Yield Curve

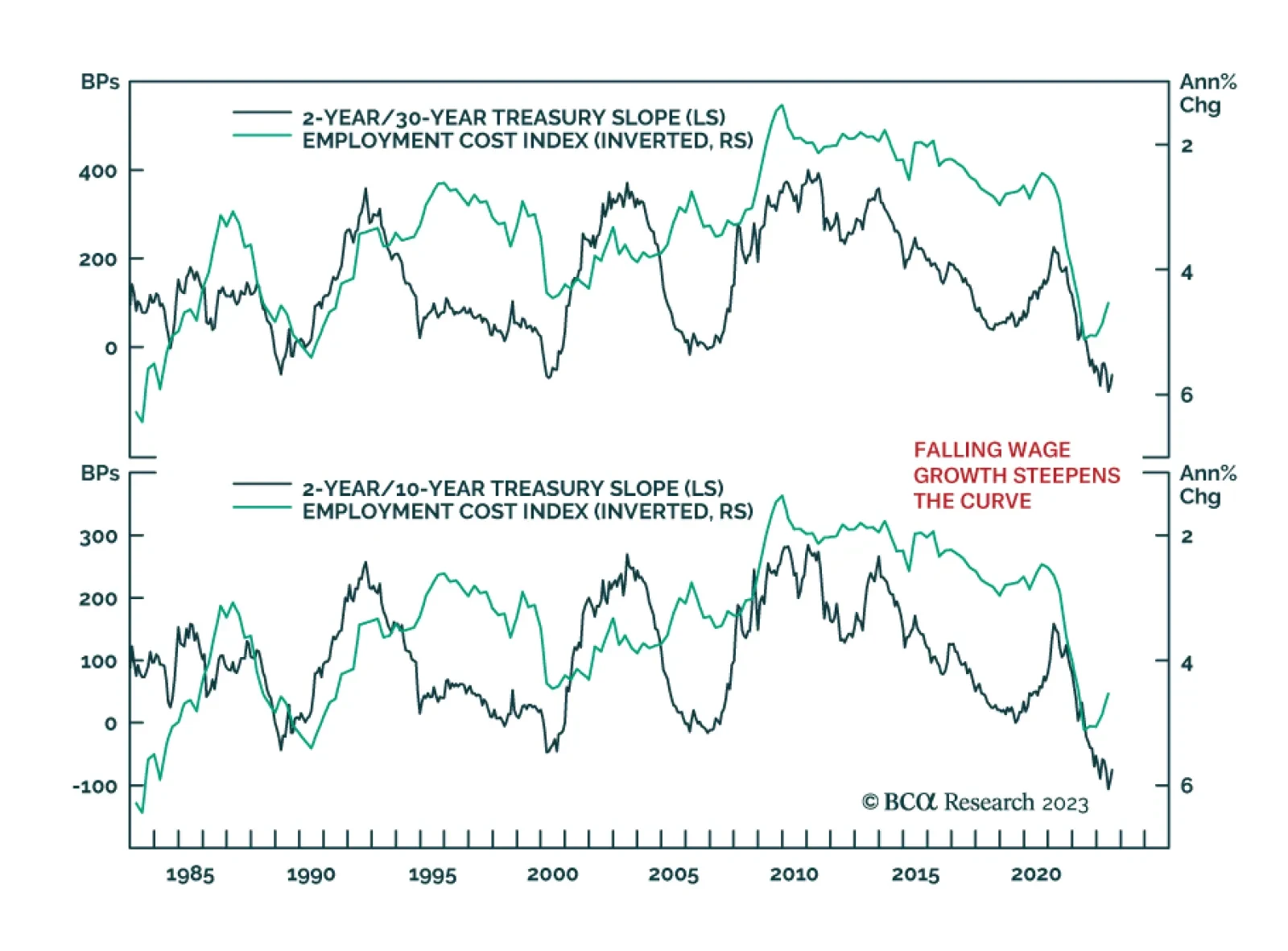

The recent bear-steepening of the US Treasury curve has been driven by the combination of stronger-than-expected economic growth and stable Fed rate expectations. Historically, such periods do not last very long, and we see the current bear-steepening episode ending soon. We also highlight an opportunity in Agency MBS.

US monetary policy is restrictive, as evidenced by a falling jobs-workers gap. The reason that unemployment has not risen is because labor demand still exceeds supply. That will change in the second half of 2024 when the US economy succumbs to recession. Investors should increasingly favor bonds over stocks.

