United States

1

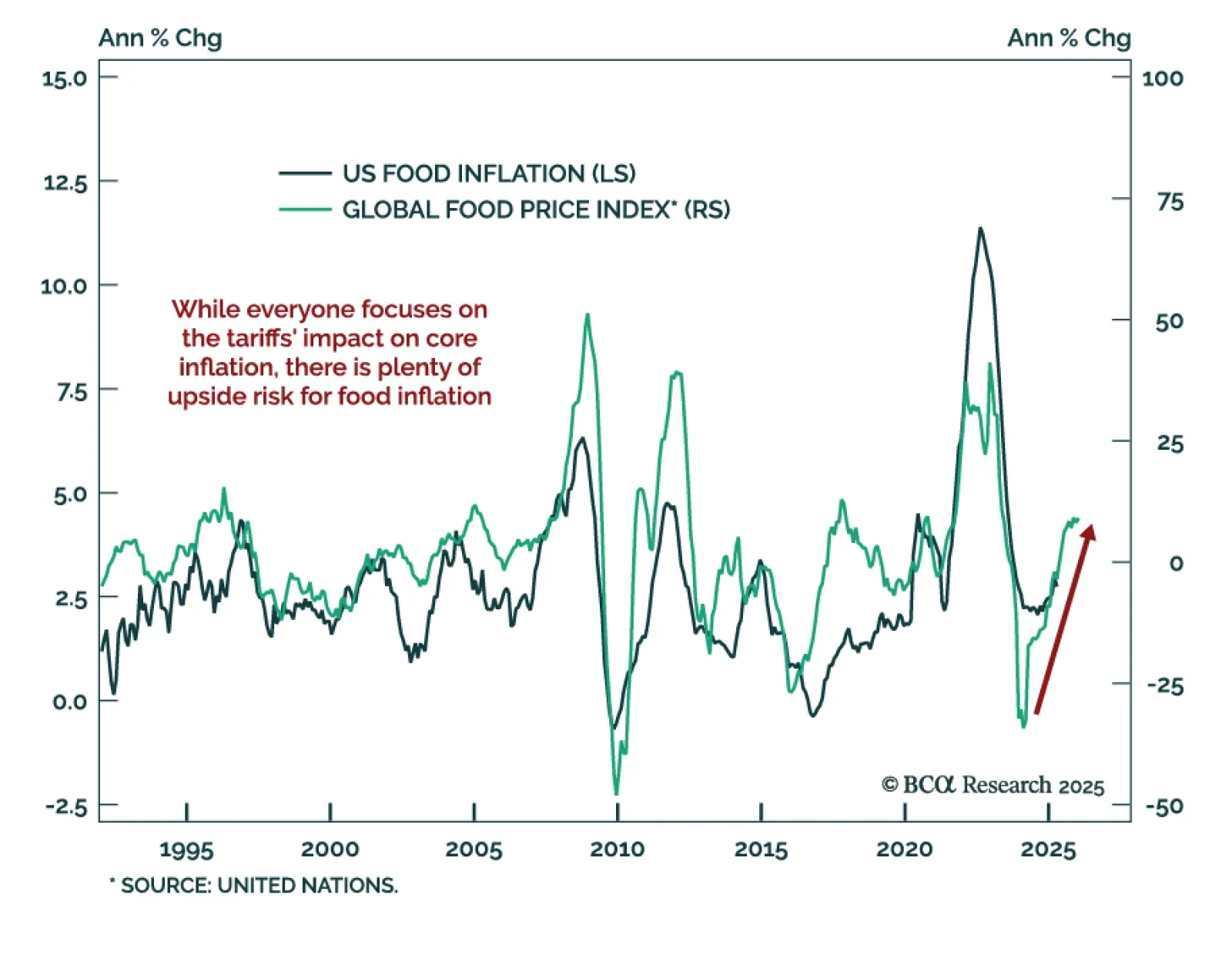

Food For Thought

…

1

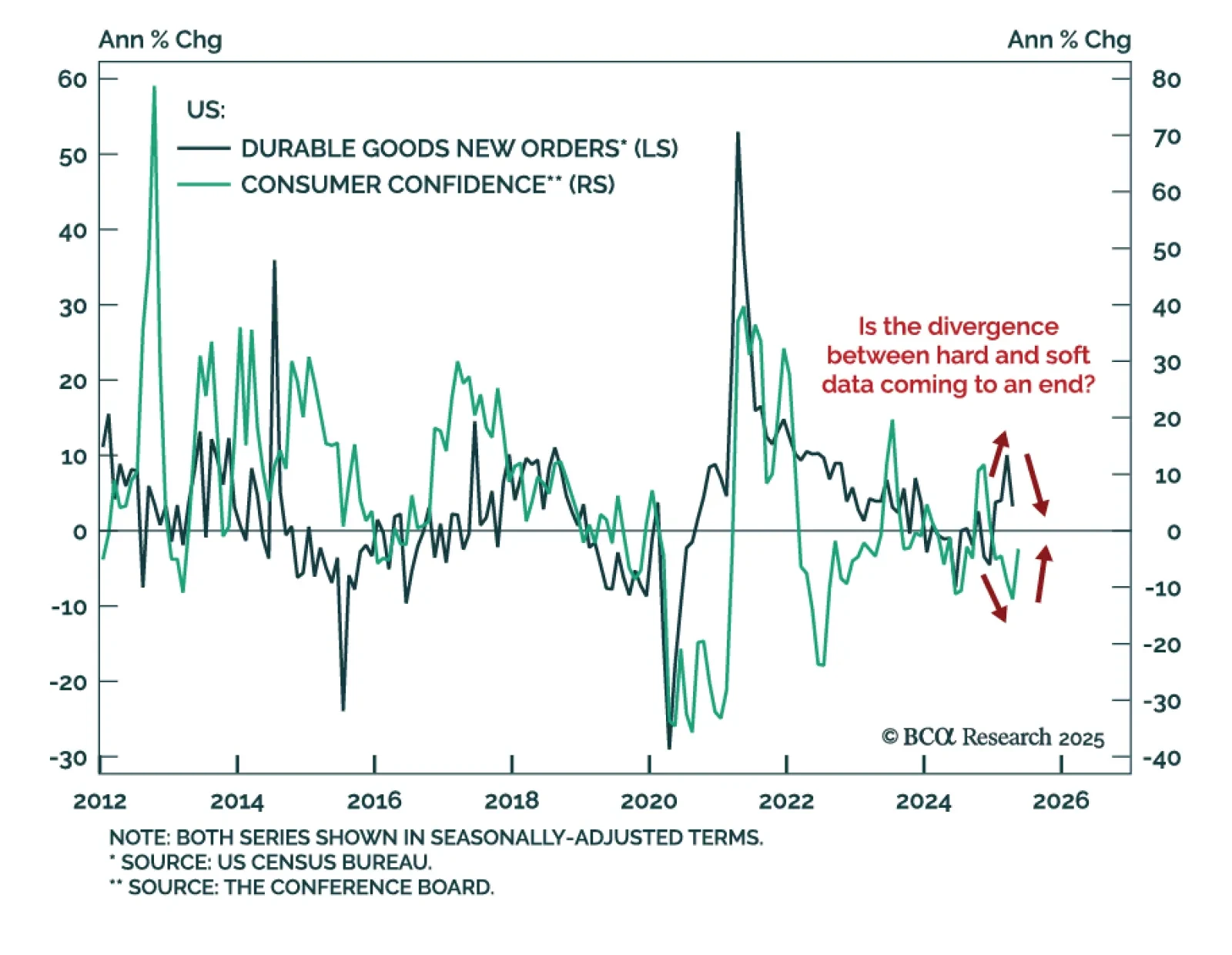

US: Hard And Soft Data Are Converging

…

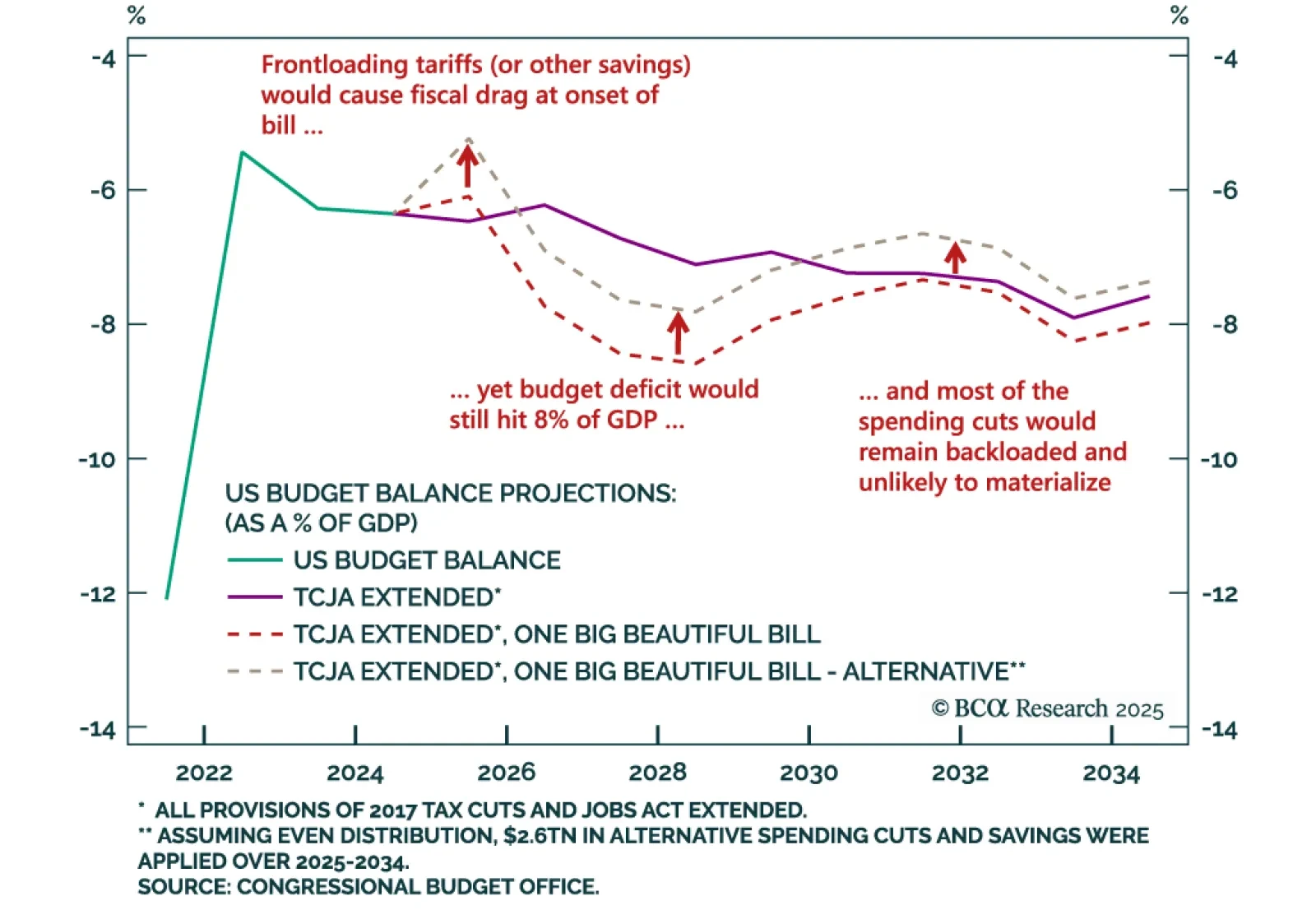

President Trump’s signature bill is surprising to the upside with budget deficits, as predicted by our Geopolitical Strategists. Some form of the bill is guaranteed to pass, no matter how many tries it takes. The bill will cut taxes more than…

Trump’s signature bill is surprising to the upside with budget deficits, as predicted. Some version is guaranteed to pass – but higher bond yields and inflation will weigh on the economy and stock market.

