United States

1

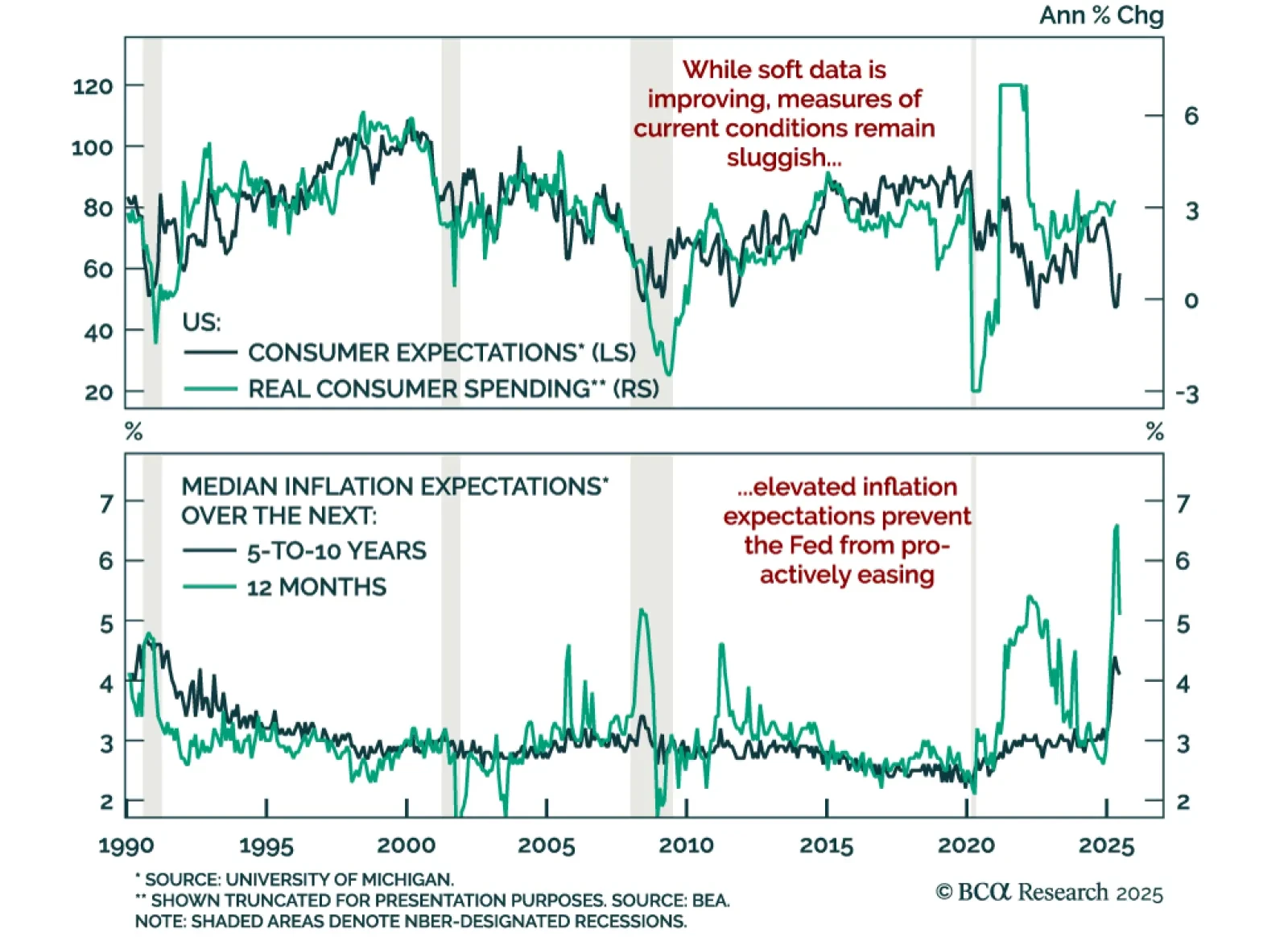

Consumer Sentiment Rebounds, But Fed Still Trapped by Sticky Expectations

…

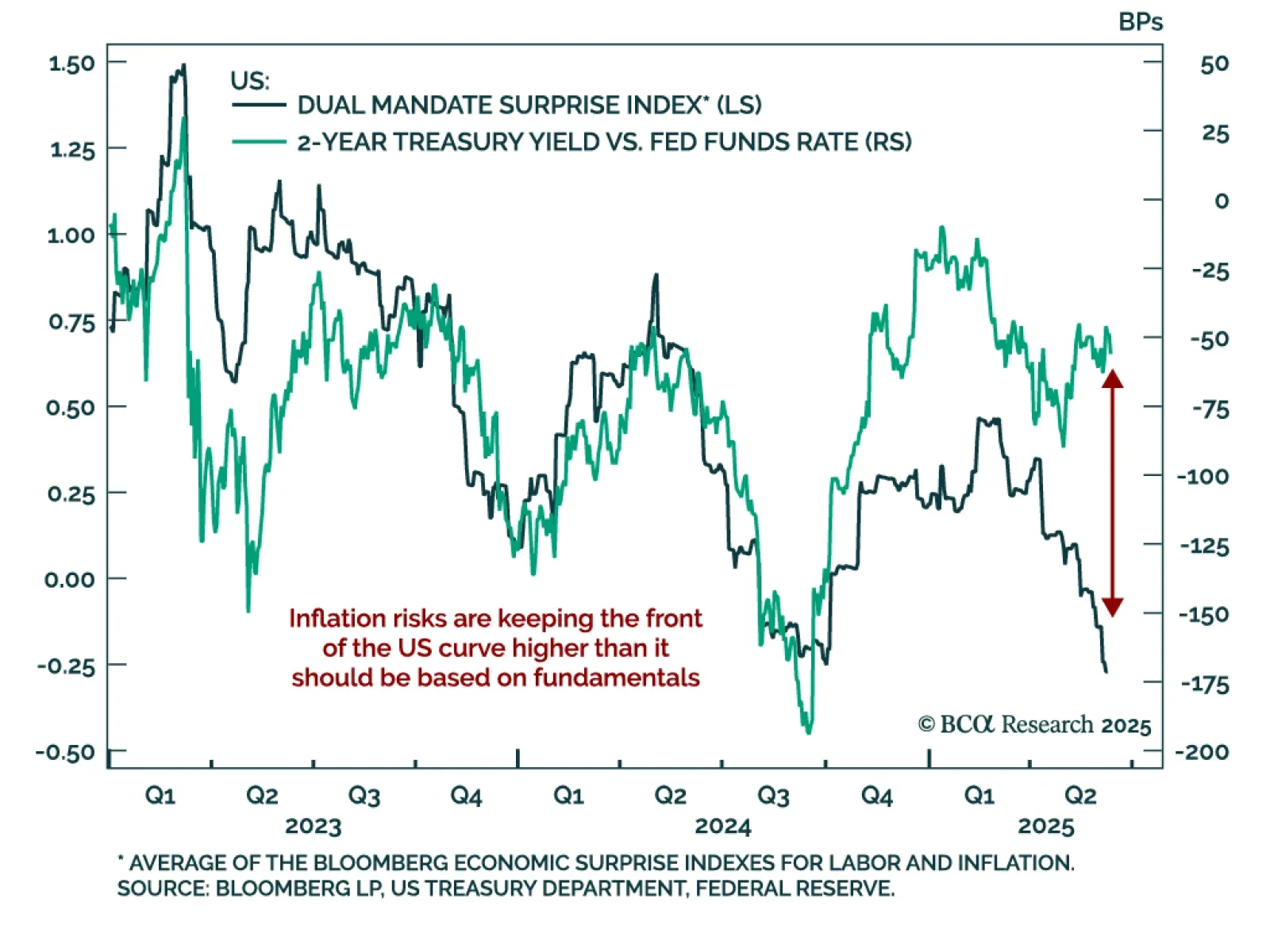

Elevated inflation expectations are keeping the Fed sidelined, reinforcing our long-duration and steepener bias in US rates. The US May CPI would have normally supported cuts, but the Fed cannot risk elevated short-term inflation expectations feeding…

