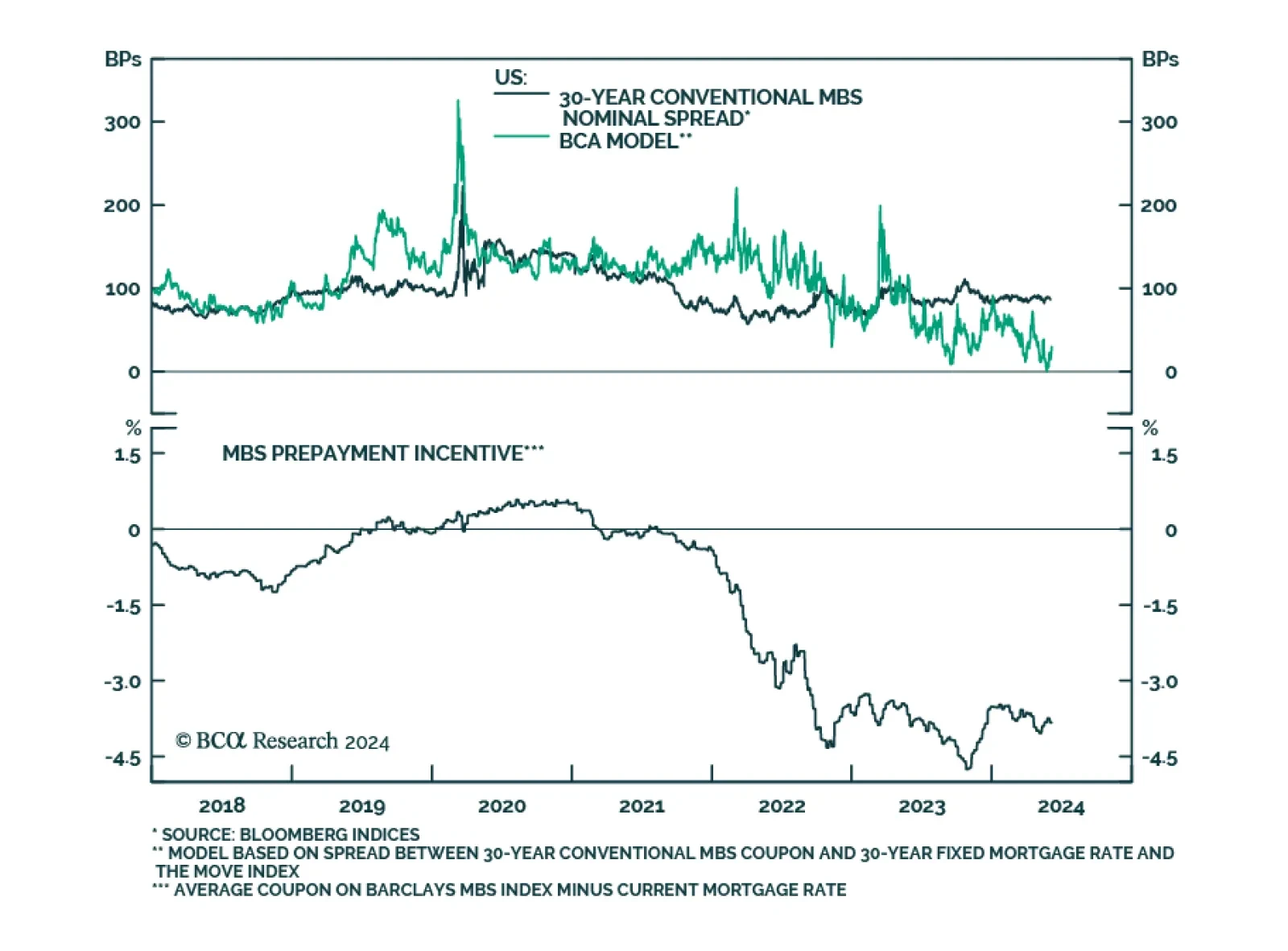

Yield Curve

Our Portfolio Allocation Summary for June 2024.

