Valuations

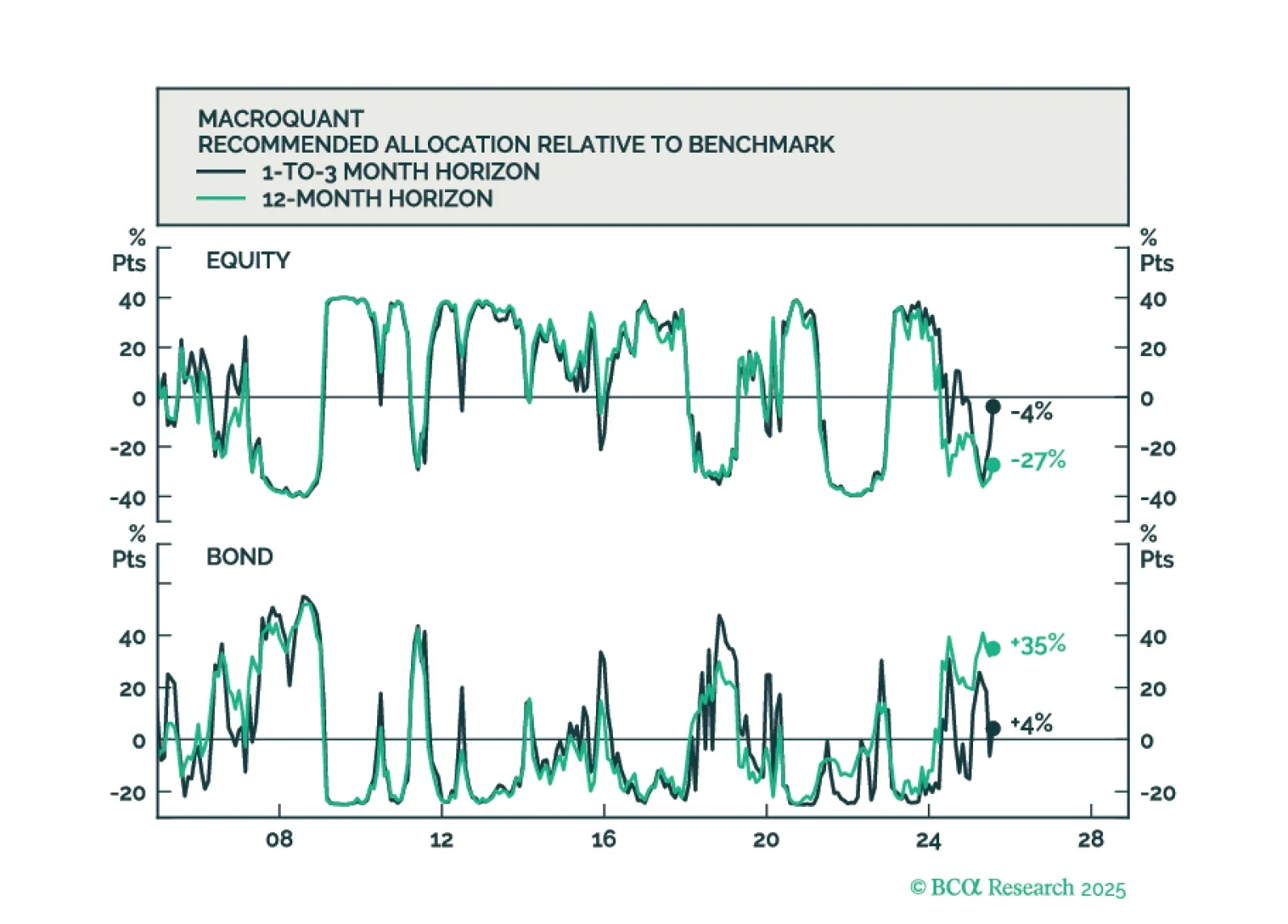

MacroQuant is tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold and copper.

