United States

The Japan-US trade deal removes short-term uncertainty but leaves in place high tariffs. The deal imposes a 15% tariff on most Japanese exports, lower than the previously threatened 25% on autos, and includes Japanese commitments to purchase Boeing aircraft…

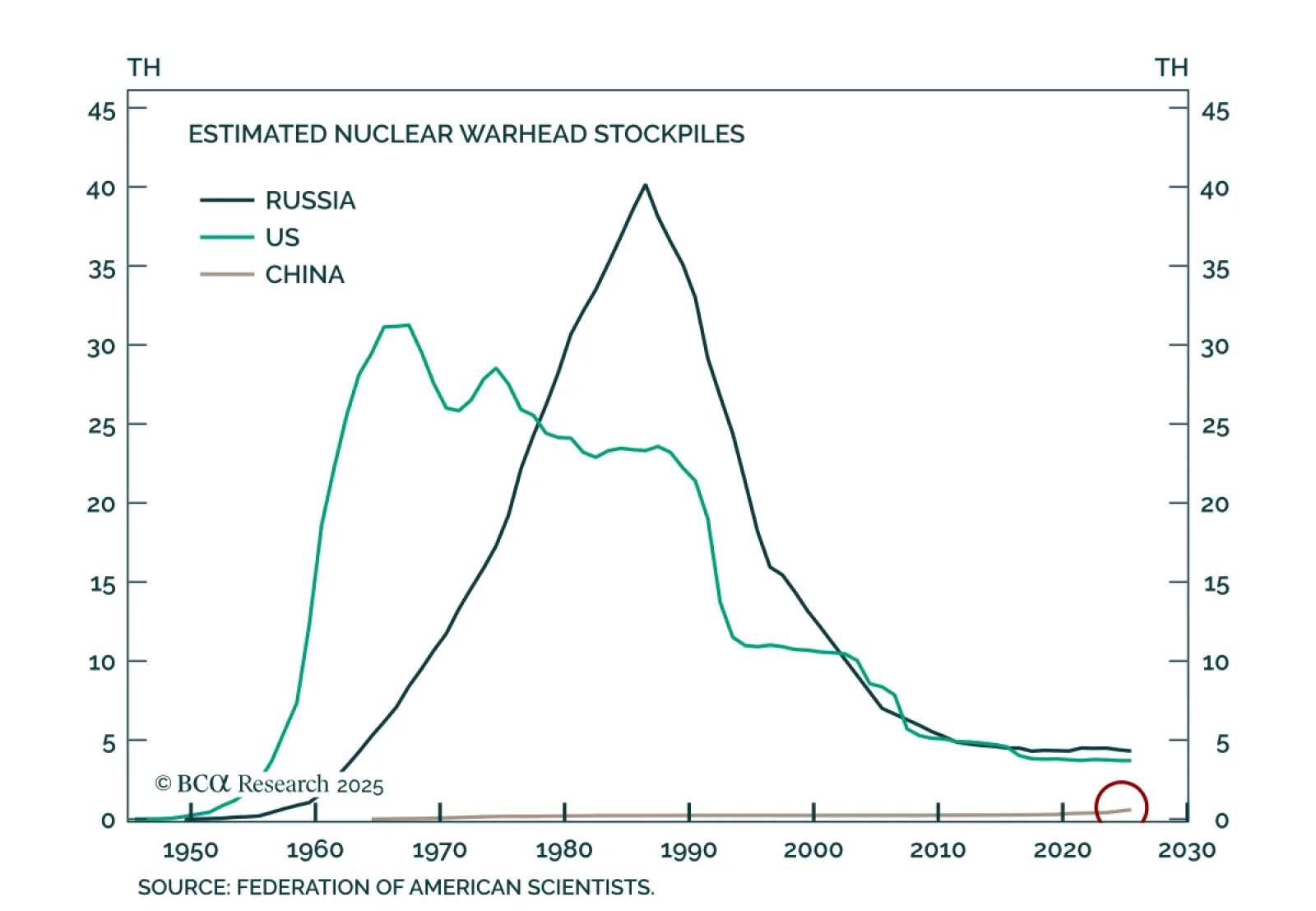

BCA’s Geopolitical strategists advise investors to remain open to the possibility that a new Cold War dynamic is forming in global trade. While the US-China rivalry does not map perfectly onto the original Cold War, the analogy retains analytical value. US…

