Iran

In the short term, there is plenty to be worried about in macro beyond the Middle East. The market was on thin ice before the Iran conflict. In the long term, the base case scenario remains bullish, but the war in the Middle East needs to be brief.

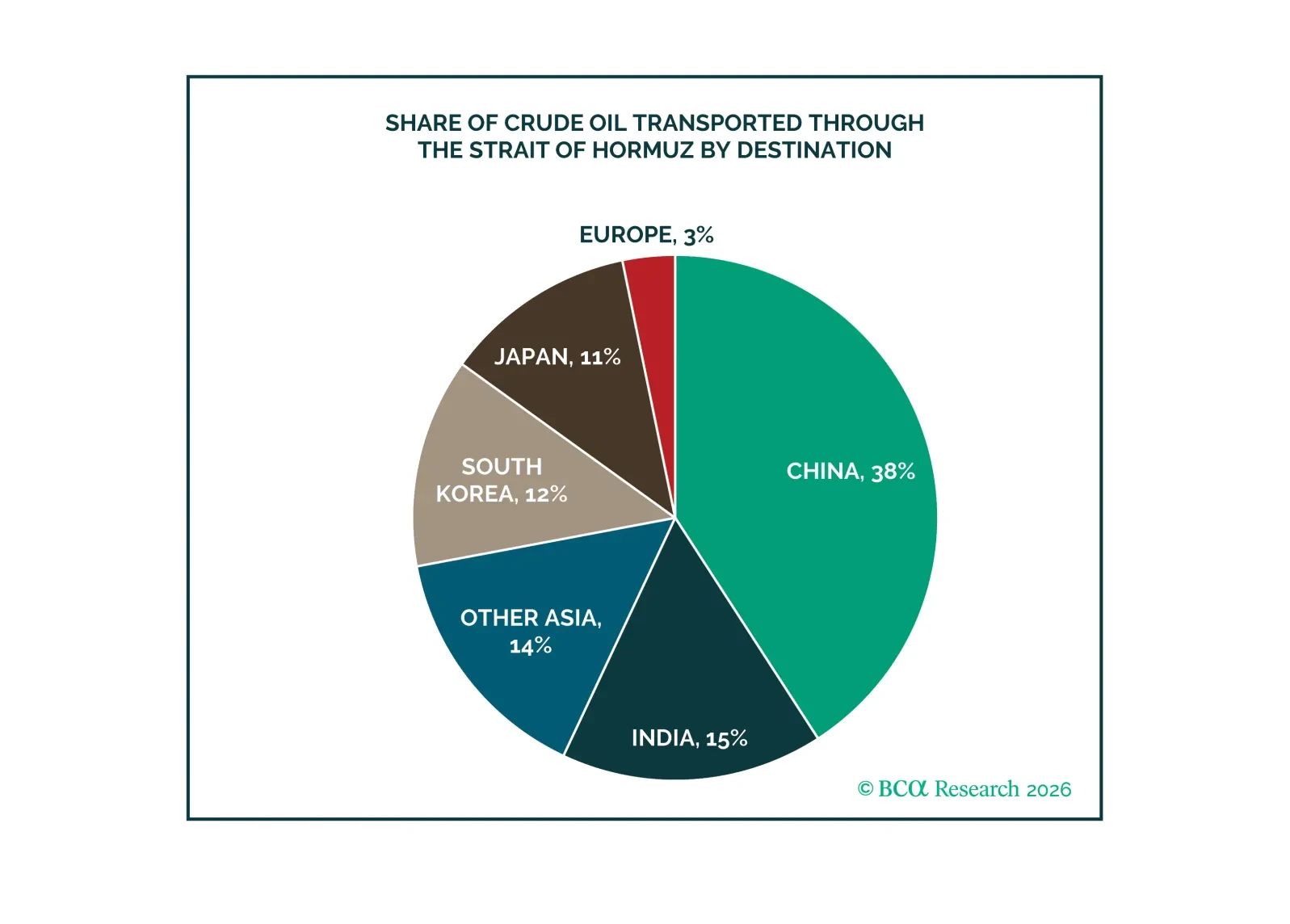

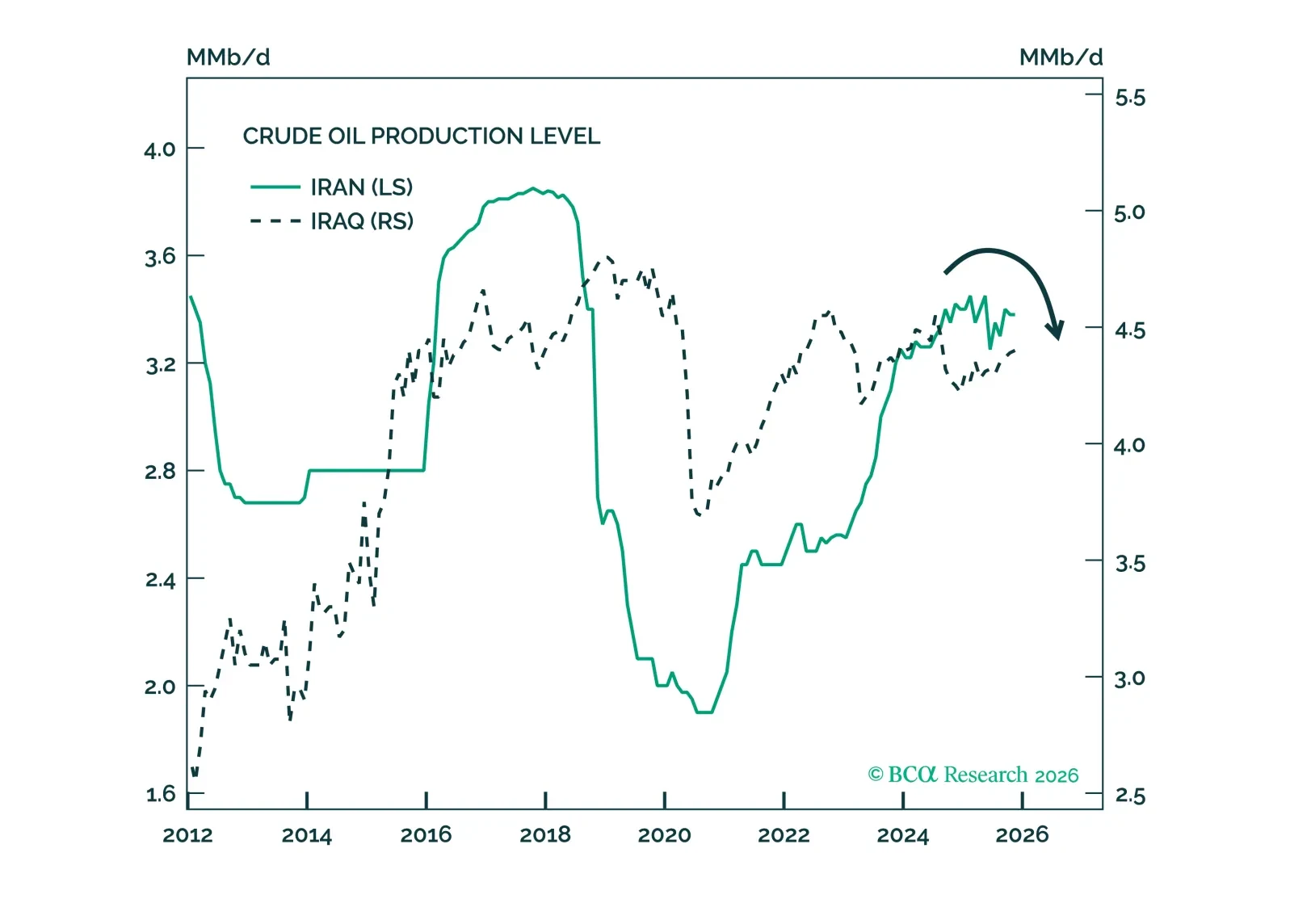

The war in Iran is disrupting global oil and LNG flows and remains a threat to regional energy infrastructure.