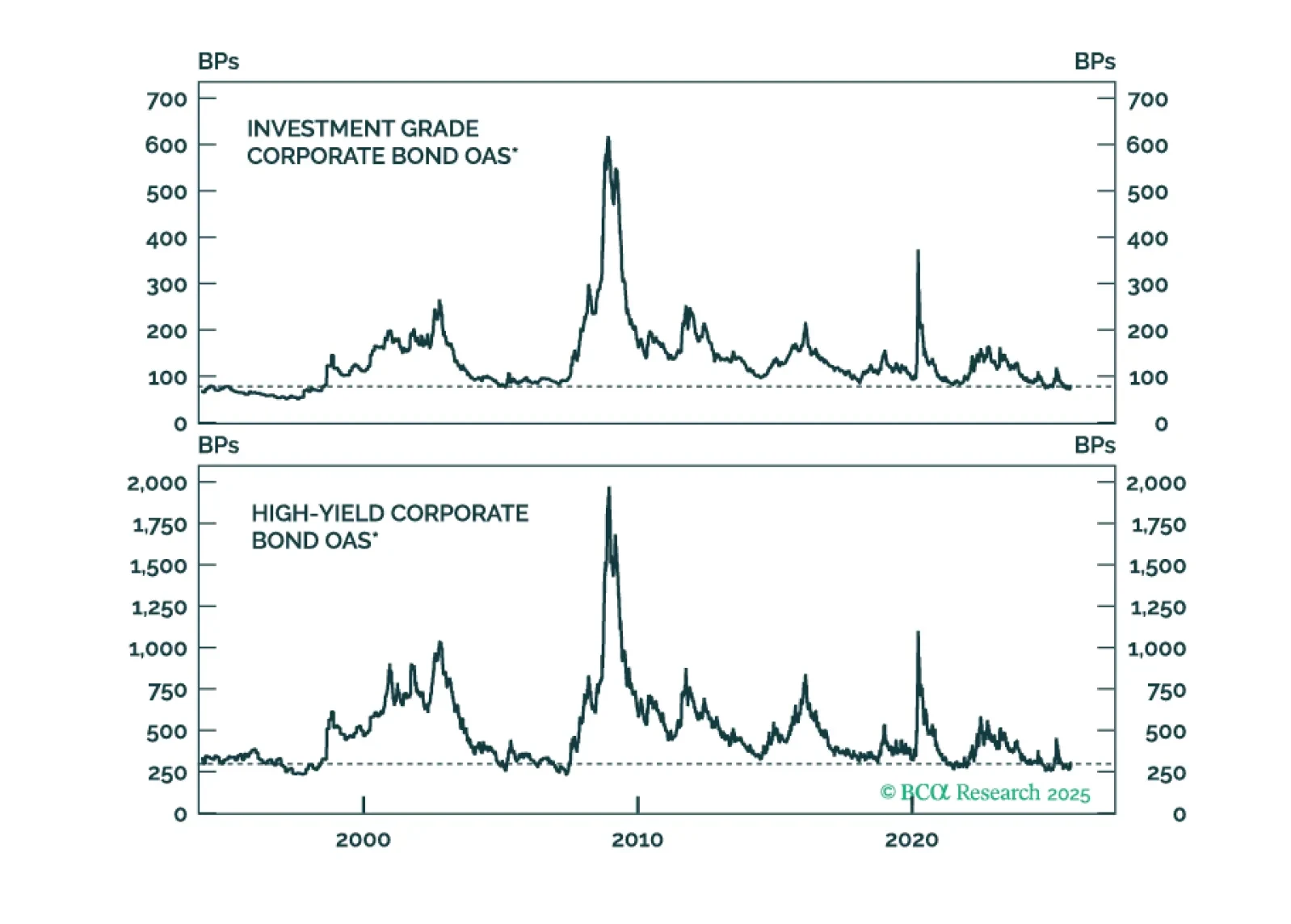

This week’s Special Report evaluates the reward and risk in corporate bonds. We address the question of whether low expected excess returns today are justified by low risk or an example of overvaluation.

