Yield Curve

We present the performance review of the Global Fixed Income Strategy Model Bond Portfolio for 2023. We also discuss the outlook for 2024 performance based on our Key Views for the year. The portfolio is positioned to benefit from a year where the global backdrop will be one of weak growth and further declines in inflation, leading central bank to begin cutting interest rates.

Low inflation argues for the Fed to move relatively quickly toward rate cuts. Continued above-trend GDP growth poses a risk to this view, but leading indicators point to slower growth in the coming quarters.

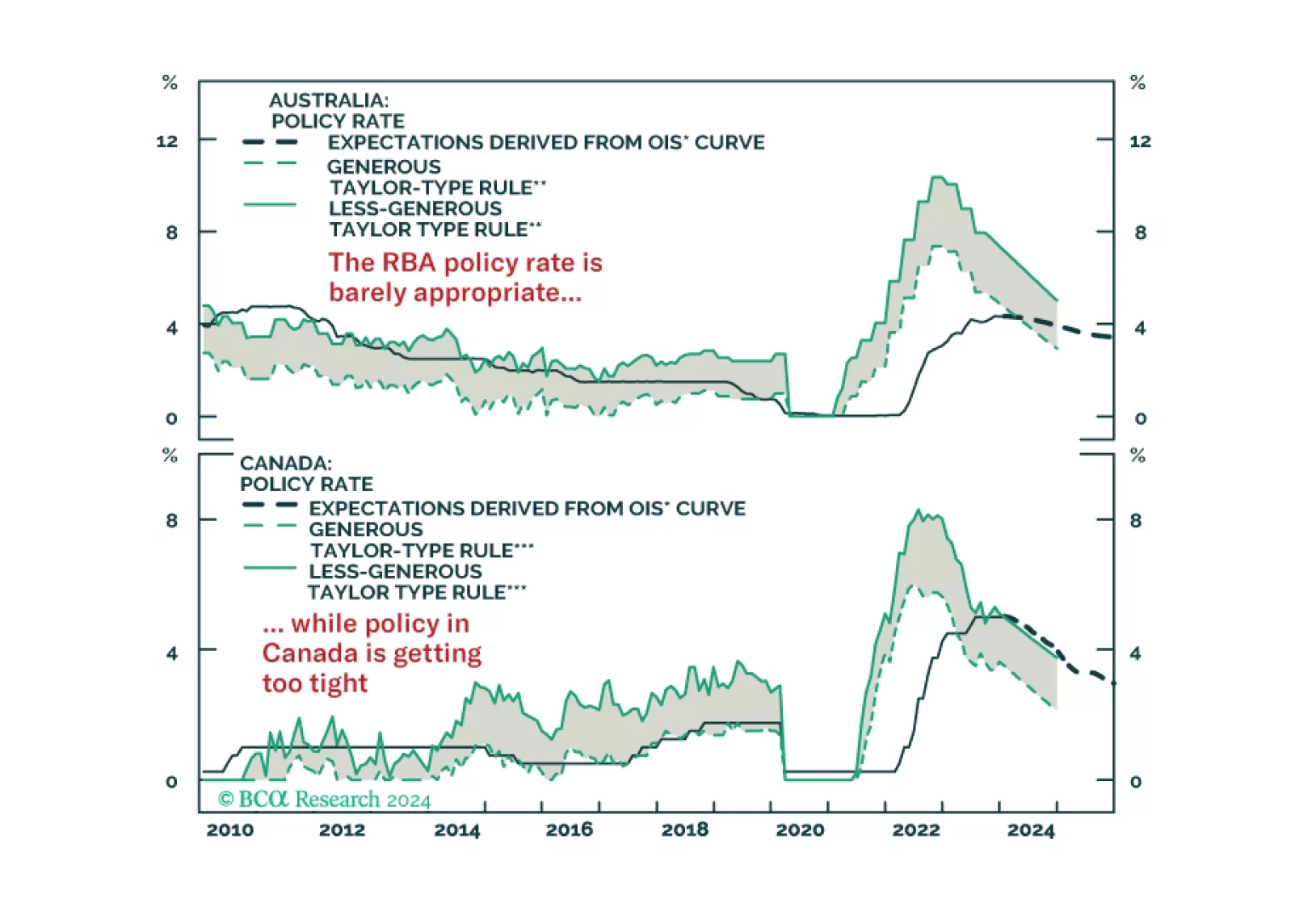

In this Strategy Insight, we assess the monetary policy path for Australia and Canada in 2024 and we discuss how to profit from a growing divergence between the two economies.

