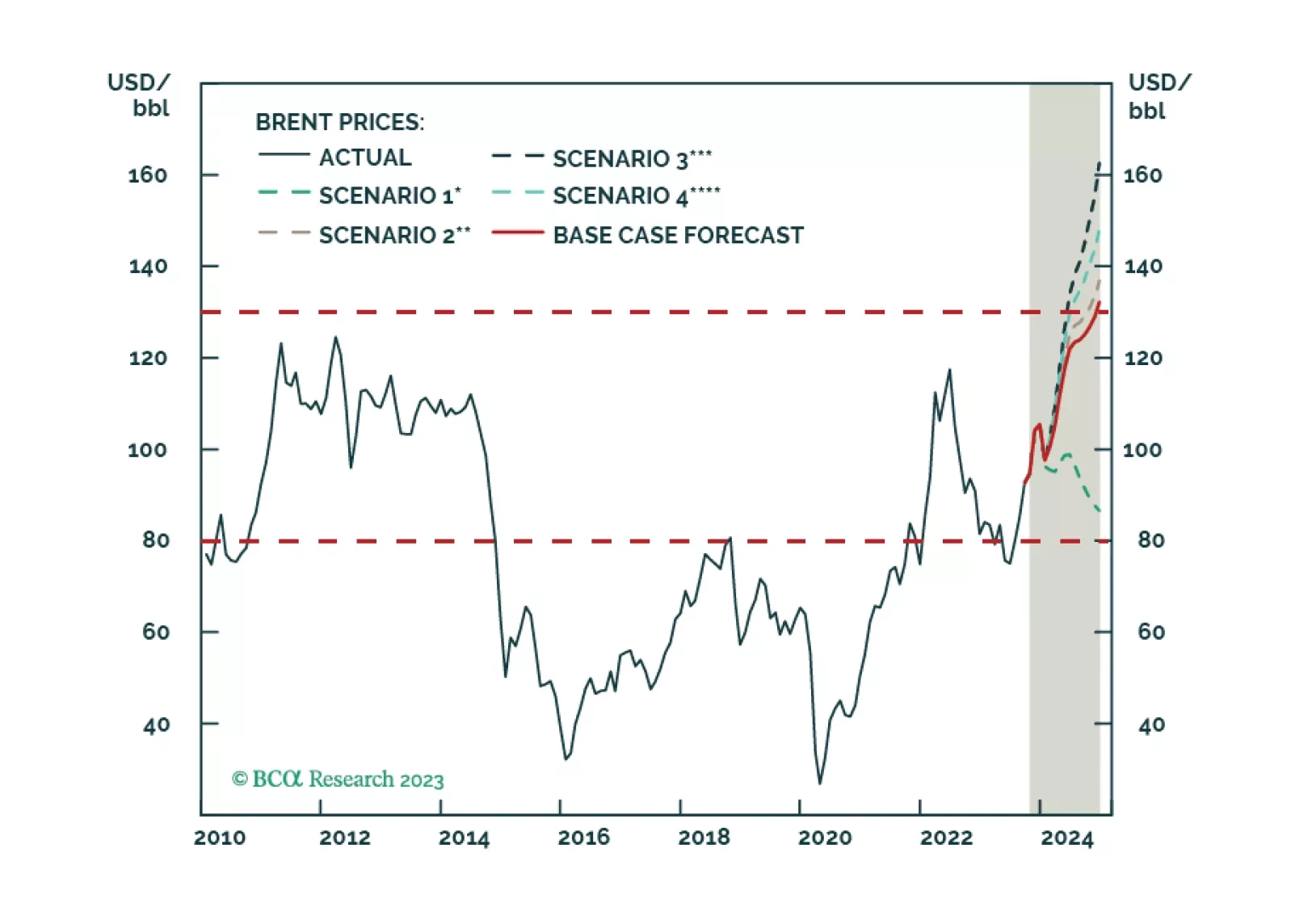

The US and core OPEC 2.0 are – wittingly or not – laying the groundwork for a price band with a floor and cap on oil prices – at $79/bbl and $130/bbl, respectively – “at least” to May 2024. This accommodates multiple goals for both. To meaningfully support policy, the US would need to scale up purchases to refill its SPR. We remain long the XOP and COMT ETFs for direct exposure to energy E+P equities and commodities.