Equities

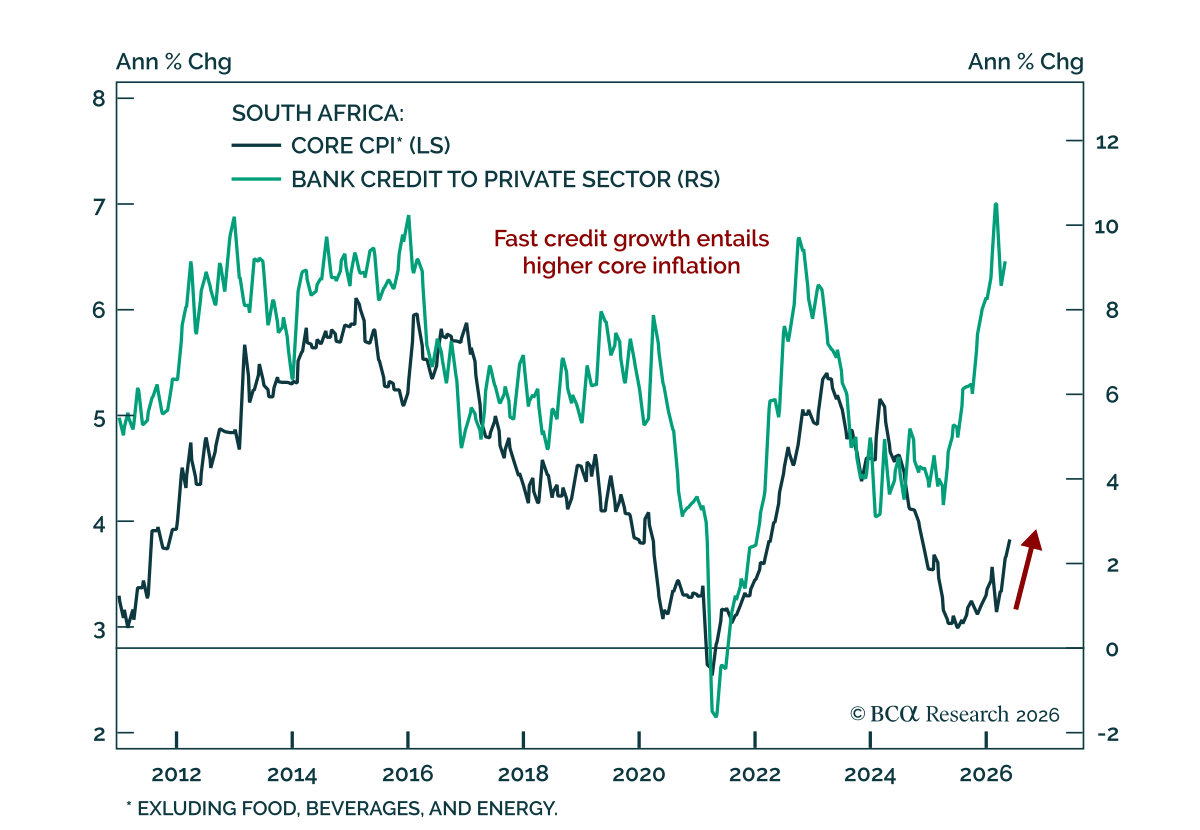

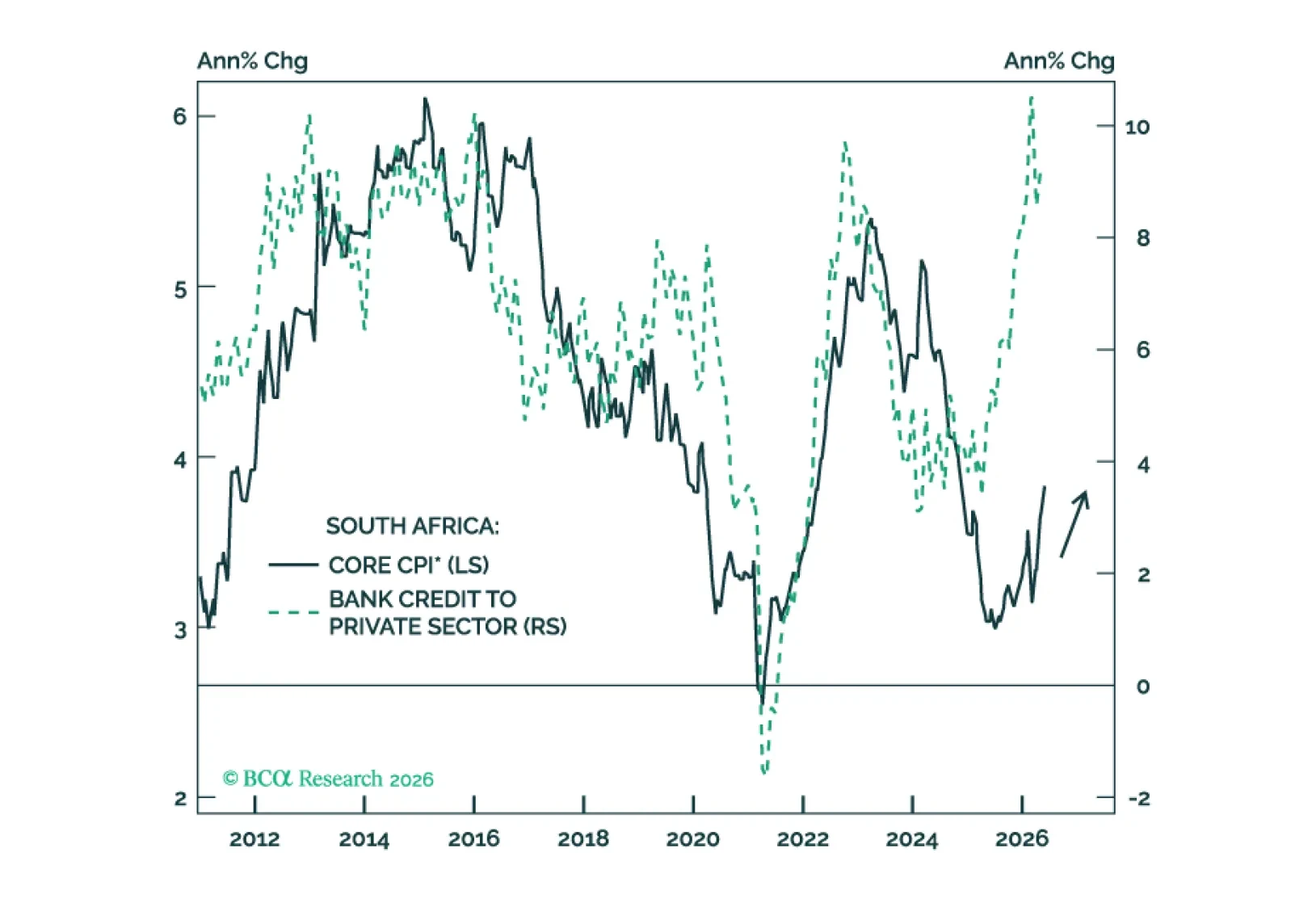

South Africa’s ambitious reform agenda will take time to bear fruit. Meanwhile, the country faces a stagflationary squeeze as inflation rises while growth slows. South African stocks, bonds, and currency are all vulnerable.

