United States

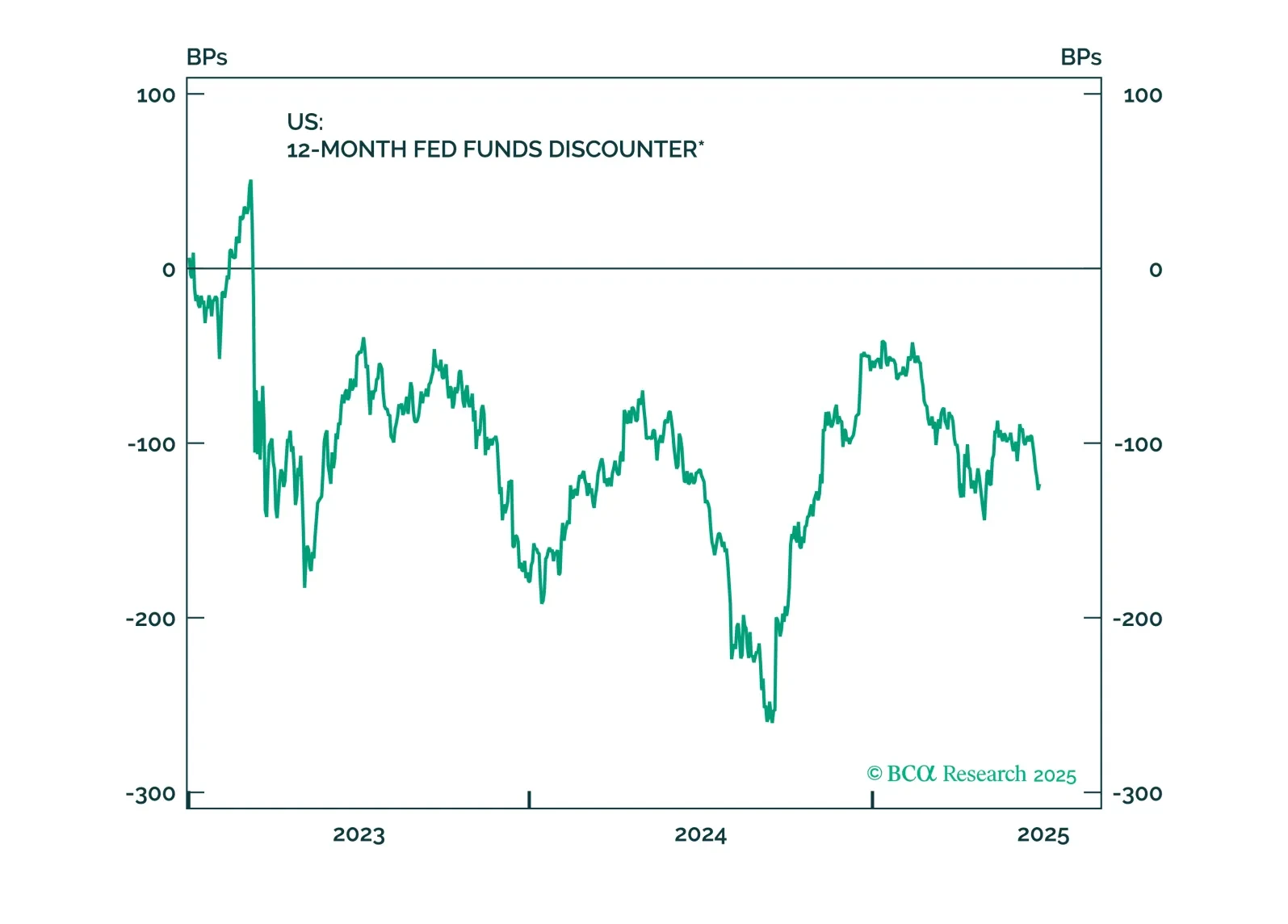

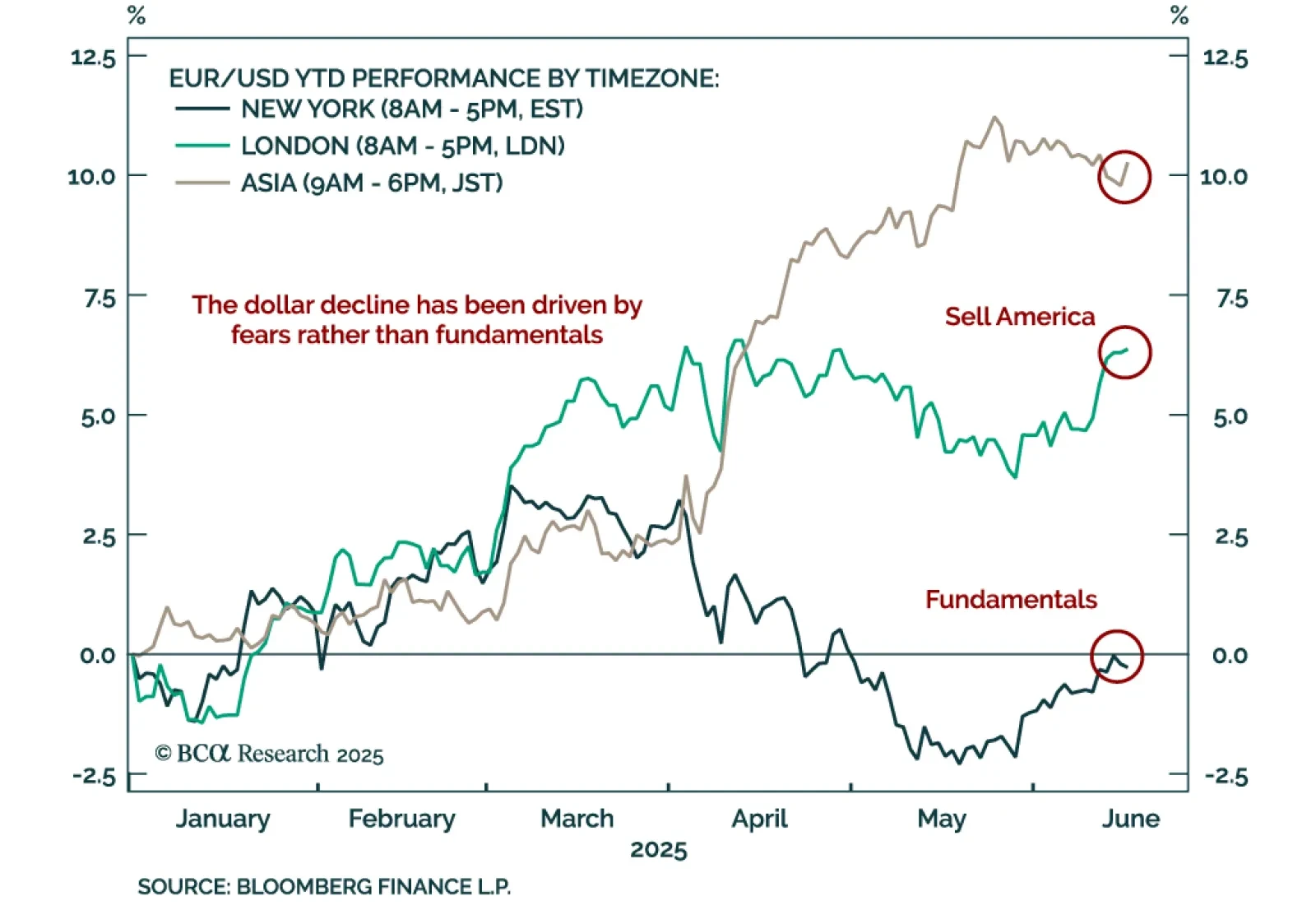

Monetary policy is about to become a powerful tailwind to the already bullish brew that includes Trump’s repeated step-downs from a global trade war, irrelevant geopolitical risks in the Middle East, and a fiscal policy that is no longer as alarming to the bond markets as the raft of campaign promises appears to be. Investors should hesitate to get overly bearish either bonds or stocks. However, we remain uber USD bears.