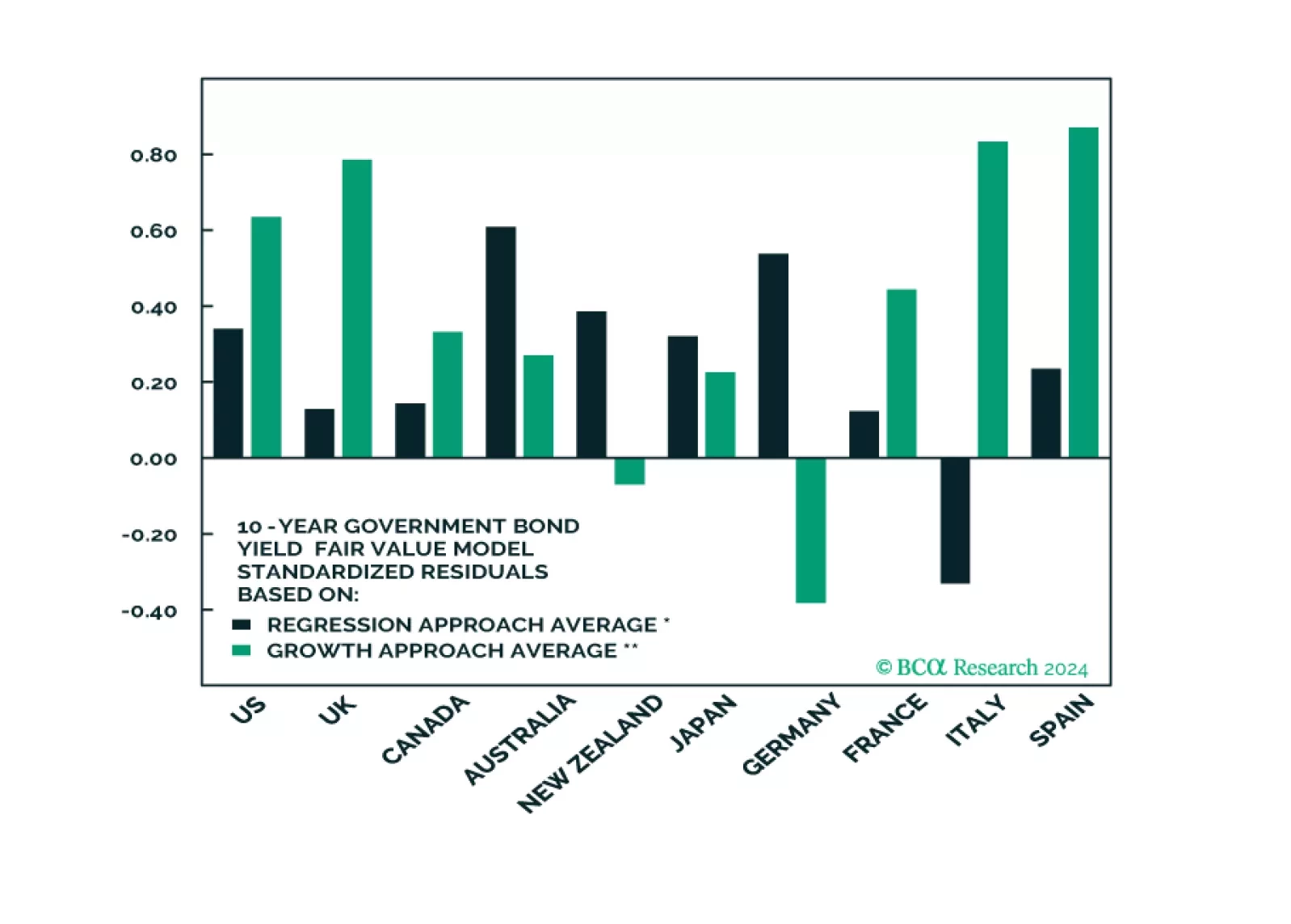

In this Special Report we assess the absolute and relative attractiveness of developed market government bonds using several fair value models. Longer-term investors who are focused on value should overweight US long-maturity bonds, and favor Spanish, Australian, and potentially UK government bonds within a DM ex-US allocation.

