Manufacturing

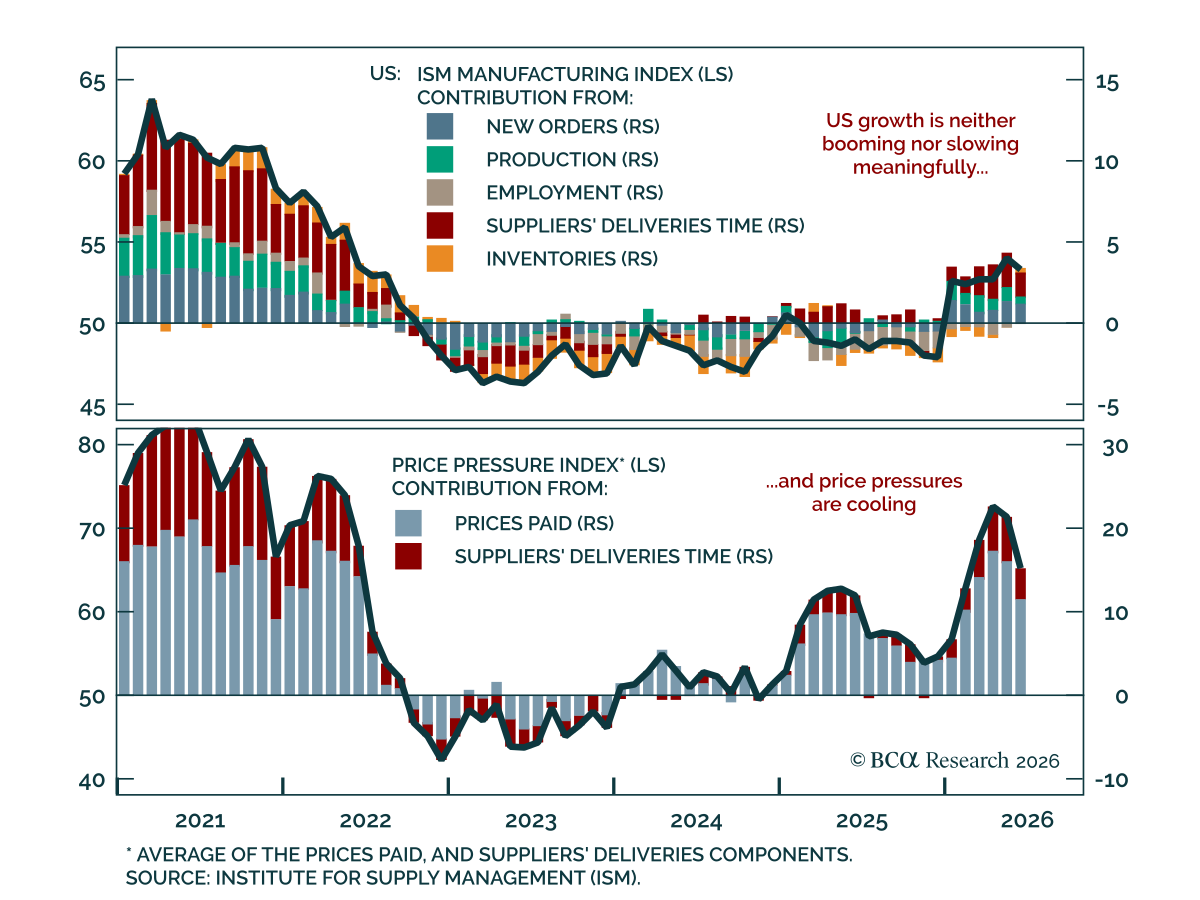

The June ISM Manufacturing index came in below estimates, but the broader US growth backdrop remains in a sweet spot. The headline index ticked down to 53.3 from 54.0. The slowdown was broad, with new orders easing to 56.0 from 56.8. Employment, however,…

