United States

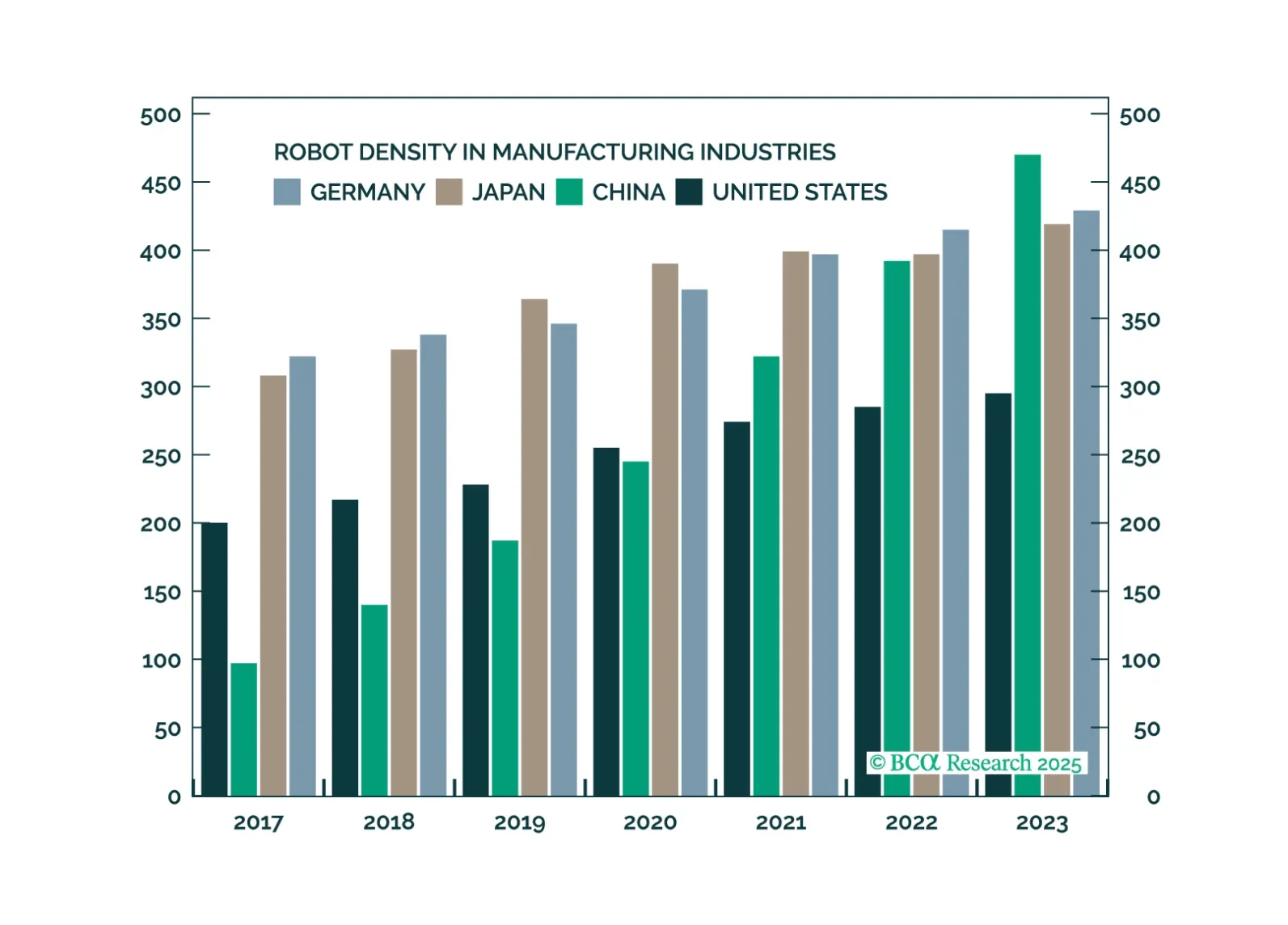

Robotics is on the cusp of a new, powerful uptrend, powered by reshoring and technological breakthroughs that make robots more capable and affordable.

