Currencies

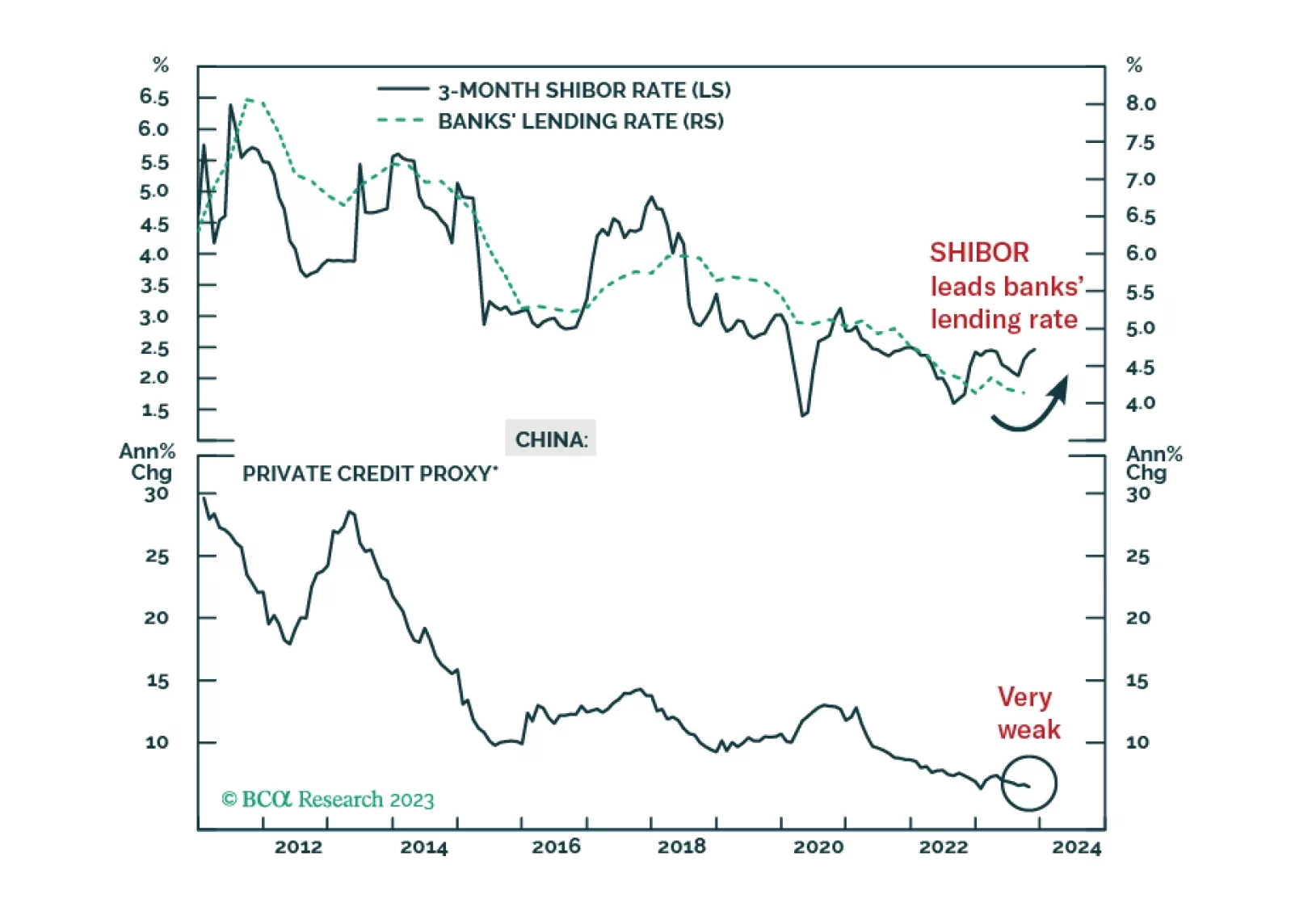

A cyclical recovery in China’s economy is still not imminent. The PBoC has tightened interbank liquidity to stabilize the exchange rate since late August. This does not bode well for the real economy. The uptick in onshore bond yields and the RMB’s appreciation will be transient. Equity investors should stay cautious.