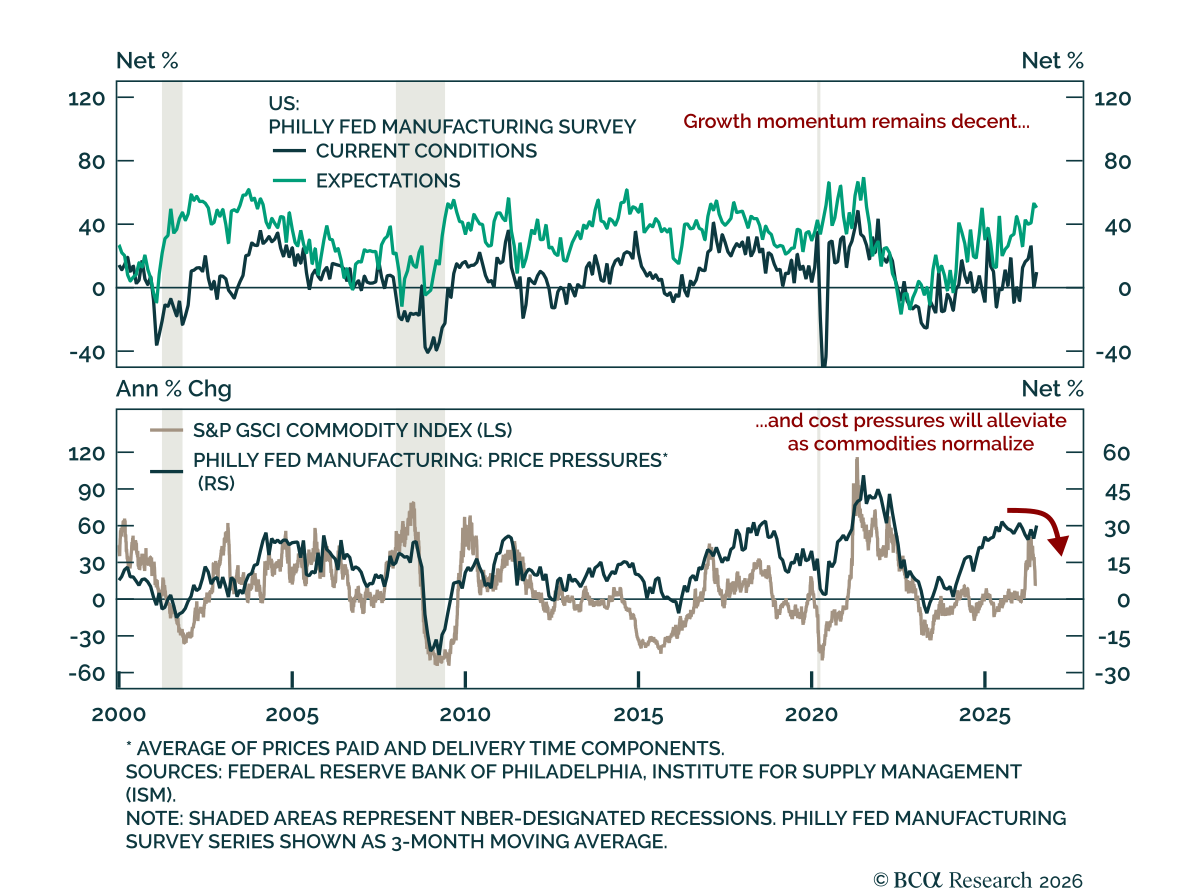

The June Philadelphia Fed survey improved, pointing to still-decent US growth. The headline index rose to 10.3 from -0.4, in line with estimates. New orders and employment also moved back into expansionary territory, while shipments increased. Despite its…

