Equities

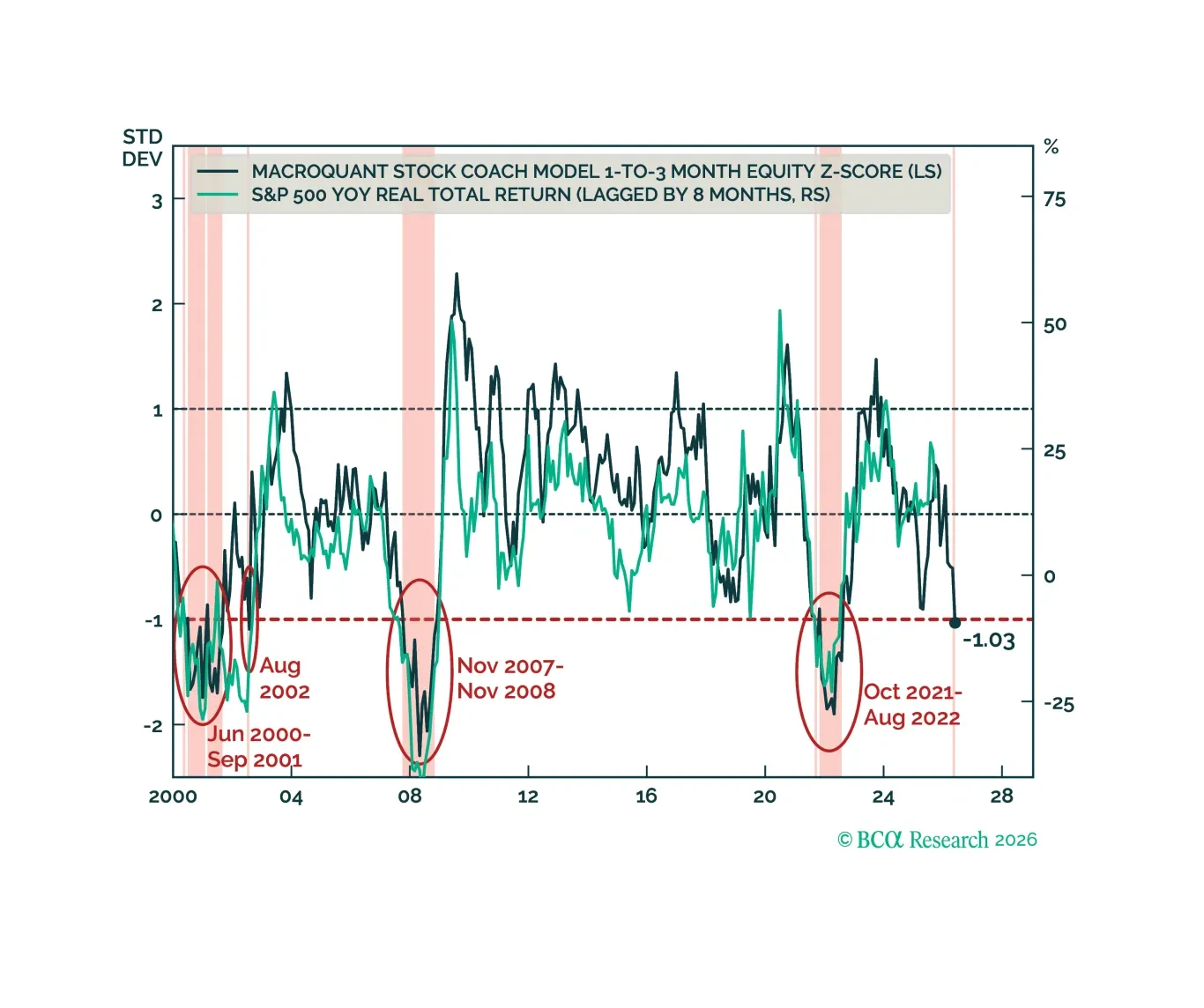

MacroQuant recommends underweighting equities and adopting a benchmark duration stance in fixed-income portfolios. The model is very positive on the US dollar, bearish on gold, neutral on copper, and bullish on oil.