Today, we are sending you the BCA annual outlook for 2024. The report is an edited transcript of our recent conversation with Mr. X and his daughter, Ms. X, who are long-time BCA clients with whom we discuss the economic and financial market outlook for the next twelve months toward the end of each year.

This report looks at the prospects for the Swedish krona, following the pause by the Riksbank.

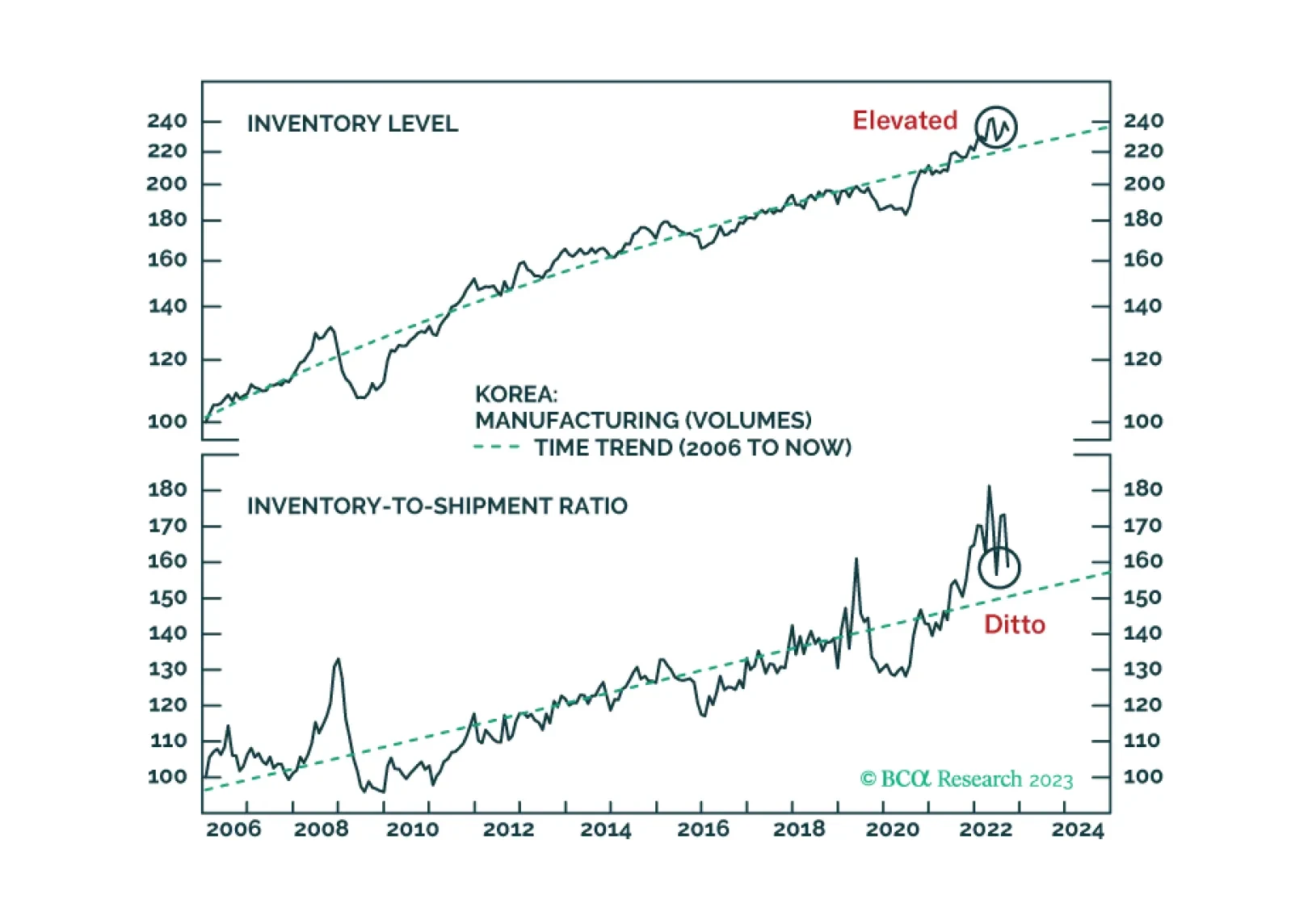

Contrary to the prevalent belief in the global investment community, goods/merchandise inventories in the US and East Asia are rather elevated. Financial markets respond to final demand fluctuations, not inventory restocking. Global manufacturing/trade will continue contracting, even though the pace of contraction might moderate in the near run. We recommend that investors fade the current rally.

