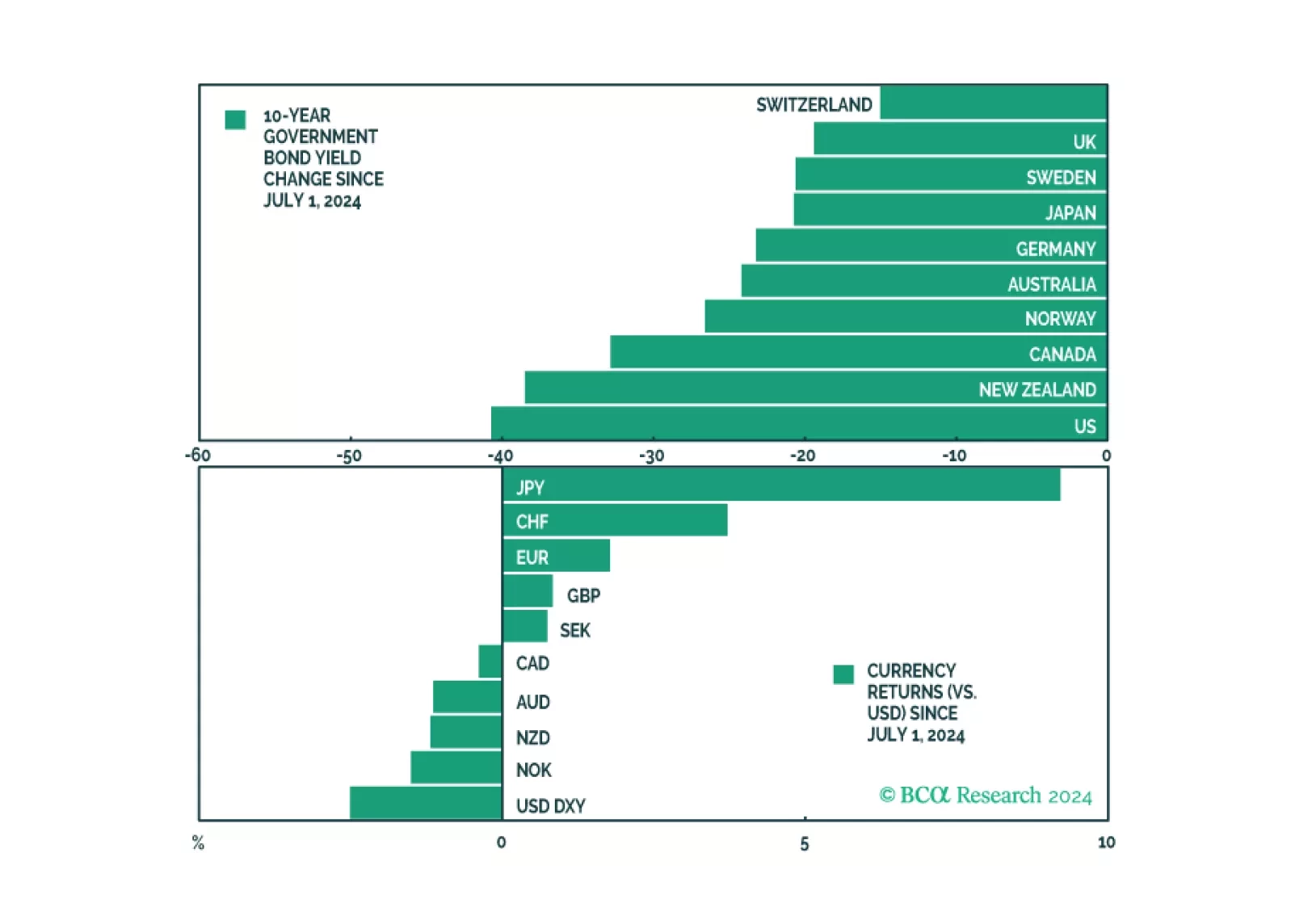

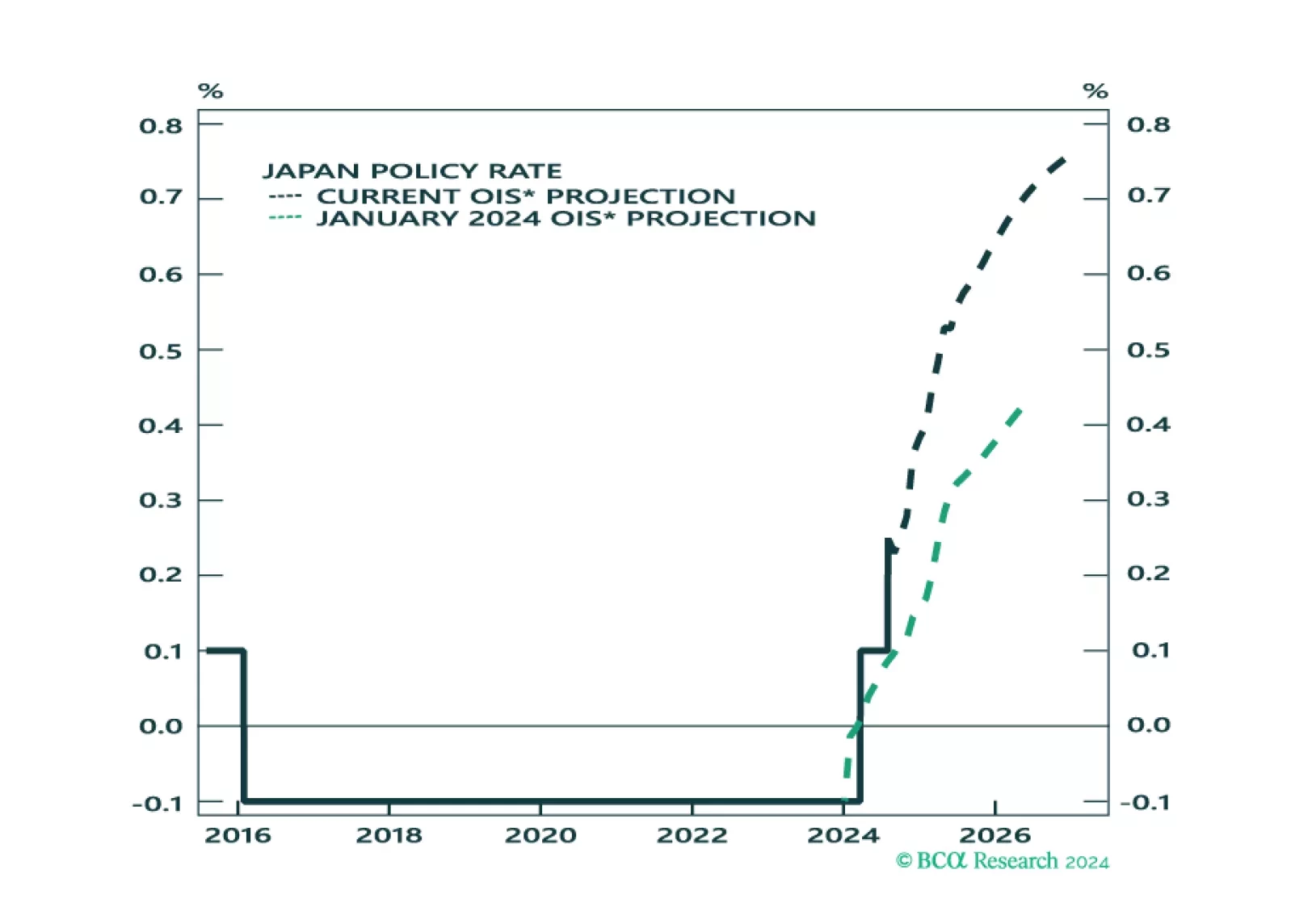

Japanese Yen

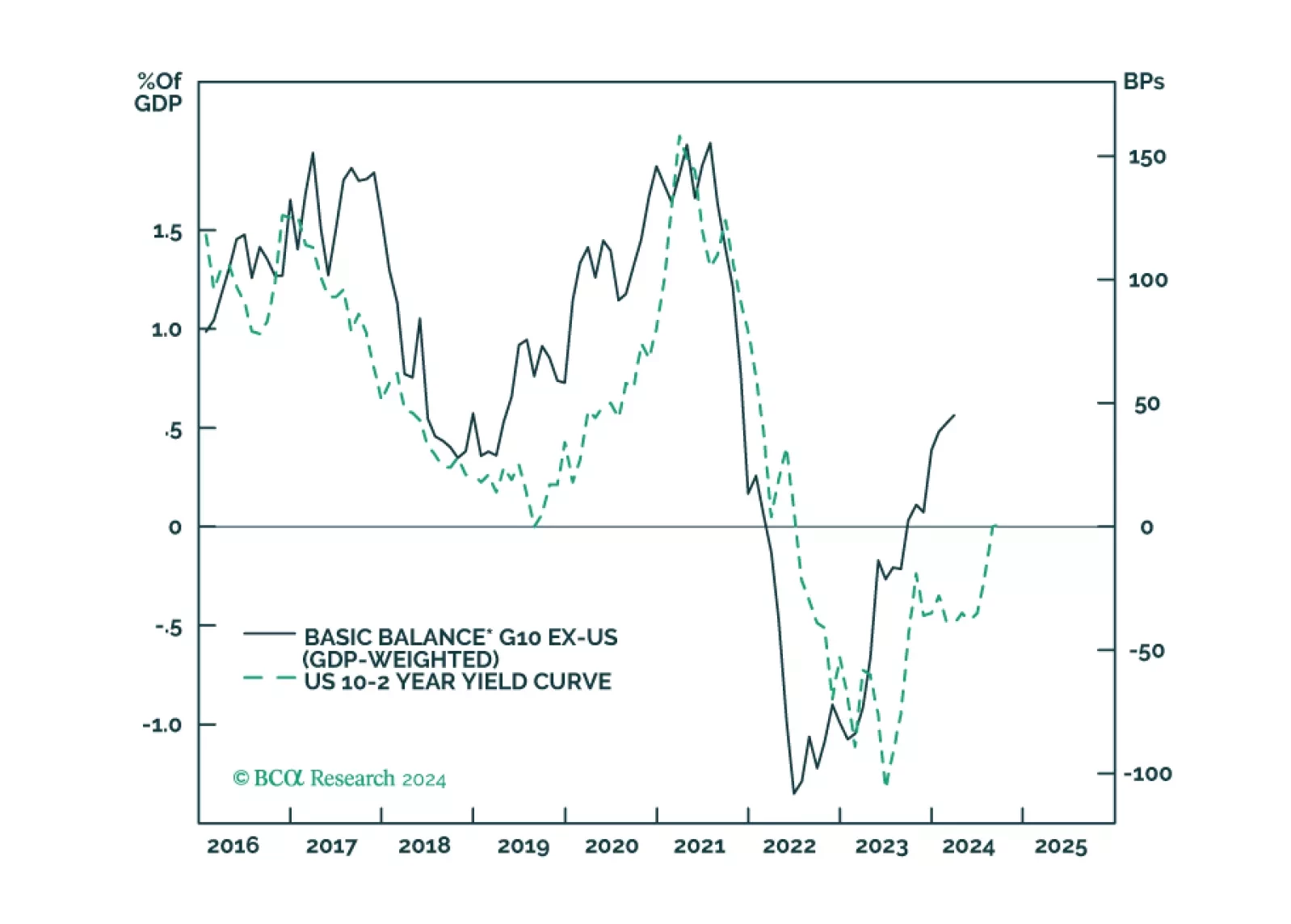

This report looks at the latest developments in G10 economies and implications for bond and FX market strategy.

Even after the Fed cuts rates, policy will remain restrictive for some time. Moreover, in history, stocks have tended to fall around the first rate cut. We remain cautious on the outlook for the economy and risk assets.