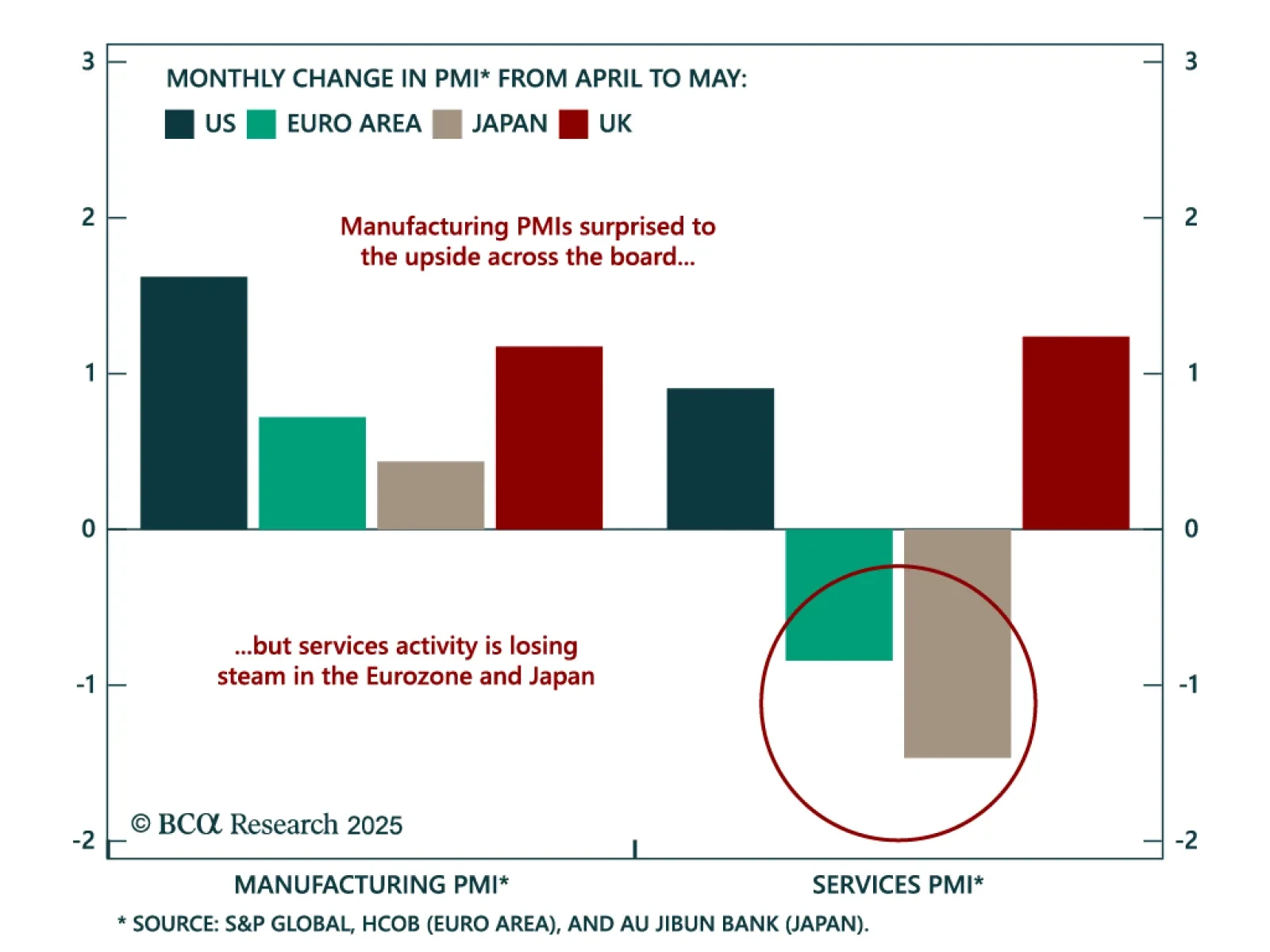

May PMIs confirm the improvement in confidence due to fewer concerns about US tariffs. Manufacturing flash PMI numbers showed resilience. The services activity PMI is more of a mixed bag.The US composite index beat estimates, increasing to 52.1 from 50.6,…

