Valuations

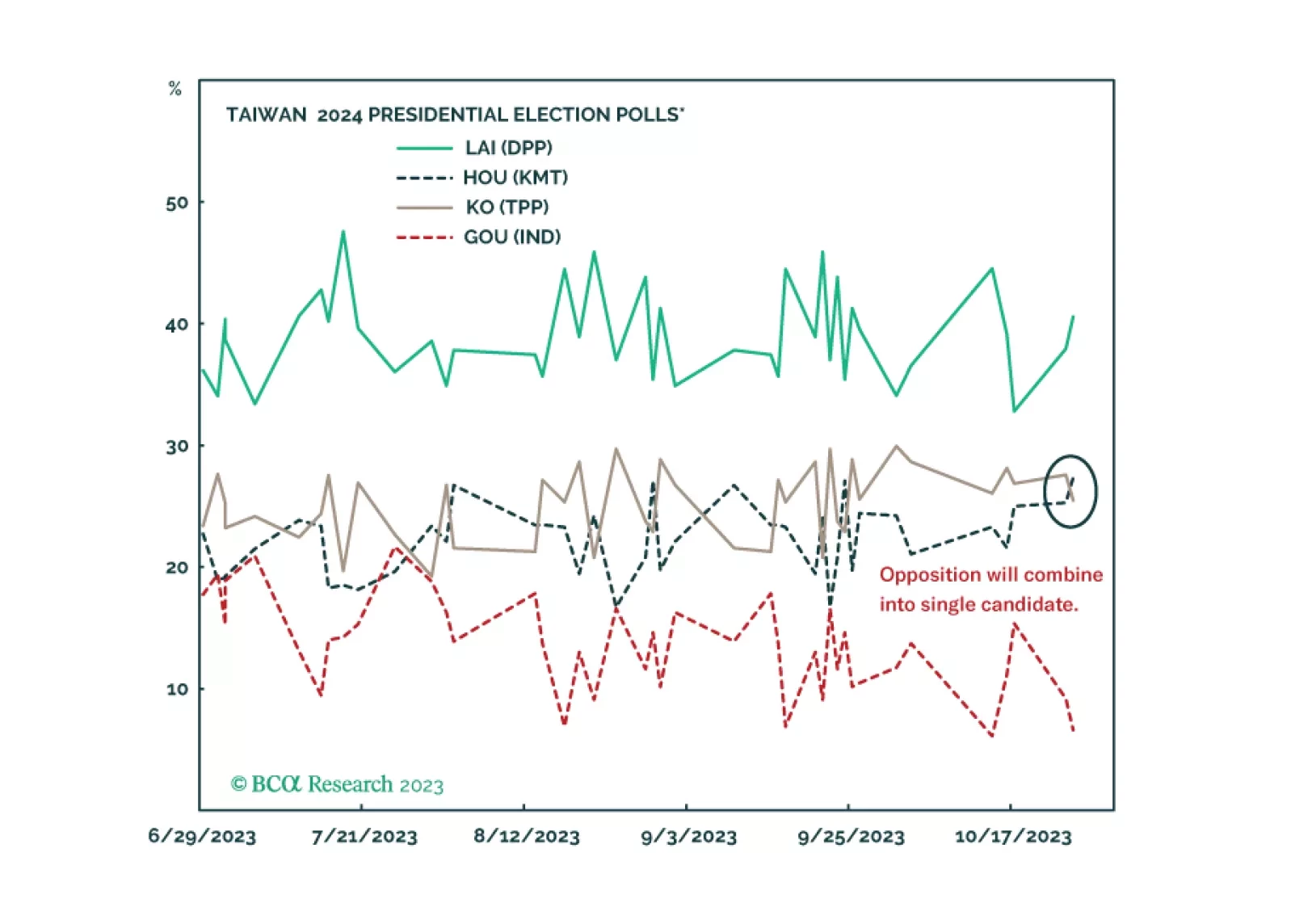

Our political forecasting scored wins in 2023 but we failed to capitalize on it adequately in our trade recommendations.