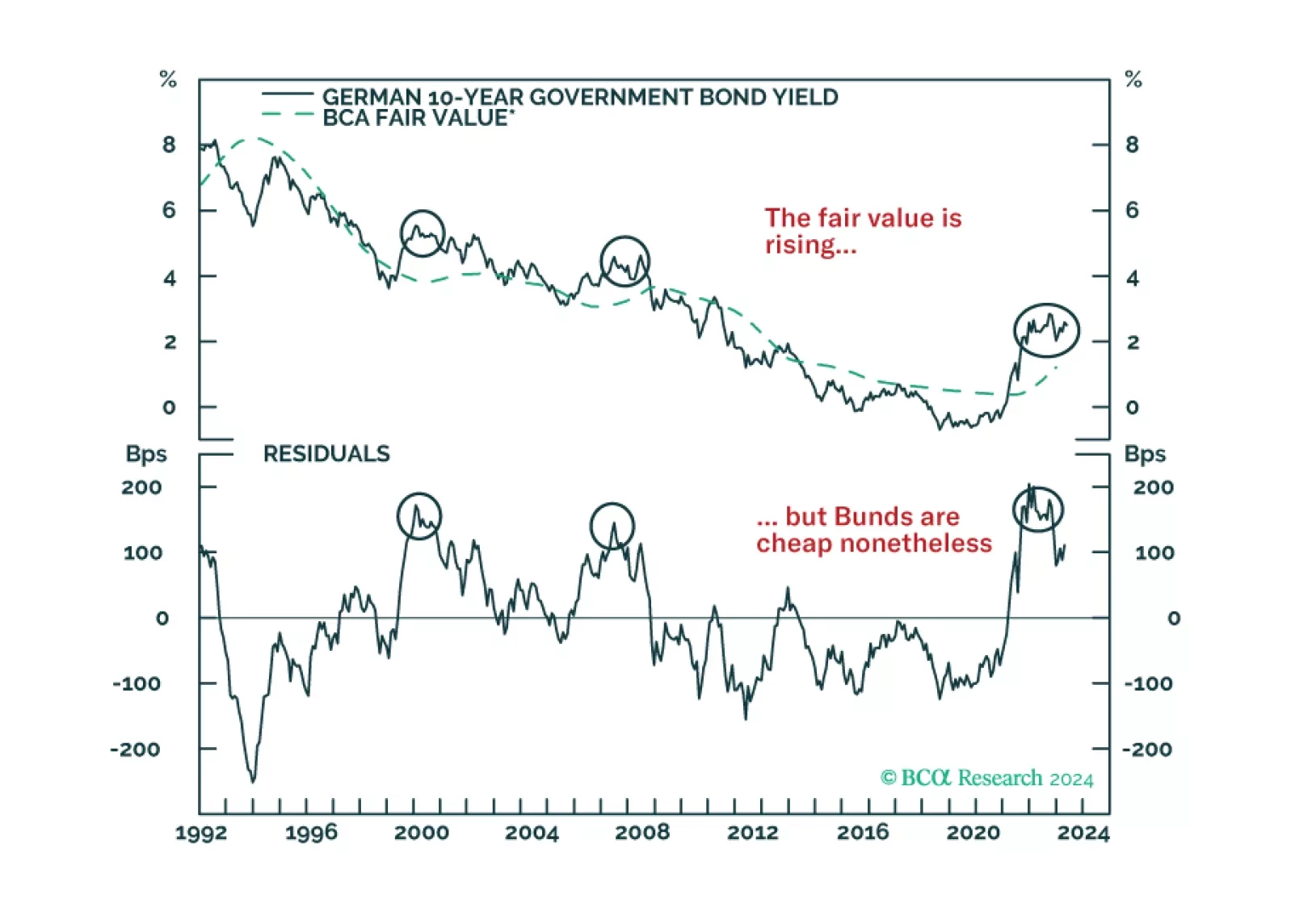

German Bunds have cheapened considerably, and the ECB is about to start cutting rates. Does this combination guarantee immediate profits from buying these bonds?