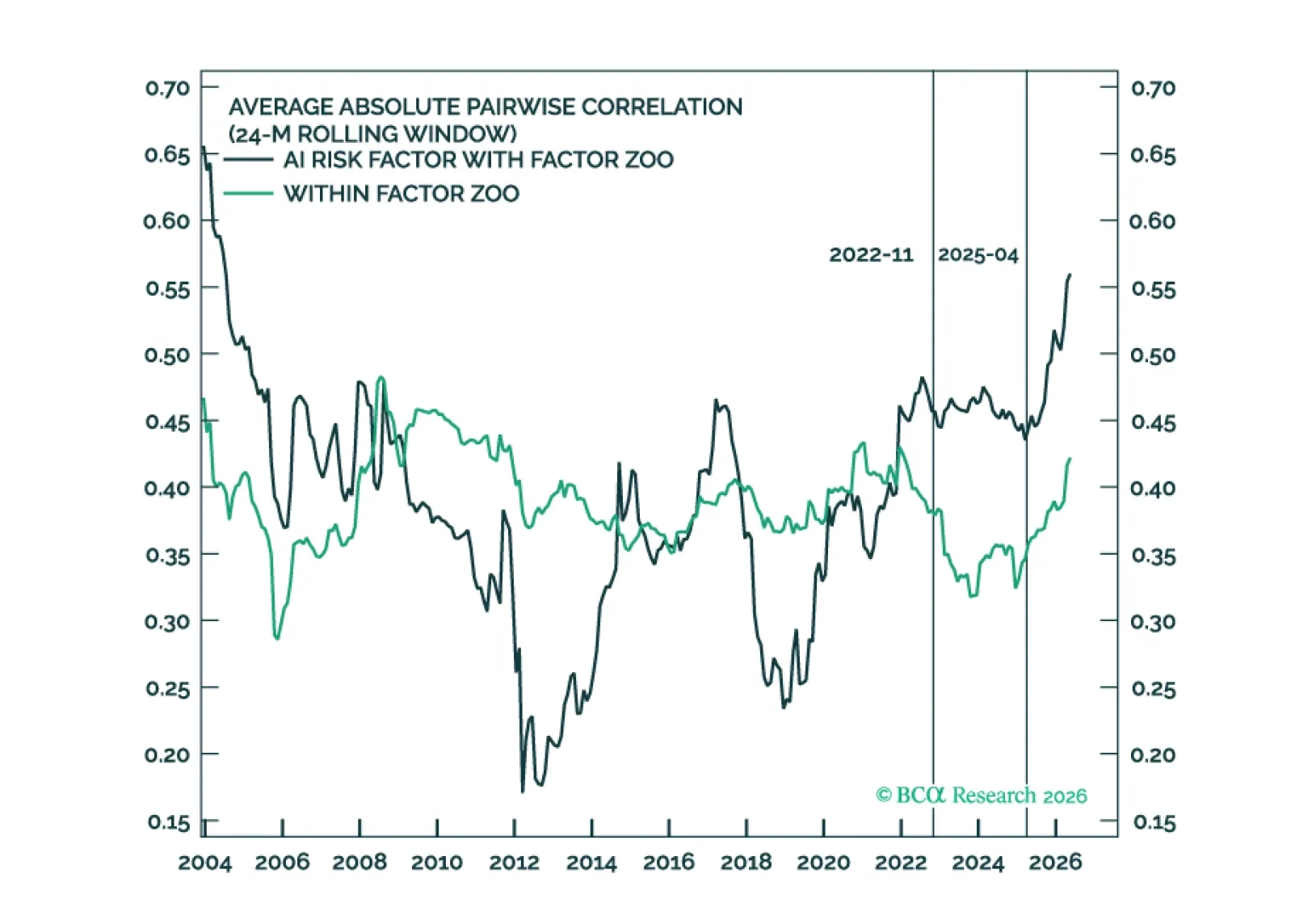

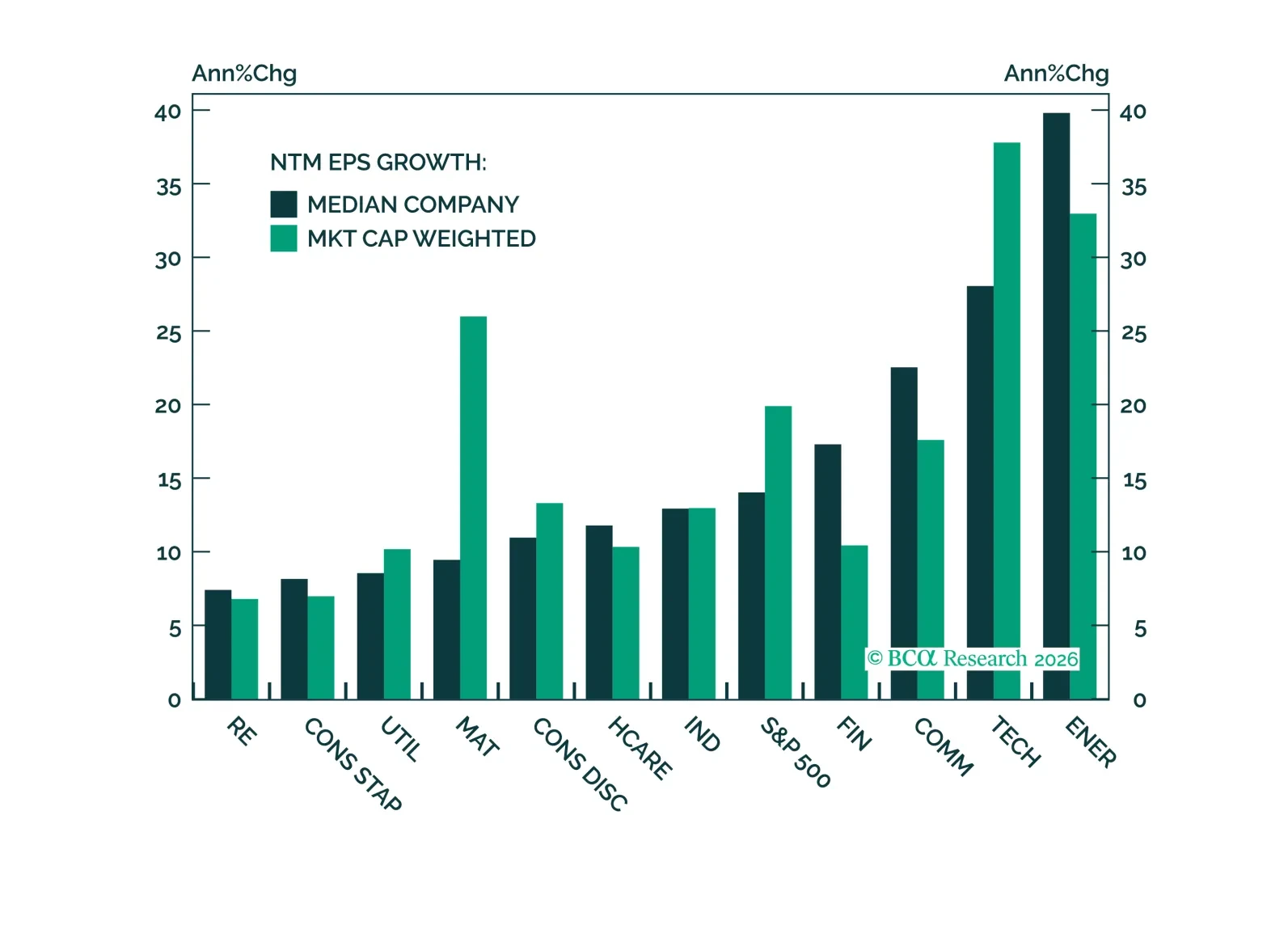

The S&P 500 has become increasingly concentrated. We know that. But the critical question is not how many stocks are driving the market; it is how many factors are driving stocks. We define an AI risk factor to test whether AI has become the dominant common exposure throughout much of the factor zoo.