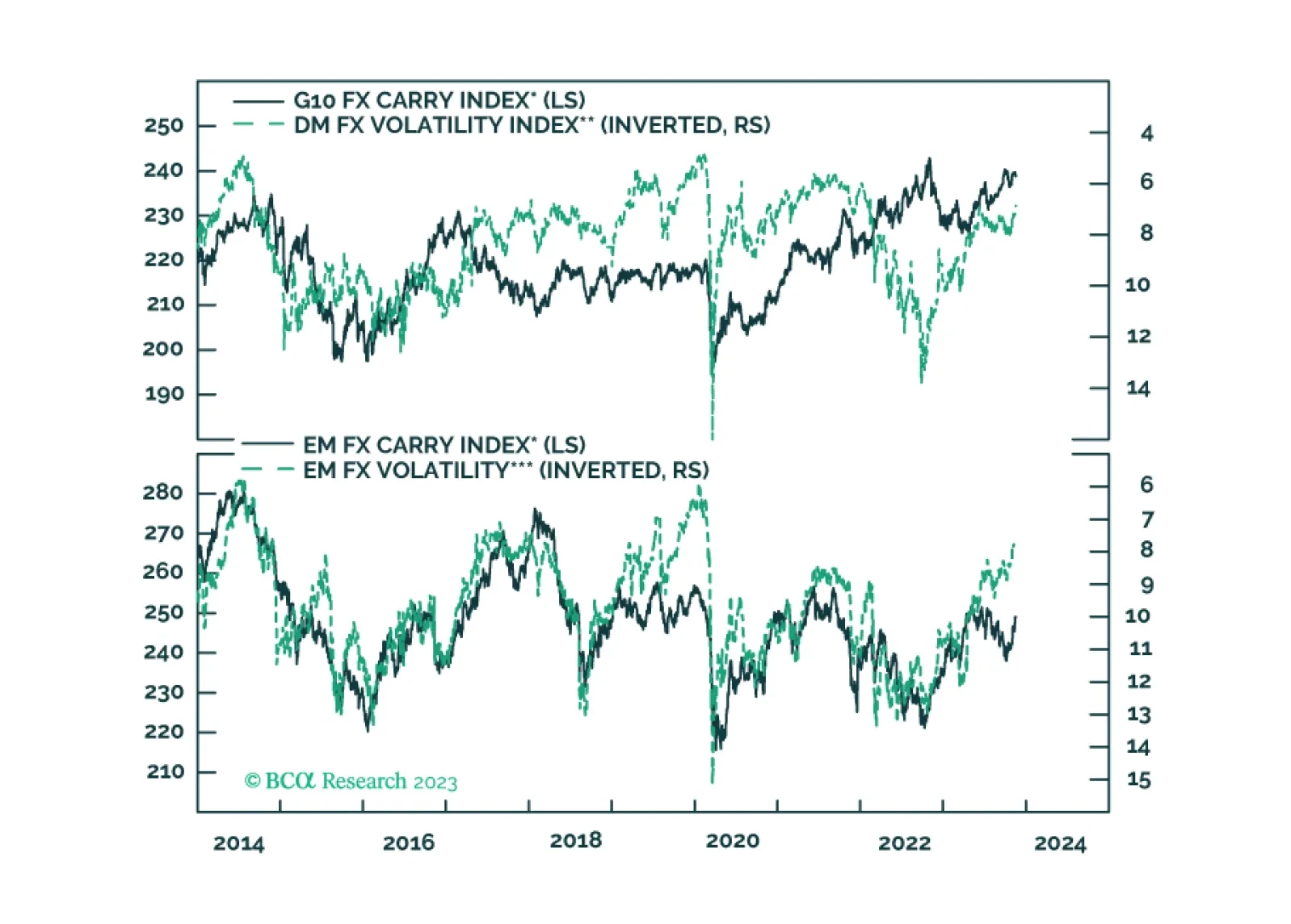

In this report, we evaluate the risk to carry trades in the coming months.