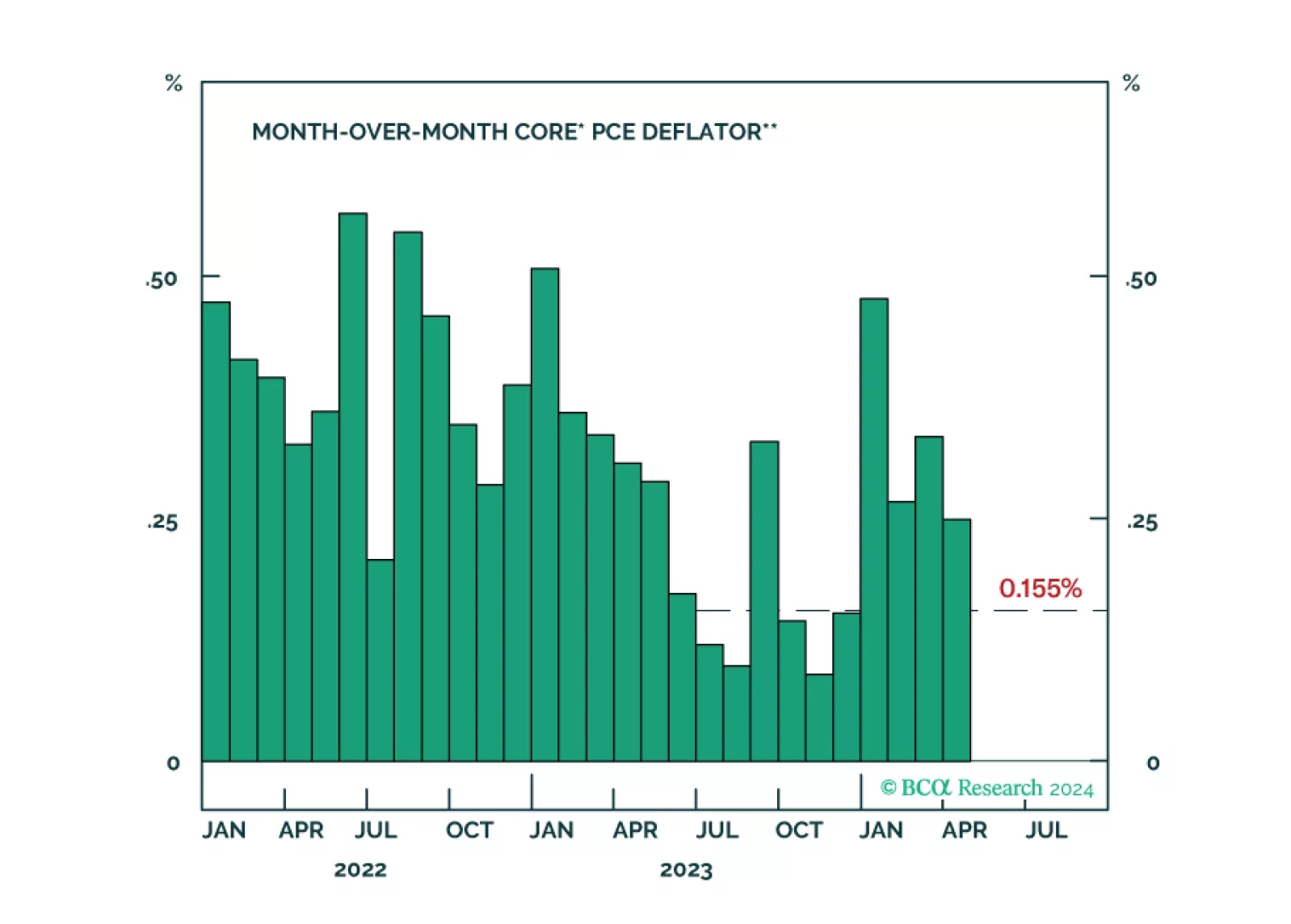

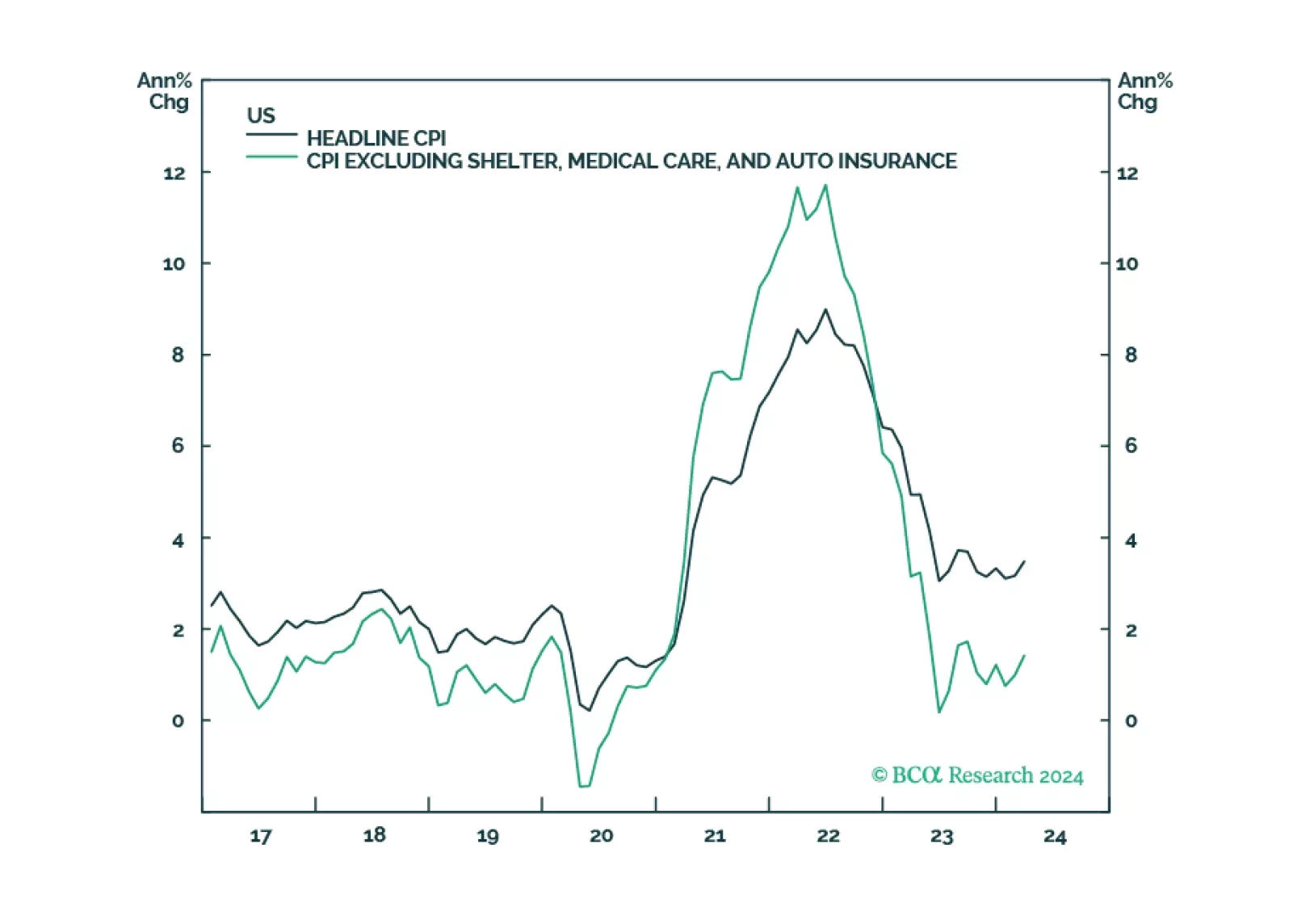

In this week’s report, we defend four out-of-consensus claims. Claim #1: Underlying inflation in the US is not reaccelerating. Claim #2: The US labor market is set to weaken abruptly. Claim #3: The S&P 500 will drop to 3700 in 2025. Claim #4: Japan is not in danger of a currency crisis.

Our Portfolio Allocation Summary for May 2024.