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

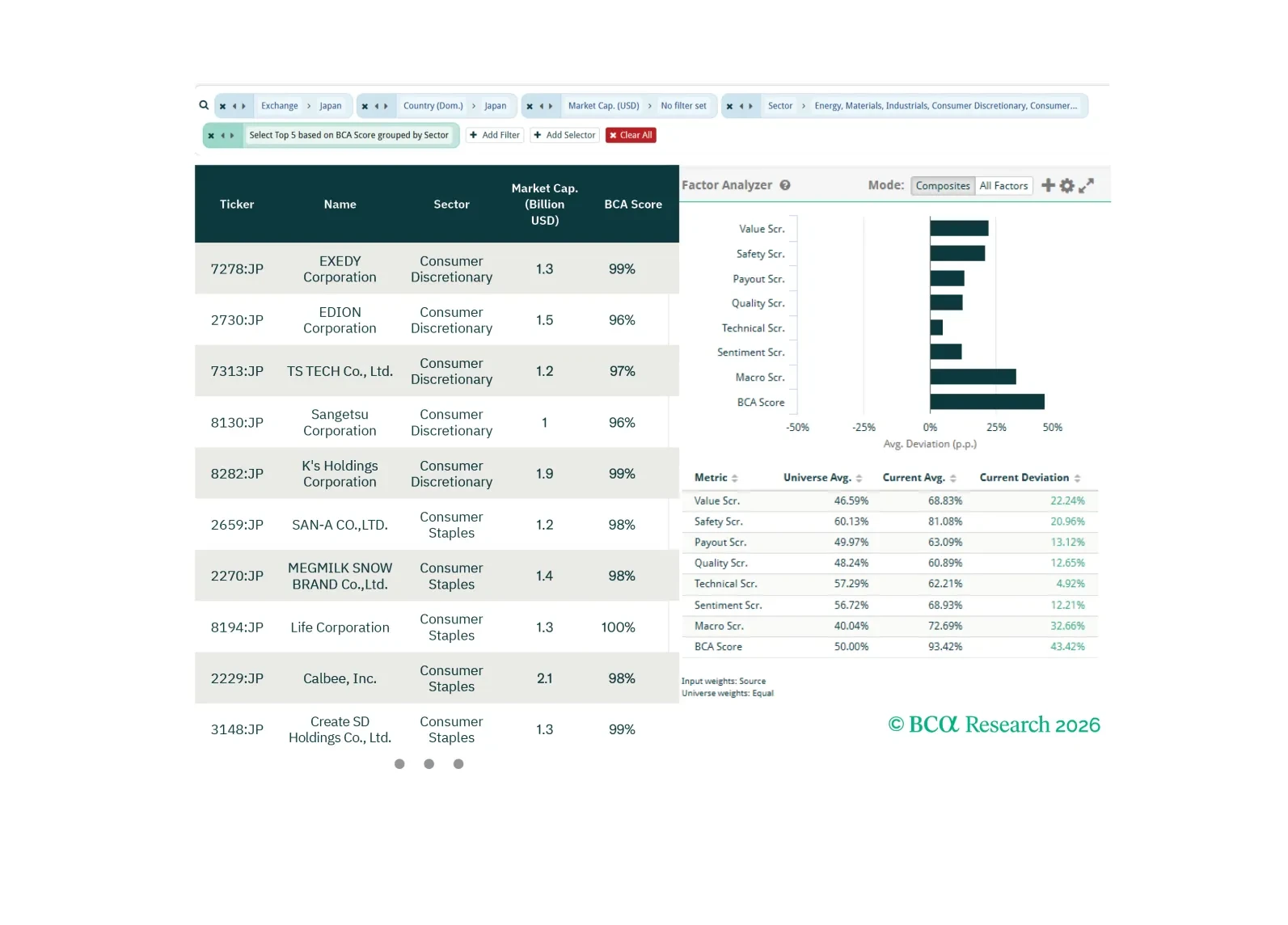

In this screener report, we explore opportunities in Japanese Non-TMT equities, El Niño hedges, and US consumer-facing equities.