We present our Portfolio Allocation Summary for October 2023.

Aggressive monetary tightening has always led to recession, although the timing is uncertain. The effects of high interest rates are starting to be felt. Investors should stay risk off and buy government bonds as a safe haven investment with carry.

A discussion of today’s FOMC meeting and its investment implications.

In this report, we review our European fixed income strategy recommendations ahead of tomorrow’s critical ECB meeting

Our Portfolio Allocation Summary for September 2023.

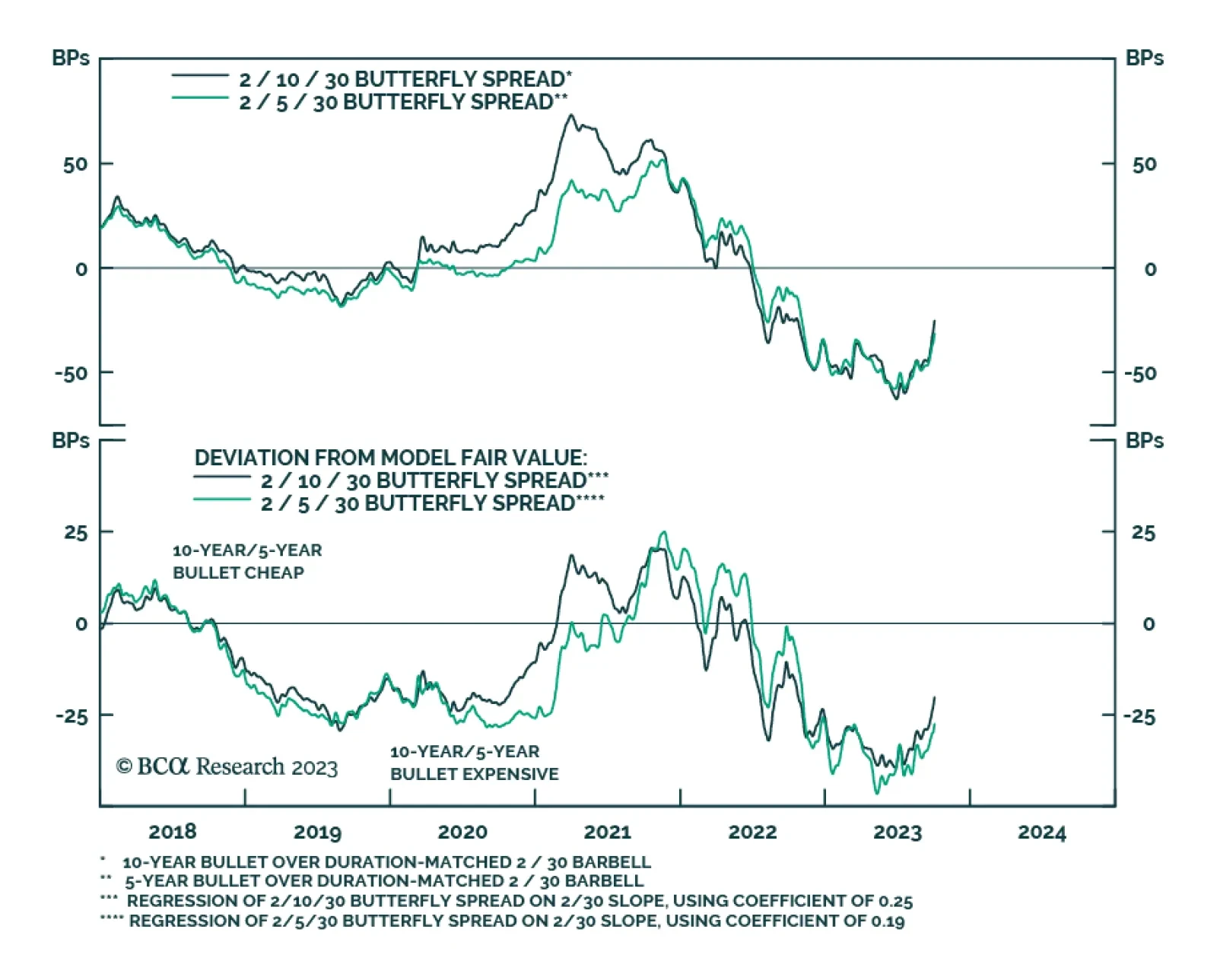

We comment on Jay Powell’s Jackson Hole speech and recommend shifting to a barbelled allocation along the Treasury curve.