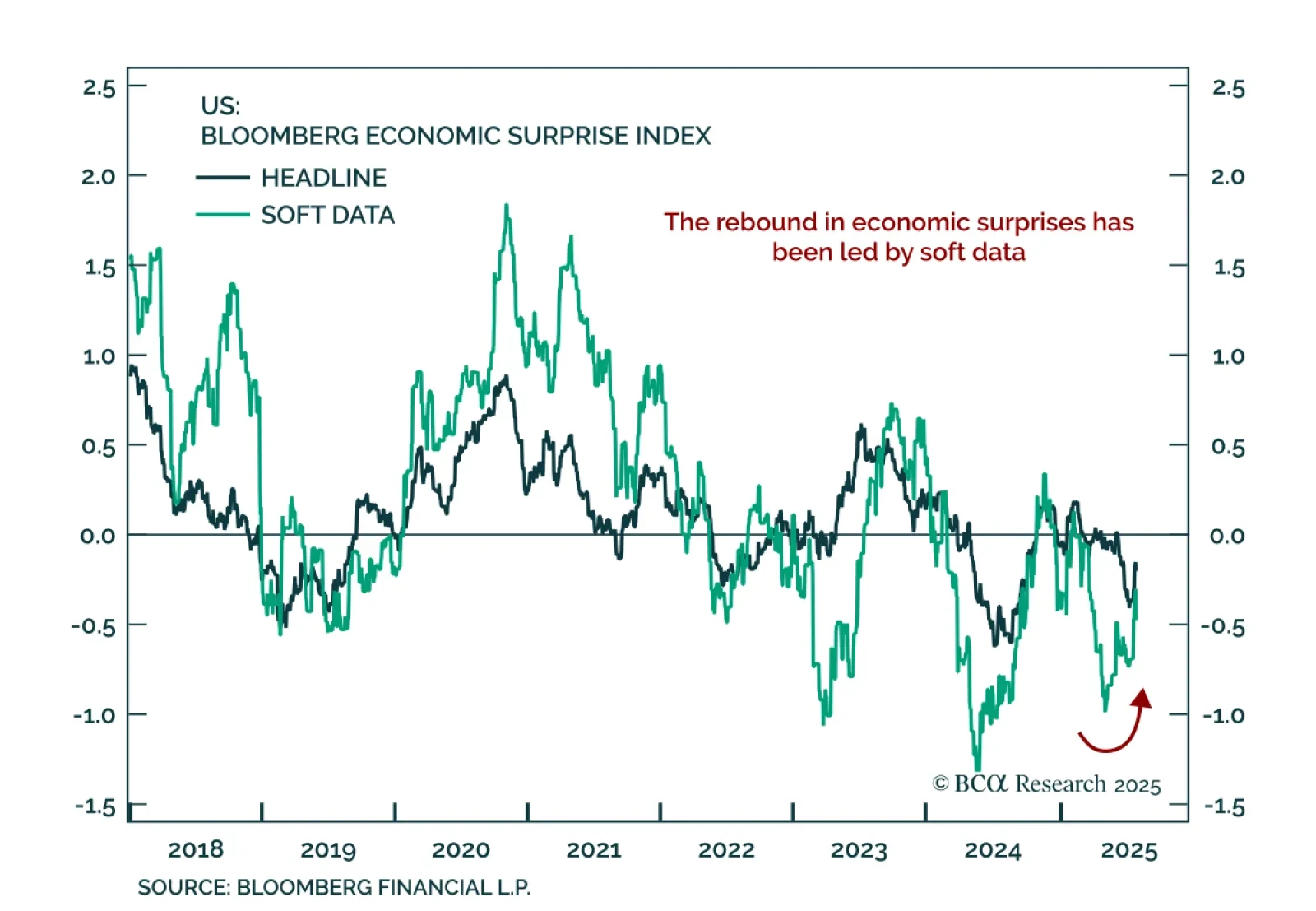

The post-Liberation Day dichotomy between improving soft data and worsening hard data points to an uneven recovery, keeping us positioned for downside risk. Soft data cratered post-Liberation Day as policy uncertainty and market volatility surged, with…