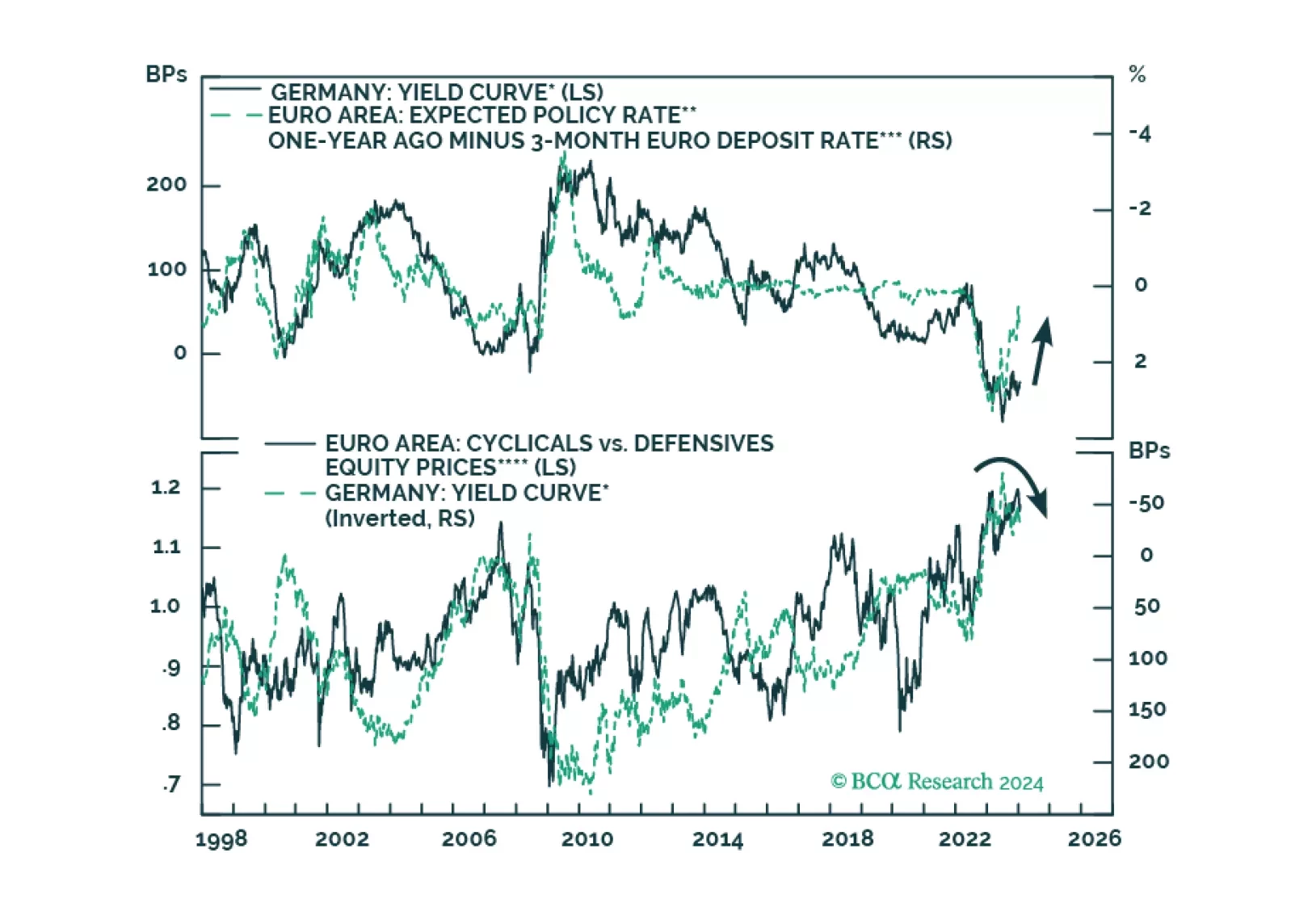

The ECB will begin cutting rates in June, what does this start date imply for the yield curve and European cyclicals?

