War/Conflict

After 250 years, the USA is still the biggest thing happening in the world. But it faces huge challenges in the coming decades from socioeconomic imbalances and strategic competition.

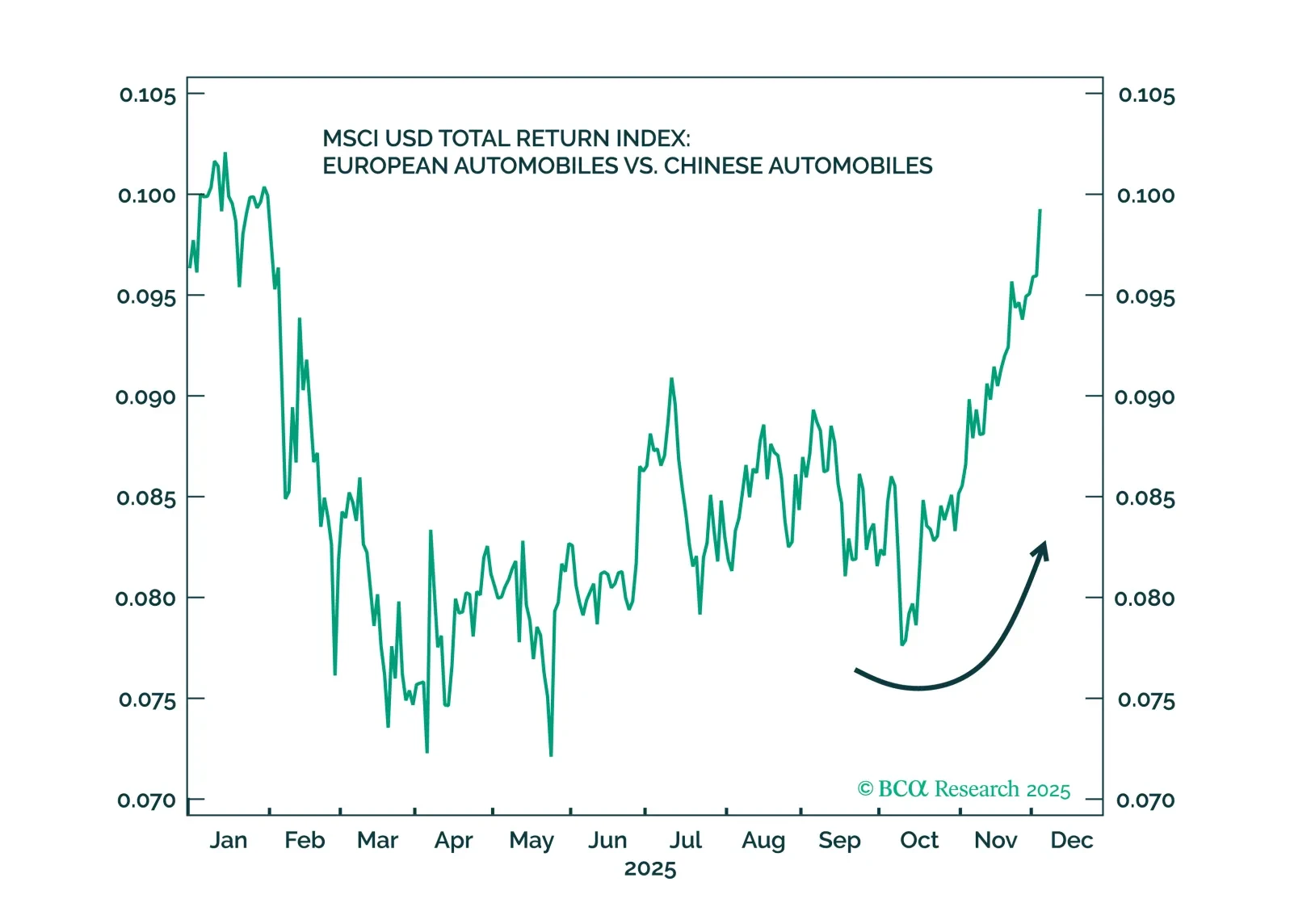