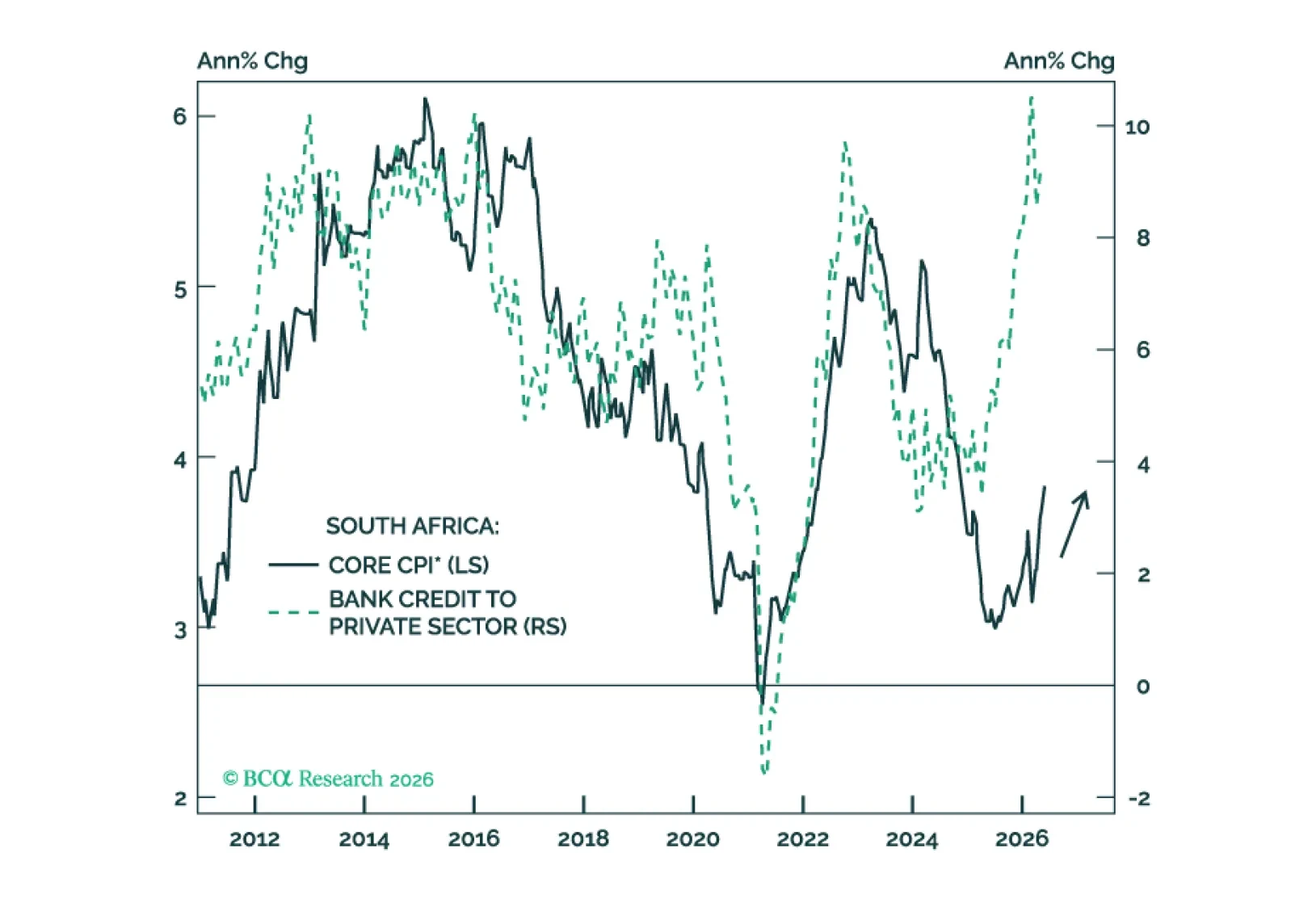

South Africa’s ambitious reform agenda will take time to bear fruit. Meanwhile, the country faces a stagflationary squeeze as inflation rises while growth slows. South African stocks, bonds, and currency are all vulnerable.