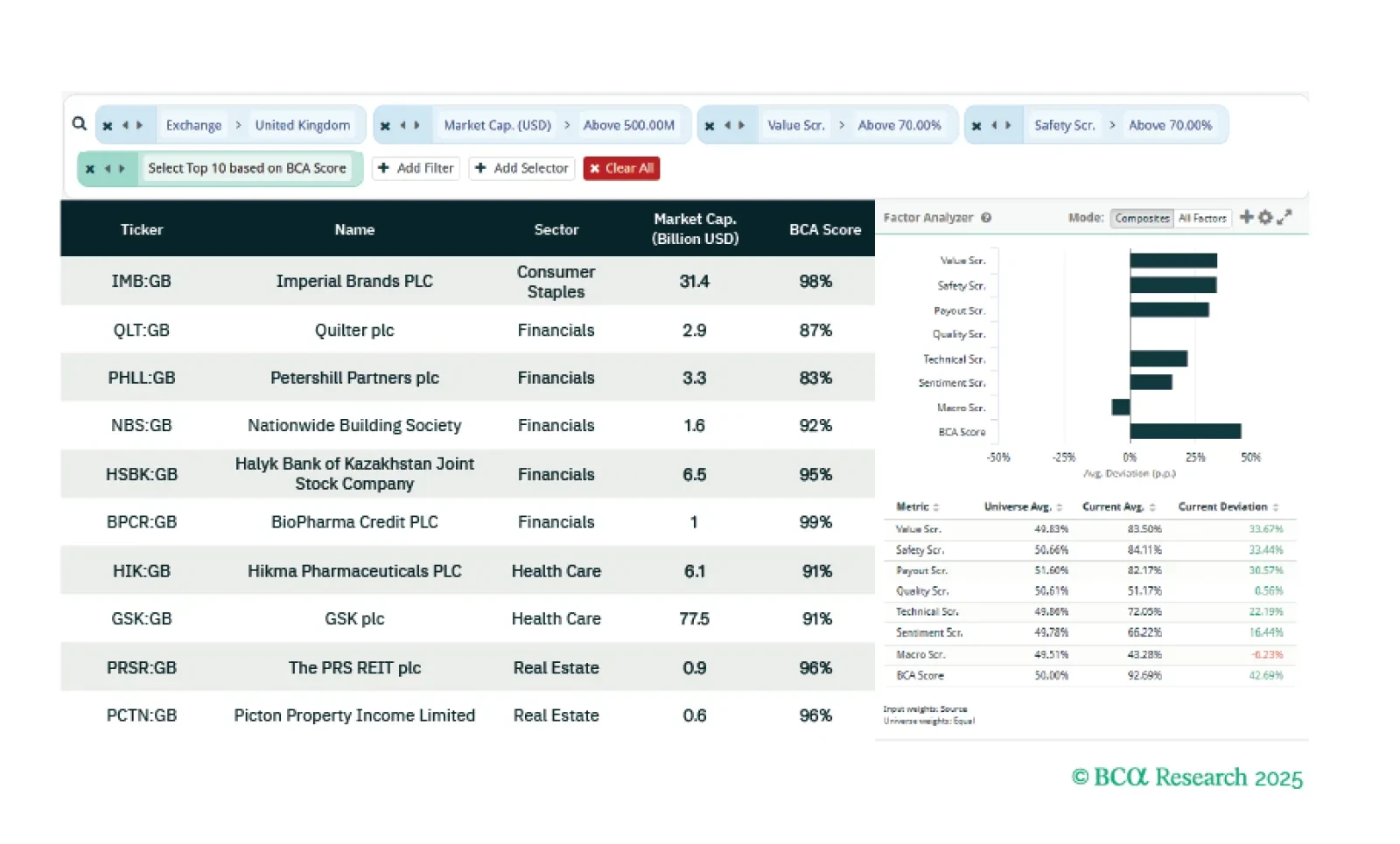

This week our three screeners explore: UK stocks that are cheap and offer a geopolitical hedge; French stocks that are sensitive to China; and US Value and dividend paying stocks.