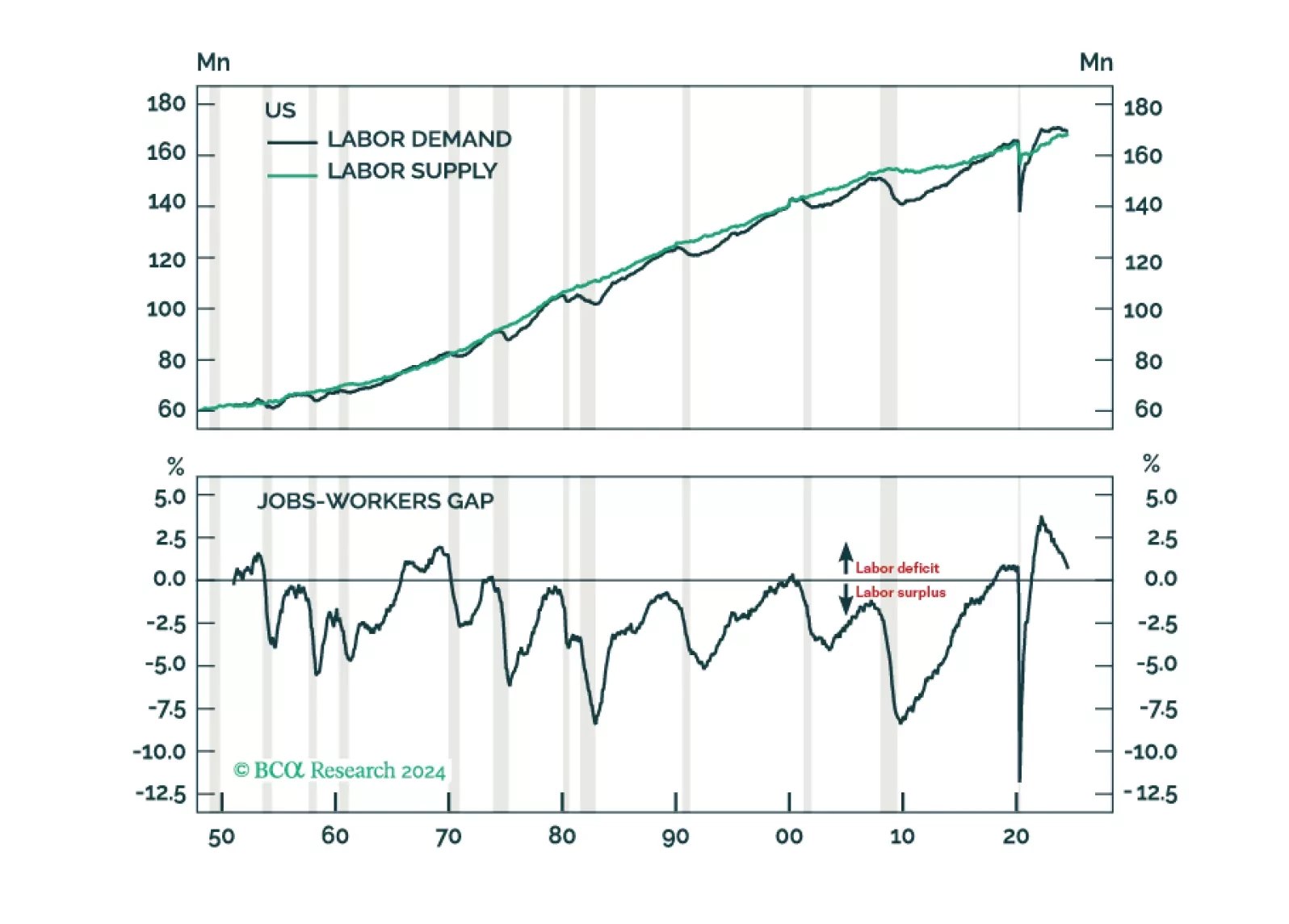

The great US labor market shortage is over. Labor demand will likely fall short of supply by the end of this year, causing unemployment to soar. Neither fiscal nor monetary policy will be able to prevent the coming recession. Investors should underweight stocks and overweight Treasuries.