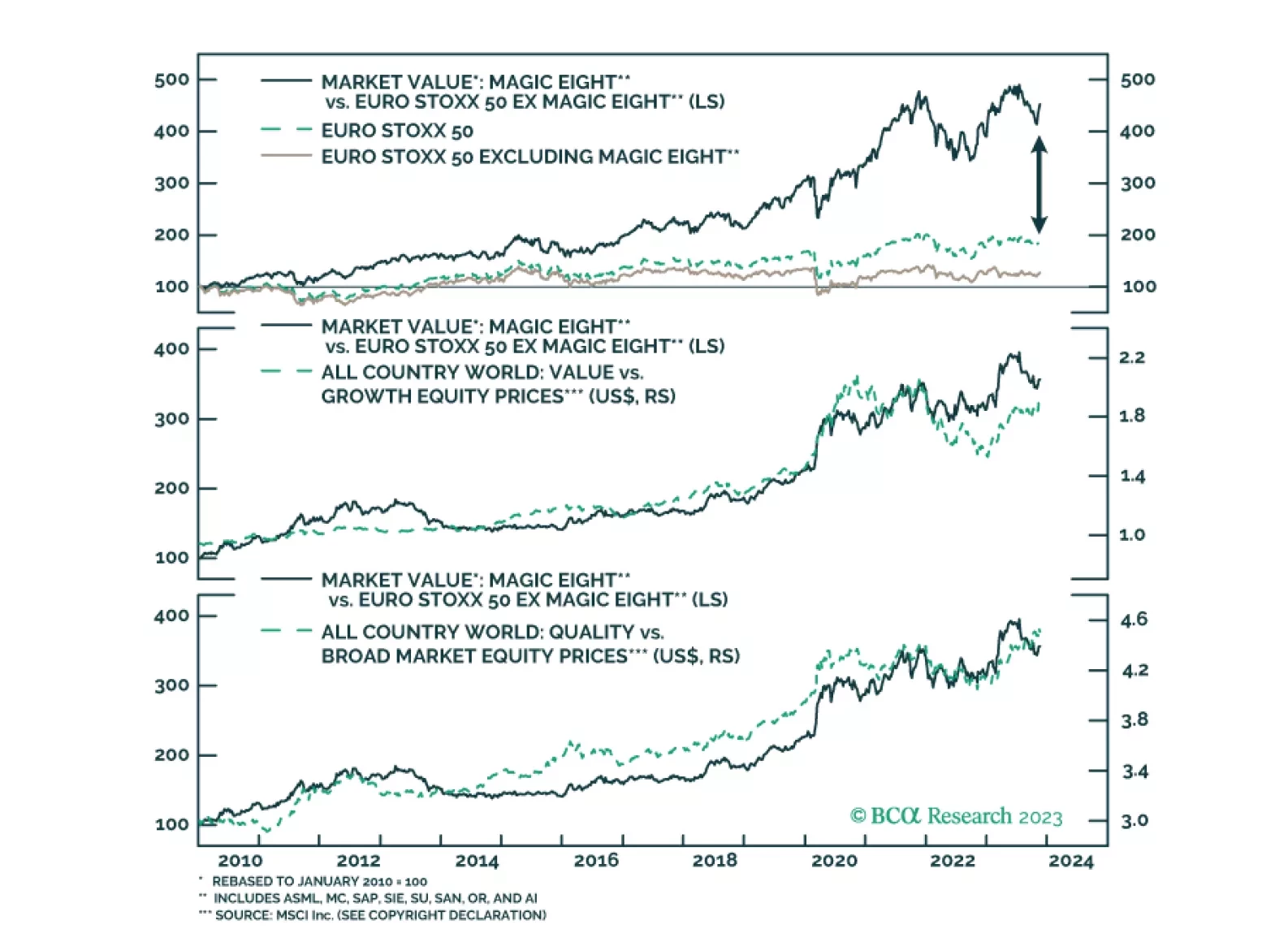

The US has the Magnificent Seven, Europe has the Magic Eight. What drives the performance of those eight stocks crucial to the European market?