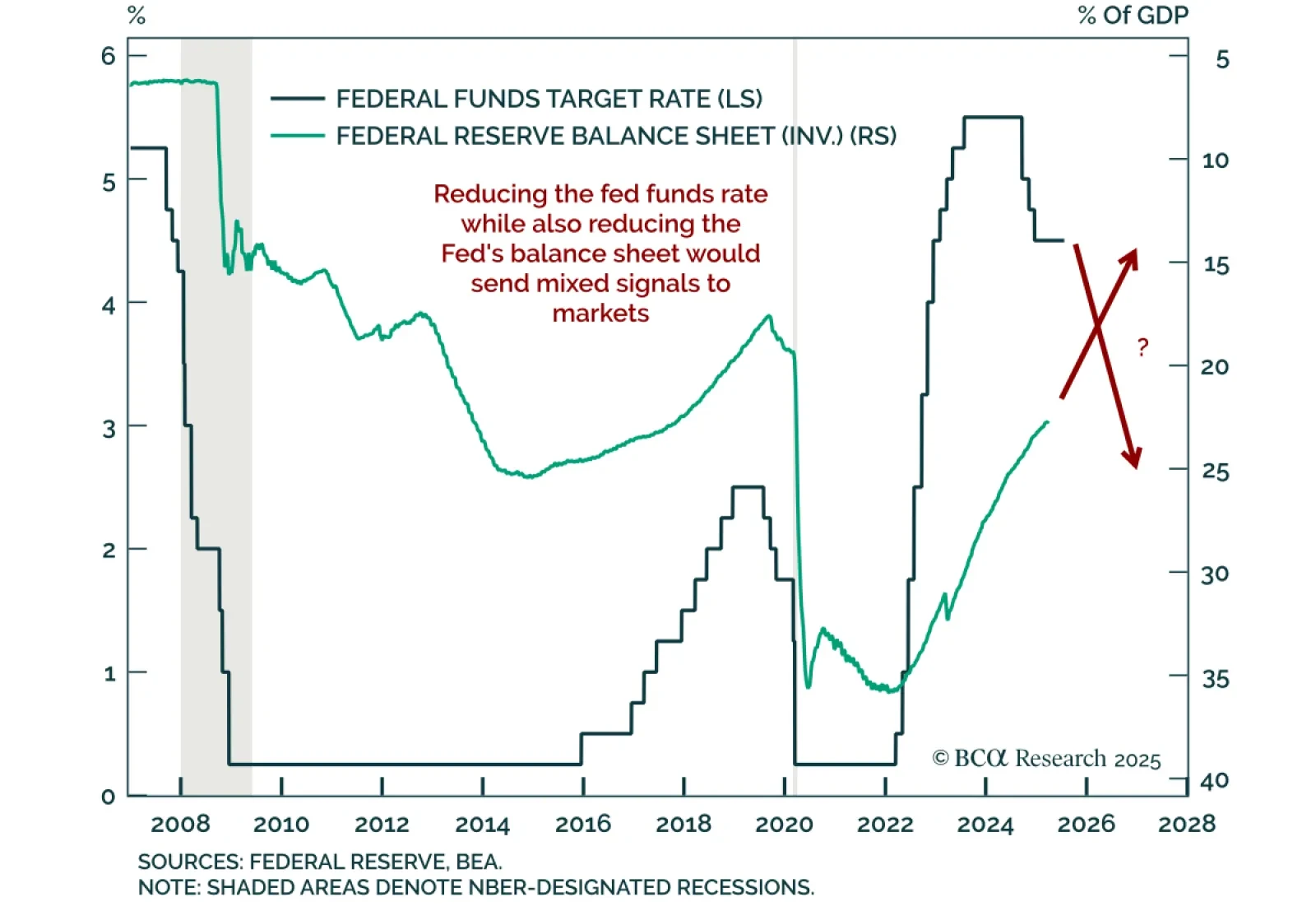

Recent criticism of the Fed centers on post-GFC policy, but proposed solutions would risk policy incoherence and higher long-end yields. Criticism covers the Fed’s reliance on balance sheet policies aimed at easing financial conditions after hitting the…