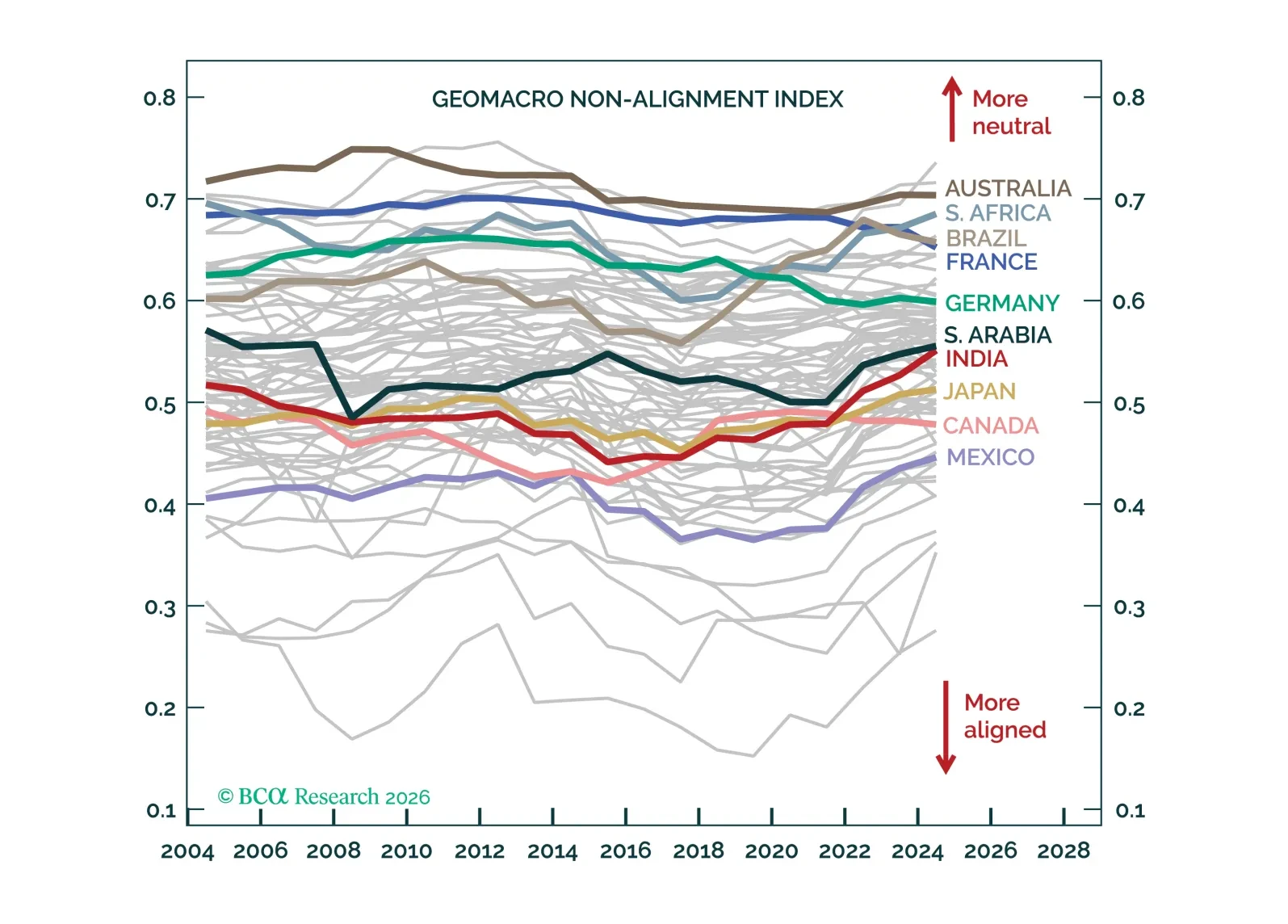

We have long argued, on a case-by-case basis, that countries willing to play the superpowers against each other win in a multipolar world. The logic is intuitive, and in this report, we measure it systematically.

