United States

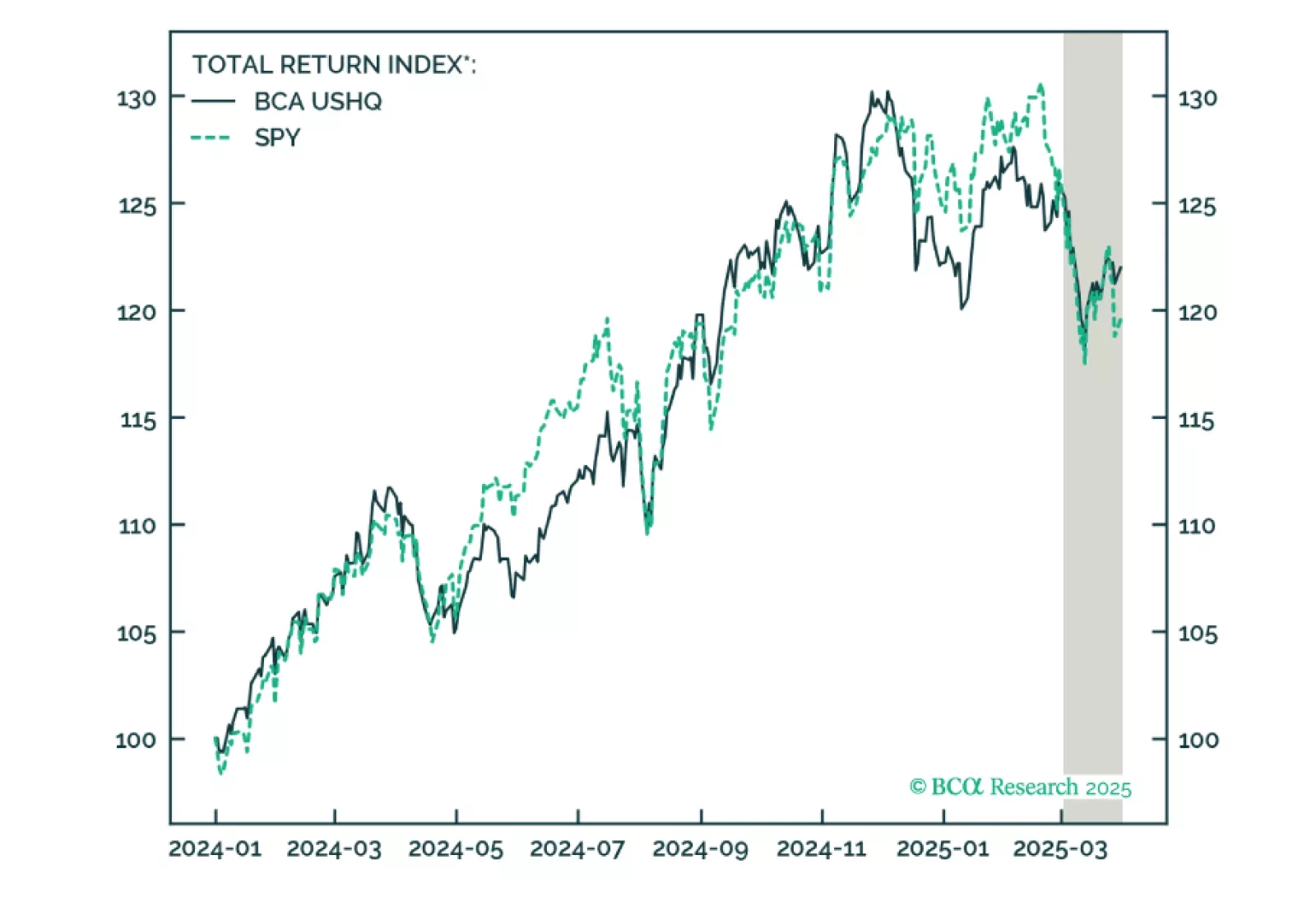

The US High Quality (USHQ) portfolio outperformed its benchmark in March, despite realizing a negative return. USHQ returned -2.6%, whilst its SPY benchmark returned -3.9%. Over a trailing-quarter basis, USHQ posted meaningful outperformance vs. benchmark, generating +230bps of excess return, while also exhibiting lower volatility and a smaller drawdown.