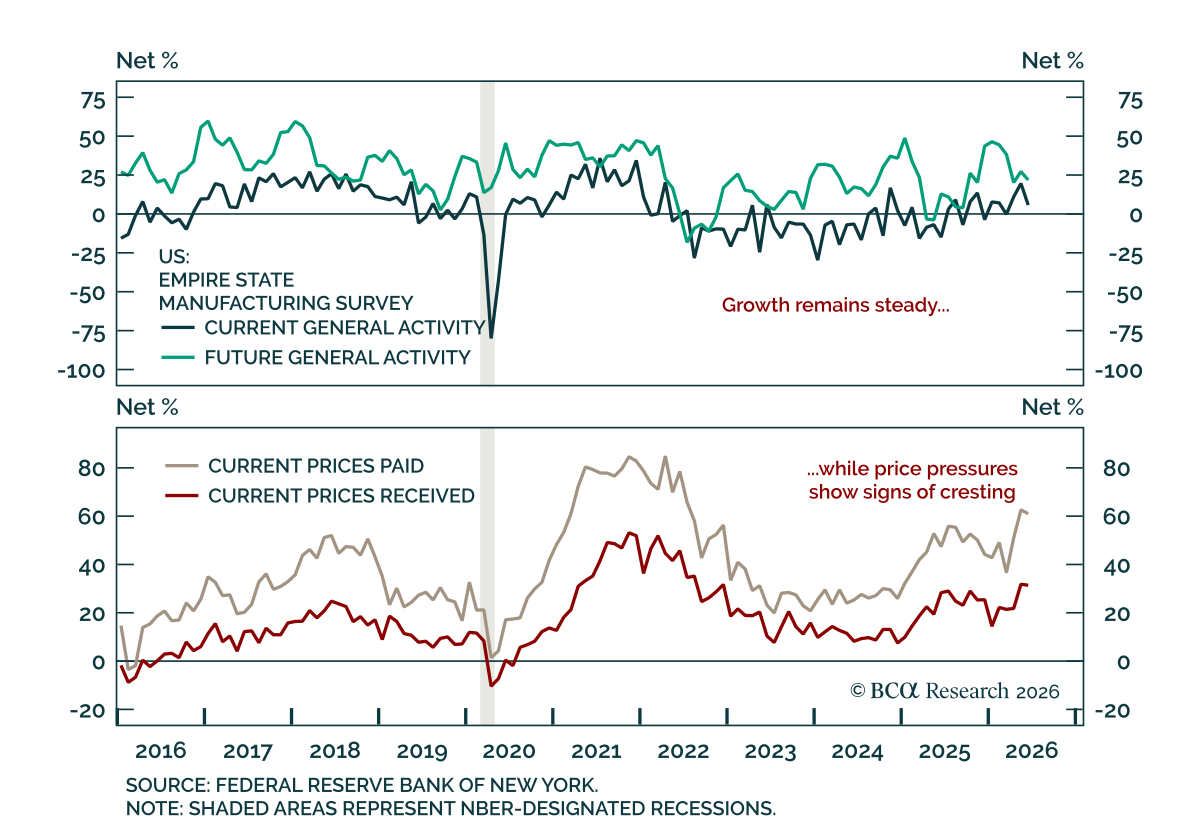

The June Empire survey cooled from May’s pace, but still pointed to continued US manufacturing growth. The headline fell to 5.7 from 19.6, missing estimates. The headline fell sharply from May, but still pointed to slower growth rather than contraction. The…