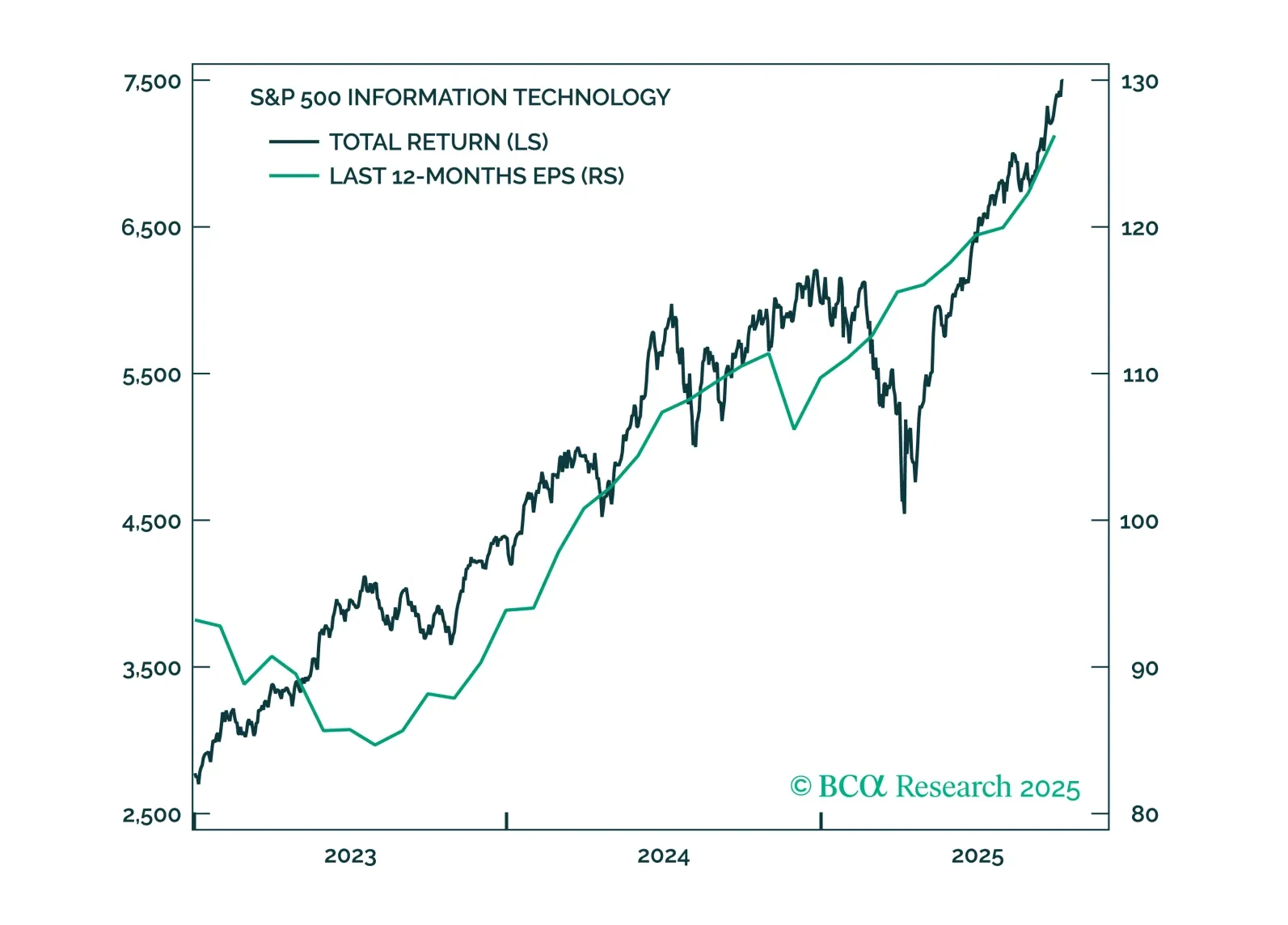

Broad GenAI adoption and monetization, alongside falling inference costs, should make hyperscalers’ and enterprise investments worthwhile. While the GenAI boom echoes the dot-com era, it differs in key ways: Valuations are elevated but not extreme, and the rally is still underpinned by solid earnings growth. With few warning signs flashing red, the bull market likely has further to run, though a period of consolidation is overdue.

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.