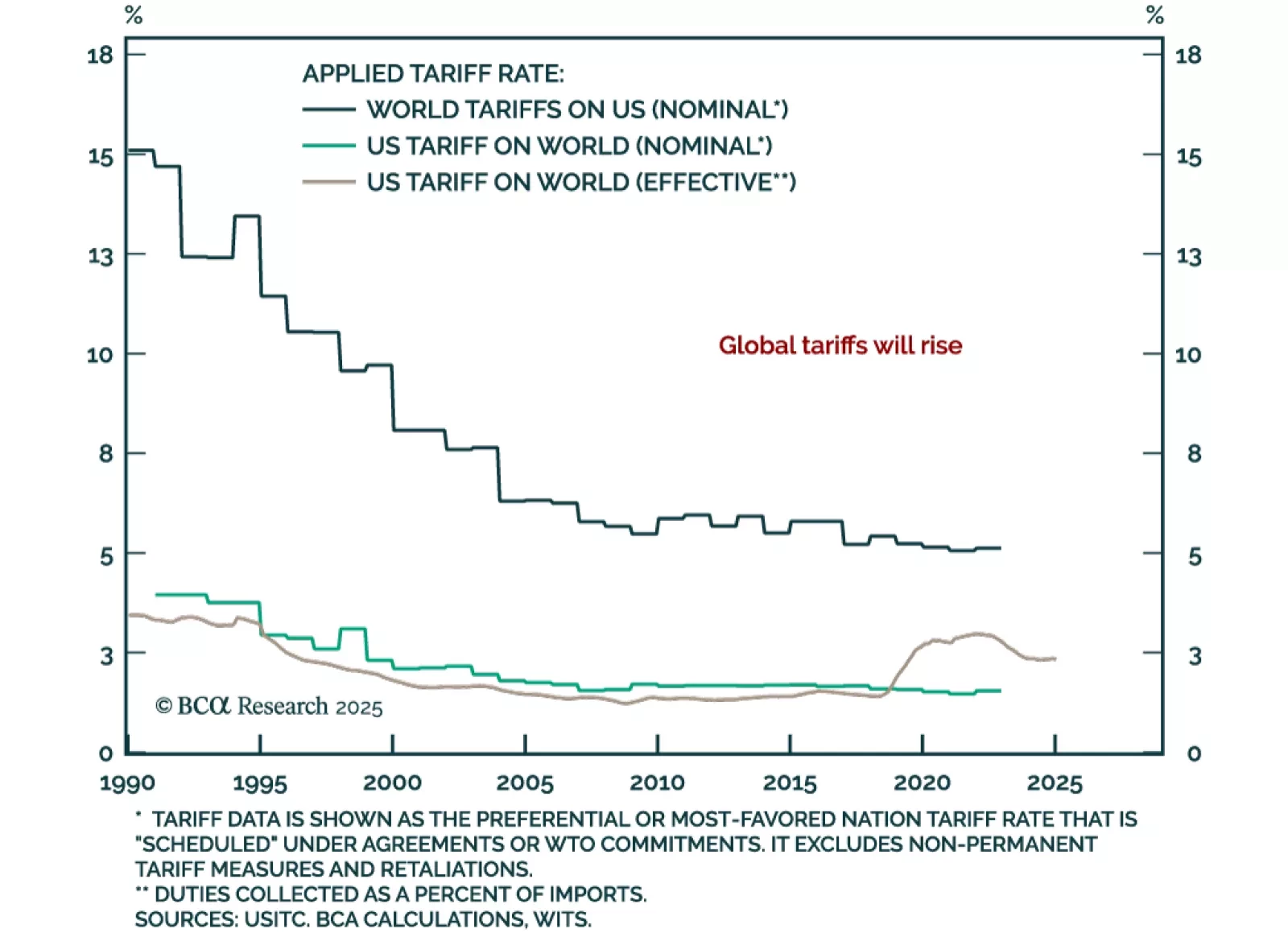

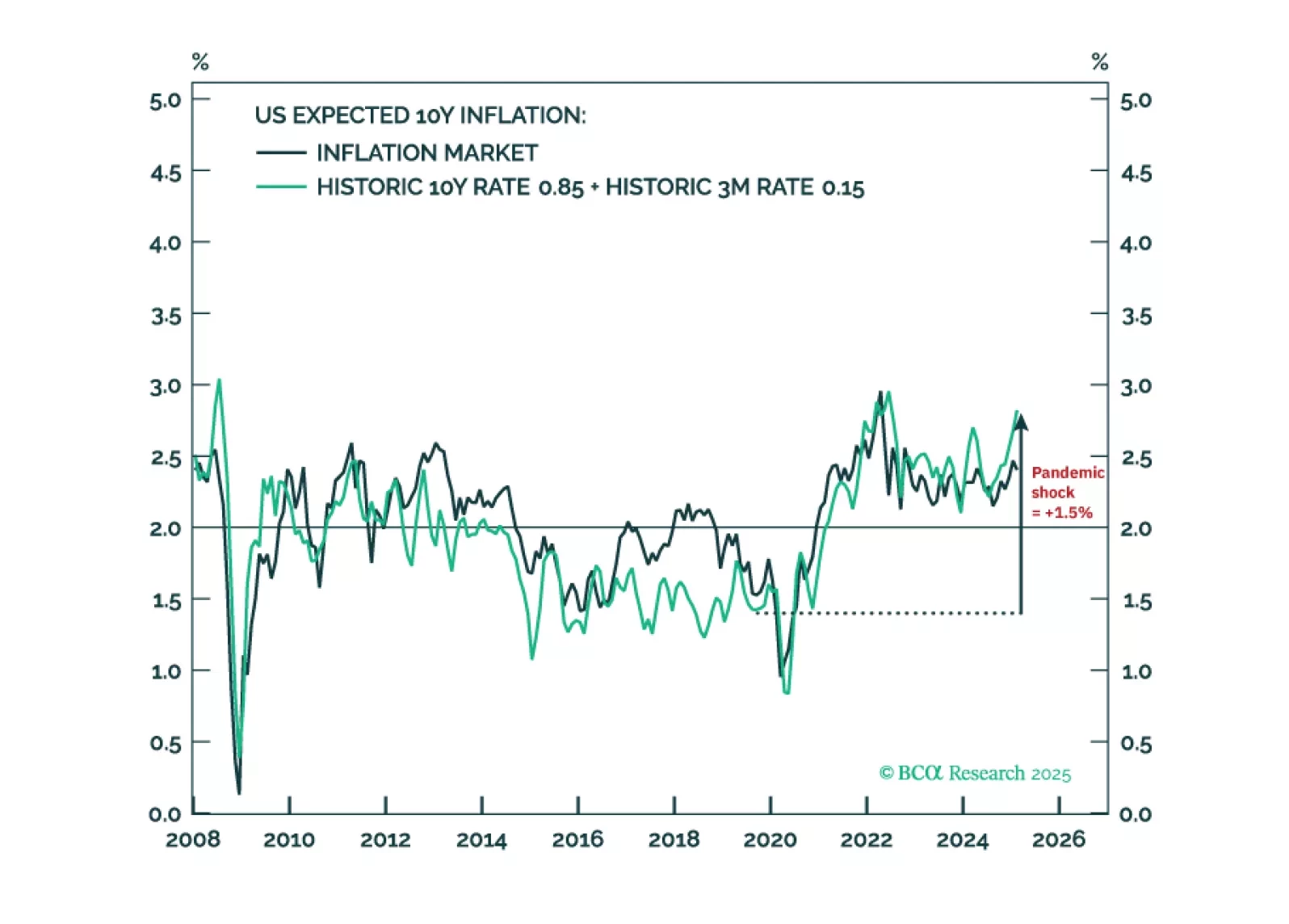

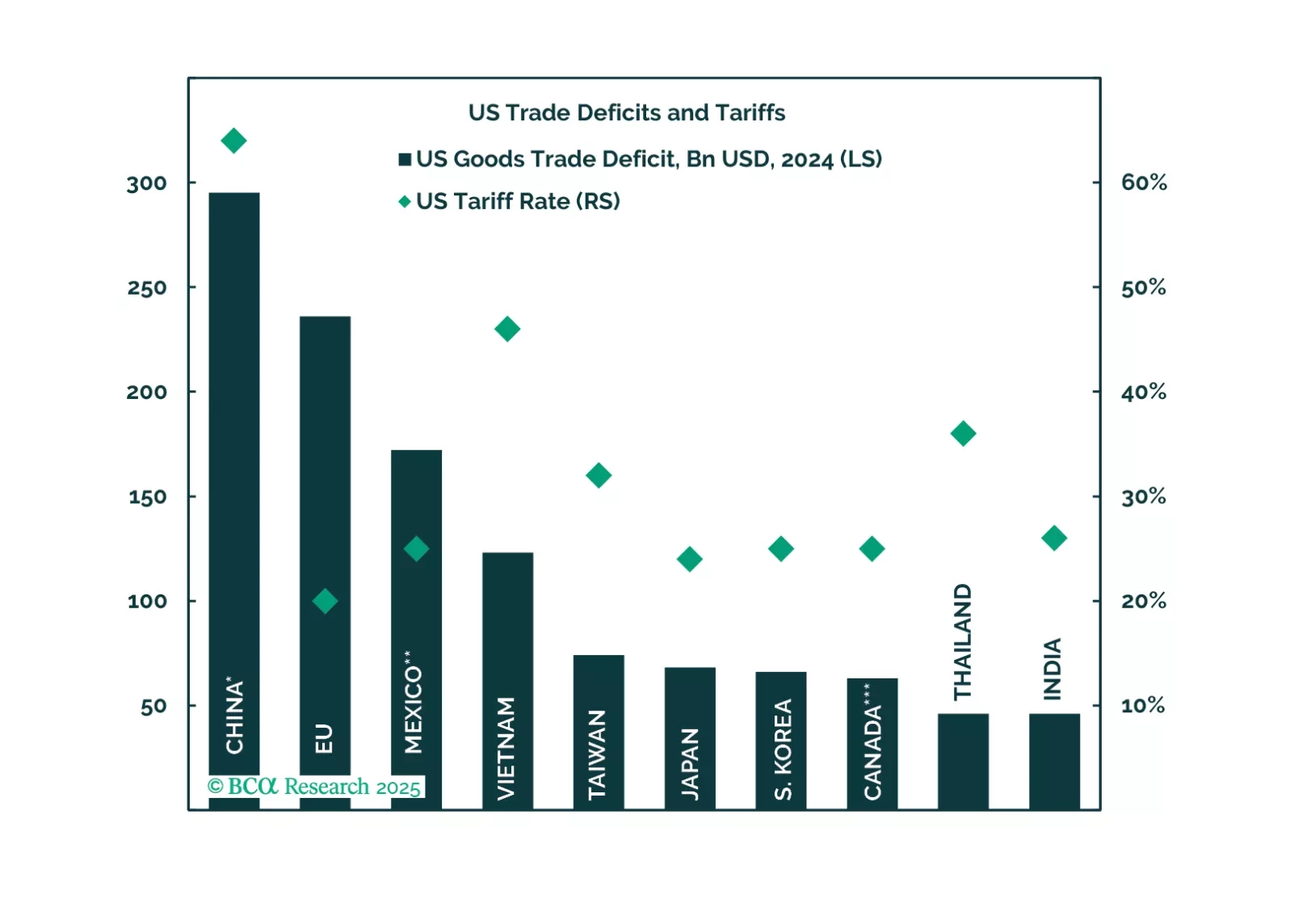

Tariffs will make a difficult job almost impossible. Hitting and sustaining a precise 2 percent inflation target is more about luck than judgement. It requires both the starting point for inflation expectations and any inflation/deflation shock to combine perfectly to 2 percent. While structural inflation expectations in the euro area and Japan could be close to 2 percent, those in the US and the UK will be stuck uncomfortably above 2 percent. We discuss the investment implications for rates and FX. Plus: gold is vulnerable to a tactical reversal.