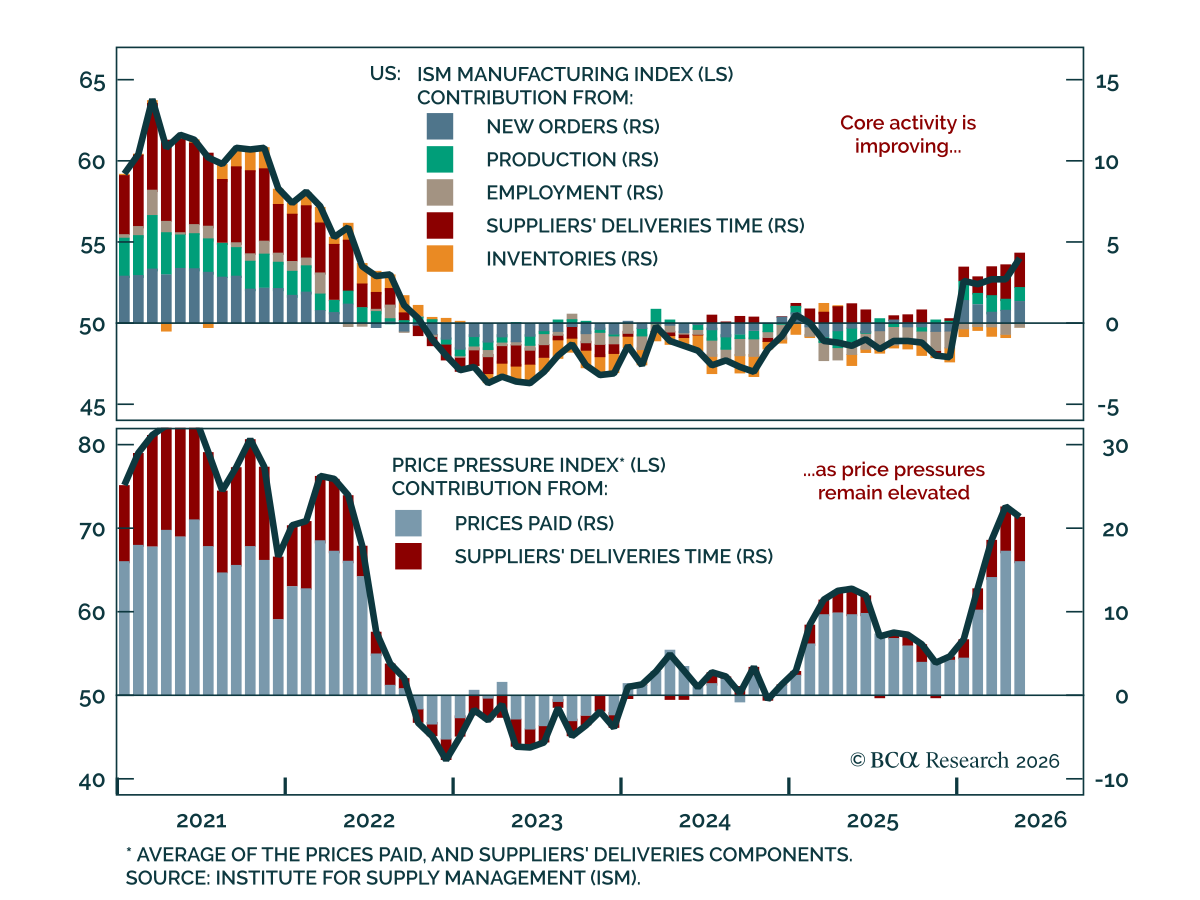

May’s US ISM Manufacturing report reinforces improving activity alongside persistent price pressure, highlighting continued inflationary impulse and hawkish risks to US monetary policy. The headline index came in at 54, above the market expectation of 53,…