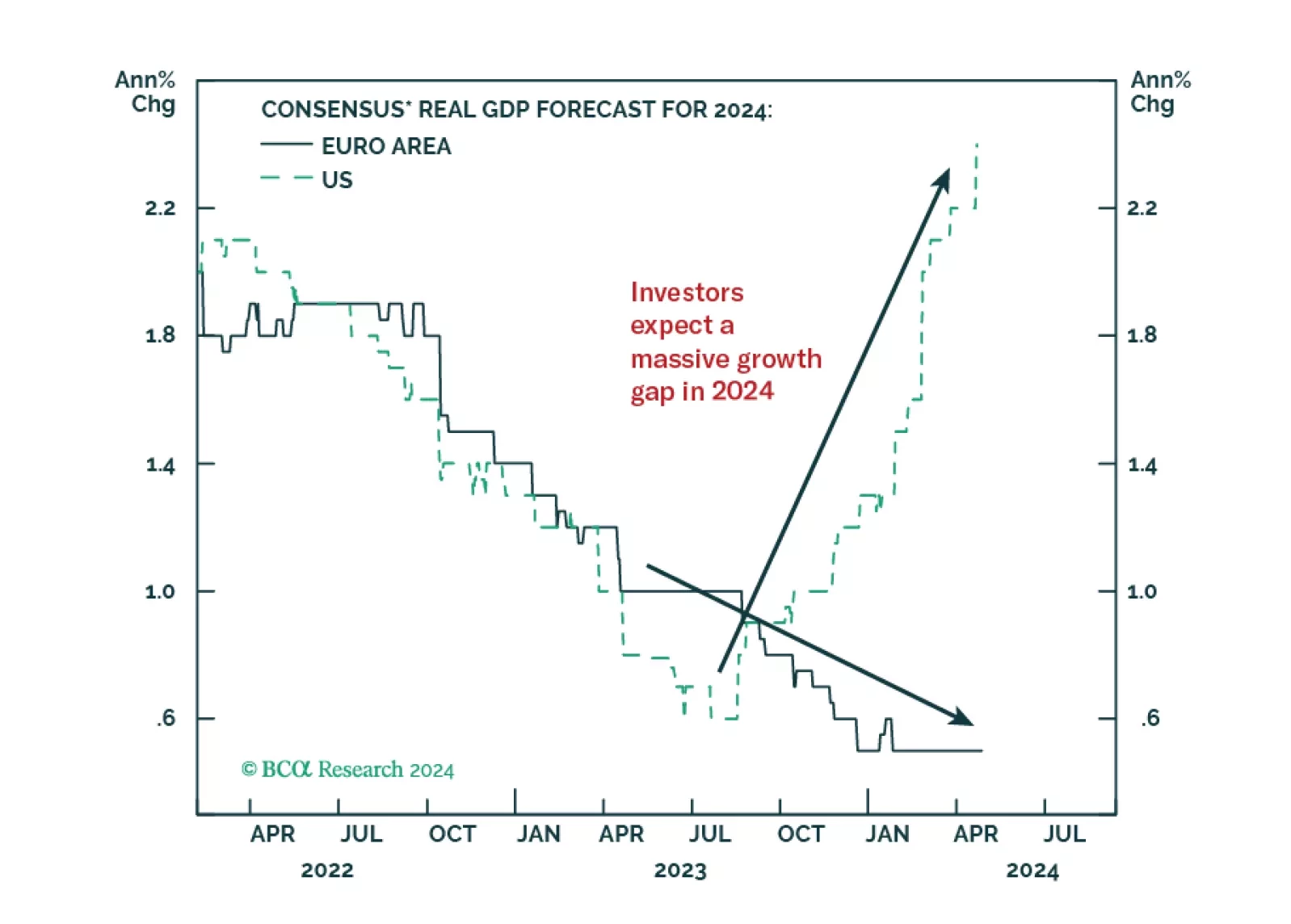

Investors anticipate a record growth gap between the US and the Eurozone in 2024. Does this skewed expectation create market opportunities?