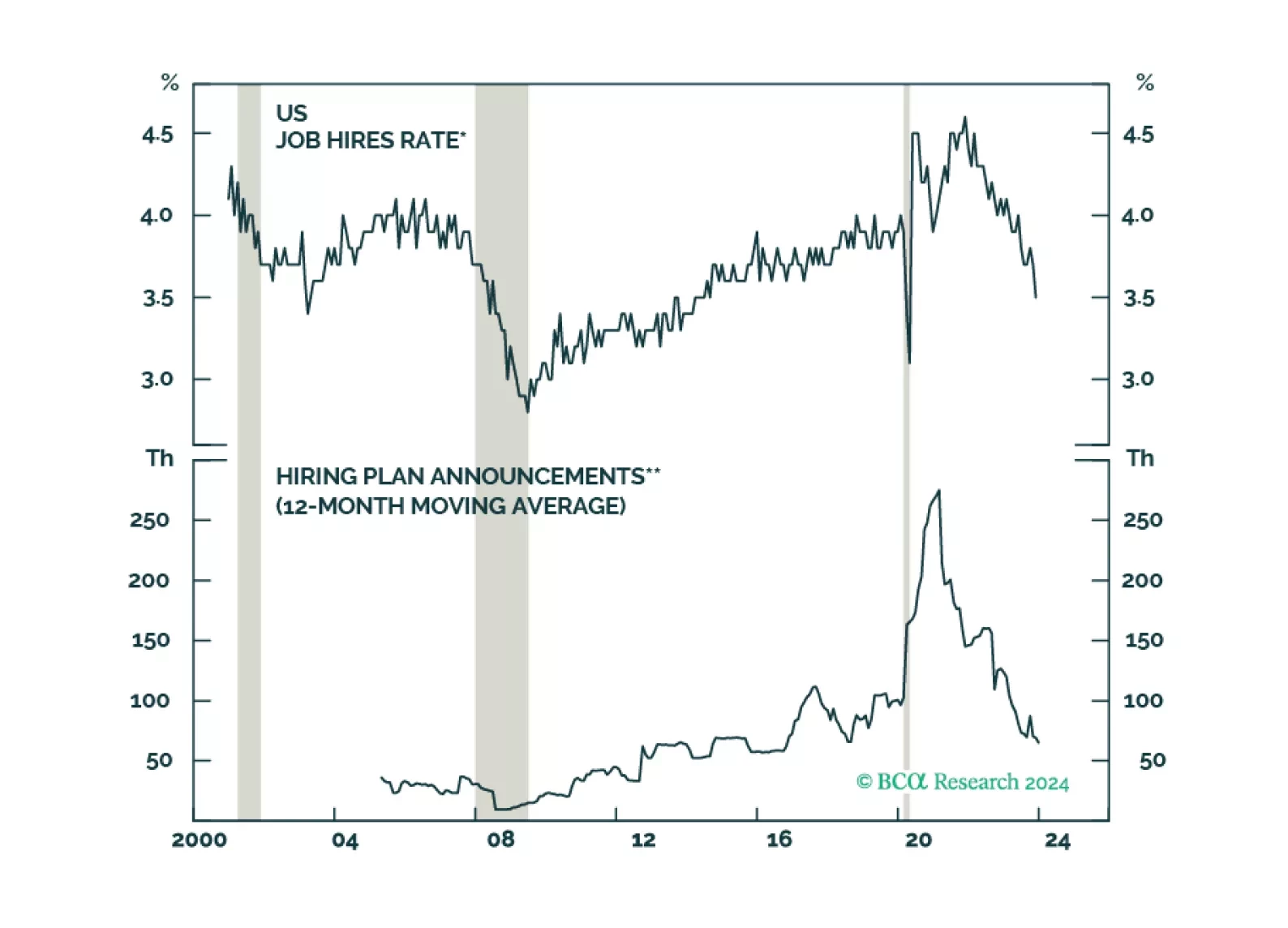

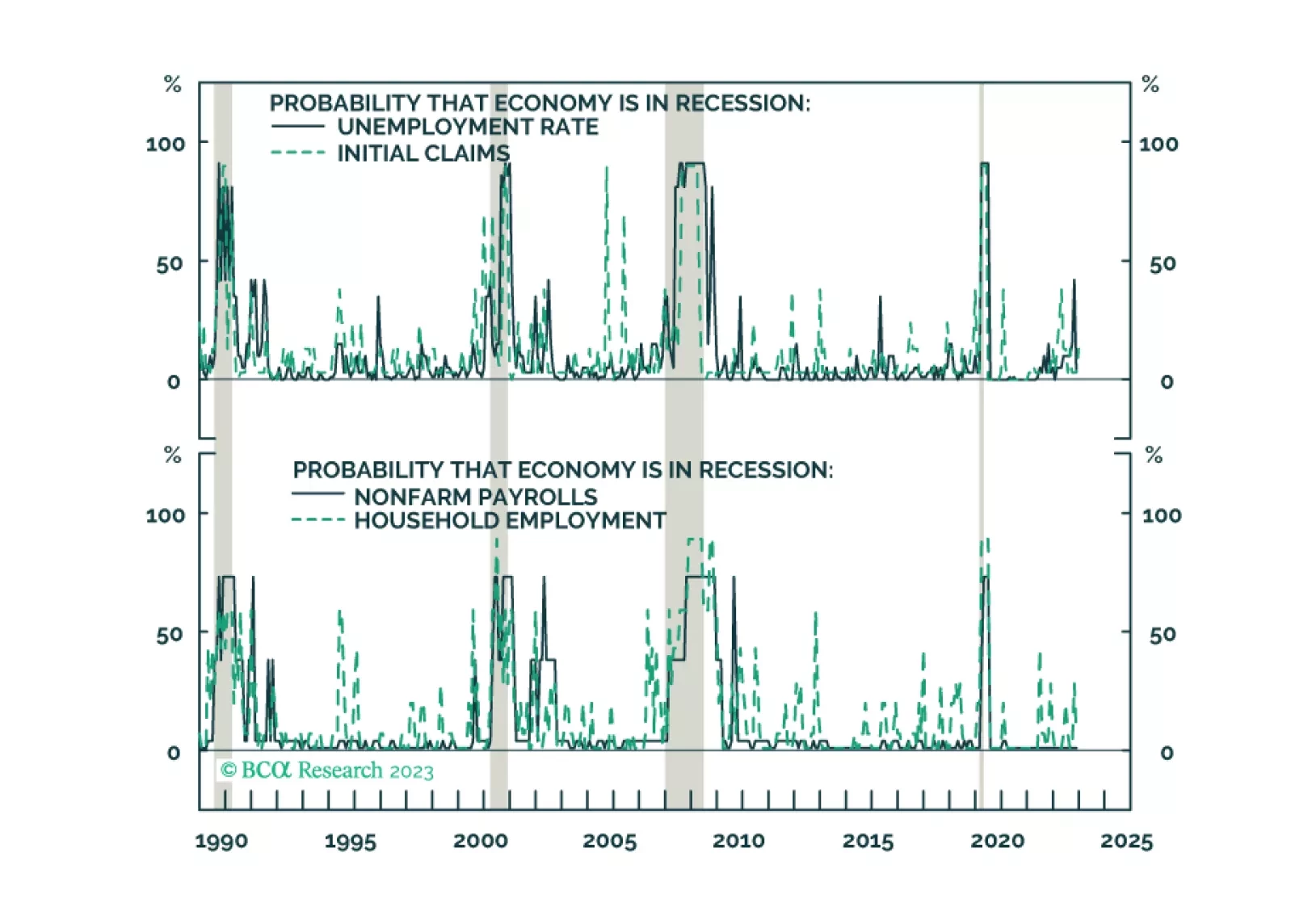

Investors have taken comfort in the fact that unemployment has remained low in the major economies. But underneath the surface, there are clear signs that labor demand is weakening. The clock keeps ticking towards our H2 2024 recession call. After being bullish on risk assets last year, we are slowly turning more defensive.