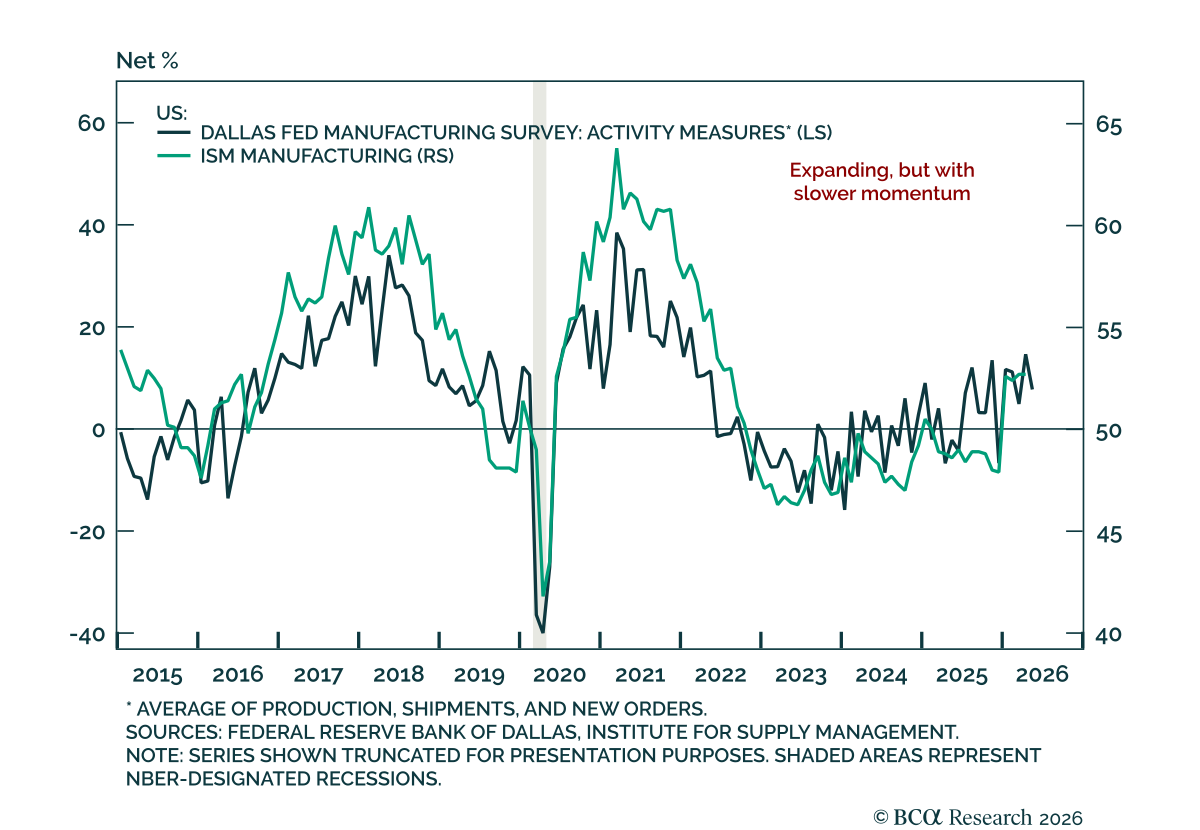

The Dallas Fed survey points to Texas manufacturing continuing to expand in May, but with slowing momentum. The production index fell 10 points to 9.4, signaling an average pace of output growth rather than a broad acceleration. The softer tone showed up…