Investors should not get their hopes up about the Biden-Xi summit. Wait to see if a new ruling party is elected in Taiwan before downgrading geopolitical risk in the Taiwan Strait. US-China strategic détente is possible but neither the geopolitics nor the macro backdrop warrant a risk-on position next year.

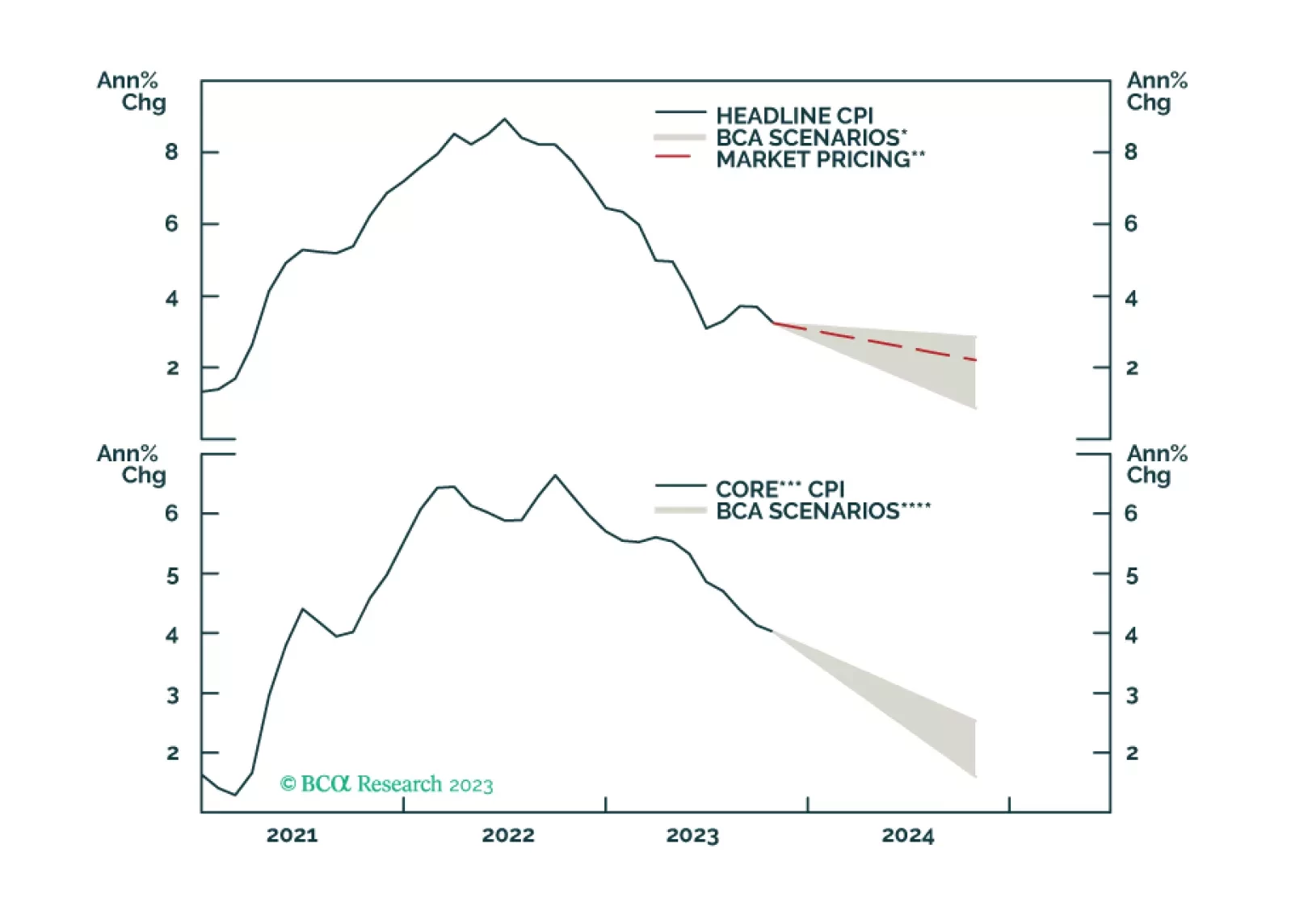

This week’s Special report revisits our TIPS Golden Rule. We provide a 12-month inflation forecast and discuss how it impacts our TIPS view.