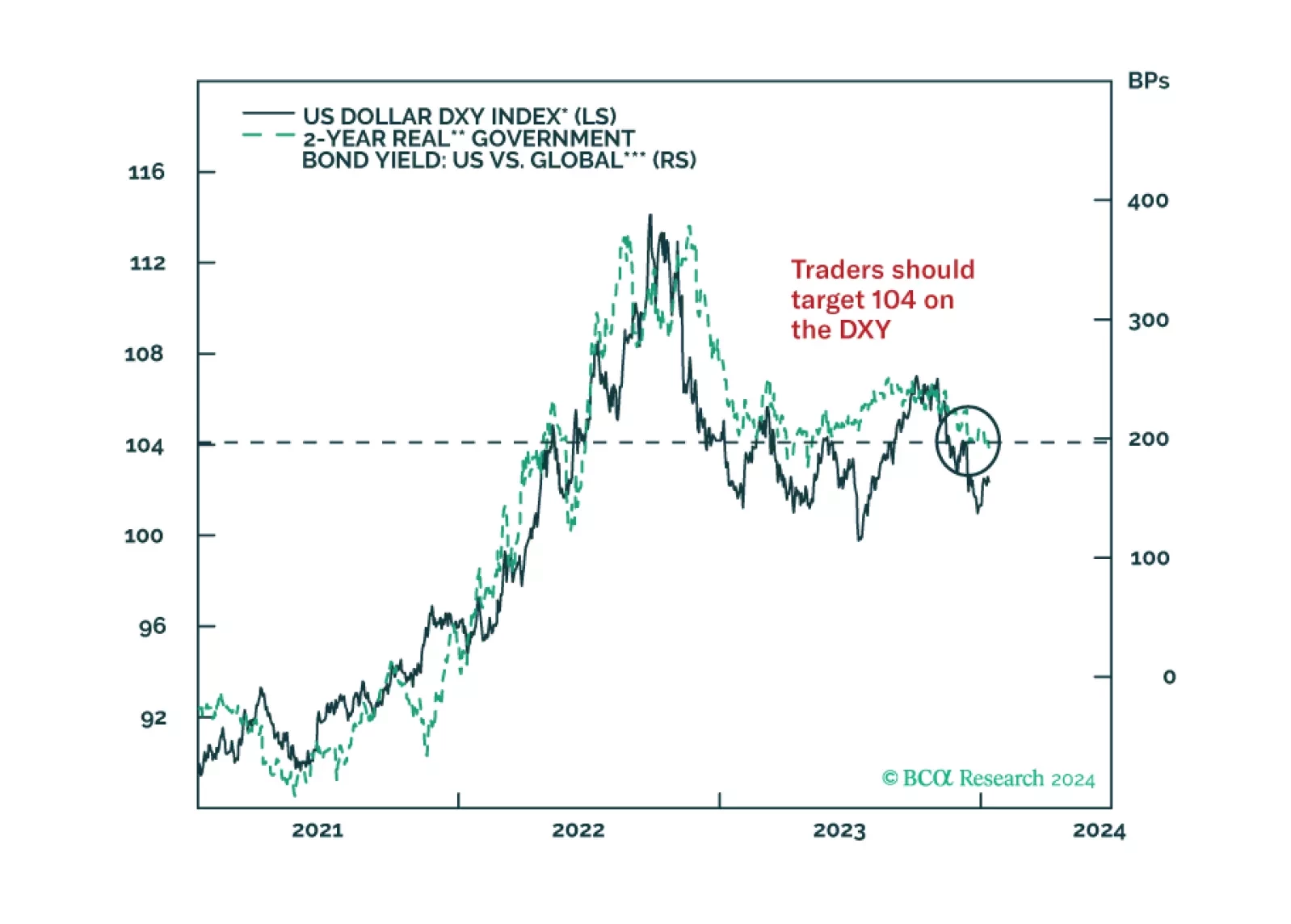

In light of the hotter-than-expected US CPI report, we look at what interest rate currency investors should focus on. Our conclusion largely keeps our existing trades in place, as published in our outlook, a few weeks ago.