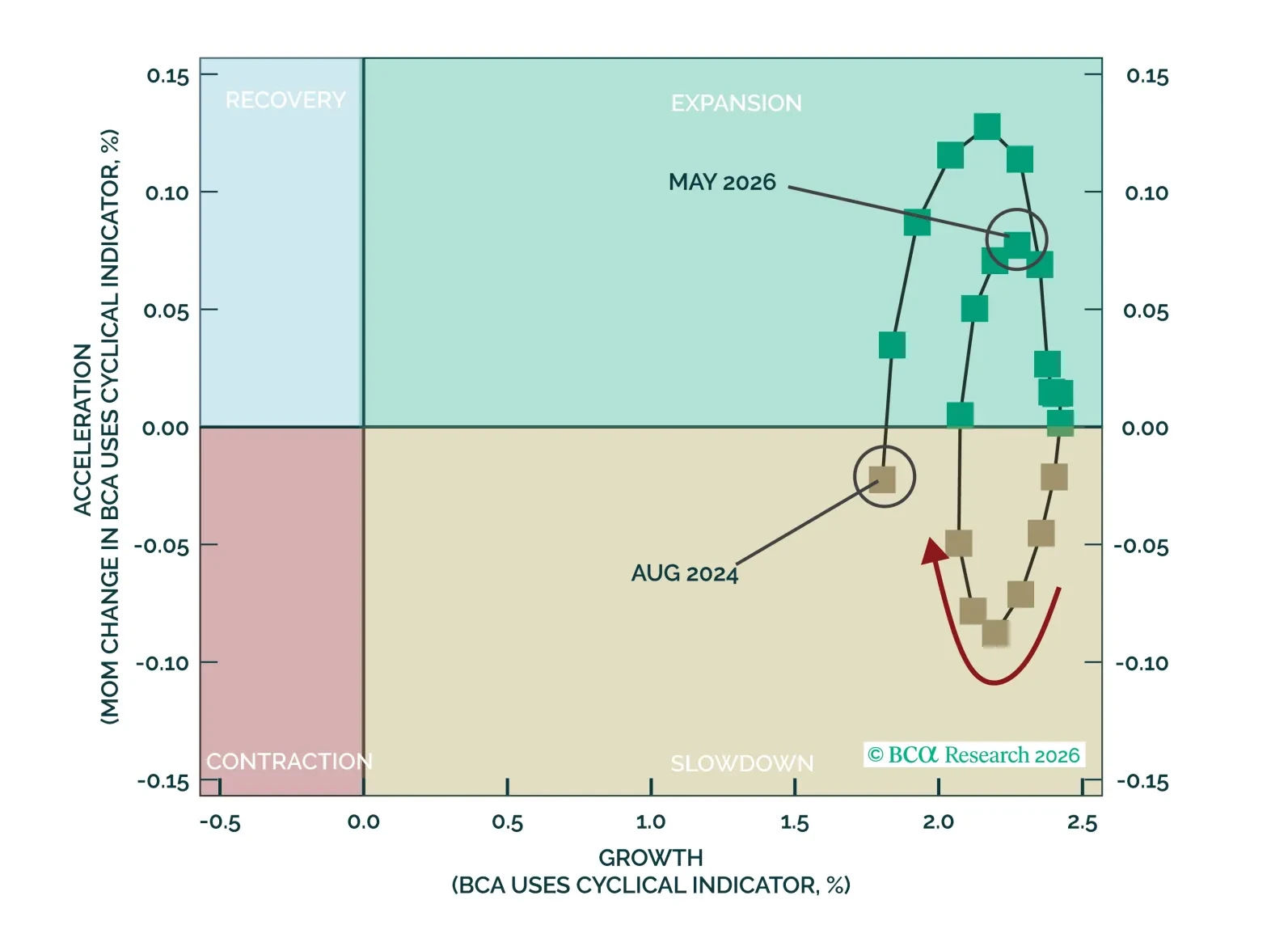

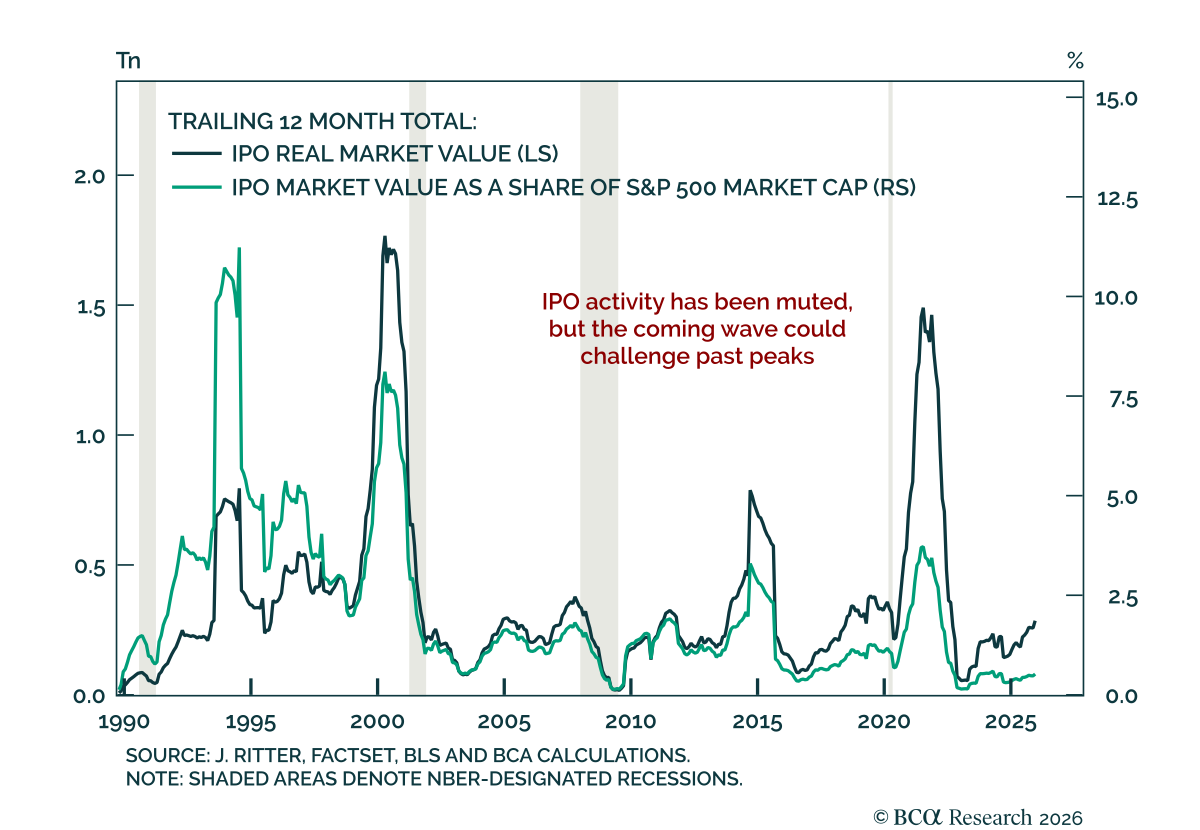

The June swoon looks like a rotation and rebalancing-driven air pocket, not a regime break. Economic growth, earnings revisions, and AI-driven capex demand remain firm, but rising yields, inflation concerns, Fed uncertainty, and a looming IPO wave are likely to constrain further multiple expansion. But progress toward a resolution of mid-east tensions, rallying bonds, and falling oil prices, have motivated us to add a tactical long consumer discretionary trade.