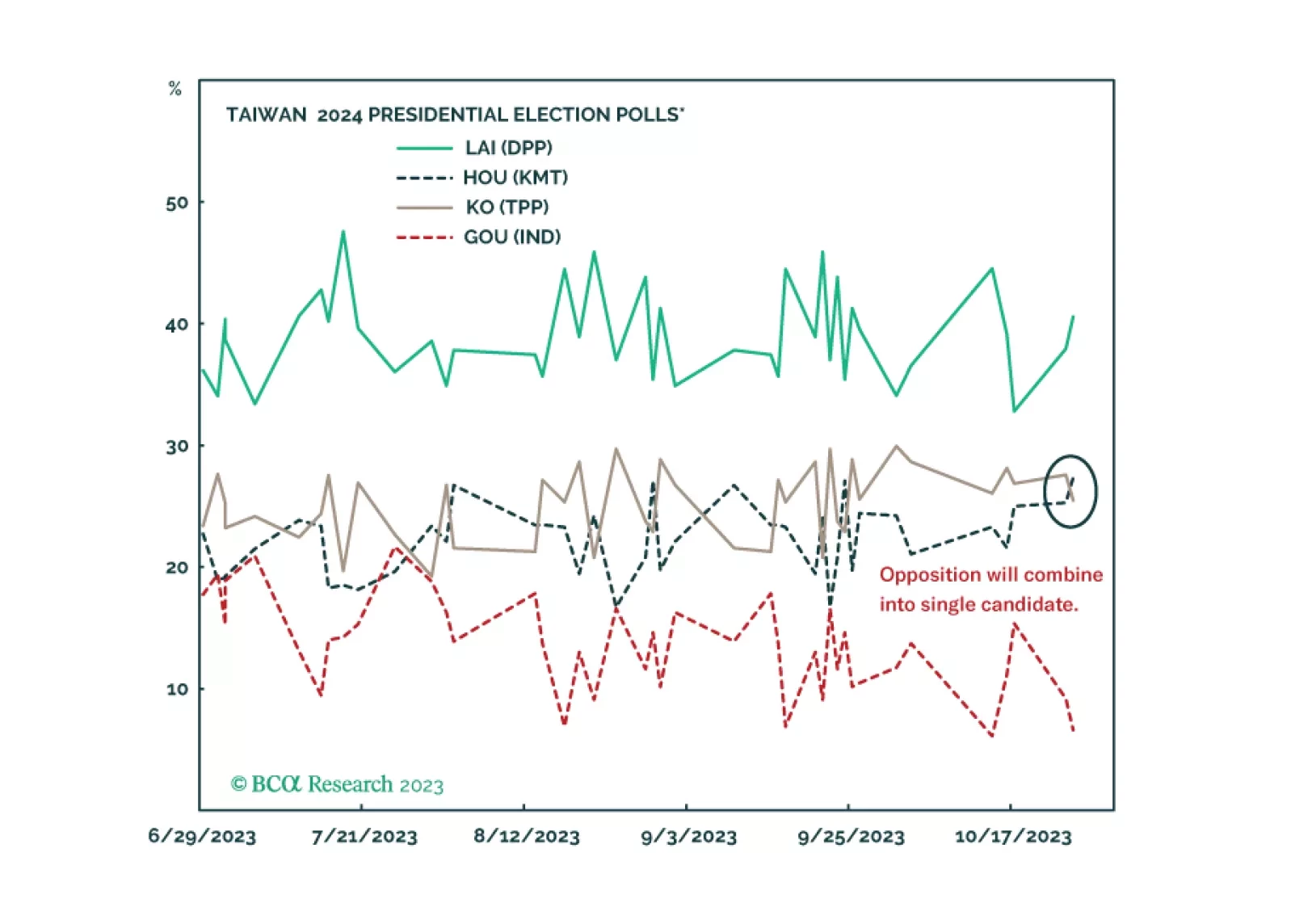

Investors should not get their hopes up about the Biden-Xi summit. Wait to see if a new ruling party is elected in Taiwan before downgrading geopolitical risk in the Taiwan Strait. US-China strategic détente is possible but neither the geopolitics nor the macro backdrop warrant a risk-on position next year.