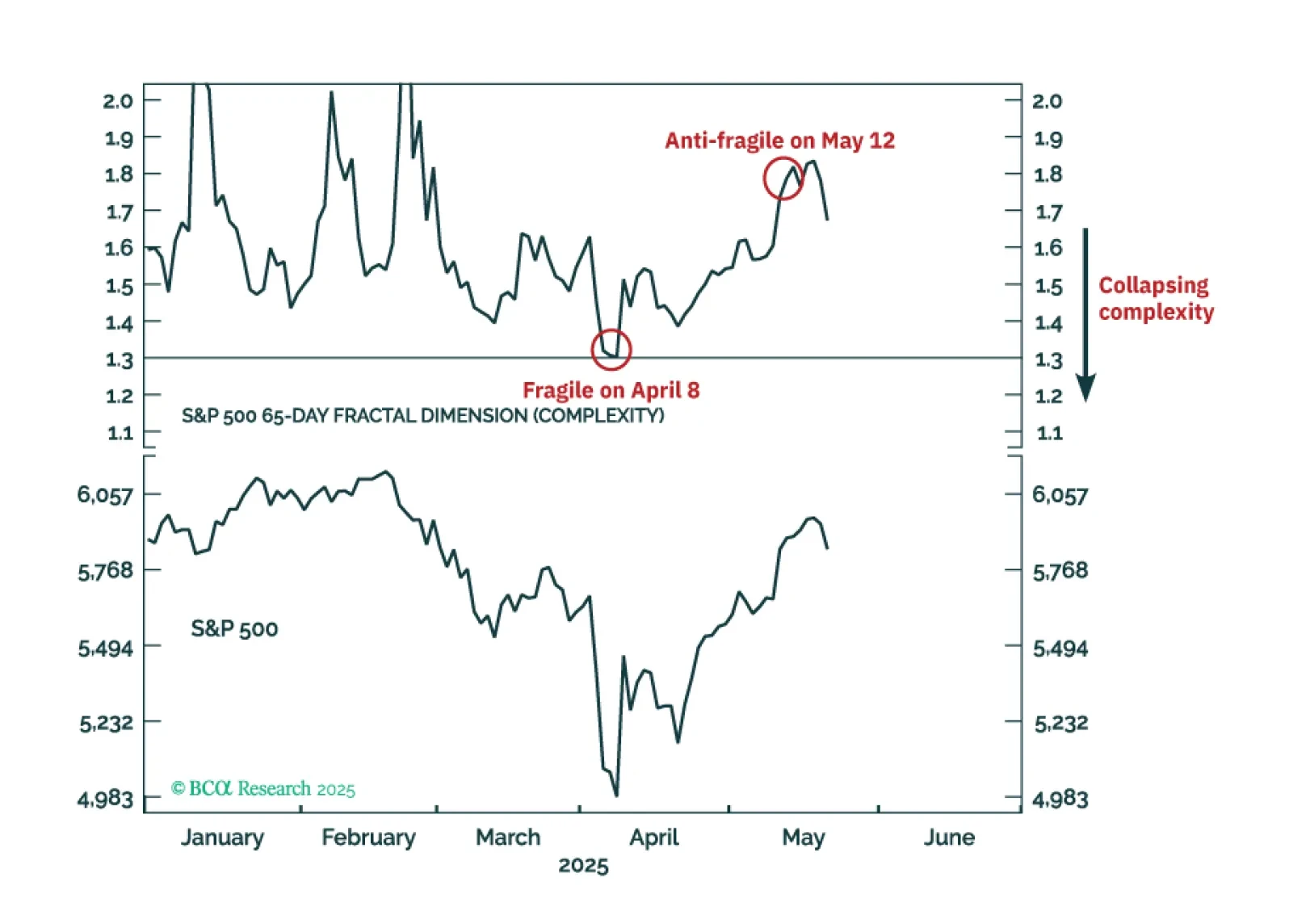

Right now, the major stock and bond markets are more ‘anti-fragile’ than fragile, and the Joshi rule recession indicators signal that a US recession is not imminent. This justifies a neutral, or default, tactical weighting to both stocks and bonds until a major market does become fragile, or until recession risk elevates. The one major price trend that is fragile is the 65-day selloff in the US dollar, which justifies a tactical overweighting to the dollar.