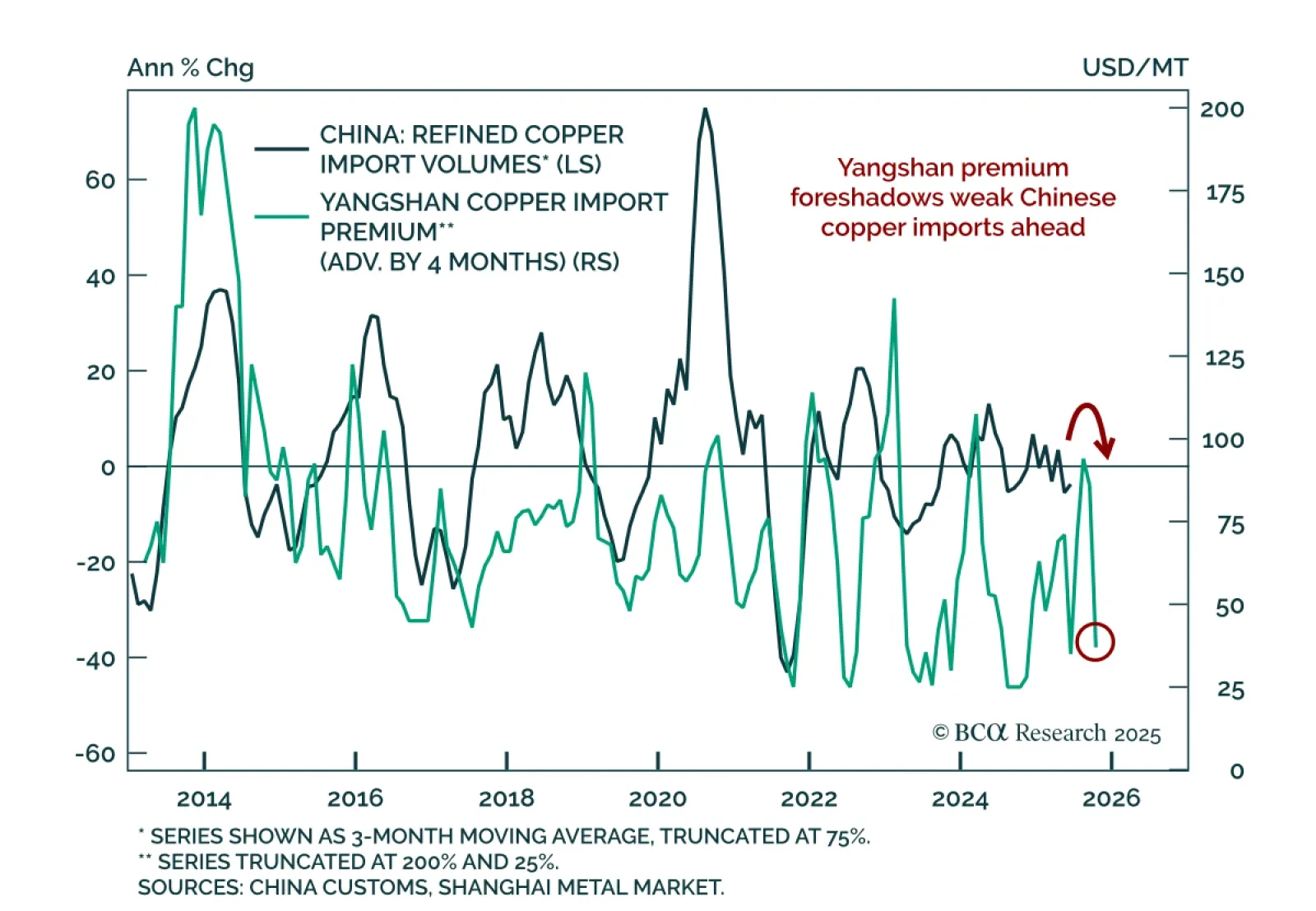

BCA’s Commodity strategists remain long gold/short LME copper and have initiated an outright short in LME copper as a cyclical trade. The US copper tariff will redirect supply away from the US, replenishing depleted inventories elsewhere and exerting downward…