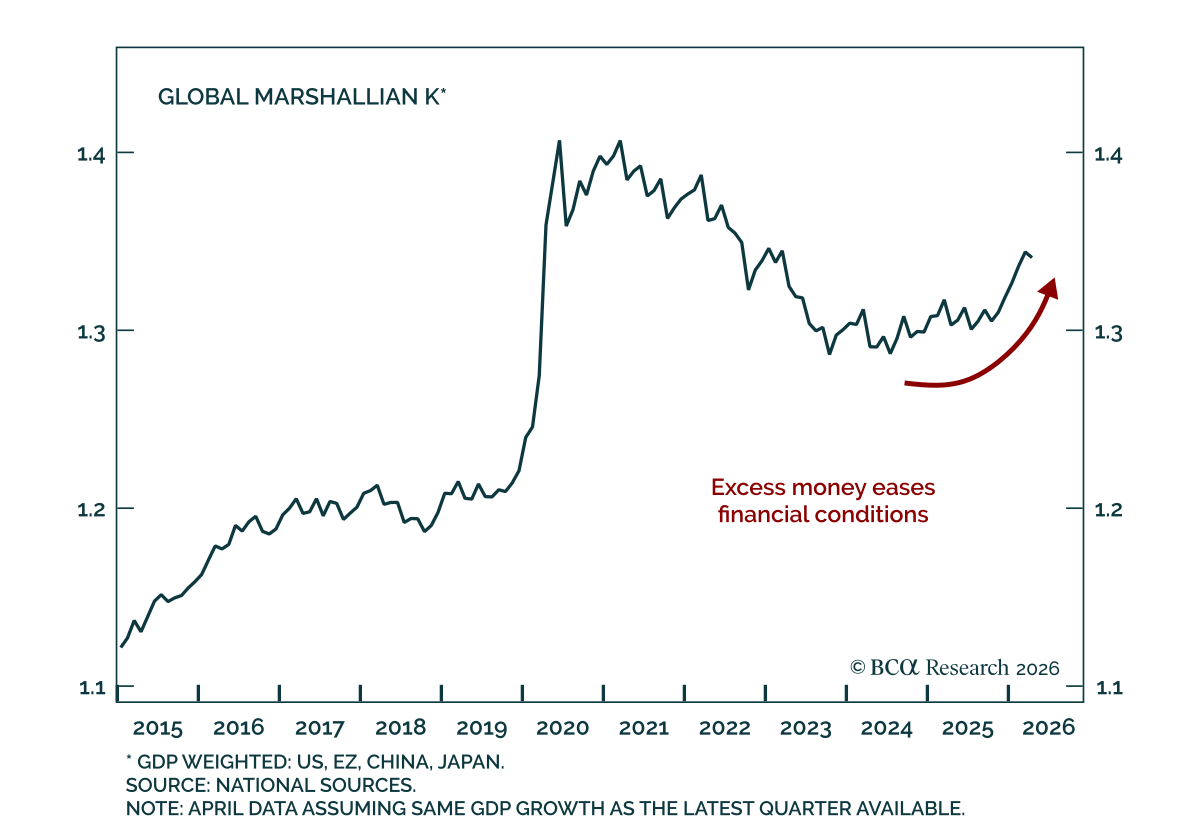

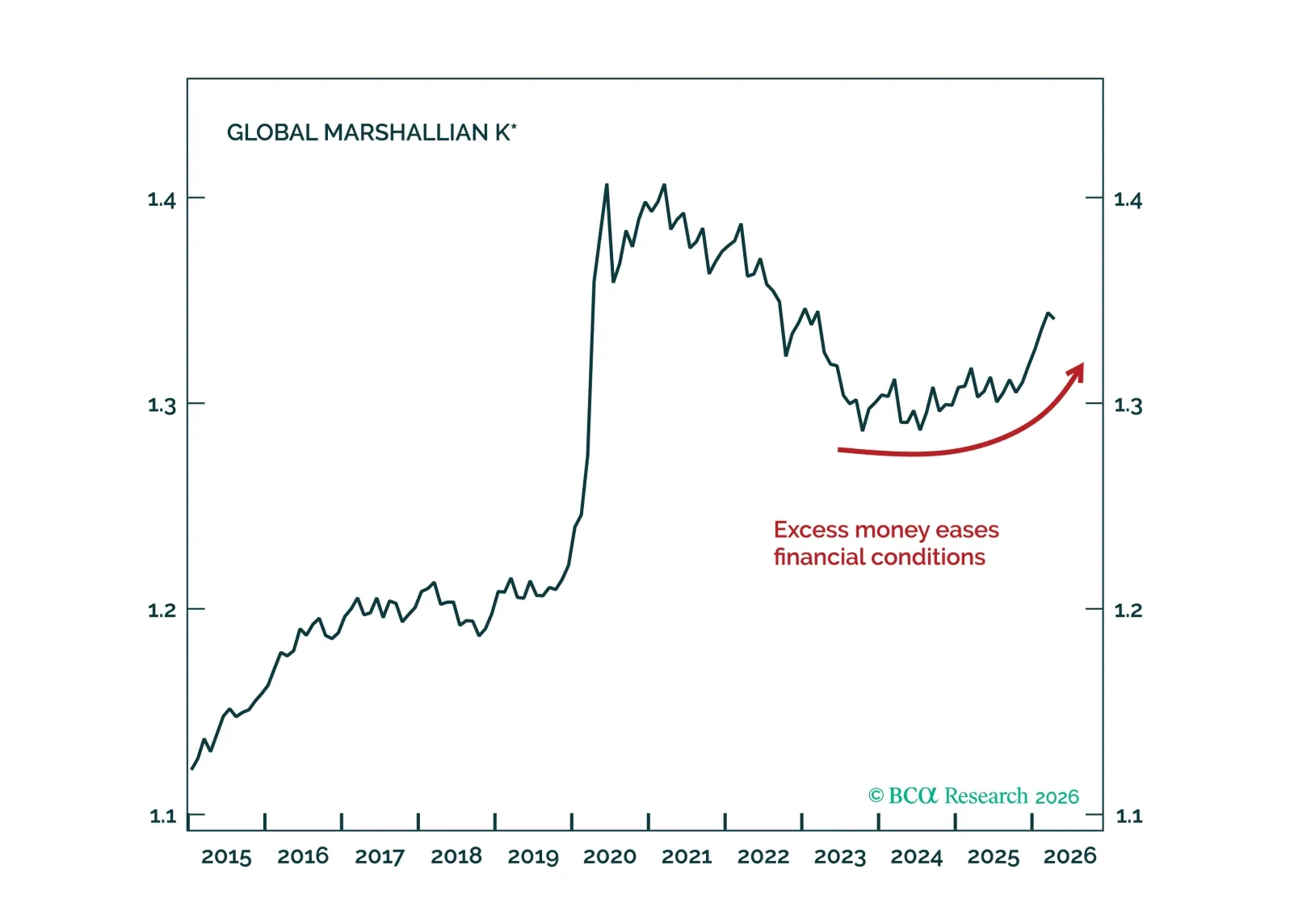

Markets keep buying the dip because liquidity remains plentiful. That buffer lasts through 2026; the bigger question is what happens when it thins in 2027.