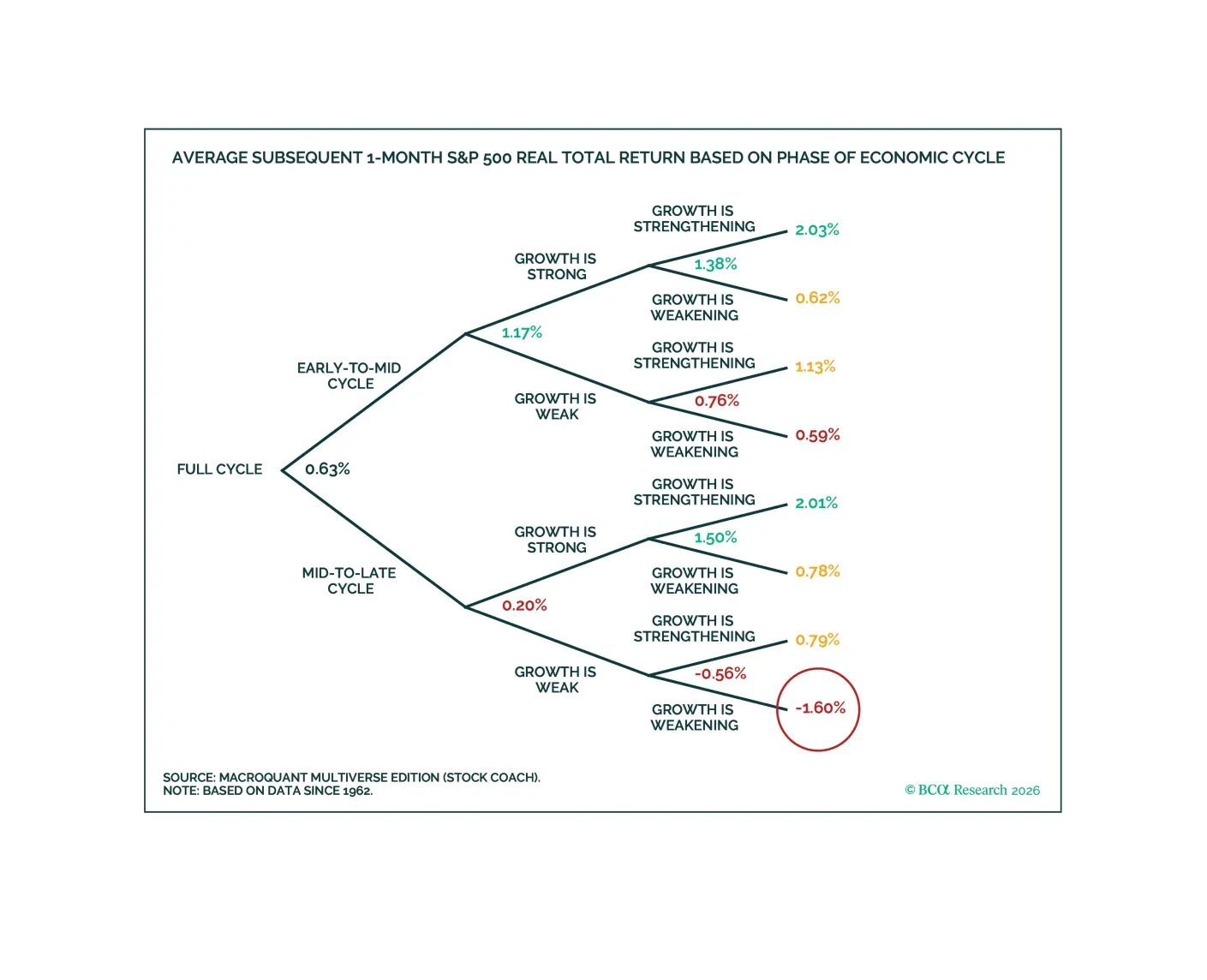

The economy has shifted into Expansion, earnings growth is broader and stronger than we expected, and we are raising our 2026 S&P 500 target to 8100 on $330 of EPS. However, we are also cutting our year-end multiple to 24.5. From here, returns will need to come from earnings growth, not multiple expansion.