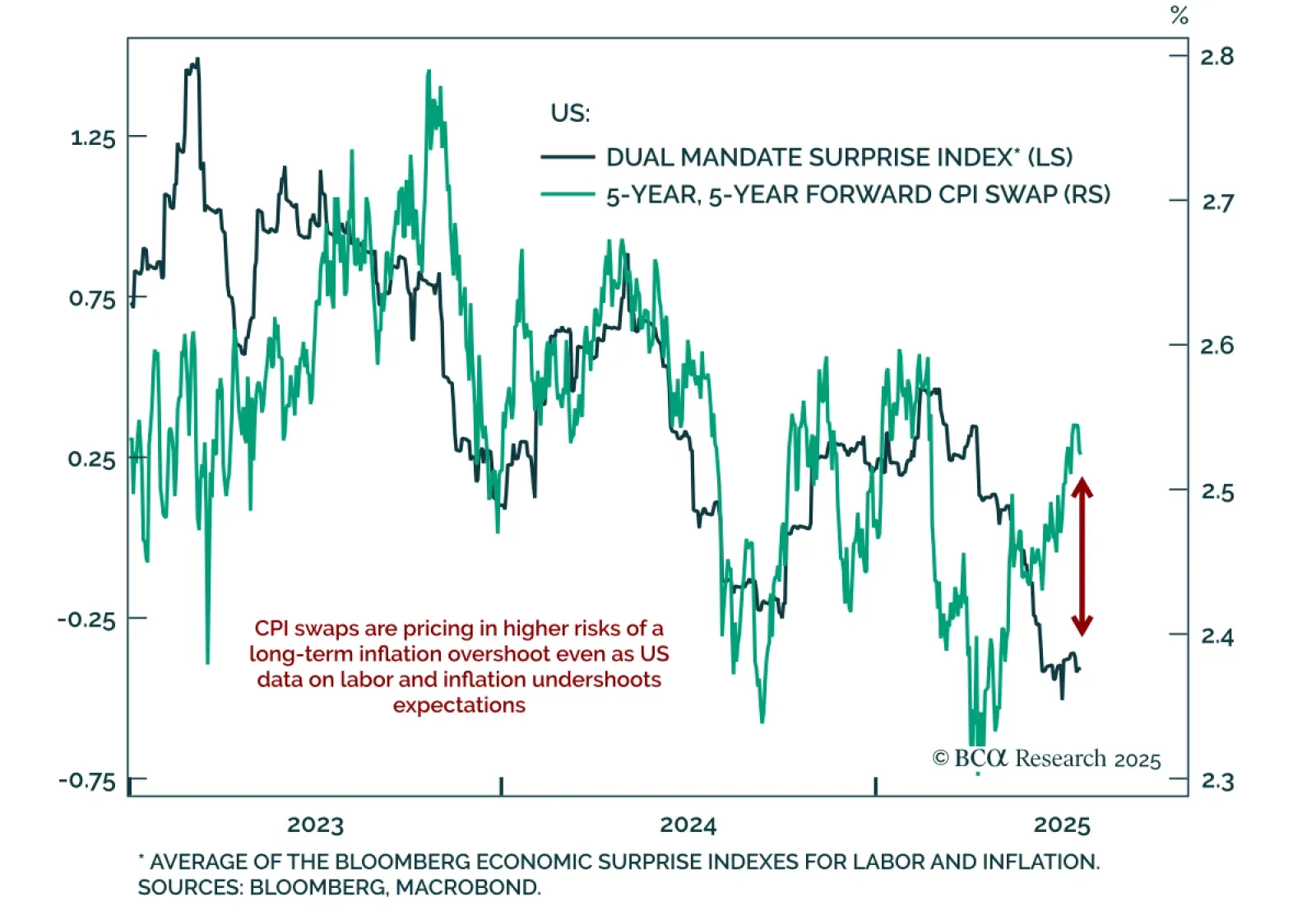

Rising political pressure on the Fed risks undermining policy credibility, risking a de-anchoring of long-term inflation expectations. The Trump administration keeps escalating attacks on Fed Chair Powell. While the Fed cannot ease proactively amid…