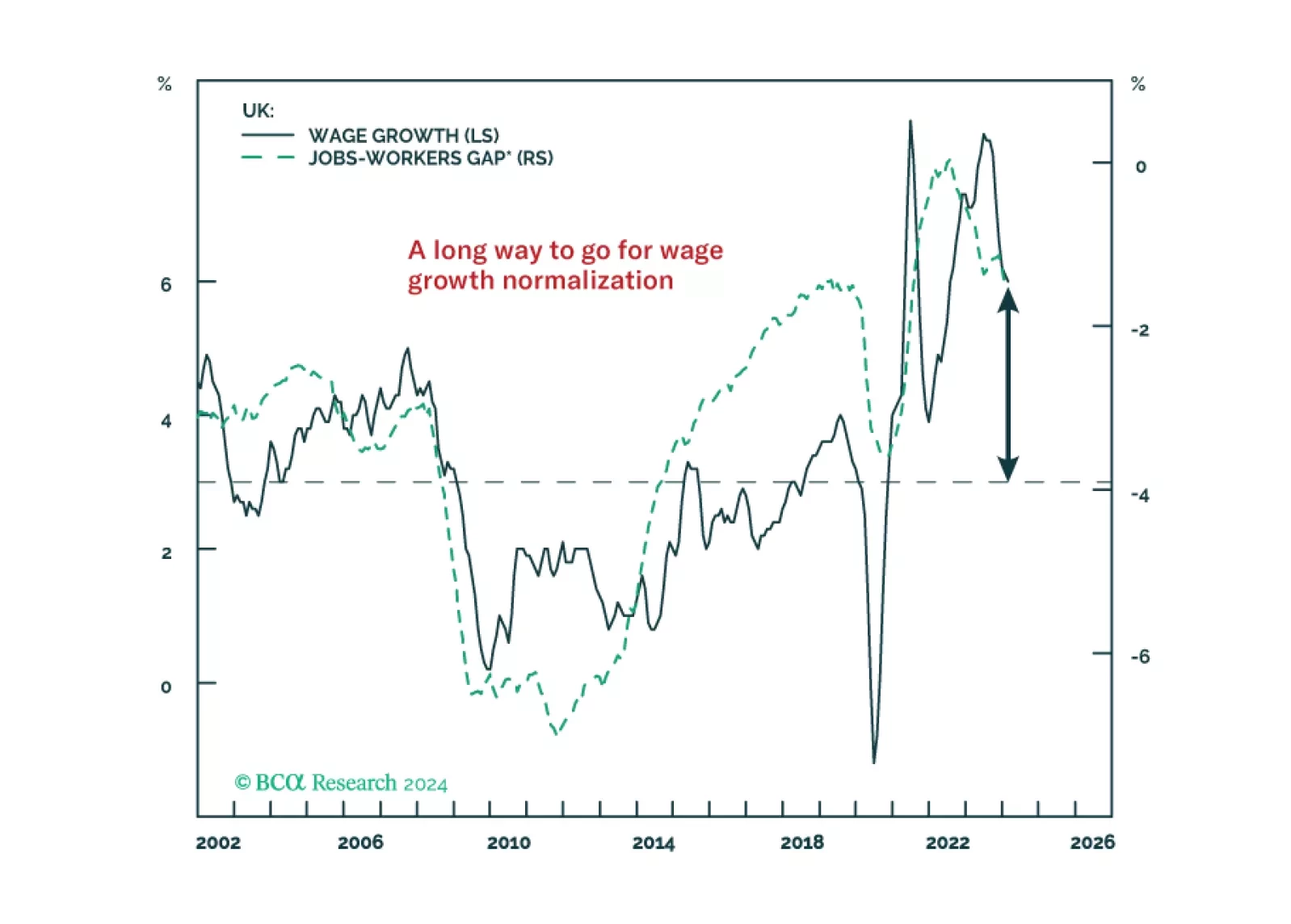

The UK labor market remains far too tight to expect wage growth to slow to levels consistent with the Bank of England inflation target. A true recession with rising unemployment is needed to finally slay the UK inflation beast. 2024 rate cuts are off the table, with the central bank having to keep monetary policy tighter for longer than markets expect and the UK economy now rebounding. We recommend downgrading UK gilts to underweight in global bond portfolios, while also