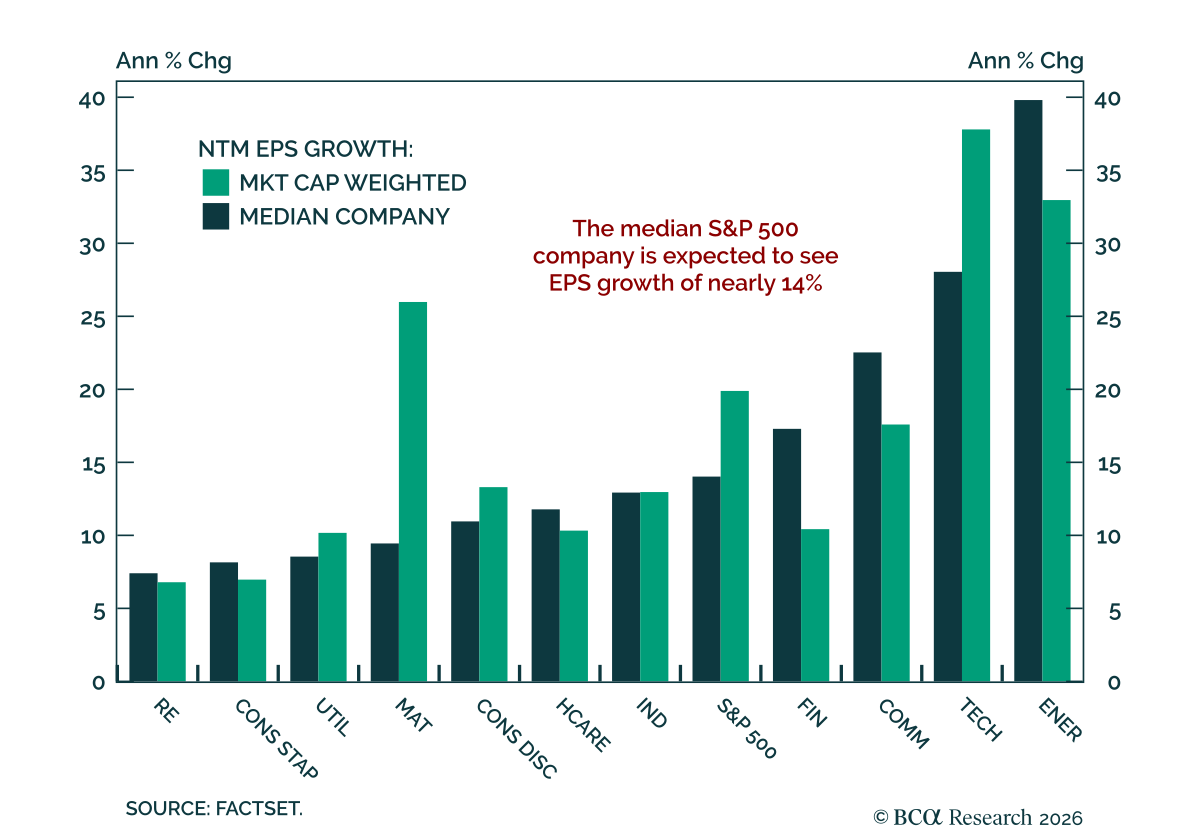

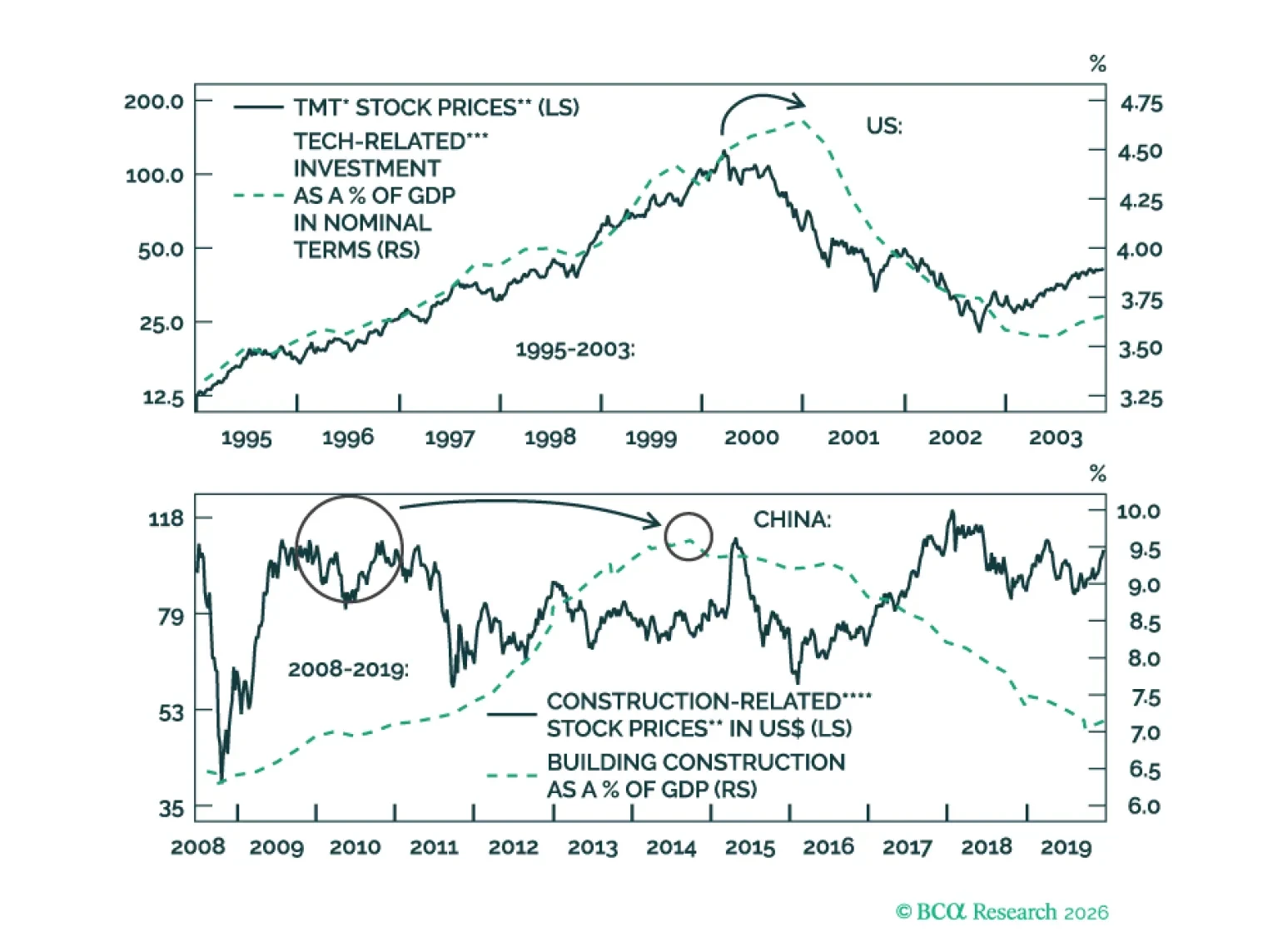

AI is transformative, yet tech stocks may not produce positive returns. Market cycles have not disappeared. Greed and fear will still produce large share price fluctuations. Meanwhile, US inflation is the key near-term risk. Global non-tech capex aspirations also look overstated.