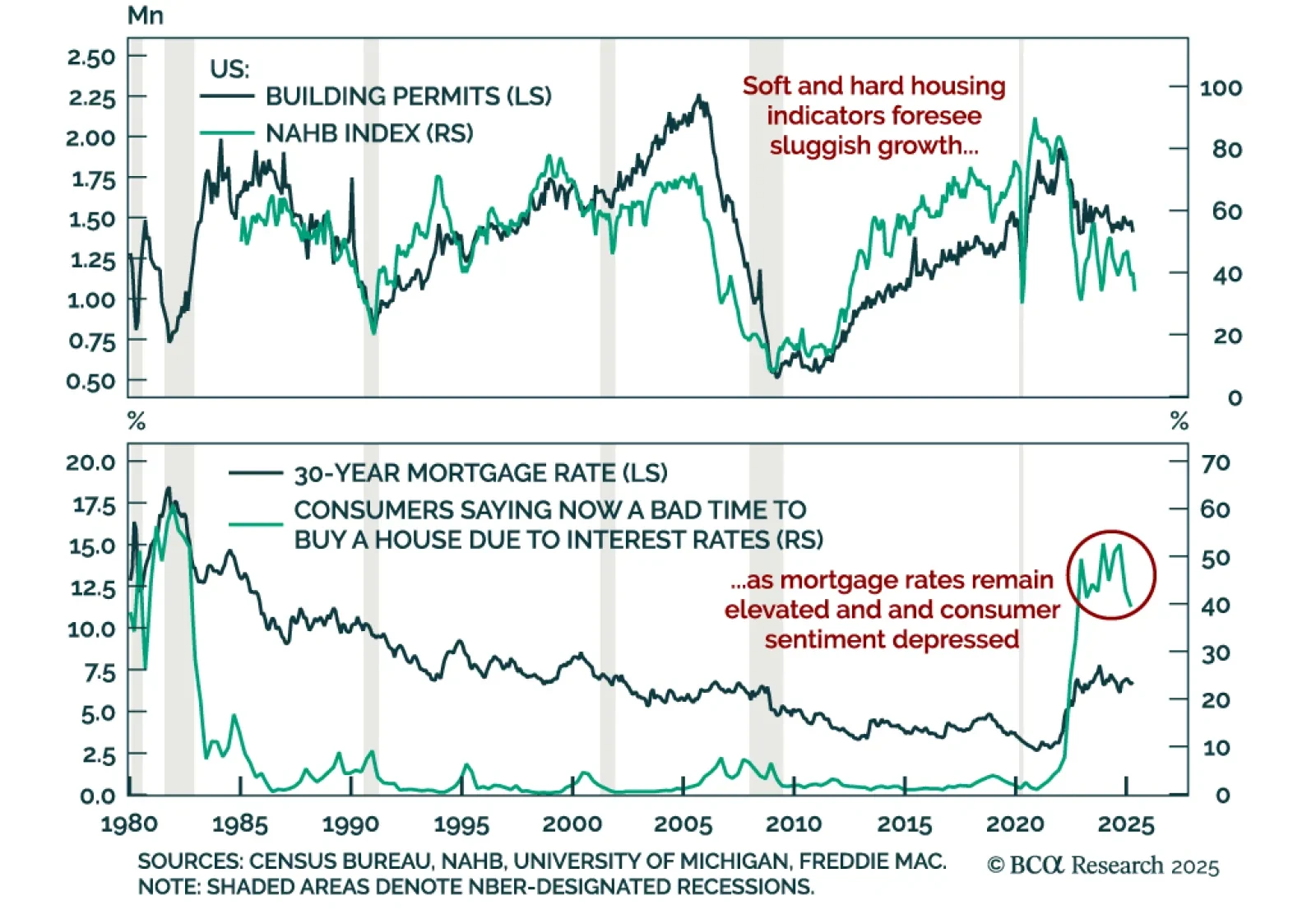

Weak April housing data and deteriorating builder sentiment reinforce our defensive stance, as recession risks remain underpriced. Housing starts rose at a 1.6% m/m annualized rate, missing expectations. Similarly, building permits, a leading indicator of…