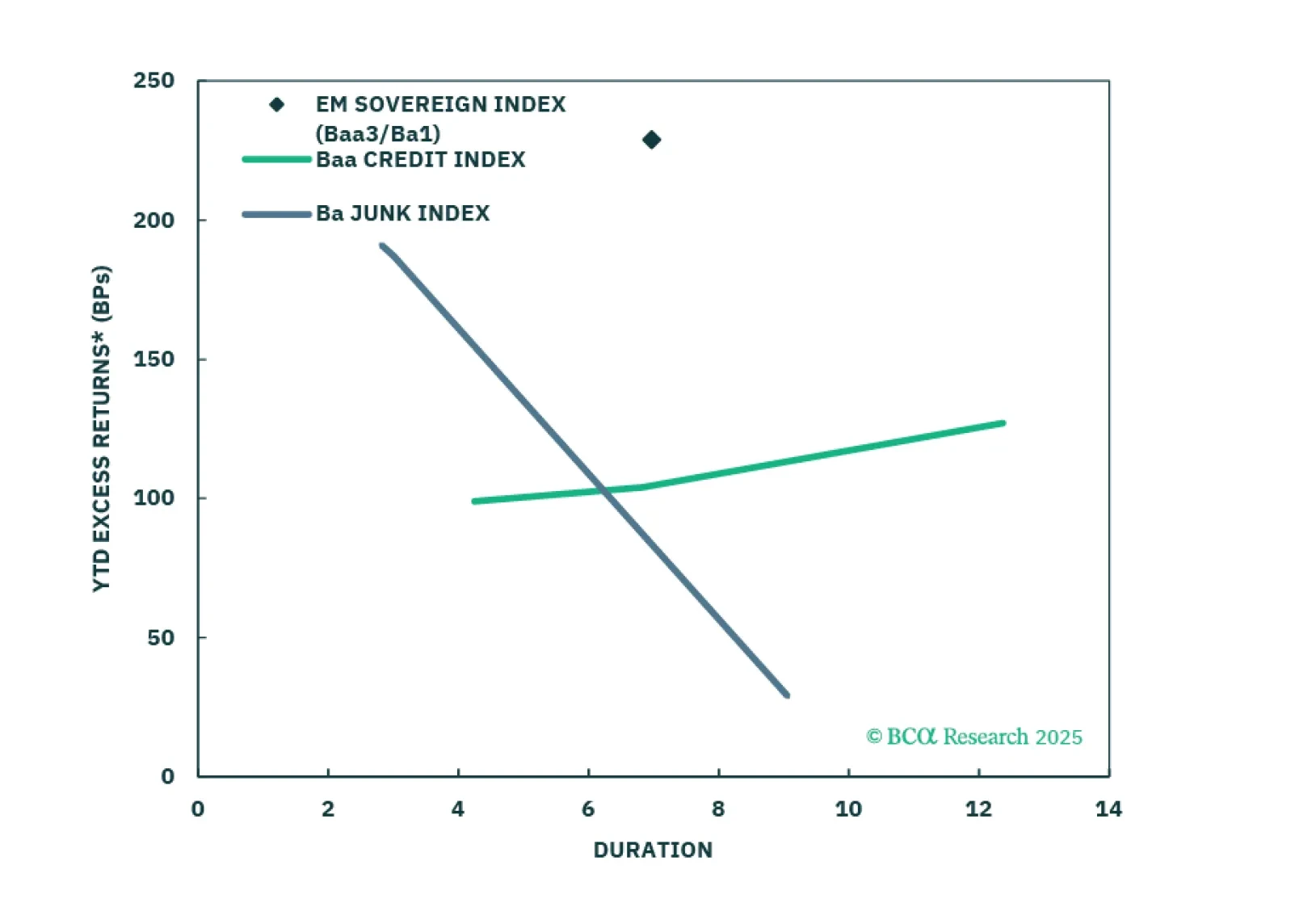

USD-denominated Emerging Market bonds have been outperforming US corporates for the past year. We don’t think the rally is exhausted yet.

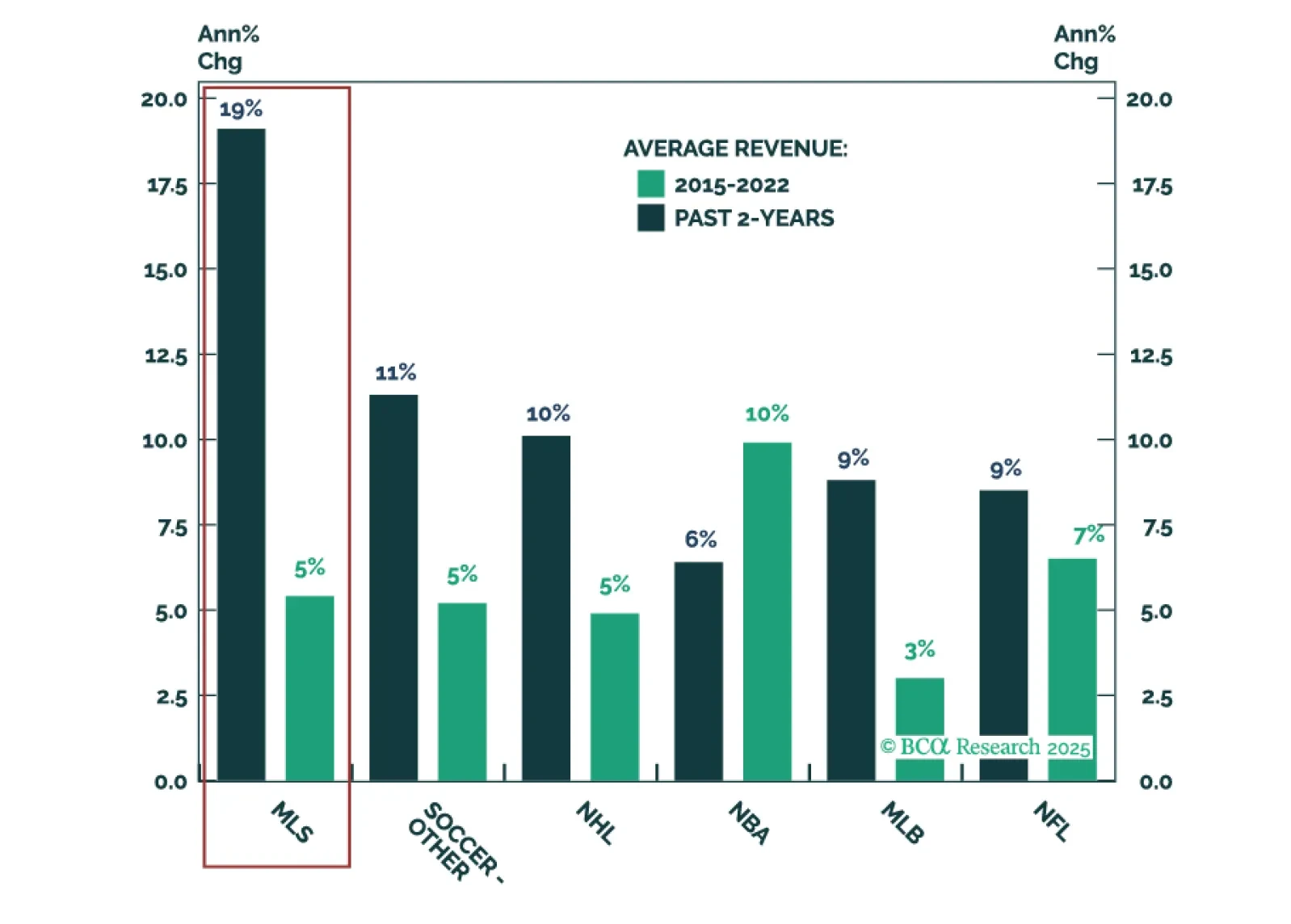

The NFL and NBA grab the headlines, but growth beats size. This report reveals the story behind Major League Soccer (MLS) growth. Valuations have jumped, yet plenty of upside remains—making the MLS relatively attractive compared to other US major leagues.