looking for opportunities to buy the British pound on pullbacks versus the euro, Canadian dollar and Swedish krona.

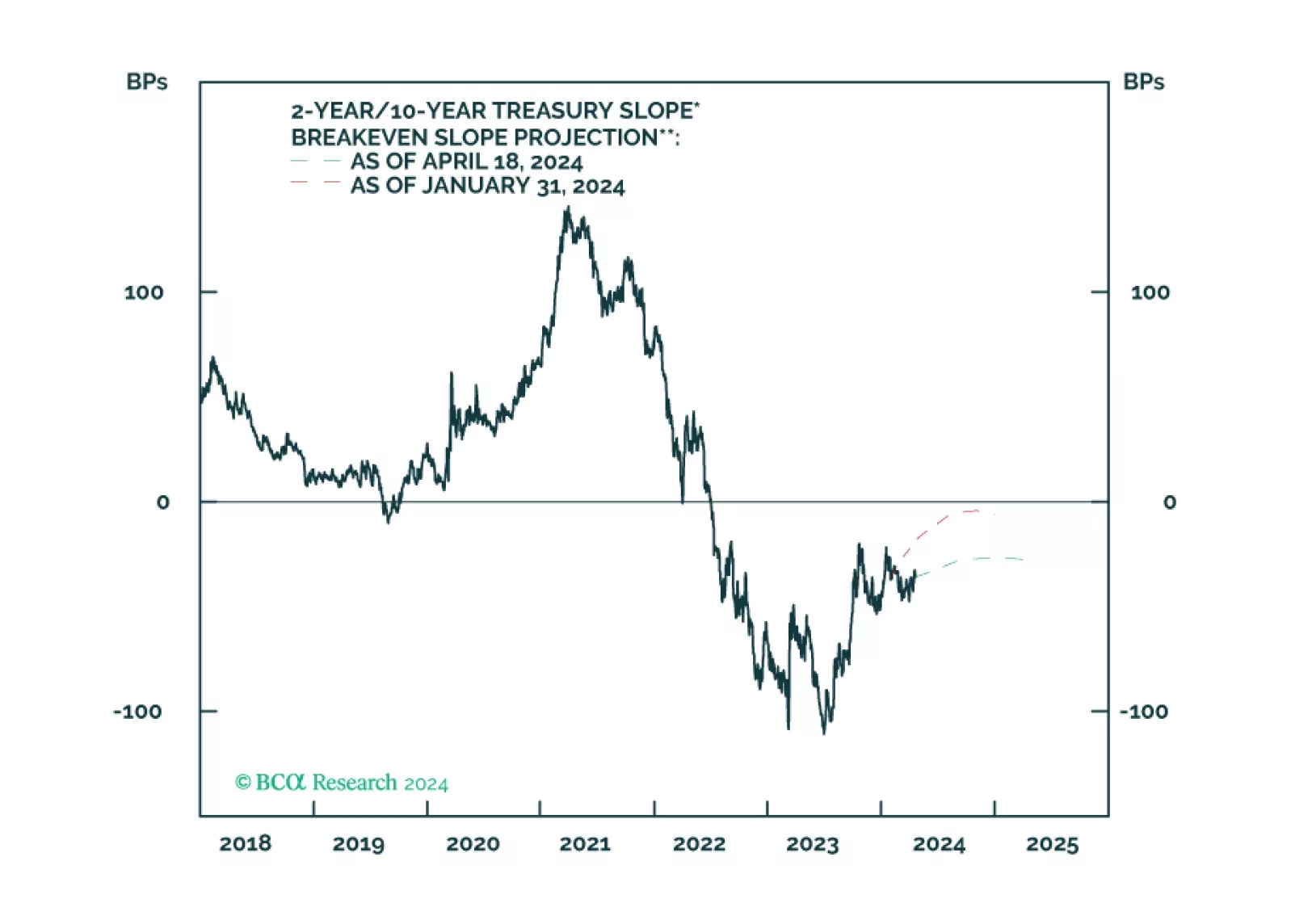

This Special Report introduces a framework for assessing the relative importance of slope change and initial yield in curve trade performance. The yield penalty for curve steepeners has fallen significantly since the beginning of the year, and we recommend shifting out of Treasury curve flatteners and into Treasury curve steepeners in US bond portfolios.