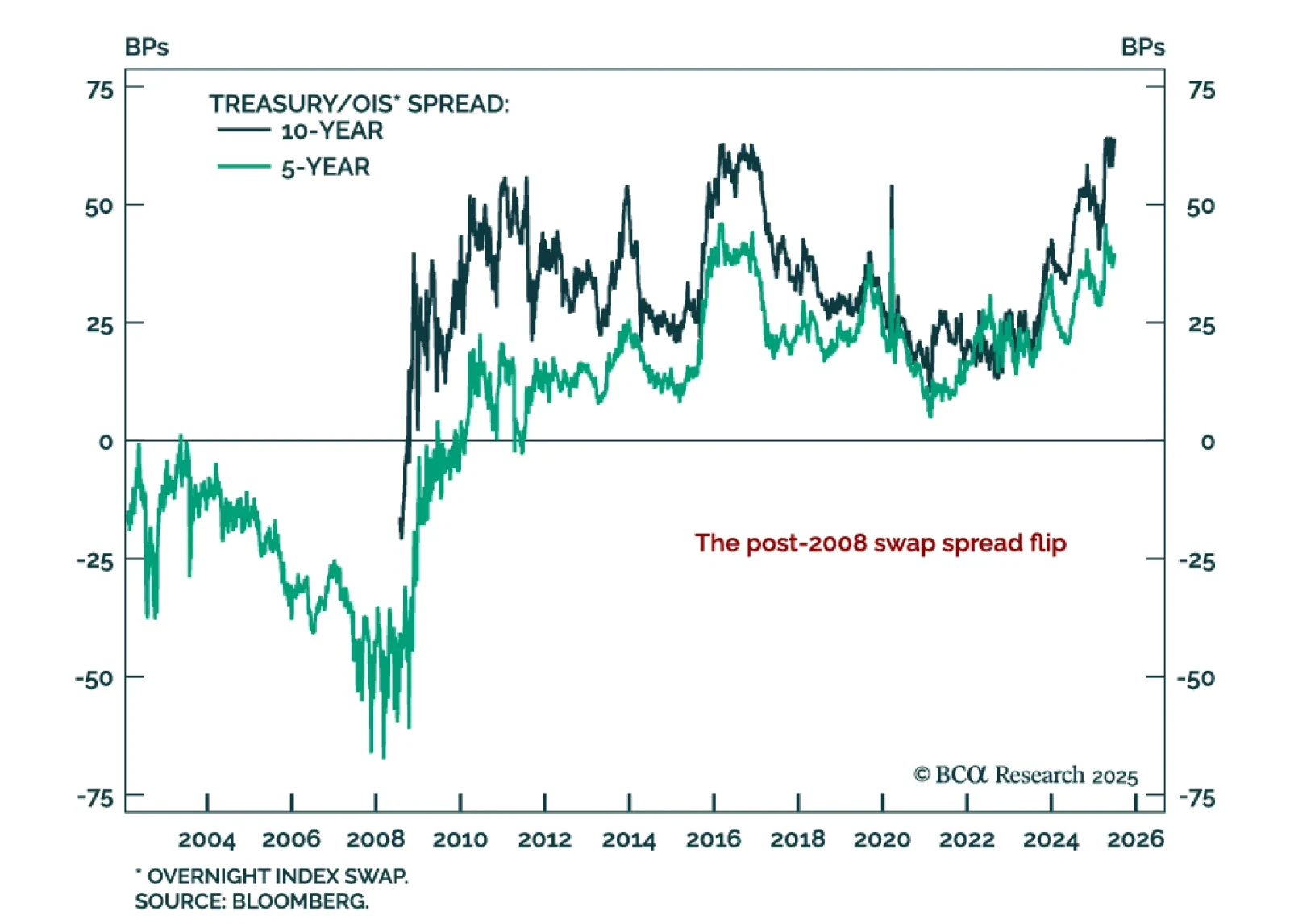

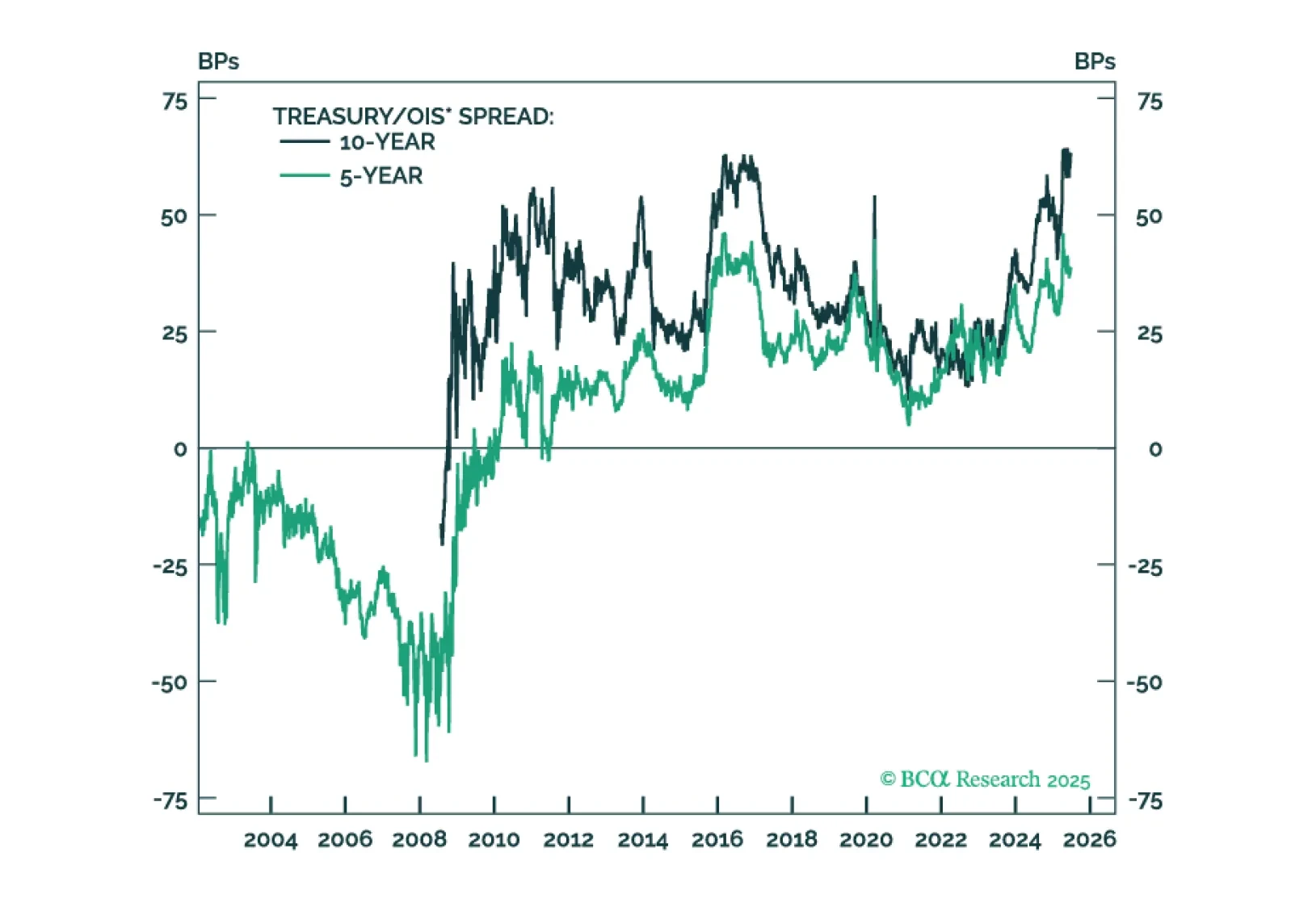

The Treasury/OIS spread has exerted notable upward pressure on Treasury yields during the past year, but the factors driving the spread are now turning more favorable.