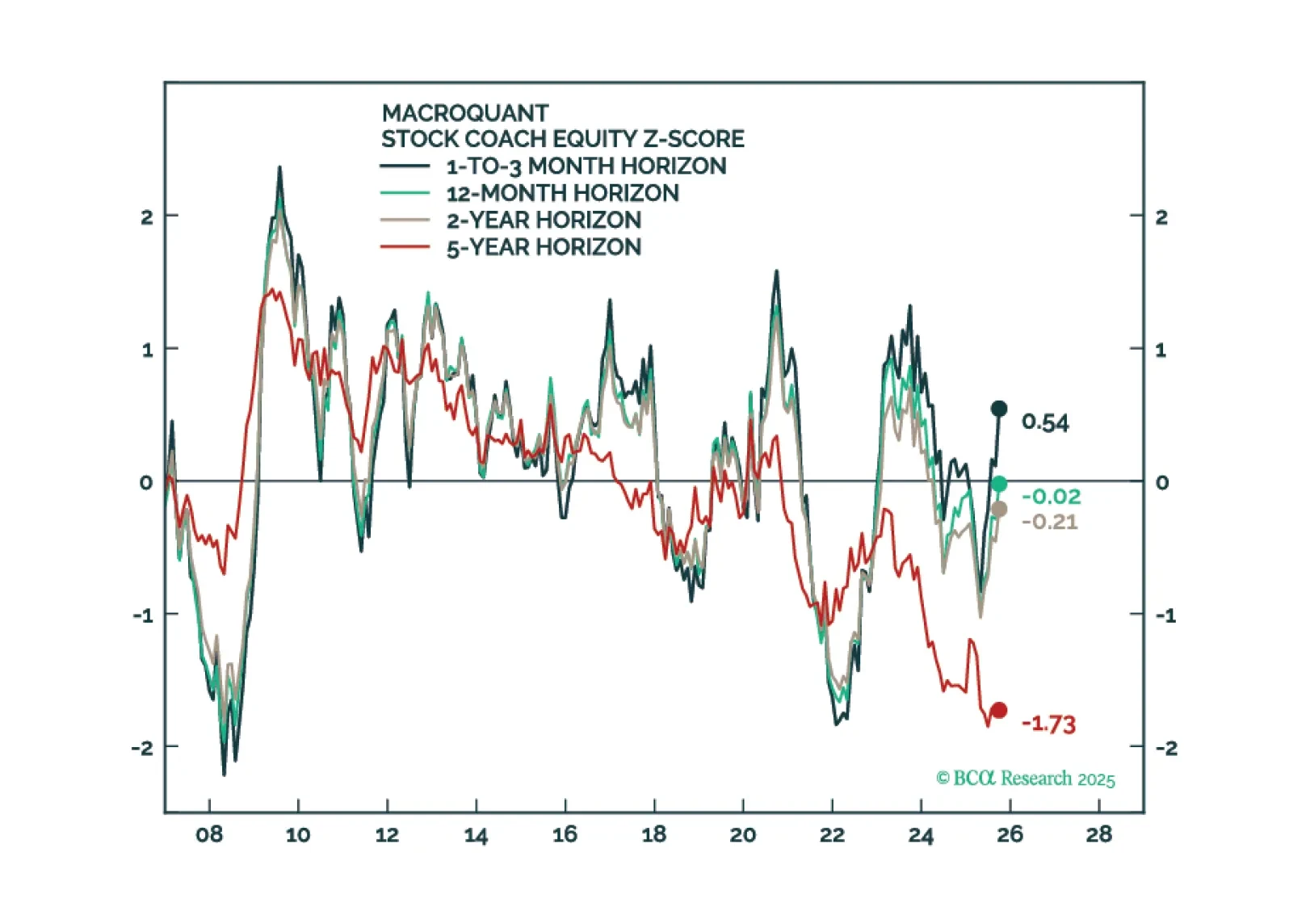

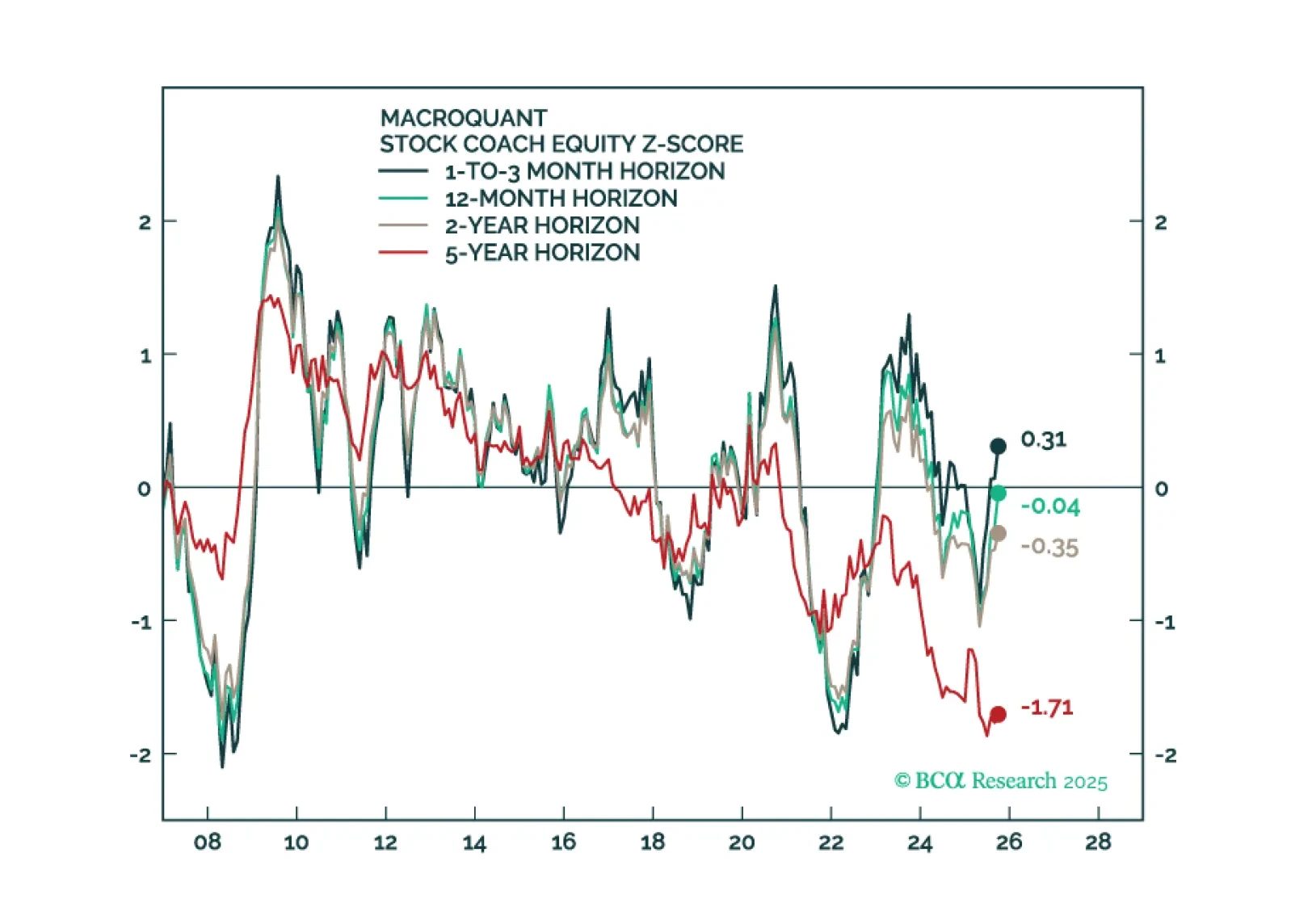

MacroQuant sees downside risks to stocks over a long-term horizon but is not yet saying that we are at imminent risk of an equity bear market.