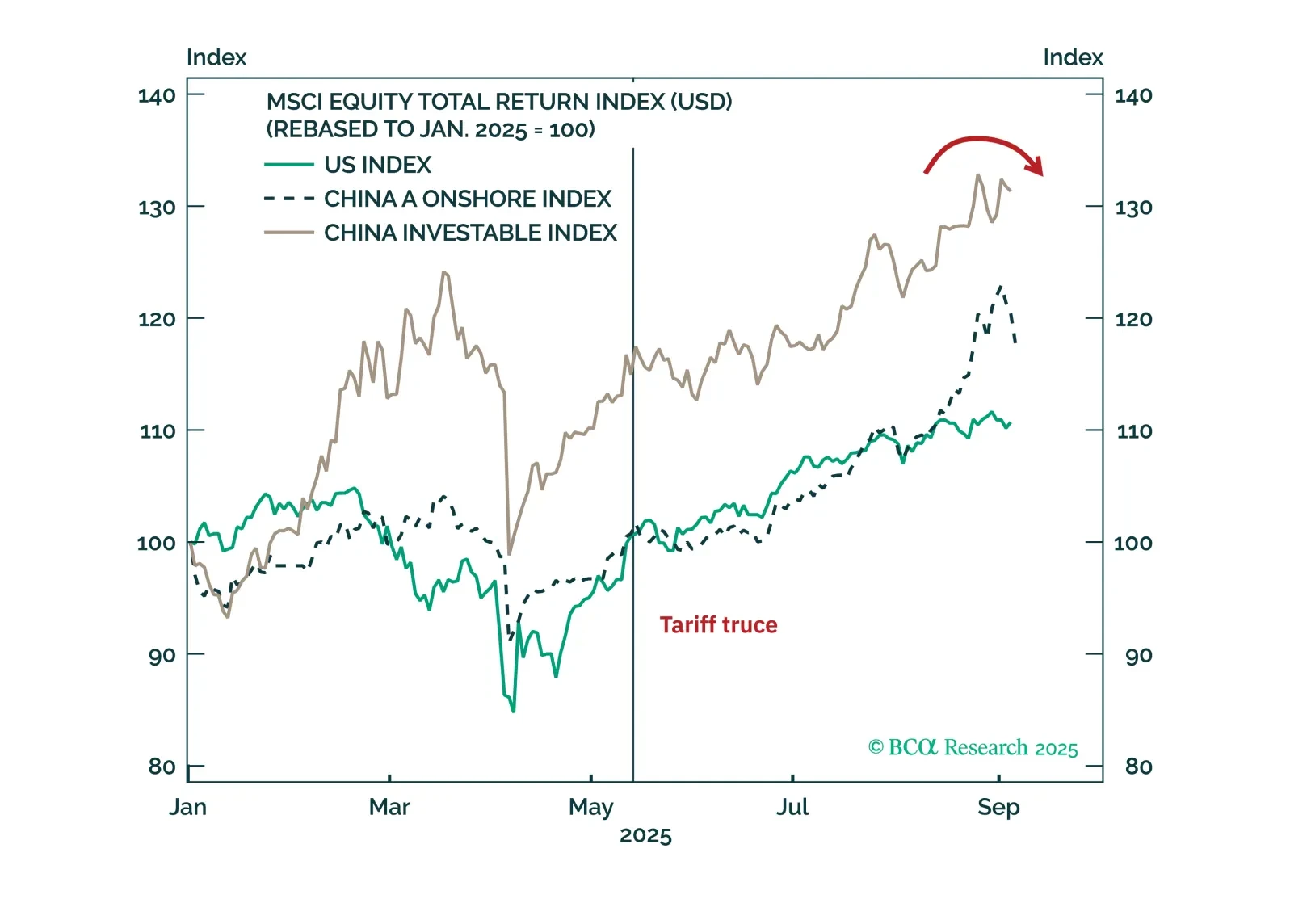

We got Trump's tariff shock and backtracking correct and predicted Israel's attack on Iran. But we missed the China rally — and there is still no Ukraine ceasefire.