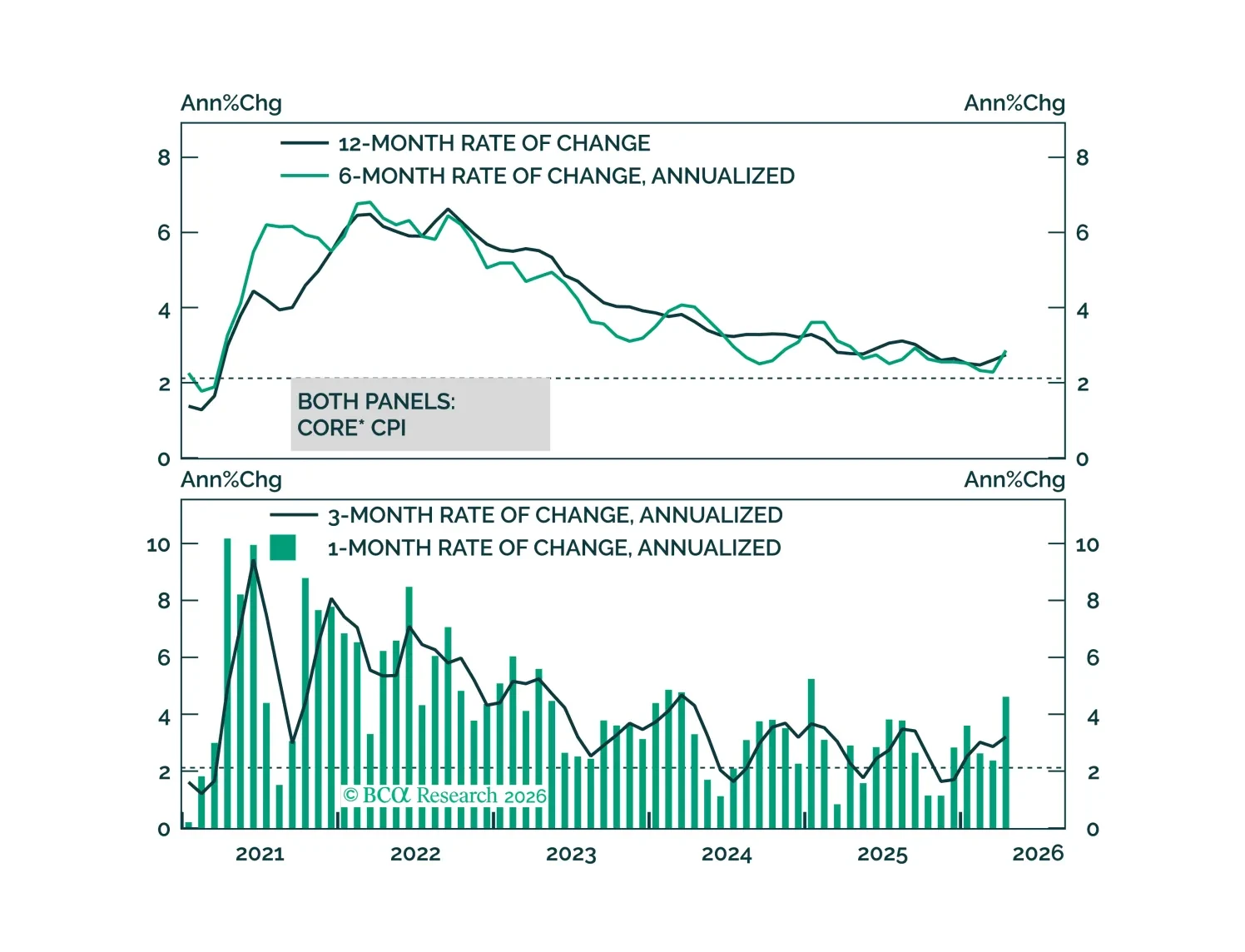

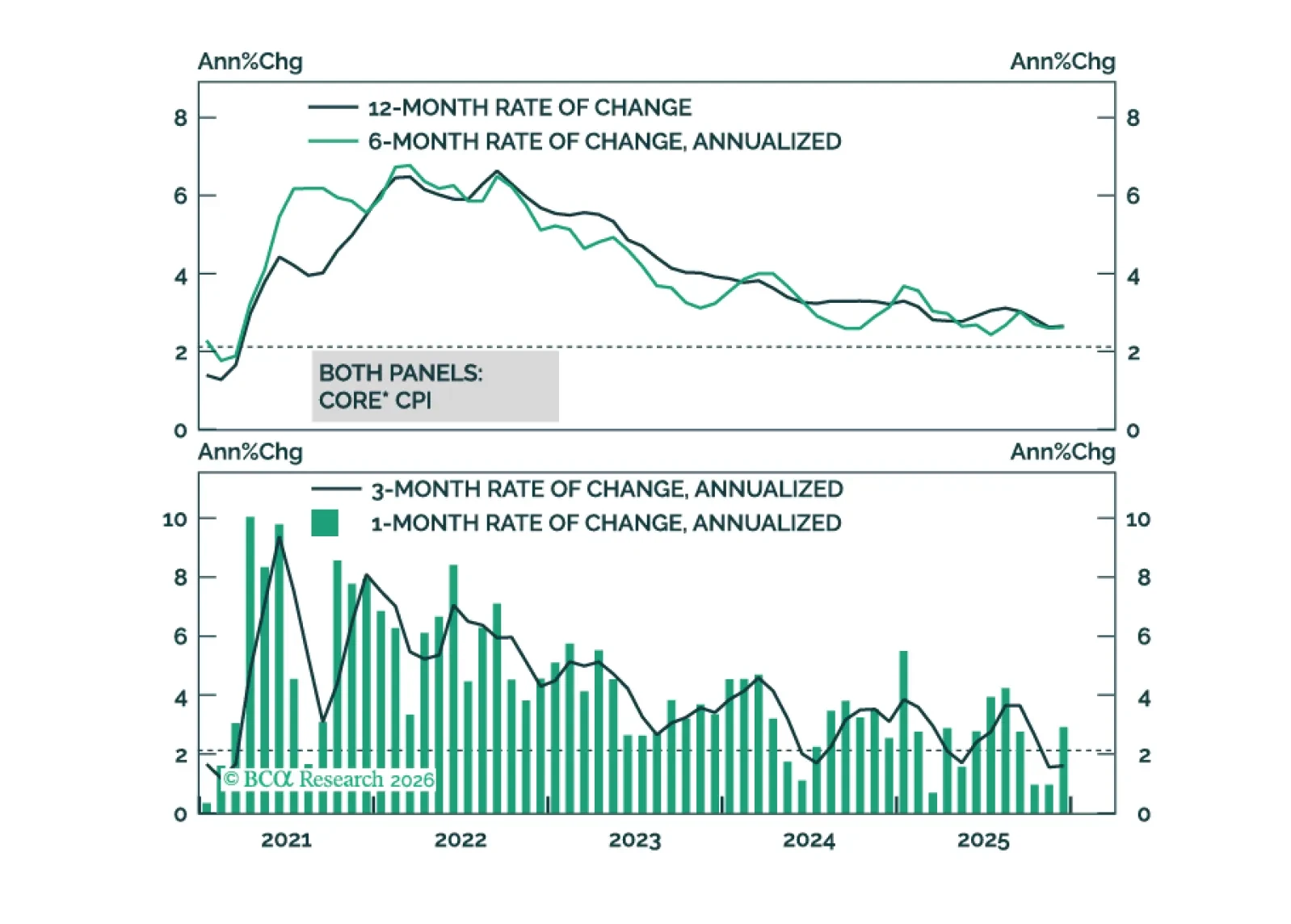

The April CPI report showed clear evidence of the direct effect of higher oil prices on inflation but, so far, limited evidence of passthrough to core.