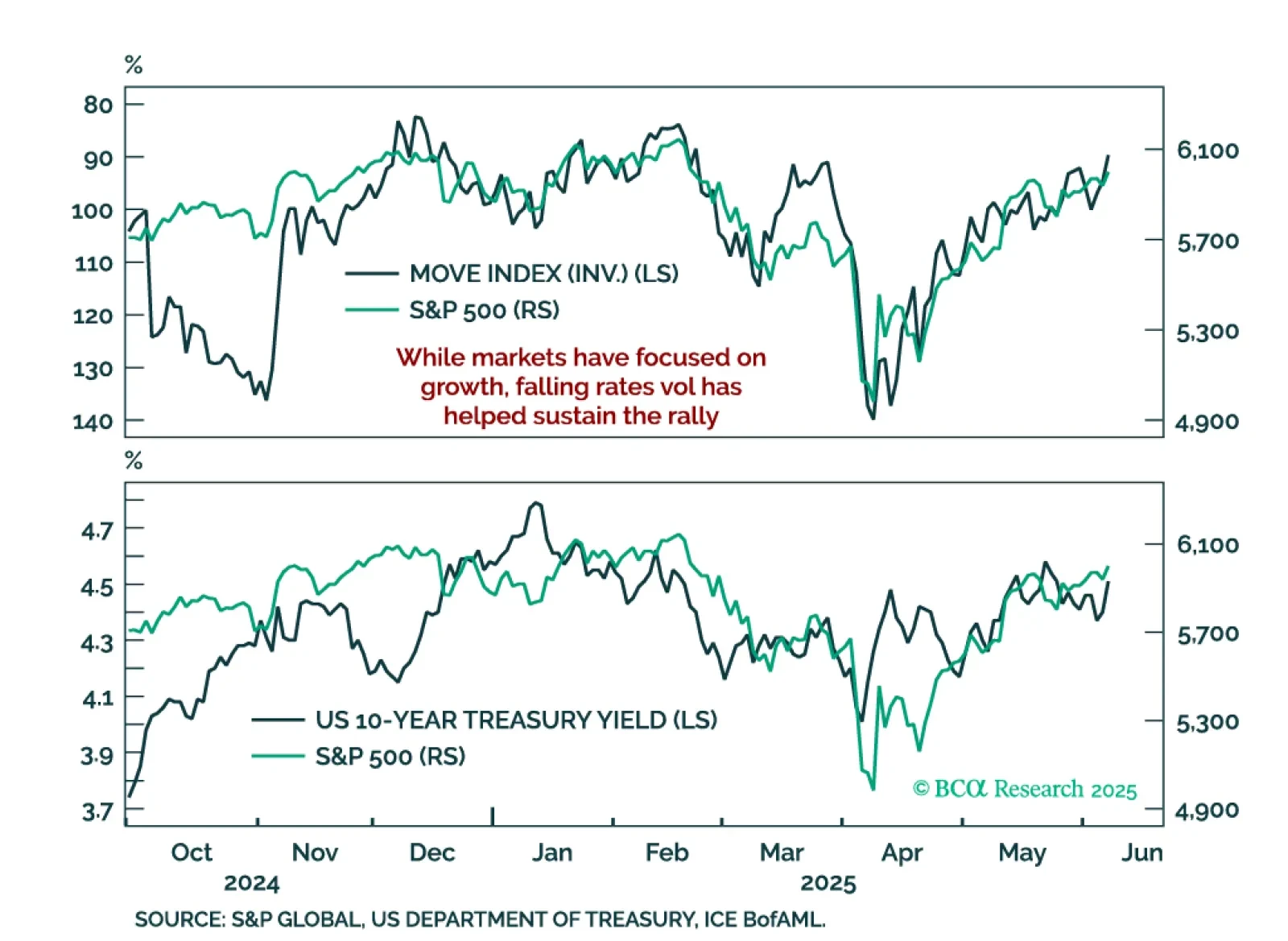

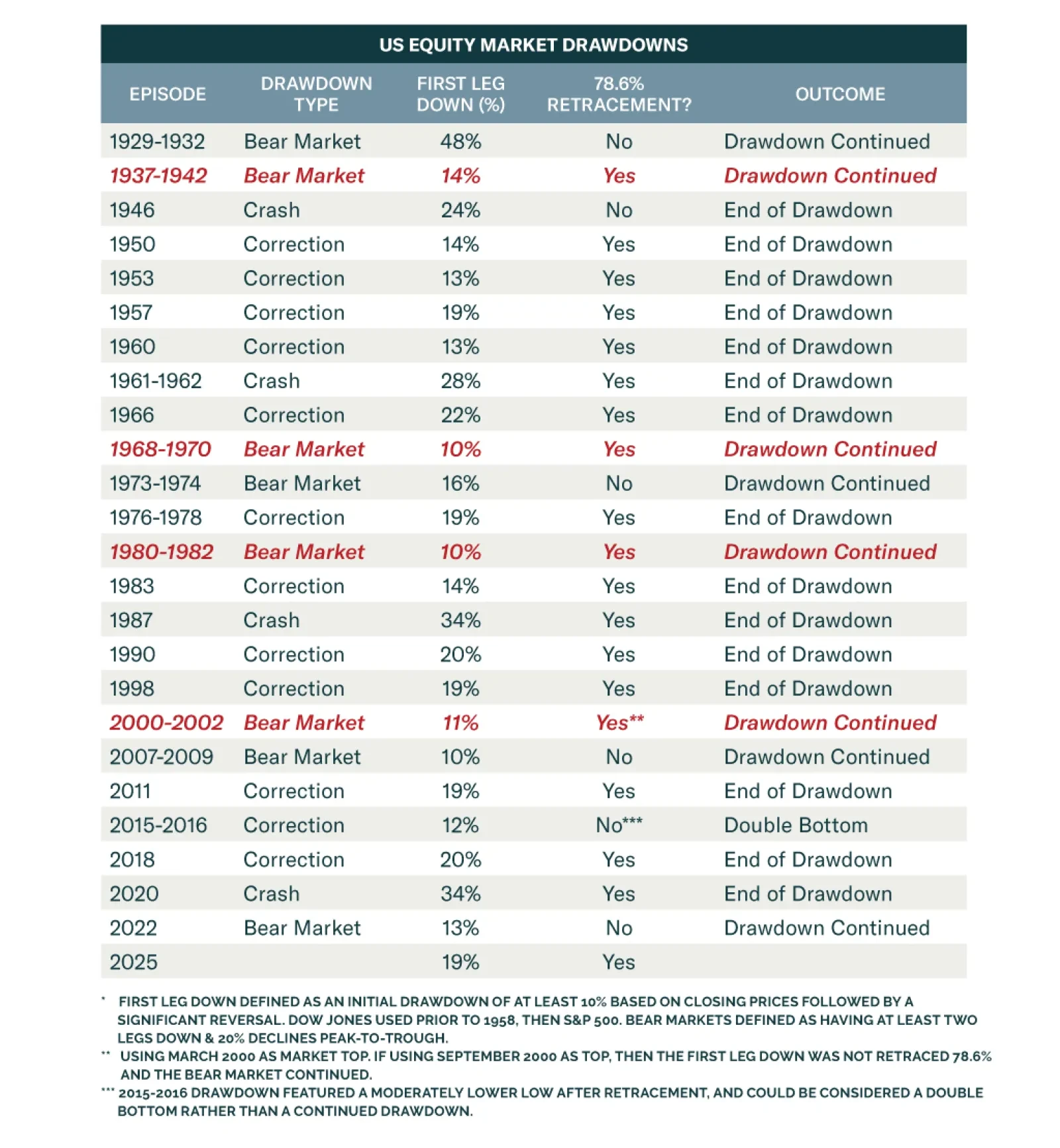

The US economy has held up better so far this year than we had expected. For the time being, investors should remain modestly underweight equities. A more aggressive underweight would be justified only once the “whites of the recession’s eyes” are visible.