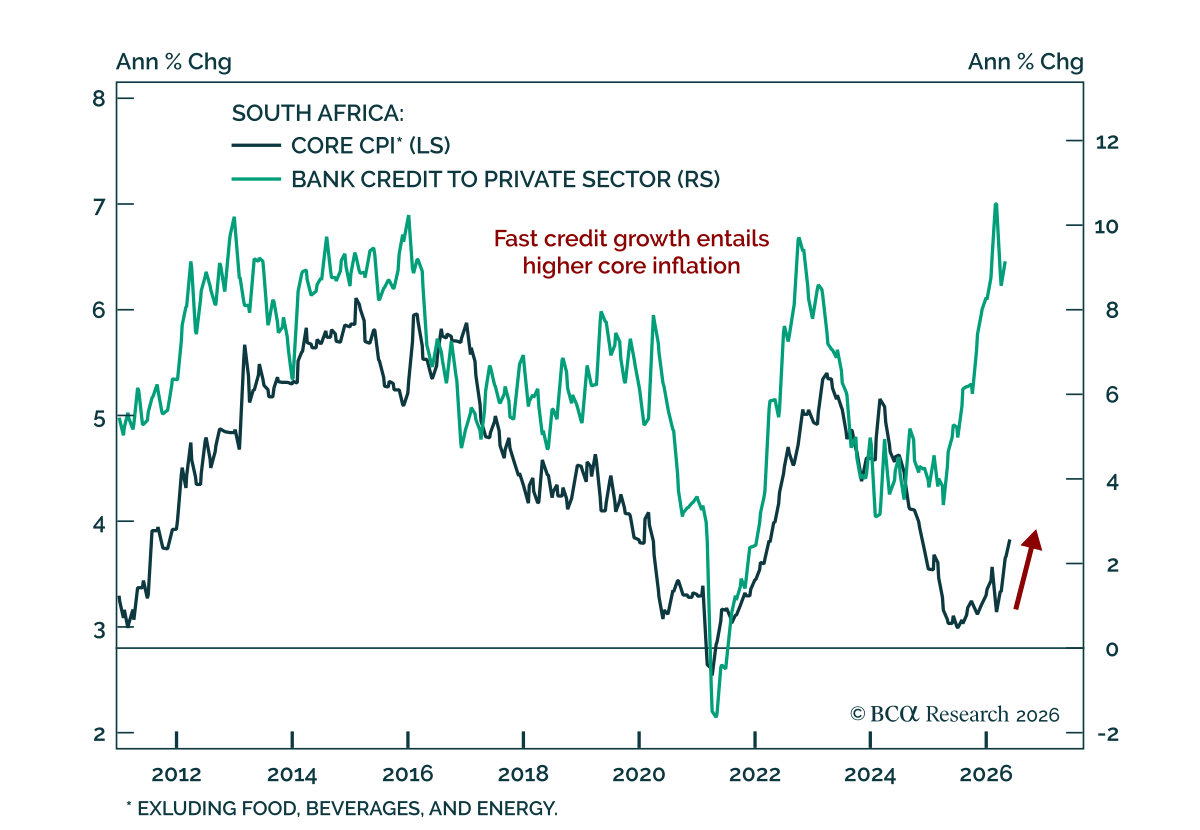

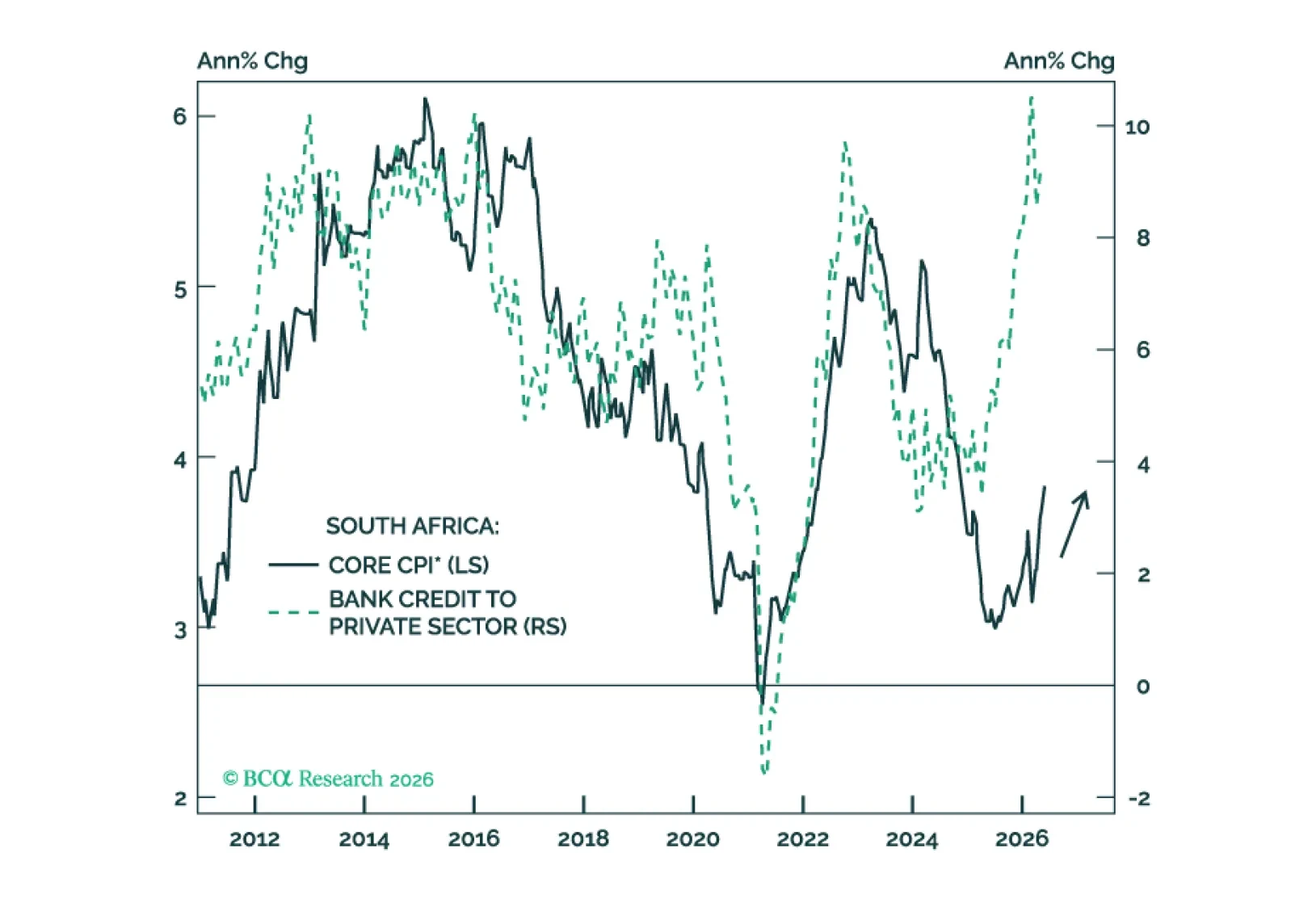

South Africa’s ambitious reform agenda will take time to bear fruit. Meanwhile, the country faces a stagflationary squeeze as inflation rises while growth slows. South African stocks, bonds, and currency are all vulnerable.