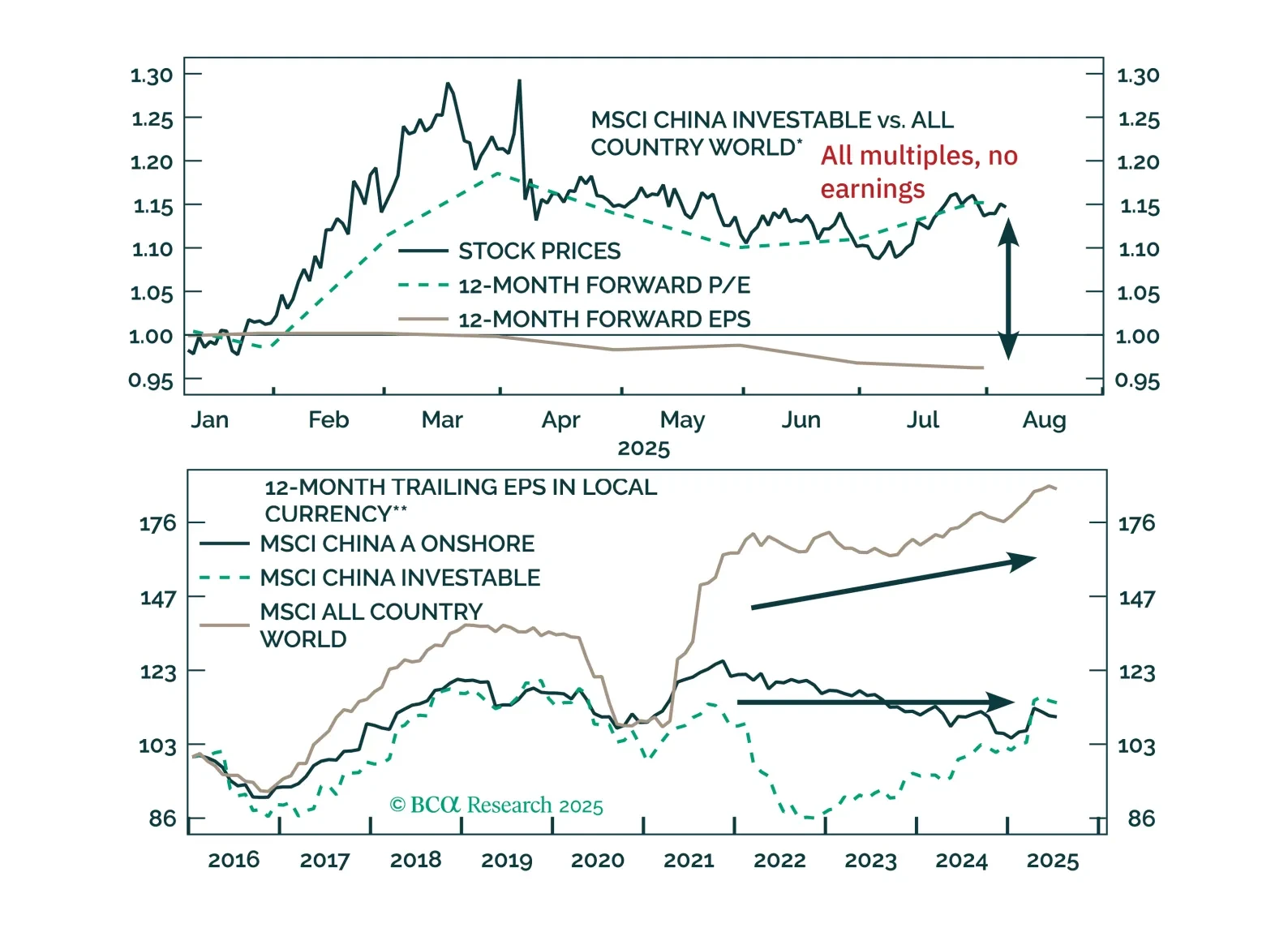

Chinese stock prices have significantly decoupled from the country’s business cycle, with the full impact of US tariffs yet to be realized. The valuation-driven equity gains without a cyclical economic recovery will be vulnerable to a reversal.