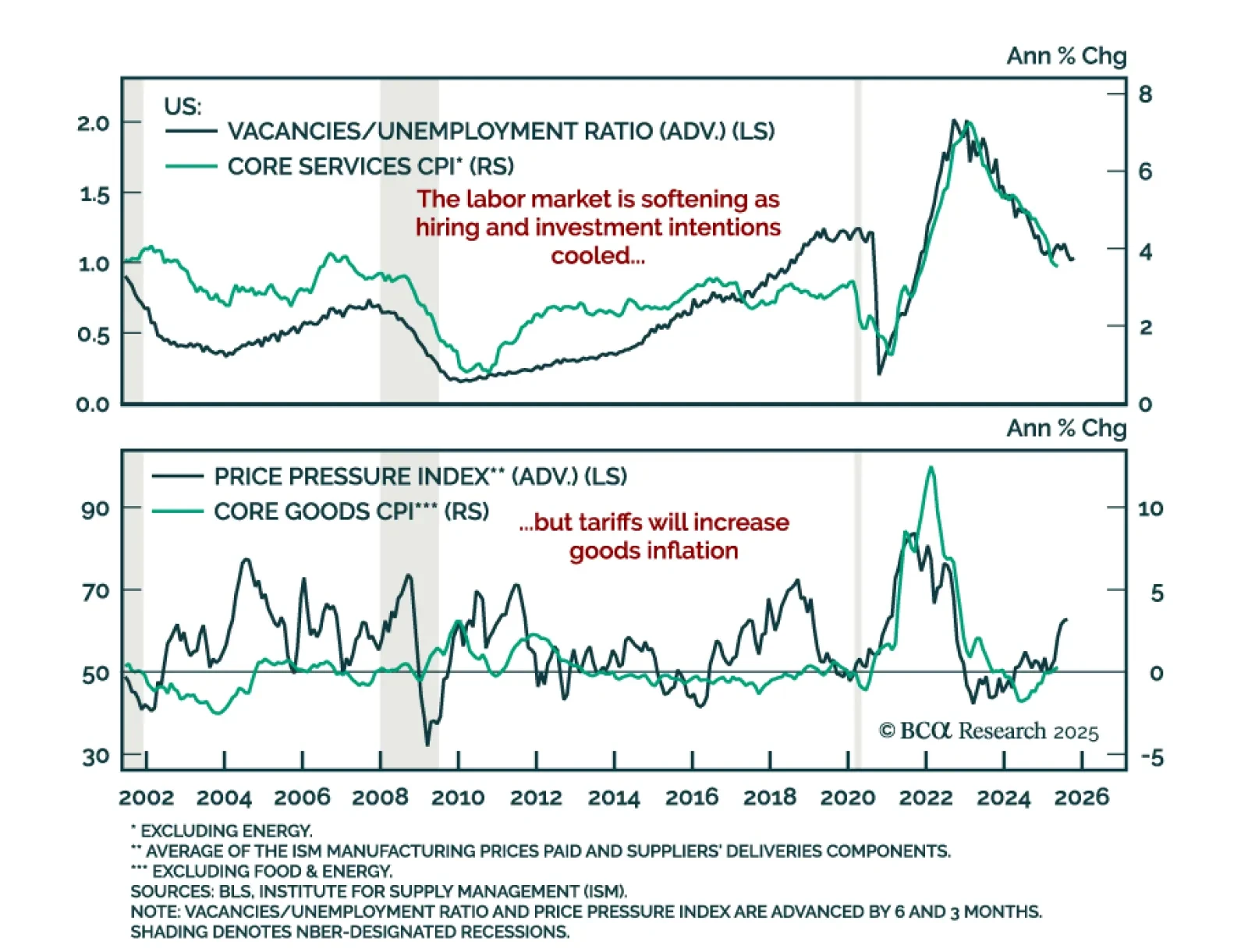

Further labor market deterioration would trigger a shift to maximum underweight in equities. While soft indicators have markedly deteriorated, hard labor data remains relatively resilient, though it has clearly weakened. The labor market is still in…