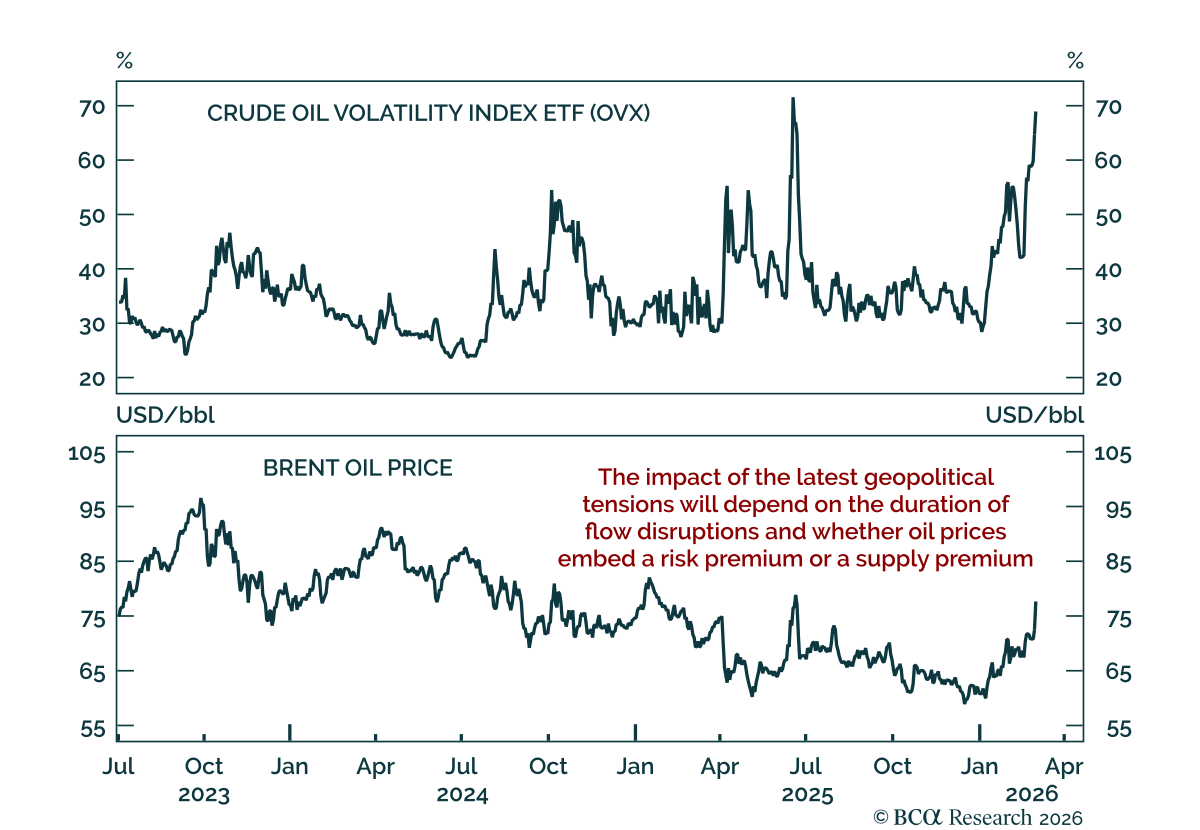

Energy price risks remain skewed to the upside over the near term.

It is too soon to sell the rip in oil or buy the dip in stocks. Stick with risk-off trades for now.