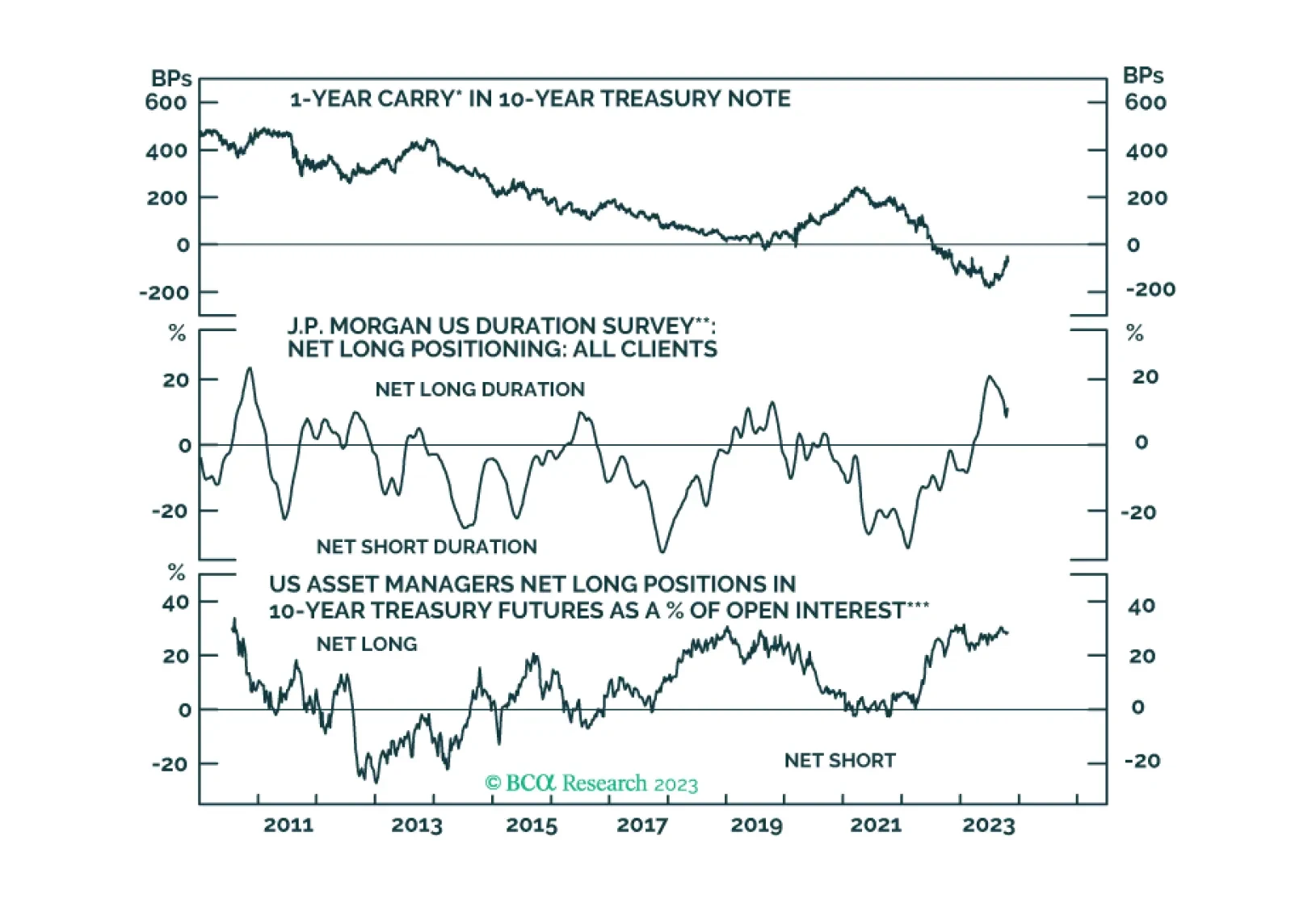

This week’s report contains an update on the Treasury curve’s recent bear-steepening trend and a look at different measures of long-maturity Treasury valuation.