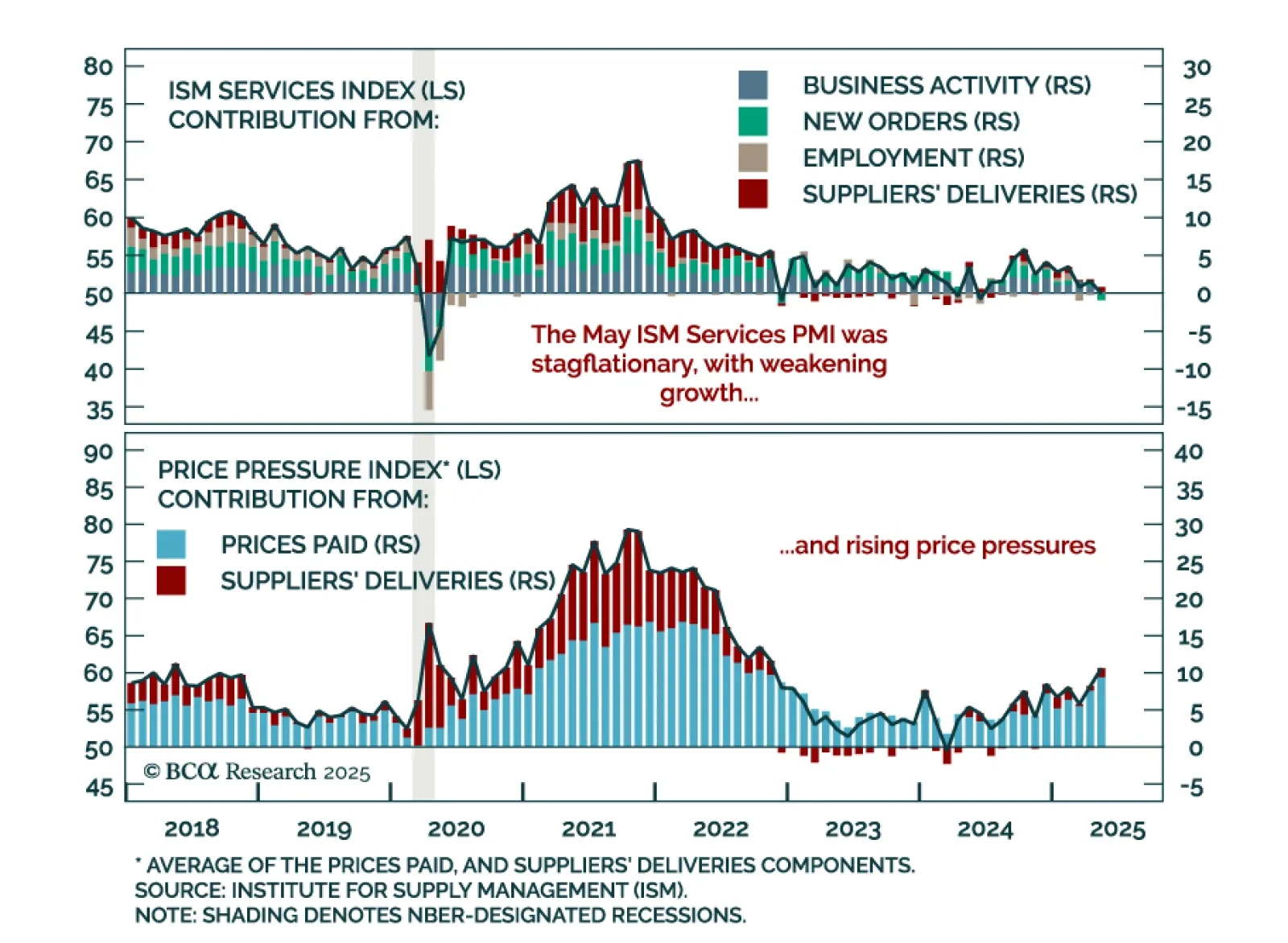

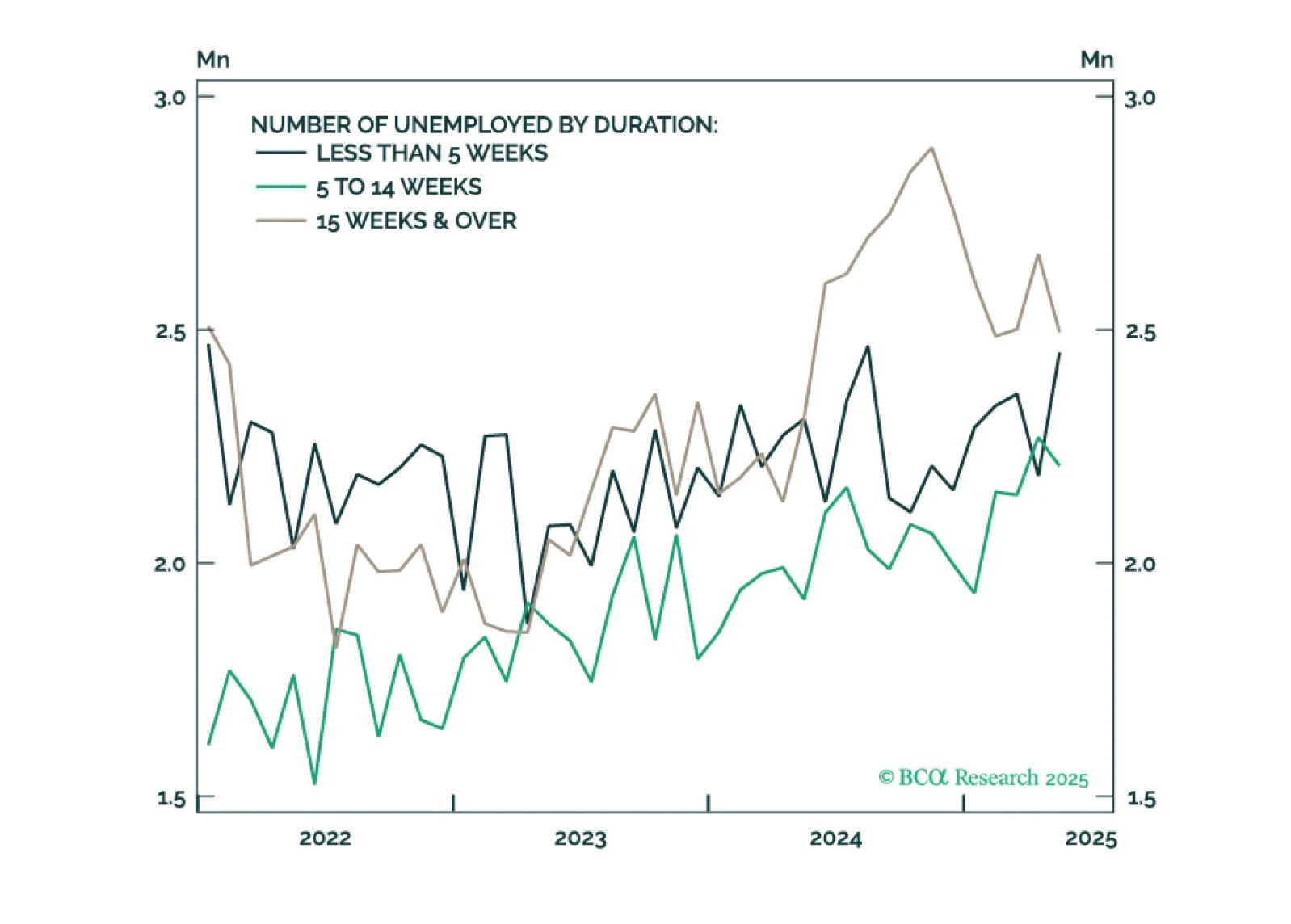

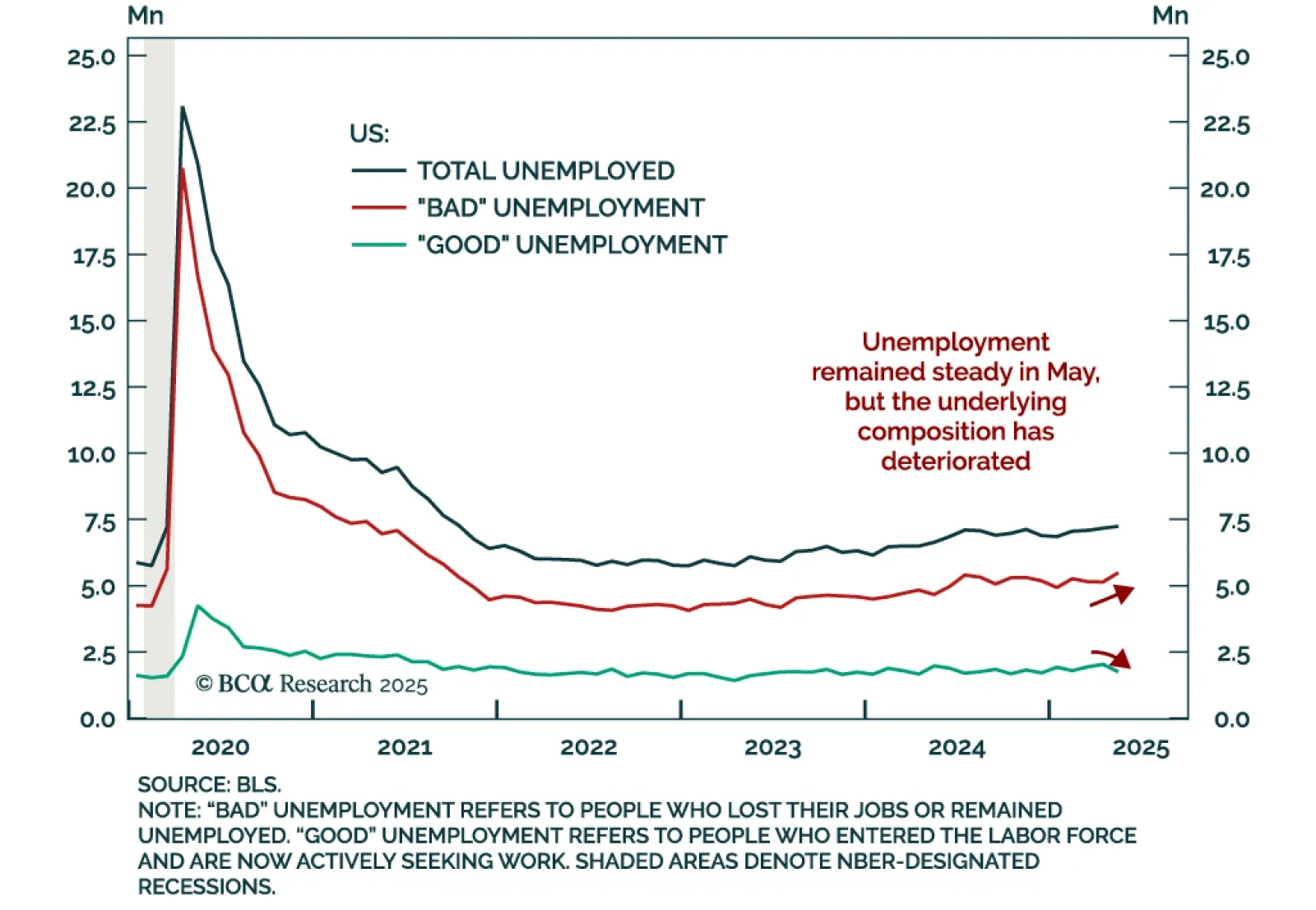

For now, measures of labor market utilization (like the unemployment rate) are only gradually weakening. But we know from history that these trends have a habit of quickly accelerating in advance of recession.