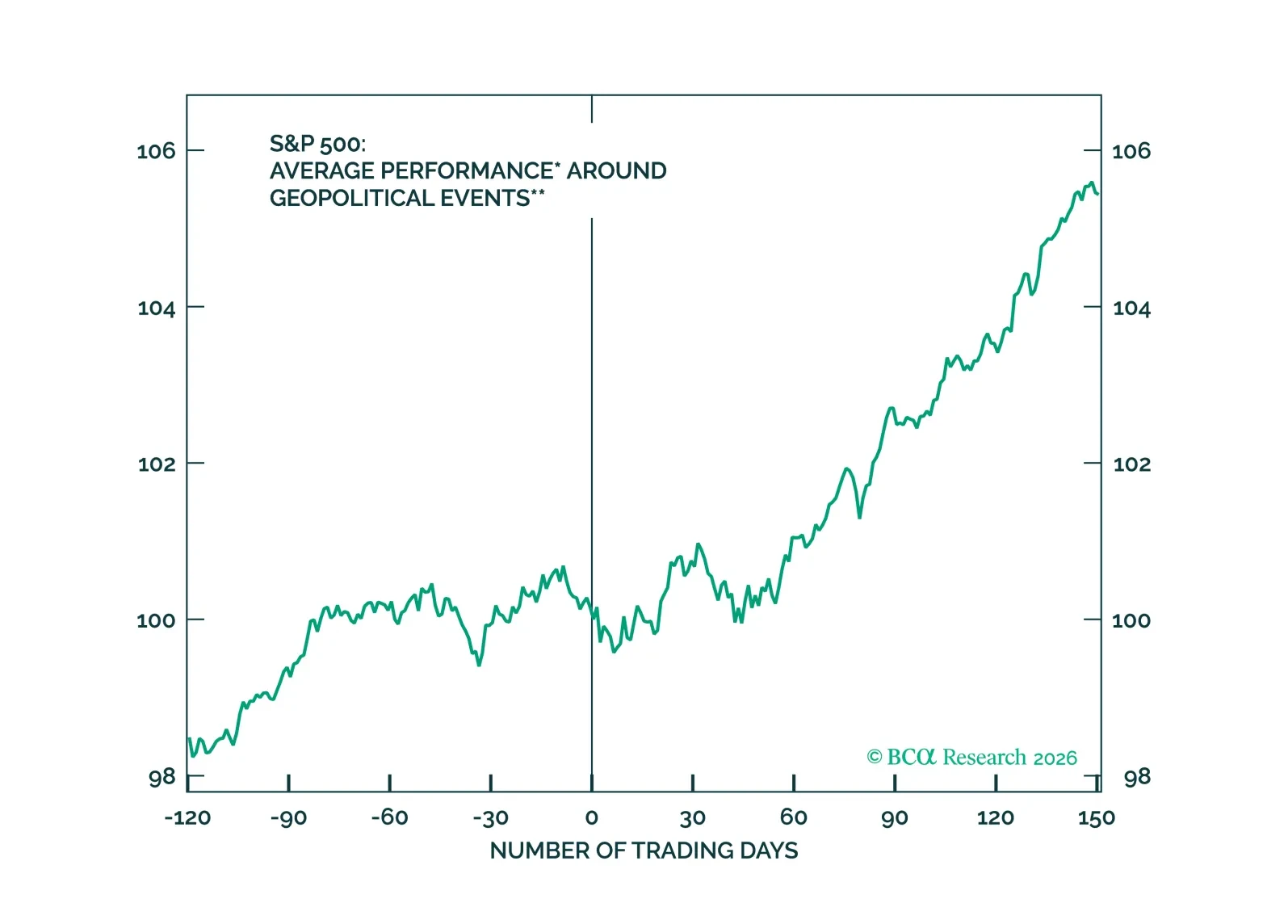

Middle East hostilities have triggered risk-off moves and pushed oil prices higher. Previous geopolitically driven oil price disruptions suggest that speed, persistence and equity market vulnerability relate to the degree of the market sell off. At the other end of the spectrum, energy stocks should benefit, but have already rallied significantly.

Since our Saturday missive, there have been several developments in the ongoing conflict between Iran and the US-Israel coalition.

The fog of war is the thickest at the dawn of kinetic action. However, BCA’s GeoMacro Strategy has trade recommendations to manage and thus we send this missive despite the significant uncertainty.