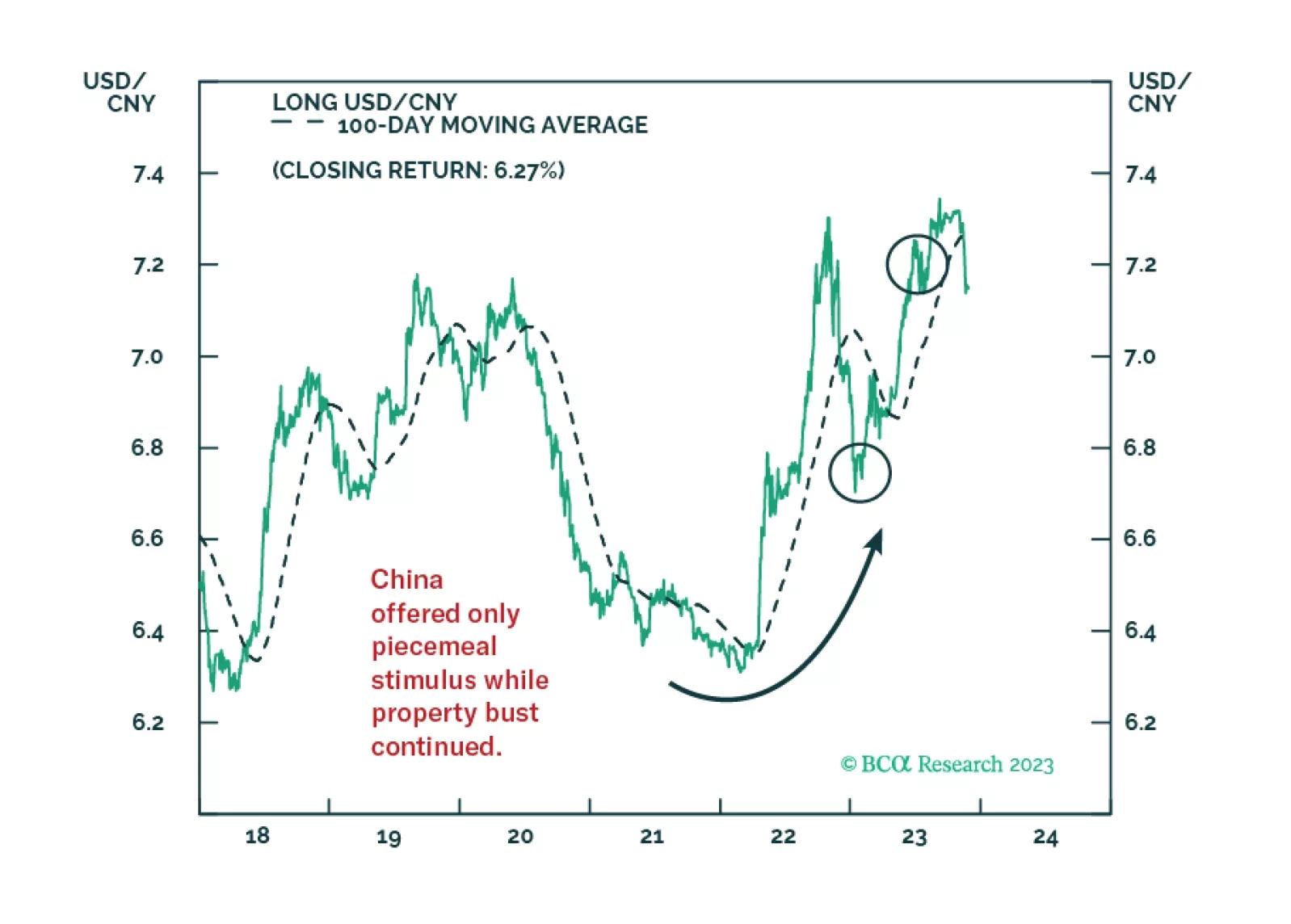

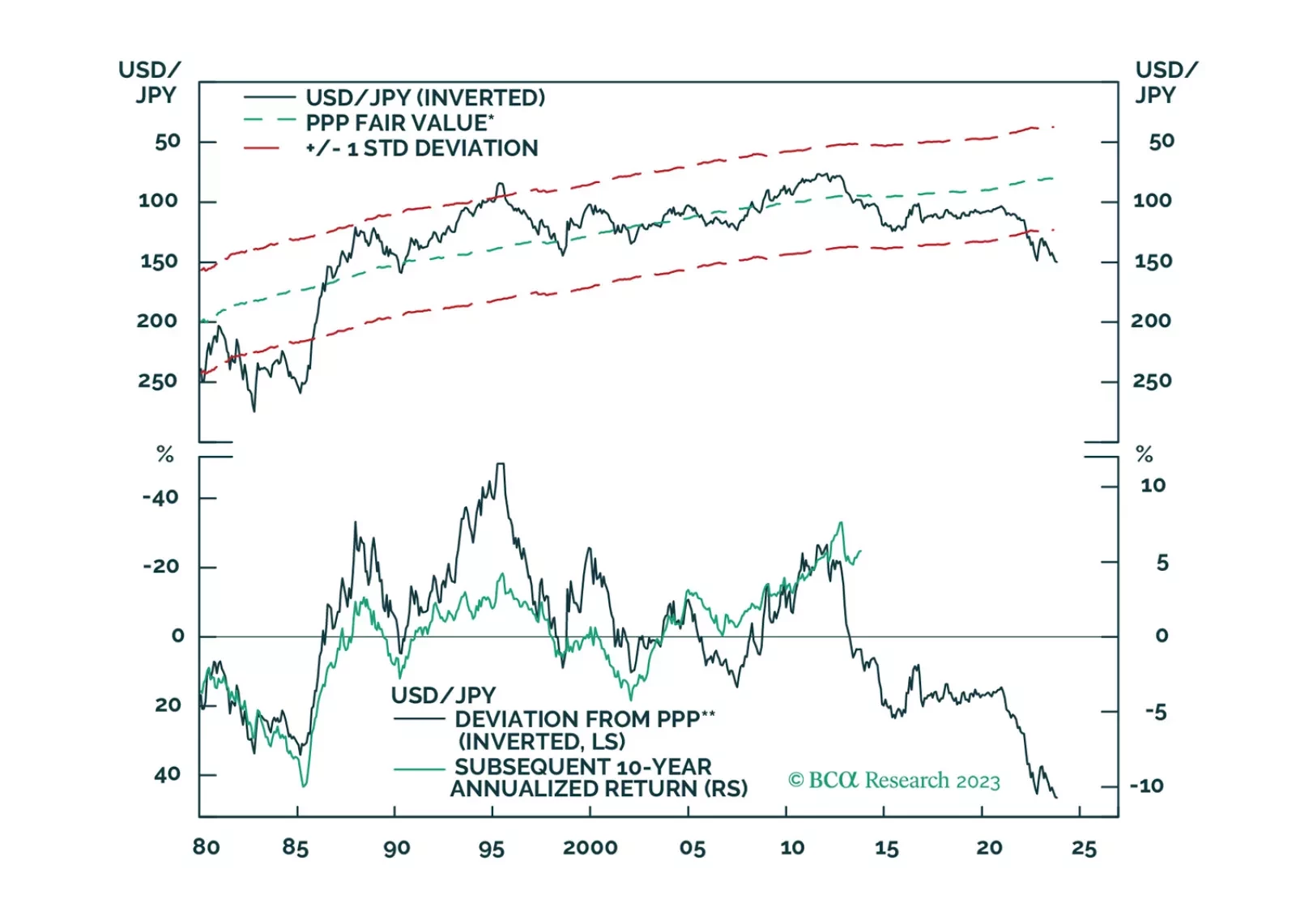

There is a high probability that the global economy will tip into recession in the second half of 2024. A long yen position is an excellent hedge against that risk.

The recent bear-steepening of the US Treasury curve has been driven by the combination of stronger-than-expected economic growth and stable Fed rate expectations. Historically, such periods do not last very long, and we see the current bear-steepening episode ending soon. We also highlight an opportunity in Agency MBS.