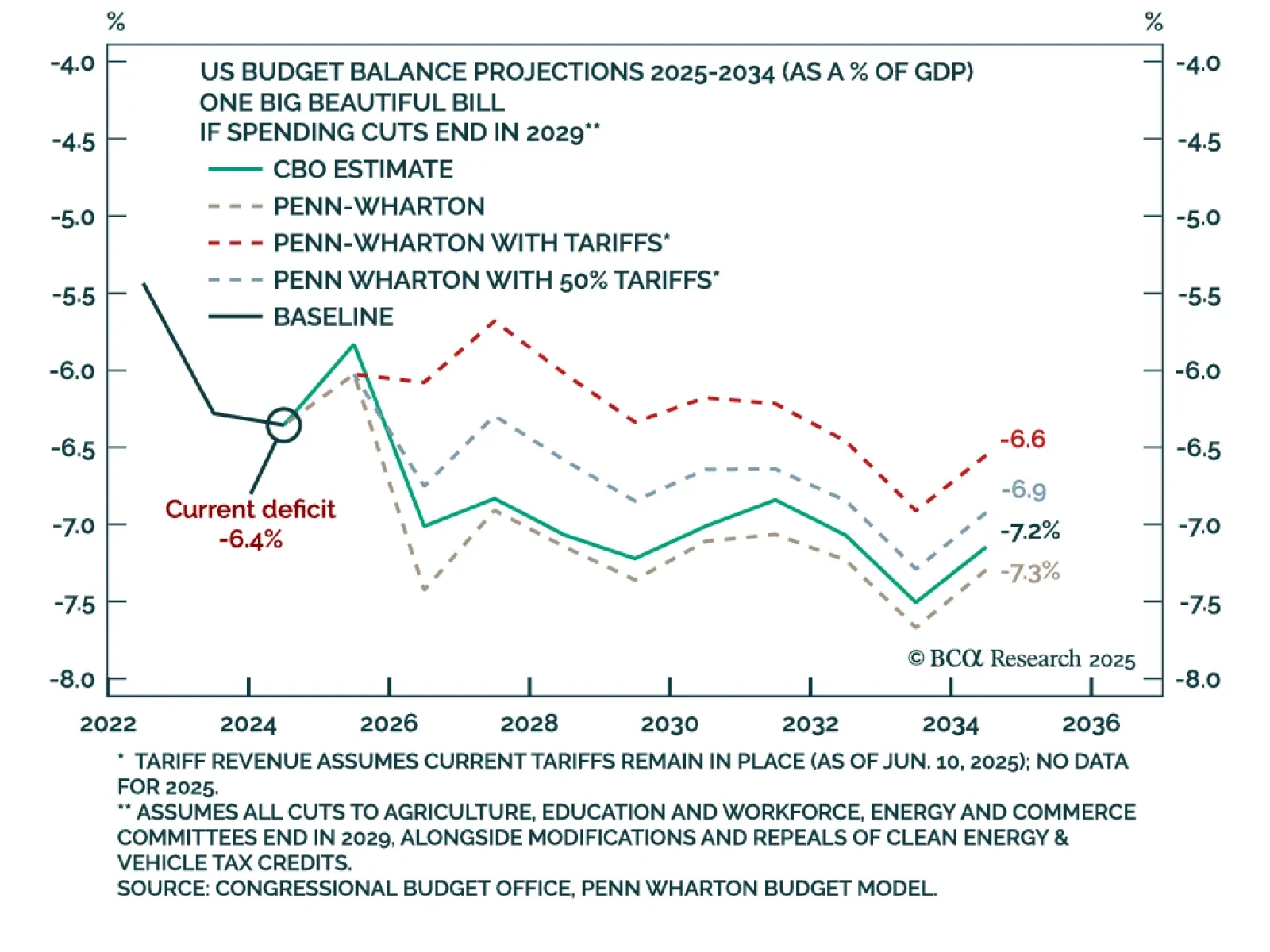

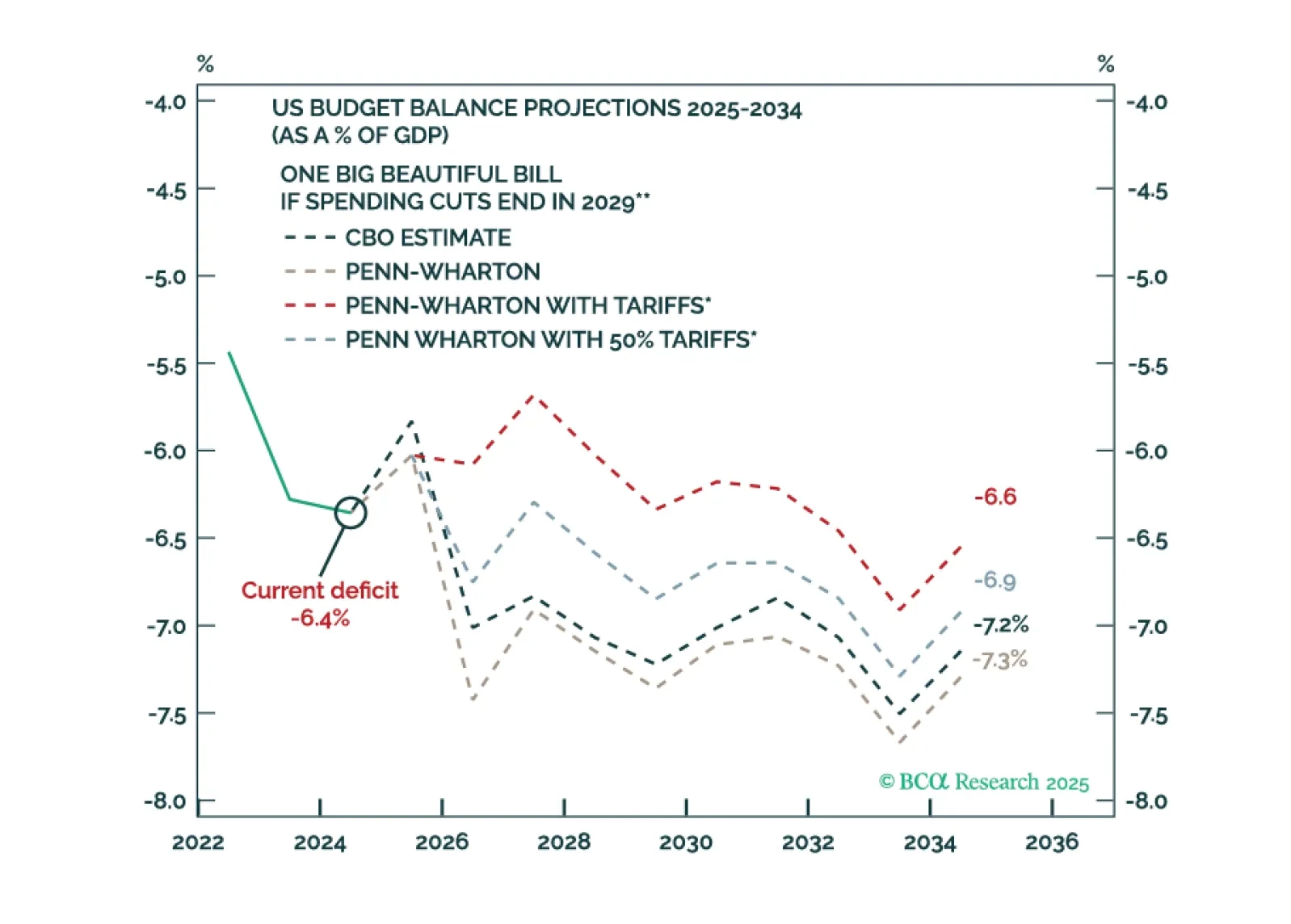

BCA’s Geopolitical strategists expect further bond market volatility as Congress advances the “One Big Beautiful Bill,” which will act as a new fiscal stimulus ahead of the midterms. They assign a 90% probability to the eventual passage of the OBBB which is…