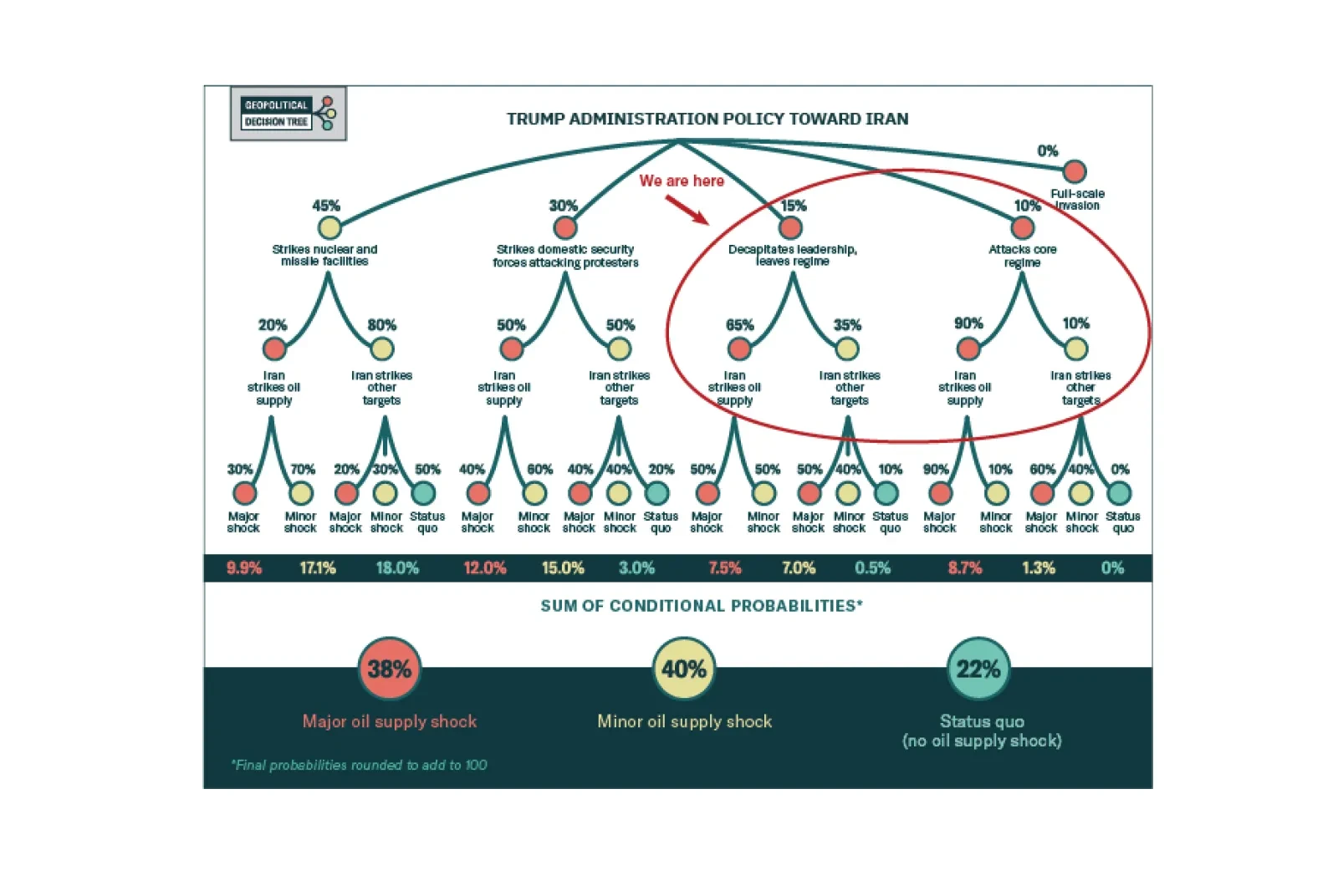

The “Chuck Norris Premium” is now fully in the market. Since the miraculously successful nabbing of President Nicolas Maduro on January 3, the odds of subsequent use of military against Iran increased.