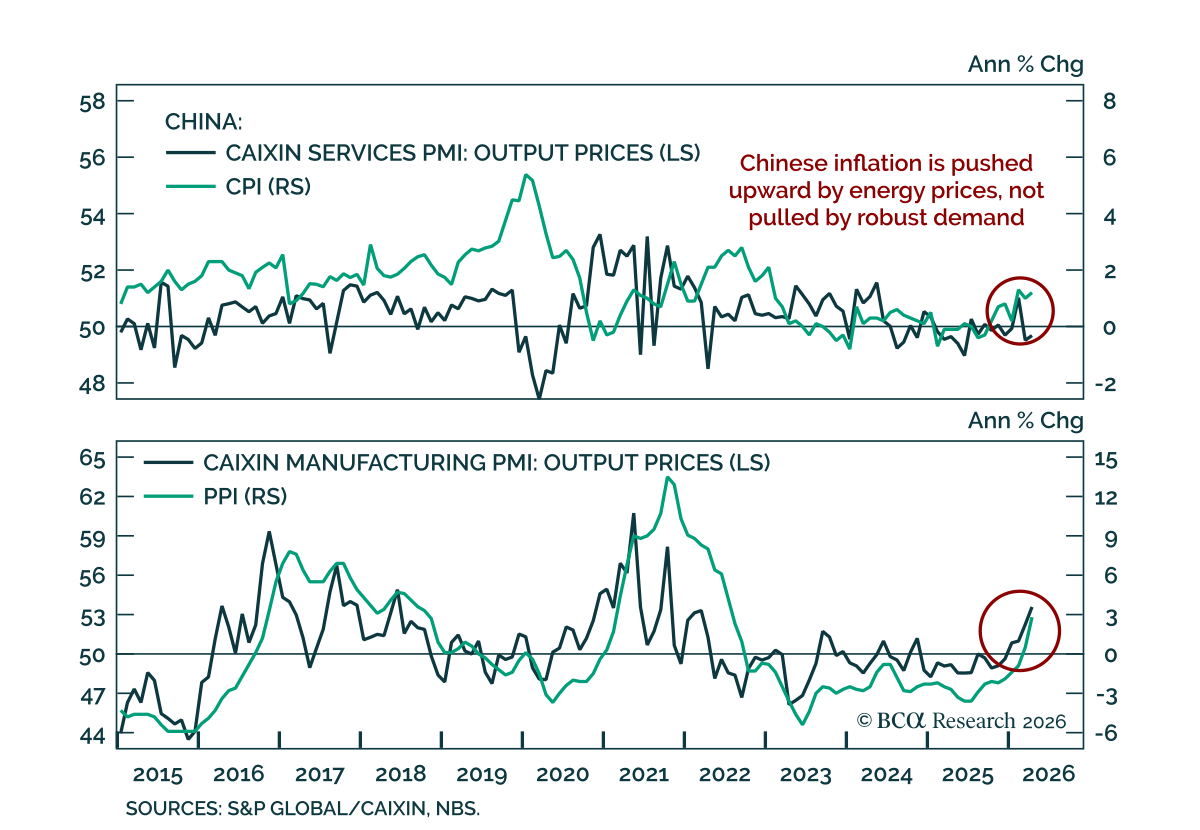

Chinese inflation surprised to the upside, but the rise reflects higher energy prices rather than stronger demand. CPI rose 1.2% y/y versus 0.9% expected, while PPI was the bigger surprise at 2.8% y/y, almost double consensus. The PPI move matters more…

The global economy has weathered the oil shock reasonably well so far. However, the risk of a recession will increase meaningfully if the Strait of Hormuz remains closed into June.

This morning’s CPI report signals that the worst of the tariff impact on inflation may already be in the rearview mirror.