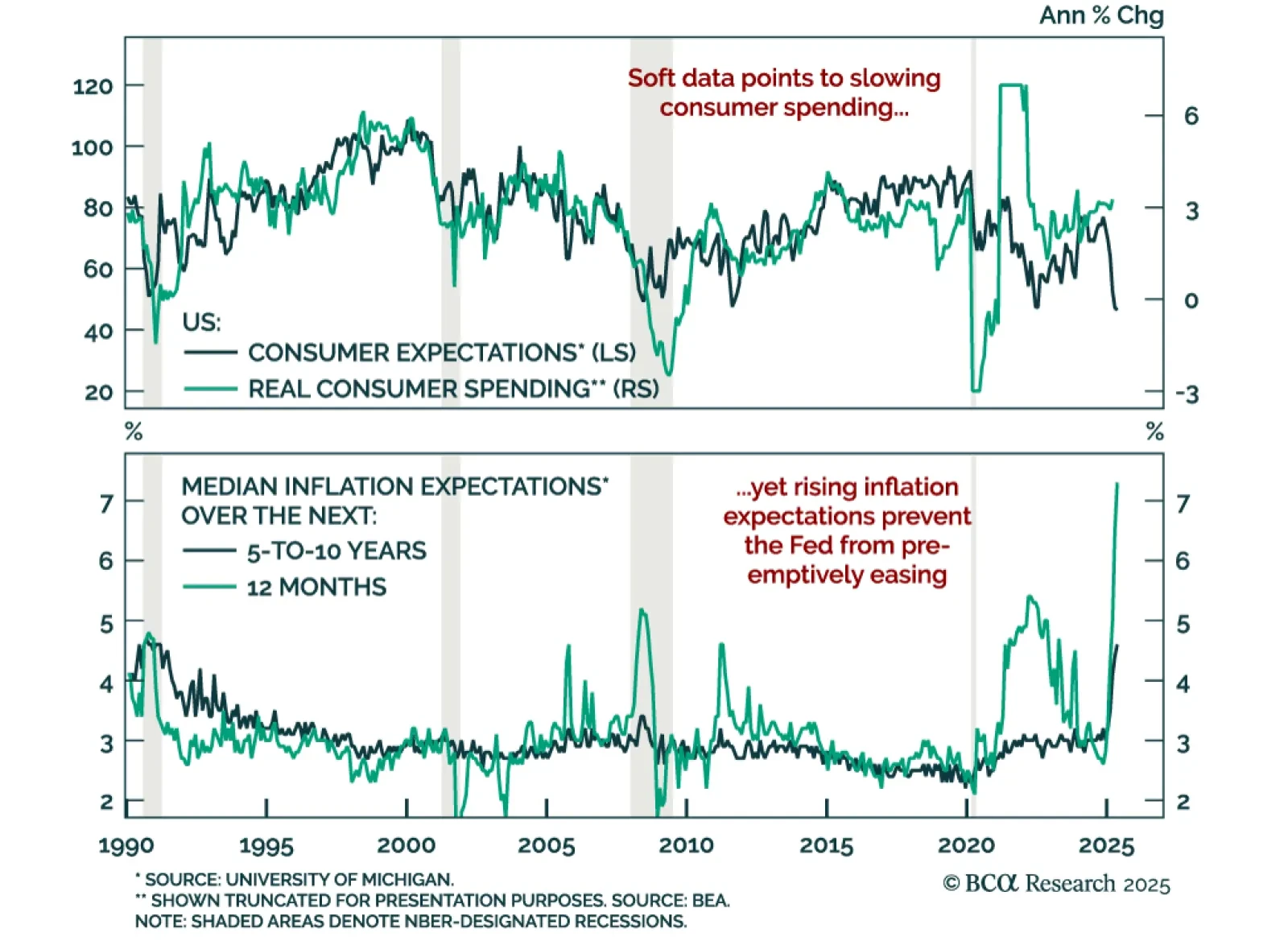

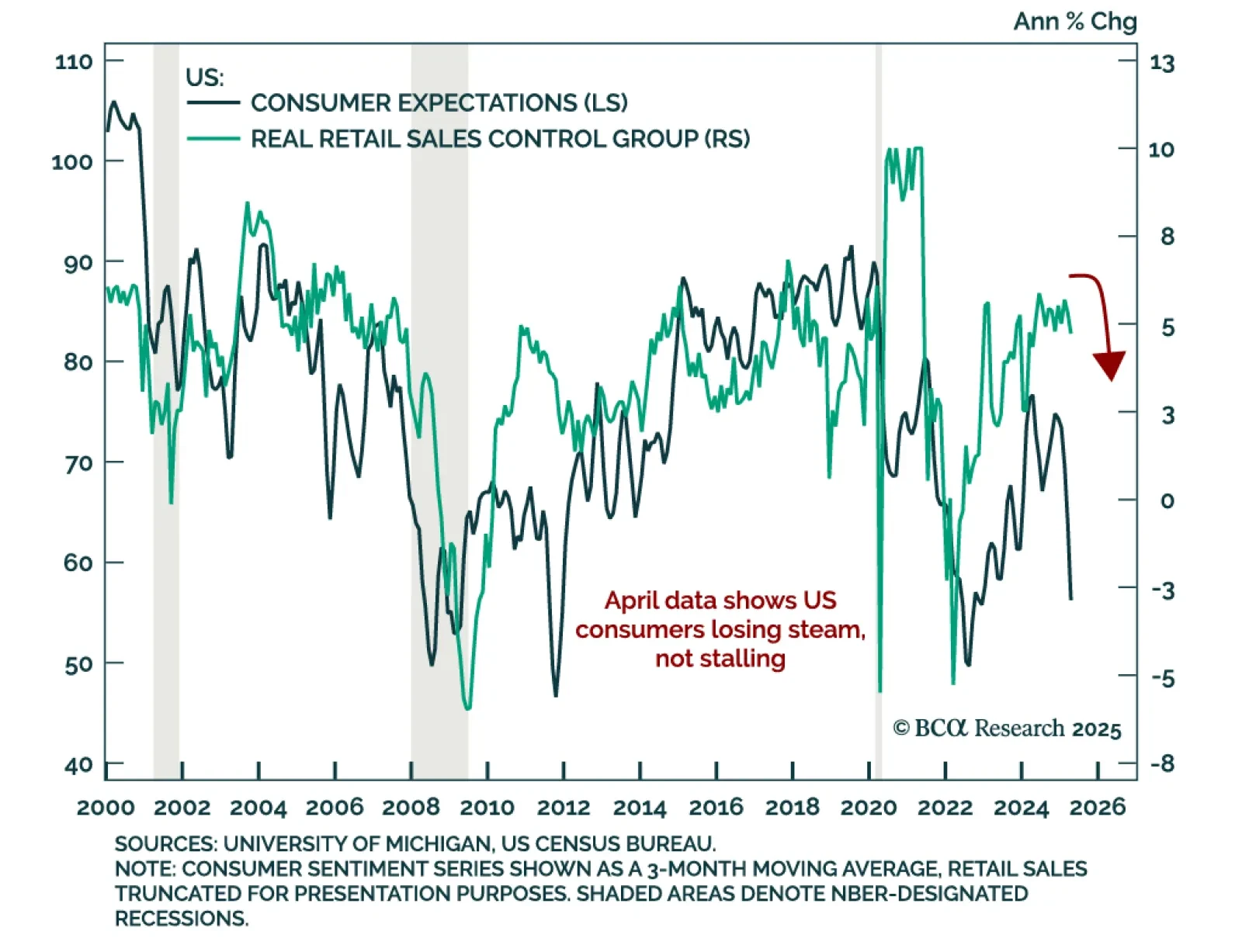

Deteriorating US consumer sentiment and surging inflation expectations add to growth concerns and reinforce our long-duration bond stance. The preliminary May University of Michigan Consumer Sentiment Index missed expectations, falling to 50.8 from 52.2. The…