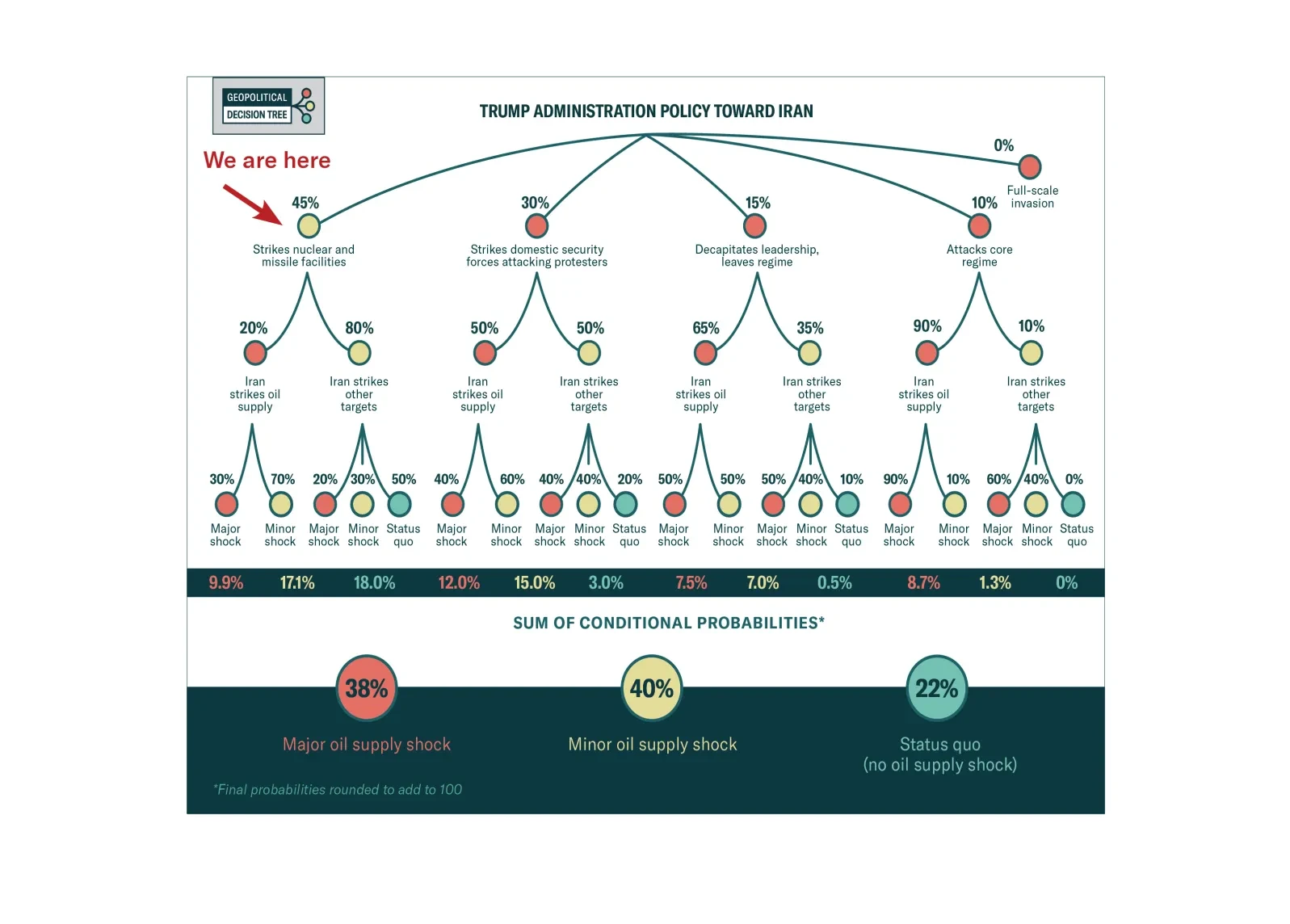

The US is likely to take significant military action in Iran, justifying our 40% risk of a major oil shock. Tactically go long Brent crude.

The risk to Iran's regime survival raises the probability of a massive global oil supply shock back to around 40%, where we put it last year.