1

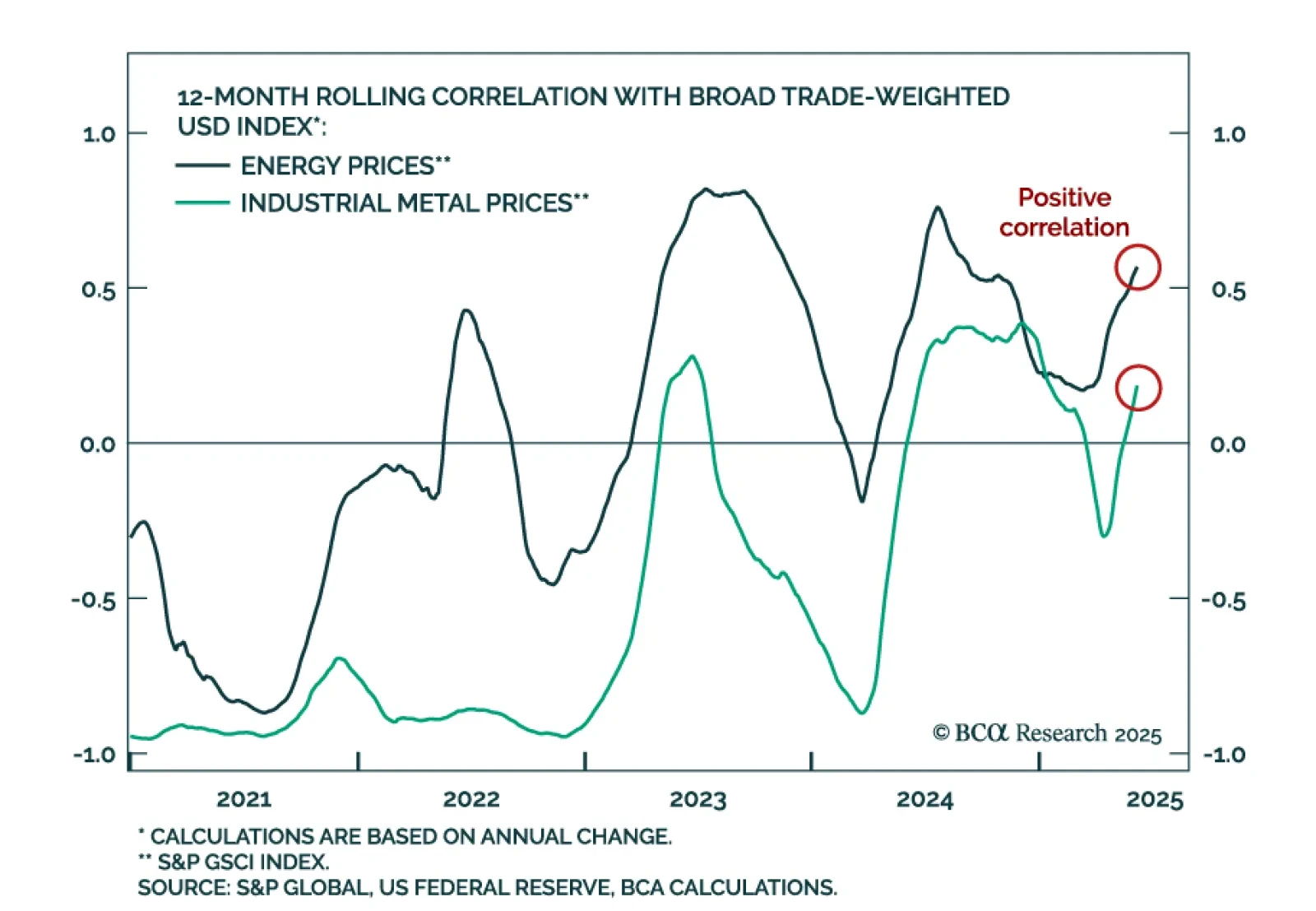

Shifting Commodity Correlations

…

1

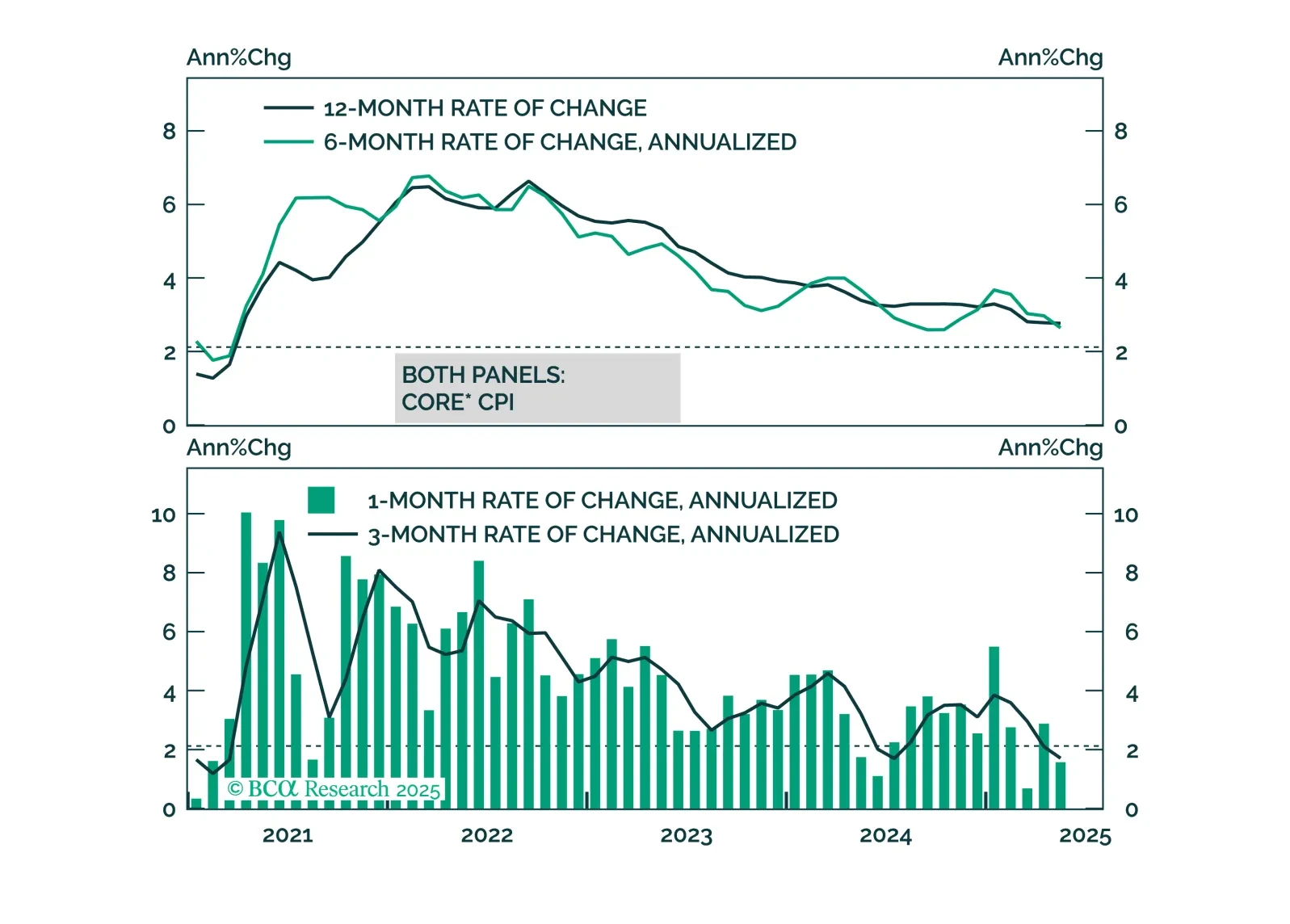

US: Cold CPI Is No Green Light For Cuts in June

…

1

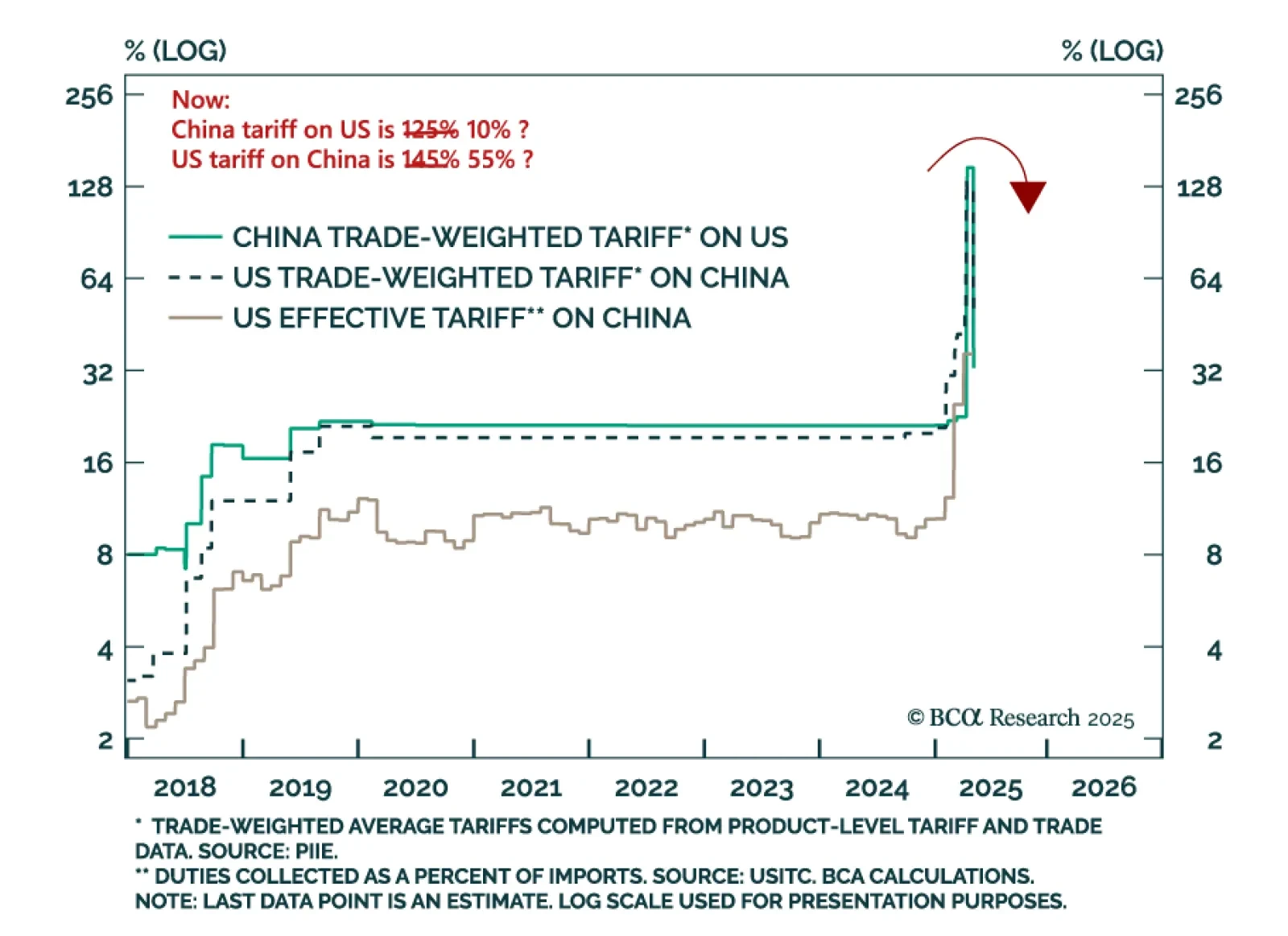

US-China Trade De-Escalation Won’t Drive New Highs

…

While we anticipate higher inflation in June, it looks increasingly likely that the price impact from tariffs will be less aggressive and long-lasting than many feared.