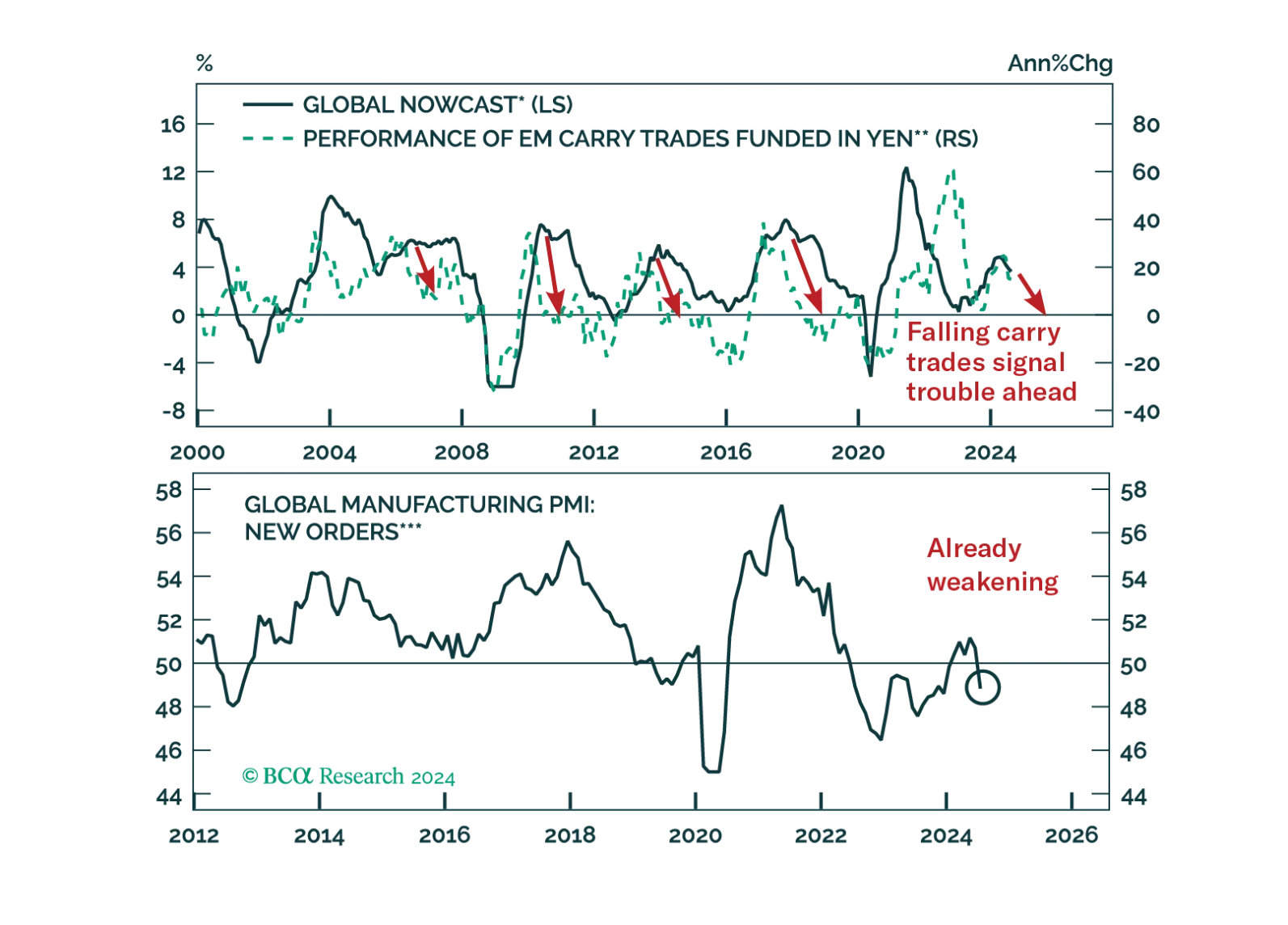

The unwind of yen carry trades caused violent tremors across the globe. Was this shock a one-off event or the prelude to more troubles?

In this monthly review, we give our take on where bond yields and the dollar are headed. This is within the lens of revisiting our fundamental indicators.

Over the past few weeks, global equities have been hit by rising scepticism over the bullish AI narrative and increasing concerns over global growth. Stocks should stabilize in the near term, but the medium-term direction is to the downside. We expect the S&P 500 to drop to 3750 in 2025 and the 10-year Treasury yield to fall to 3%.

The market is pricing in a soft landing, but we see growing signs that the global economy is faltering. Investors should be defensively positioned.

We assess the investment implications of the BoJ and Fed meetings, and give our take on the next policy moves. We also assess the impact on asset markets.