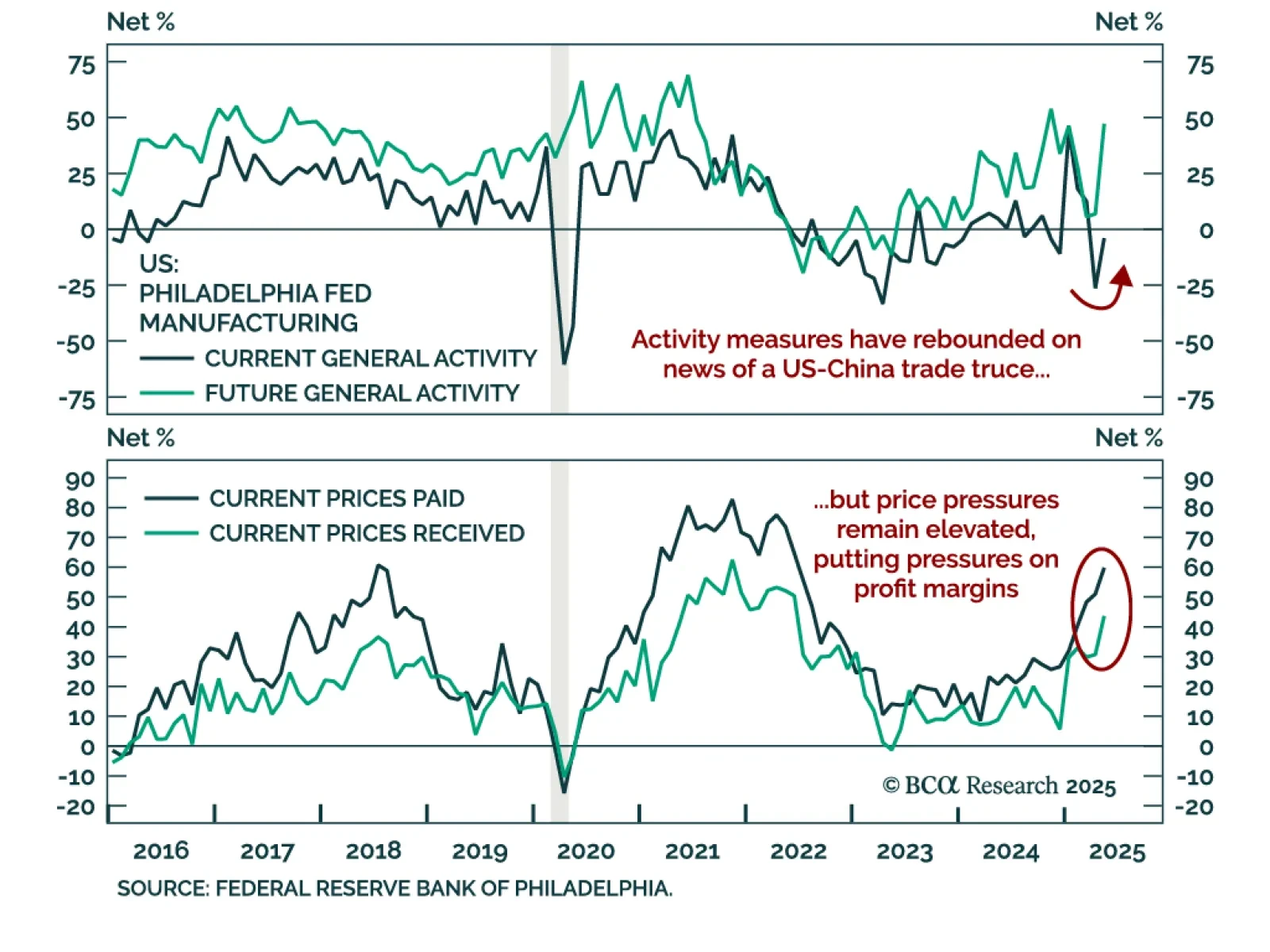

The US-China trade truce lifted short-term manufacturing sentiment in May, but margin pressures persist, reinforcing the case for defensive, domestic-focused equity positioning. The Empire and Philly Fed regional manufacturing surveys delivered a split signal…

April retail sales slowed, but signs of resilience in discretionary spending and labor data suggest US consumers are holding up. Headline retail sales rose 0.1% m/m, above expectations but decelerating from the upwardly revised 1.7% March gain. Core sales…