Bond market volatility will spike again in the near term. The Fed is committed to an easing cycle yet the Trump administration’s signature fiscal policy action will stimulate the economy. Tariffs are supposed to keep the budget deficit contained but they are inflationary.

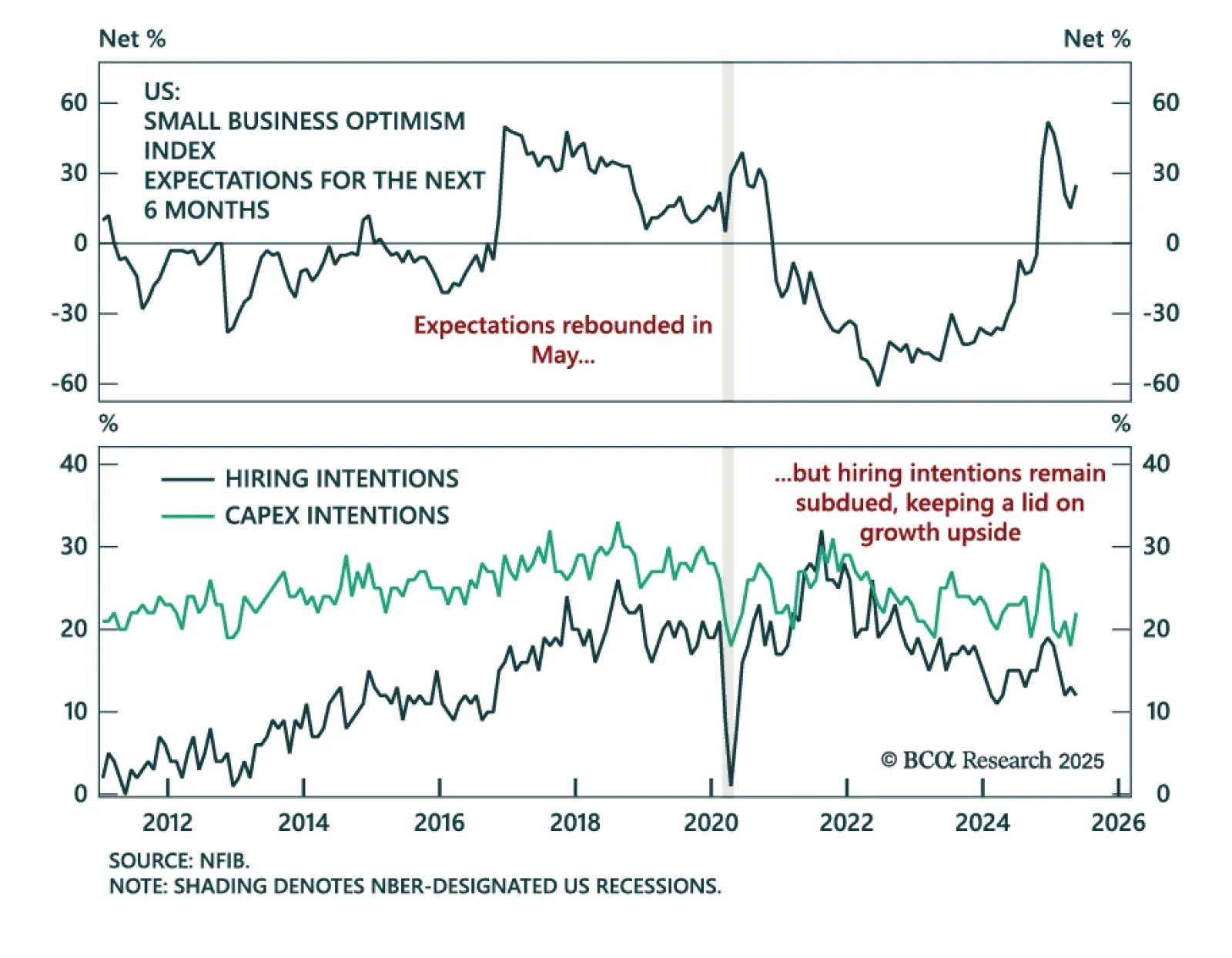

Small business confidence improved in May, but hiring intentions fell and activity remains sluggish, reinforcing our cautious equity stance. The NFIB Small Business Optimism Index rose to 98.8, beating expectations. However, most of the improvement came from…