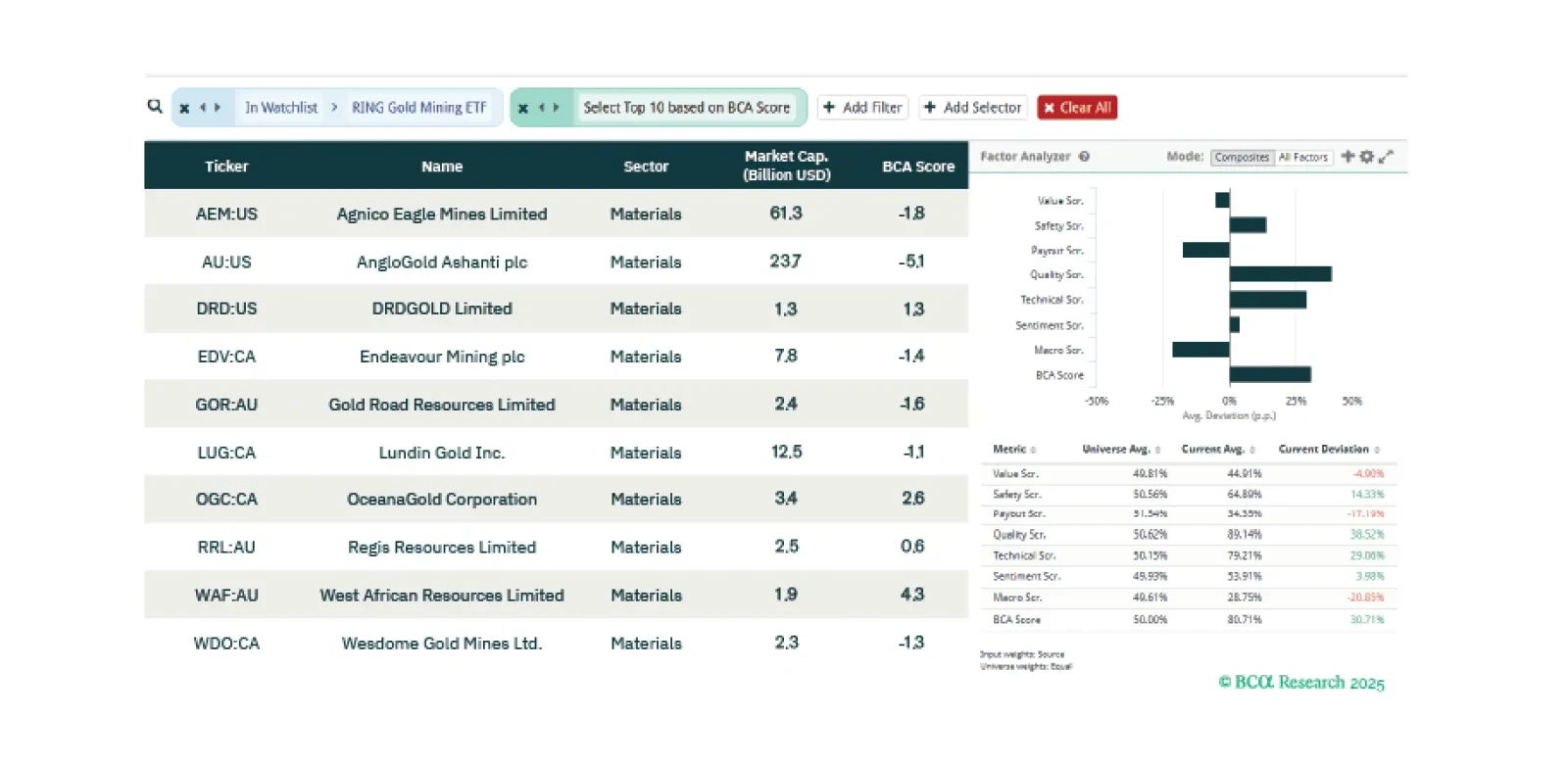

This week our three screeners explore equity trades in gold mining stocks, European banks, and US stocks ex-Tech should a recession not be imminent.