US intervention will likely force out Maduro from Venezuela and reopen the economy. This could increase Venezuelan crude production in the long run, a modestly bearish outcome for oil markets over cyclical and structural horizons.

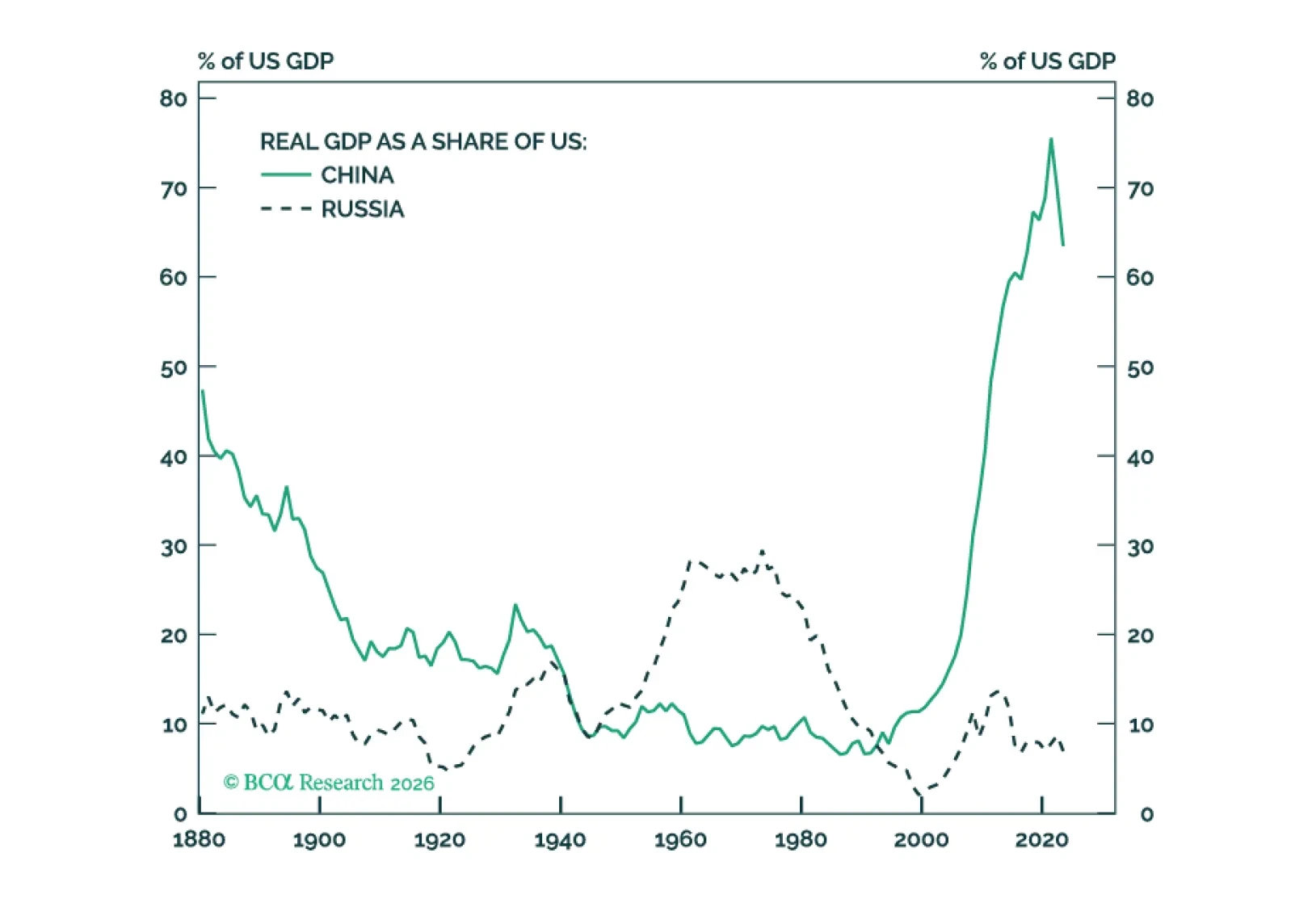

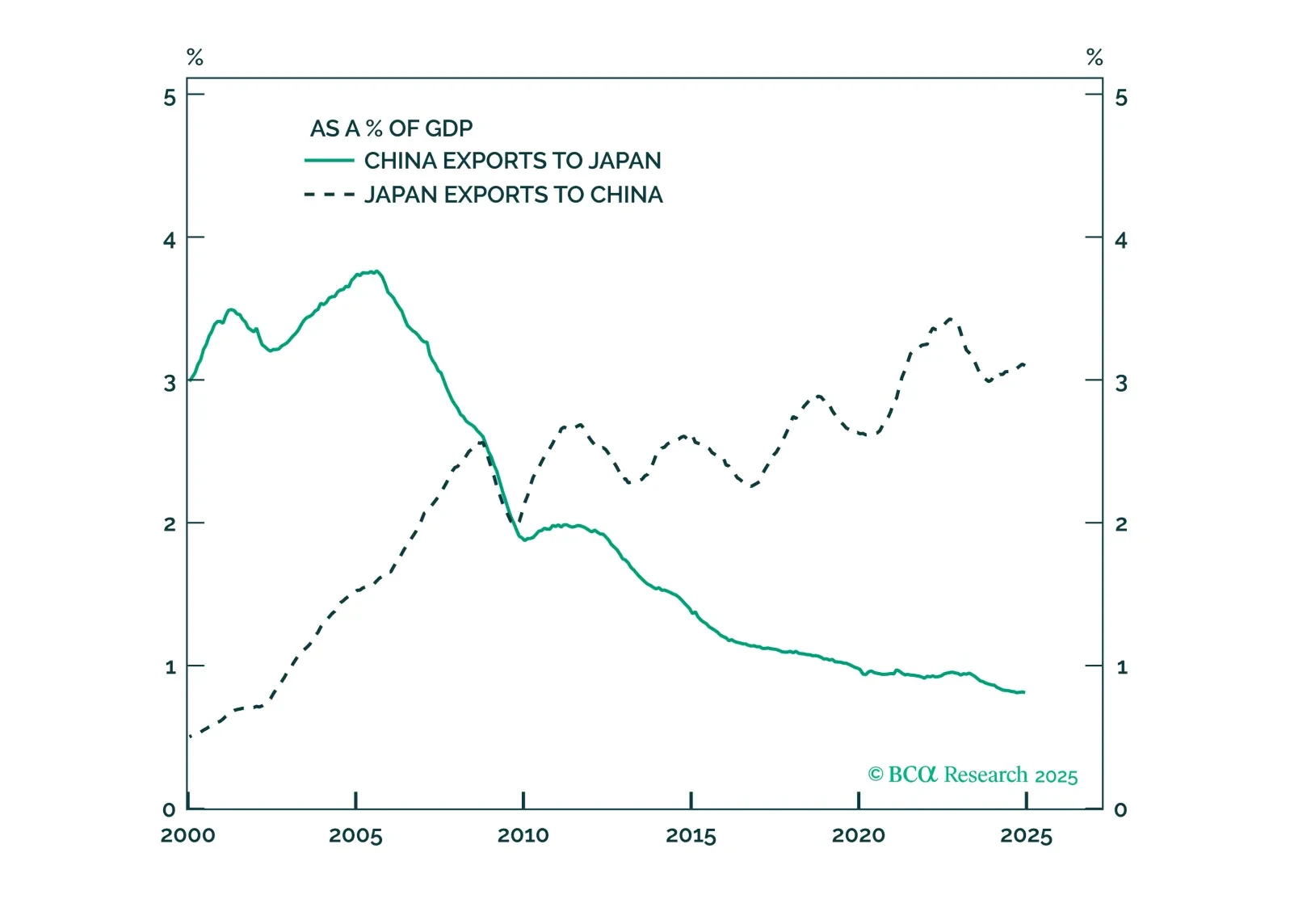

US talks with Russia and China coincide with rising EU-Russia and Japan-China tensions. Stay overweight US assets and long Japanese yen.