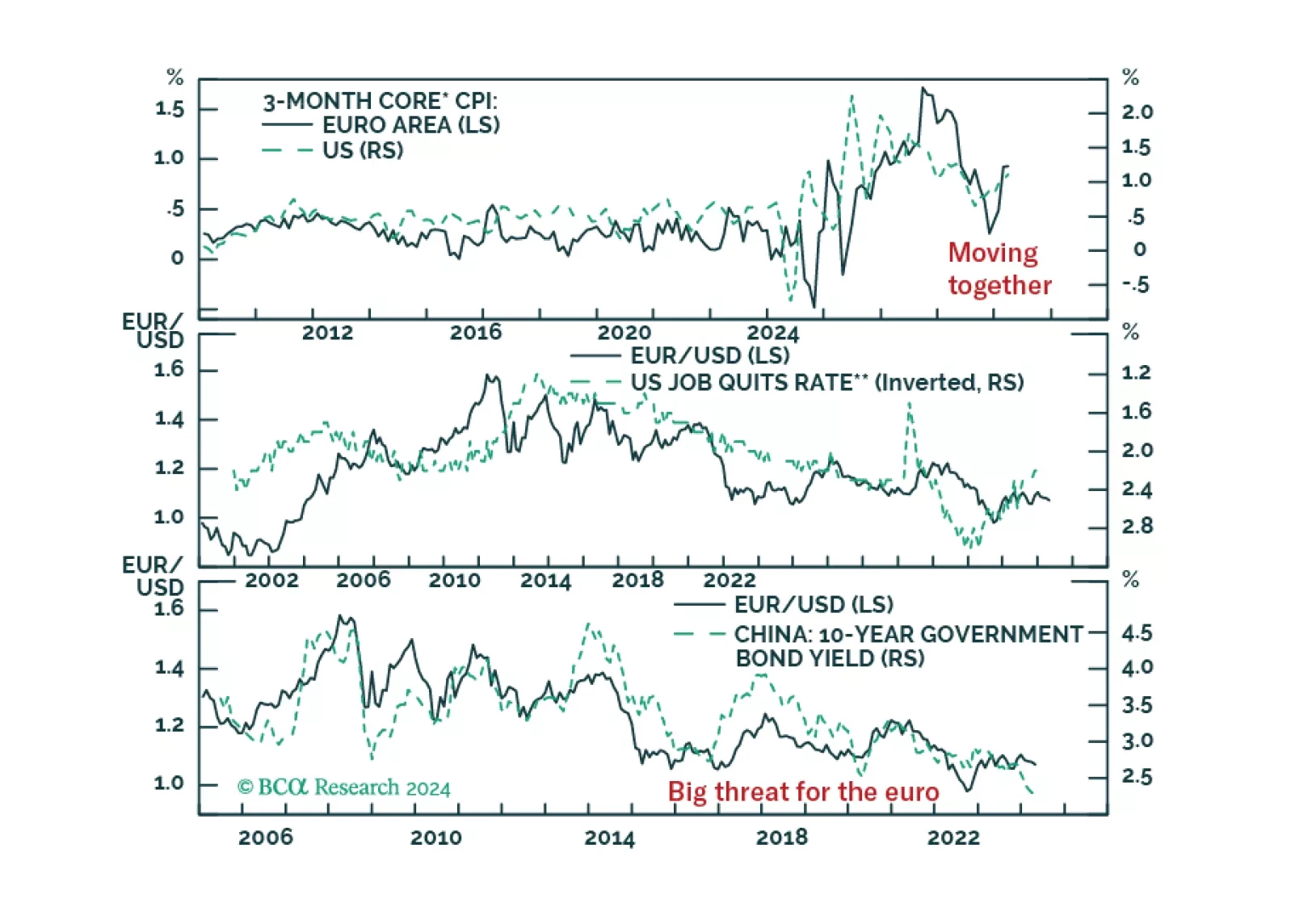

EUR/USD collapsed in the wake of last week’s hotter-than-expected US CPI report. Is this pessimism warranted and will the euro’s trading range that has prevailed since 2023 breakdown?