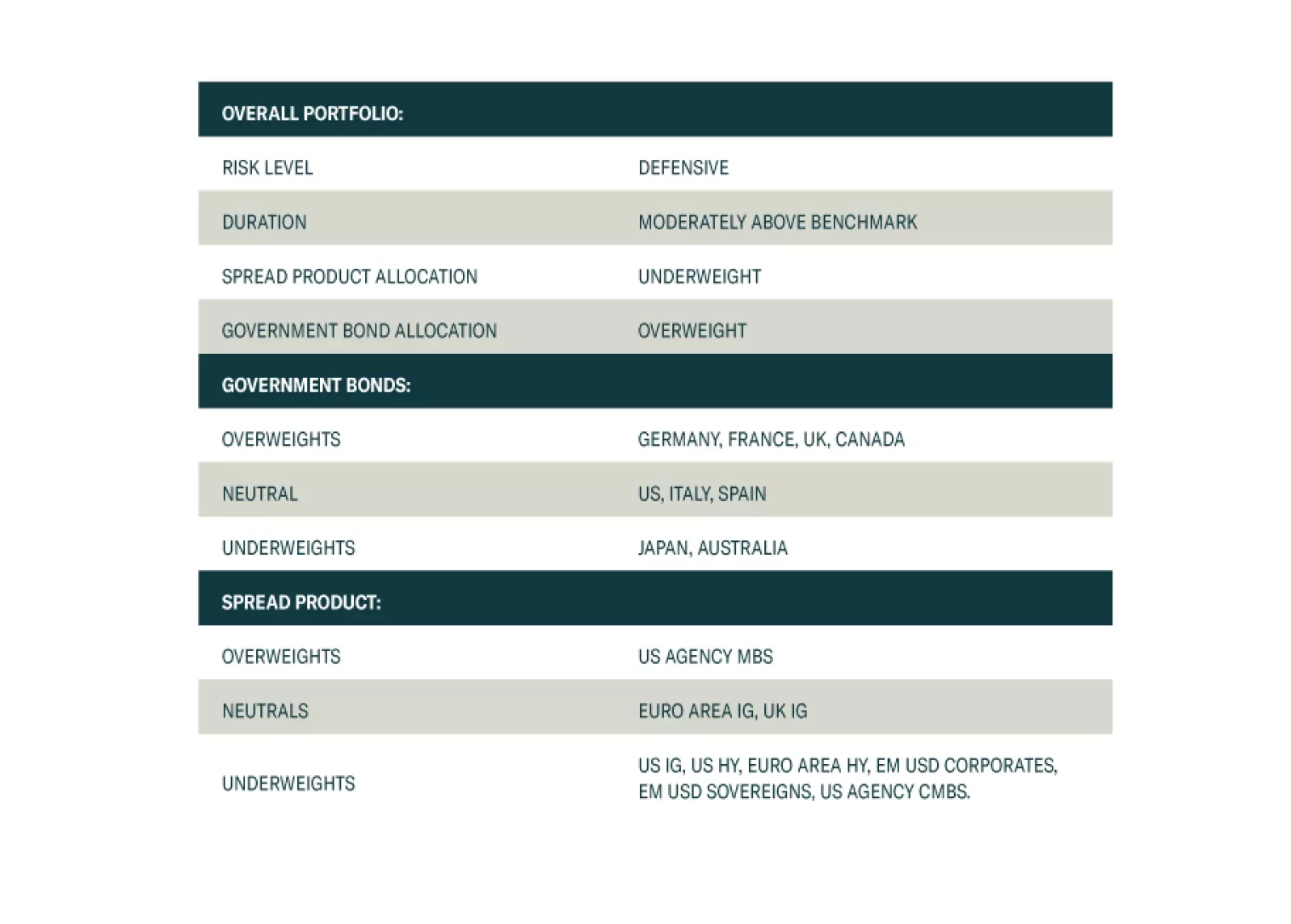

Our Portfolio Allocation Summary for January 2024.

In this, our final report of the year, we present our main global fixed income investment themes and recommendations for 2024.

Our US fixed income team’s key investment views for 2024.

Our Portfolio Allocation Summary for December 2023.