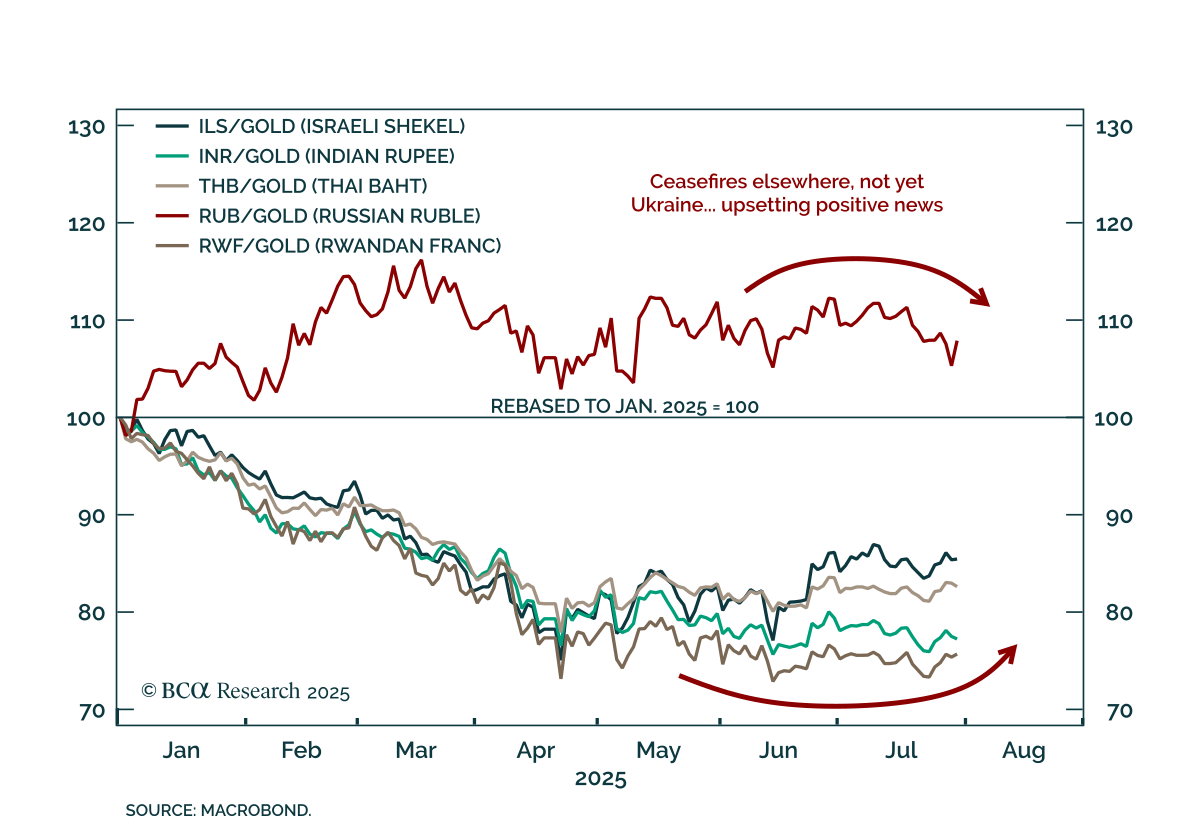

Reduce risk exposure in the very near term as President Trump's ceasefire effort falters, Russia tensions spike, and US-China trade prospects suffer.

Russia’s recalcitrance will probably trigger a near-term global stock market correction by prompting larger sanctions and derailing US-China talks. But Israel’s actions do not raise our odds of a major oil shock.

Investors will be disappointed if they buy into the China rally and then Russia escalates the war in Ukraine.

The media is missing the big picture: the war is already contained. The falling oil price confirms that. We fully expect cold feet and volatility incidents in the very near term but there is only a 5% chance of Russia triggering a larger war with NATO – and that is what really matters.