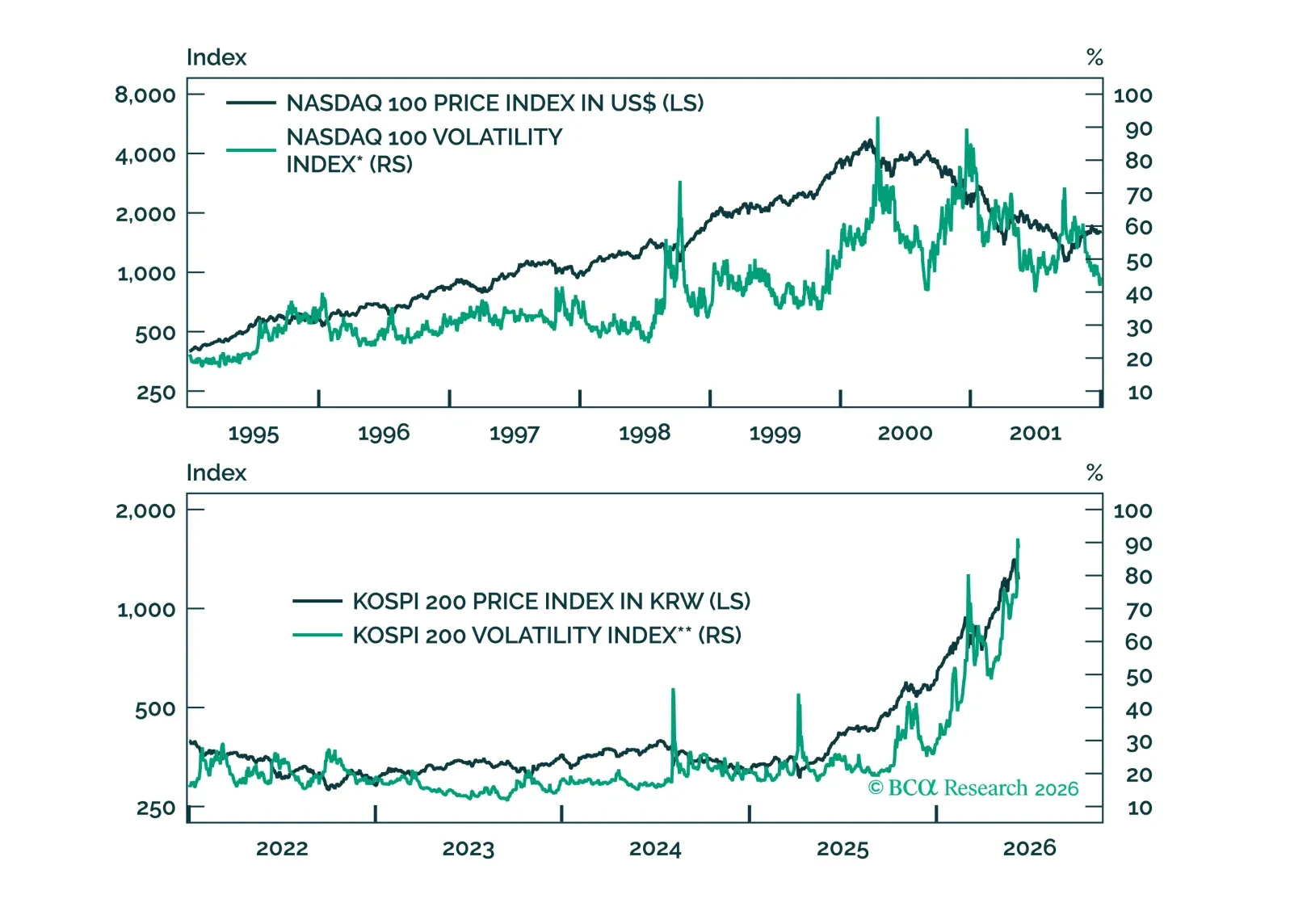

Rising volatility in Korean markets captures a late-cycle surge in which euphoria and drawdown risk are rising together. While KOSPI momentum remains intact, the bigger opportunity may be emerging in the increasingly mispriced KRW, which could rally meaningfully as portfolio flow headwinds fade.