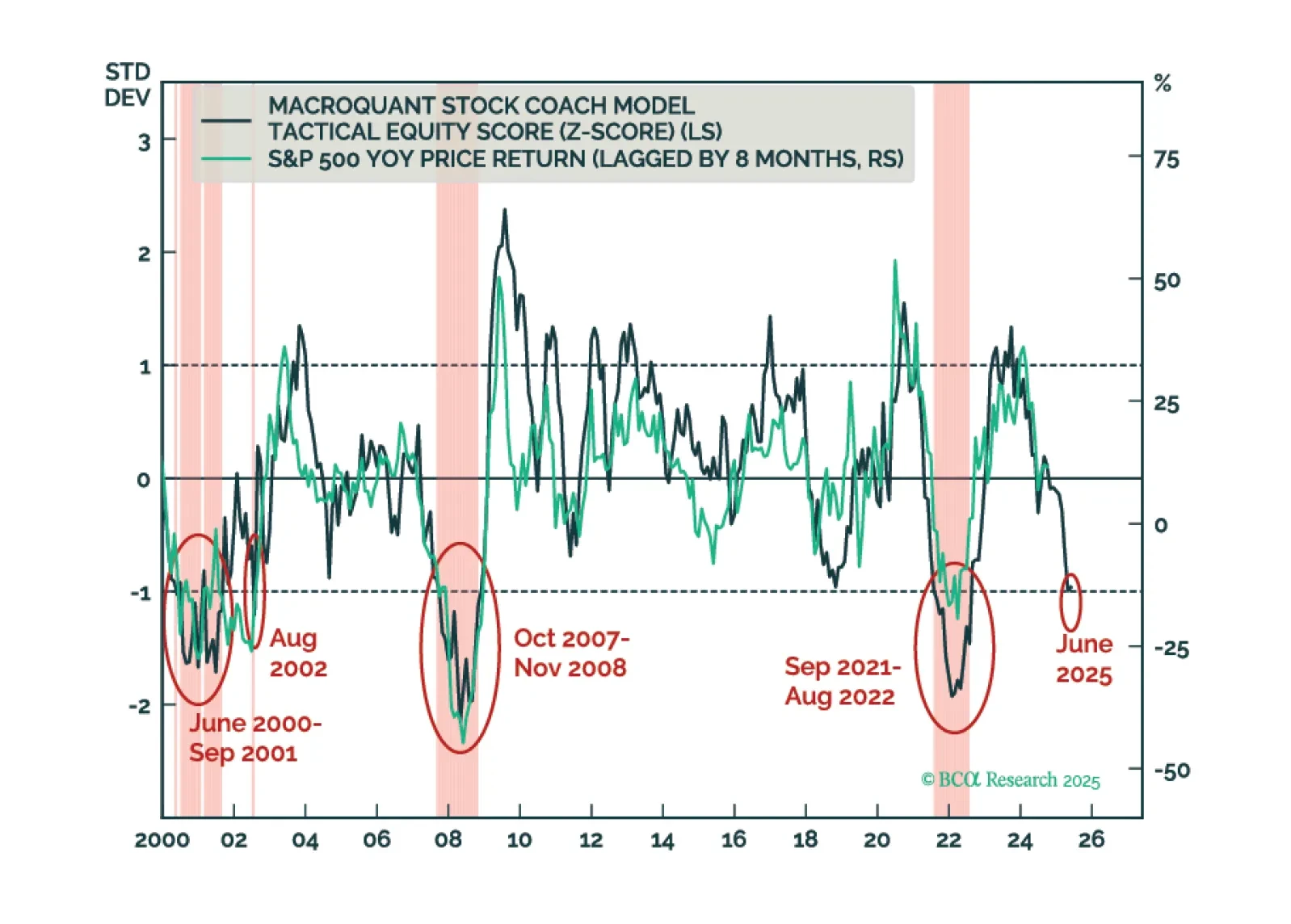

Investors should modestly underweight equities in their portfolios and look to turn more aggressively defensive once the whites of the recession’s eyes are visible. We think that will happen within the next few months.