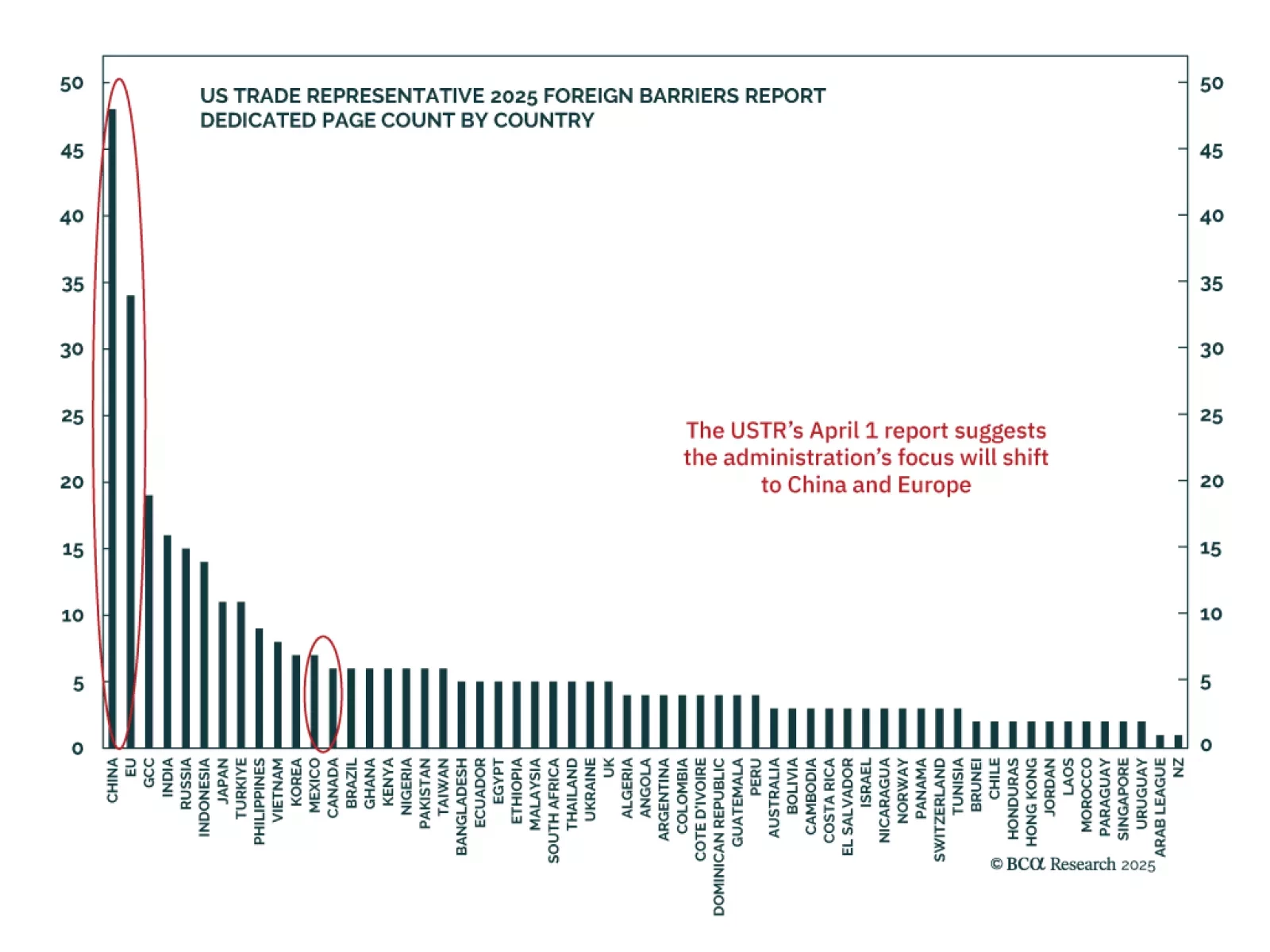

Trump's Tariff D-Day brings a negative surprise to financial markets already anxious over a declining US cyclical economy. Investors should sell risky assets, increase safe havens, and overweight US assets in the near term.