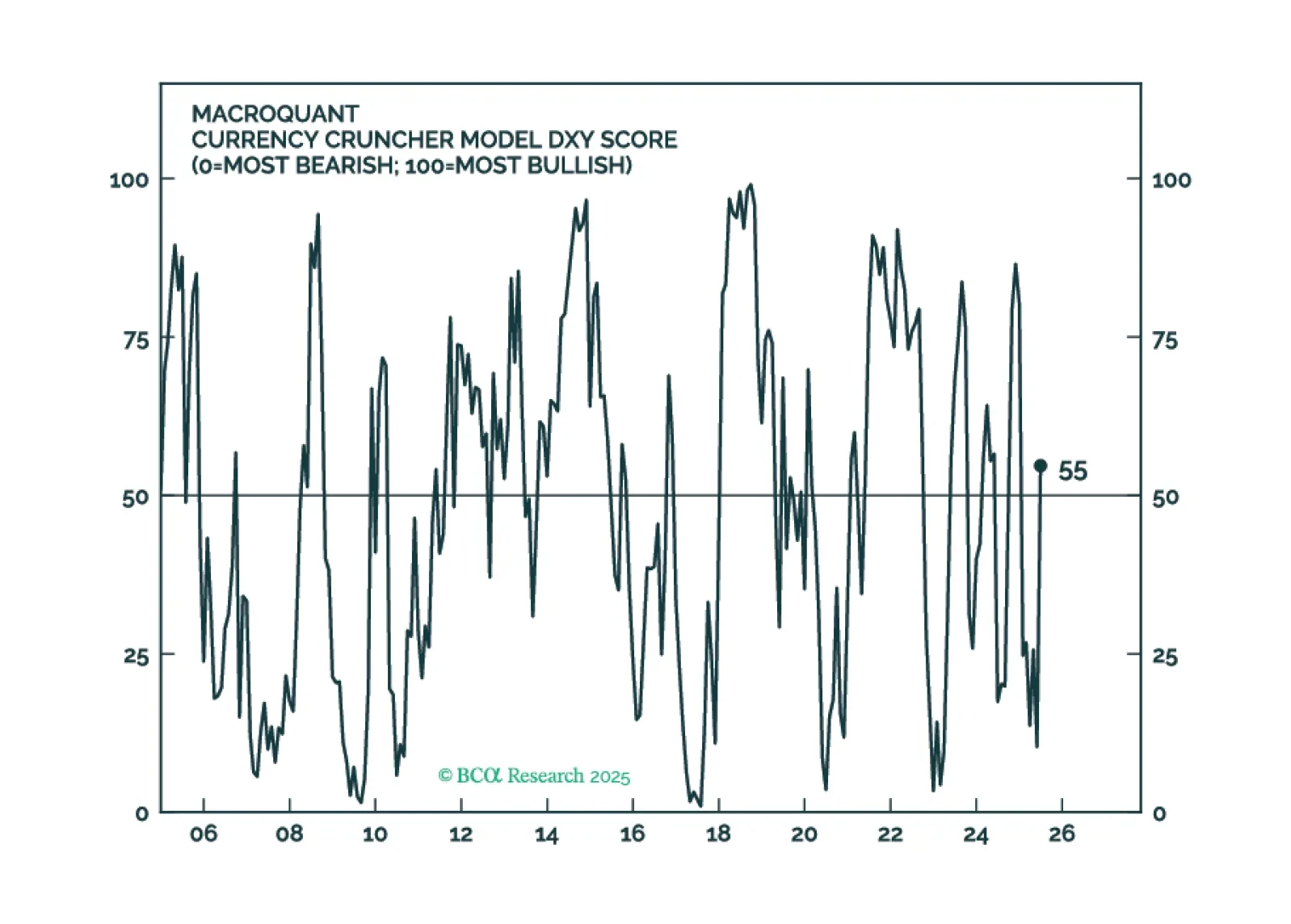

MacroQuant is recommending that equity investors keep their finger near the eject button but avoid pressing it for now. The model is warming up to the dollar again and sees scope for oil prices to rise.

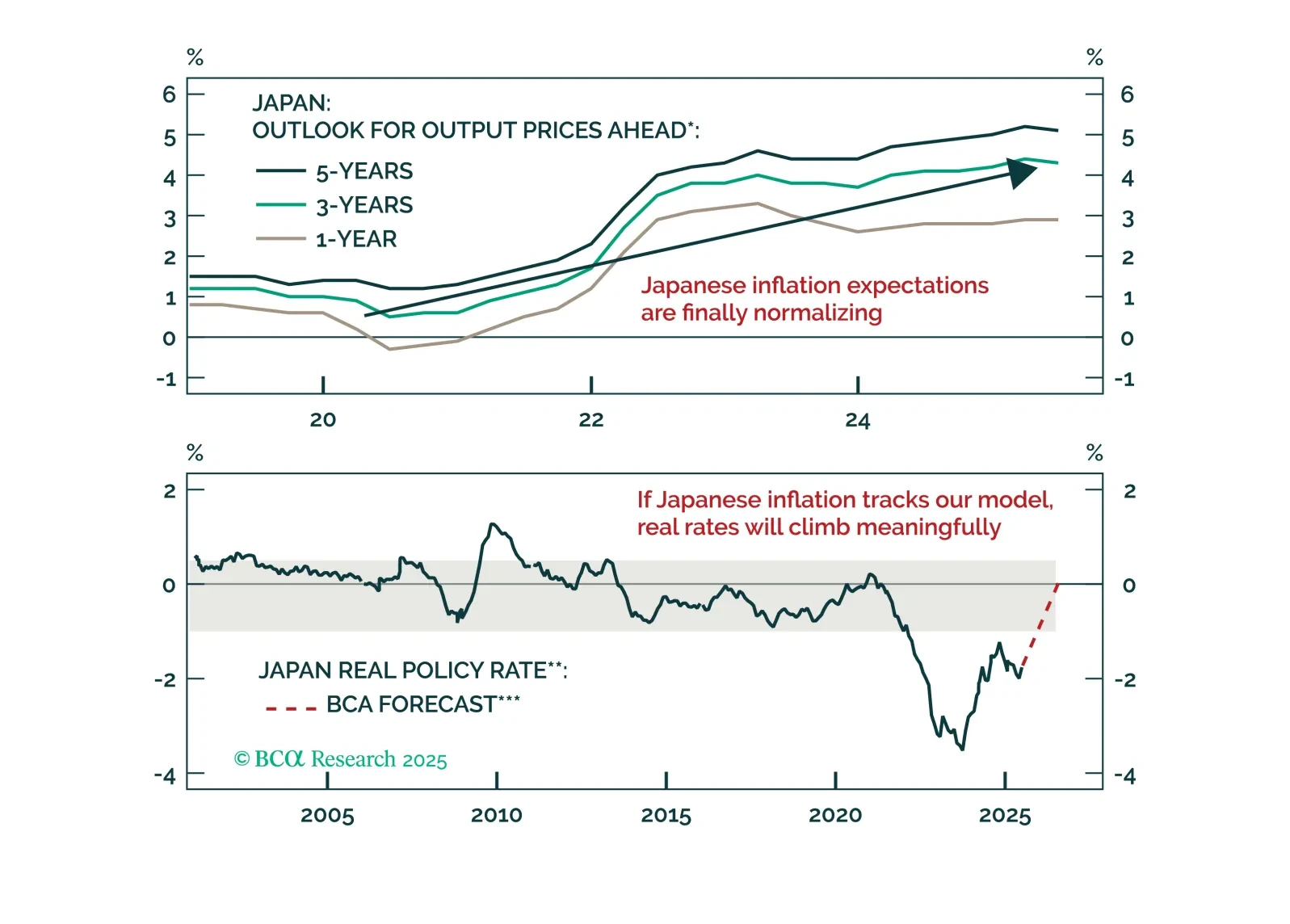

The yen’s discount, surplus, and rising real rates line up for a multi-quarter surge. Find out why EUR/JPY is the first short and when USD/JPY follows.