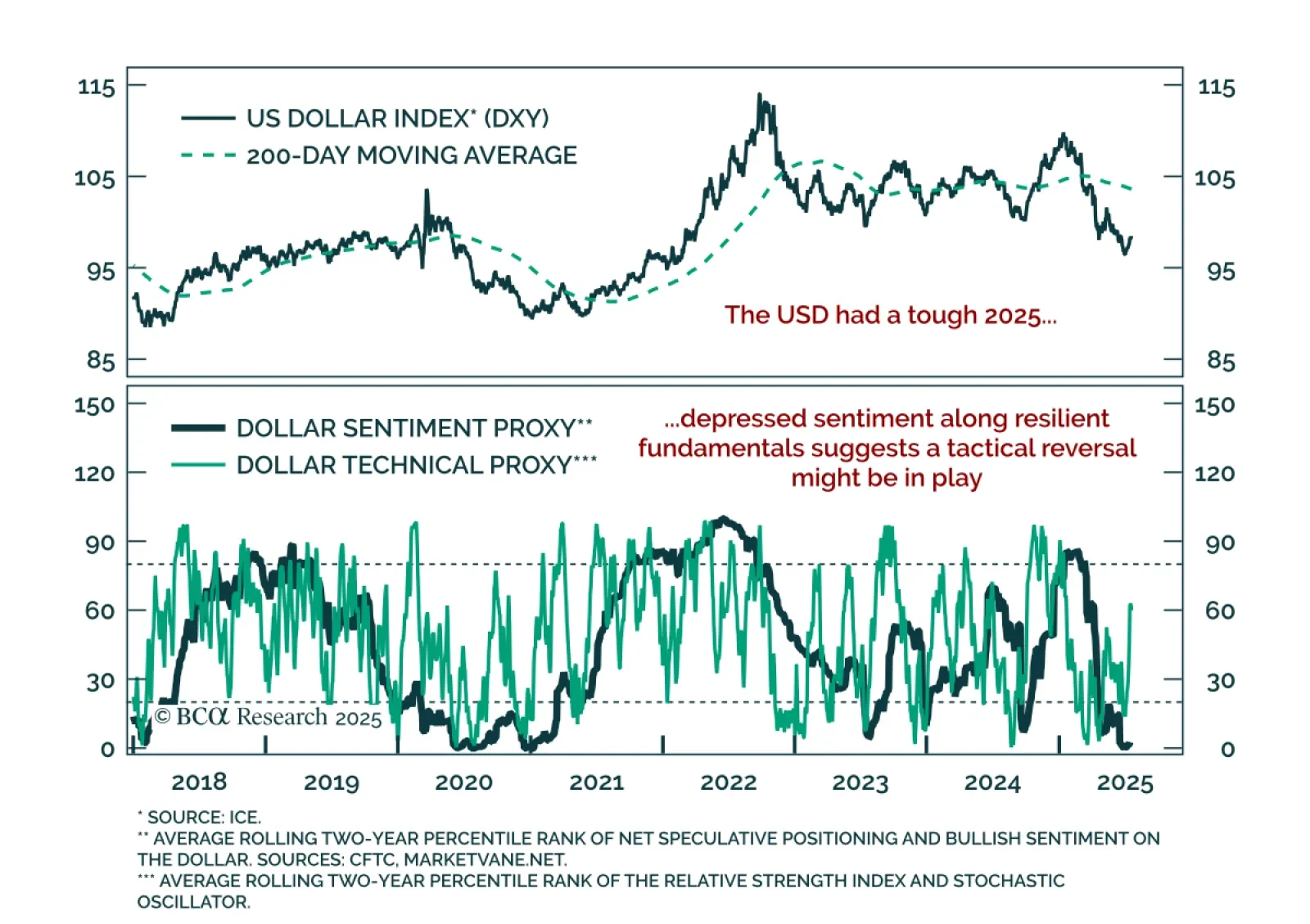

The USD remains structurally challenged, but near-term tactical conditions suggest a temporary bottom is in place. After a sustained selloff and rising concerns around its reserve status, the dollar has decoupled from rate differentials, a behavior more…

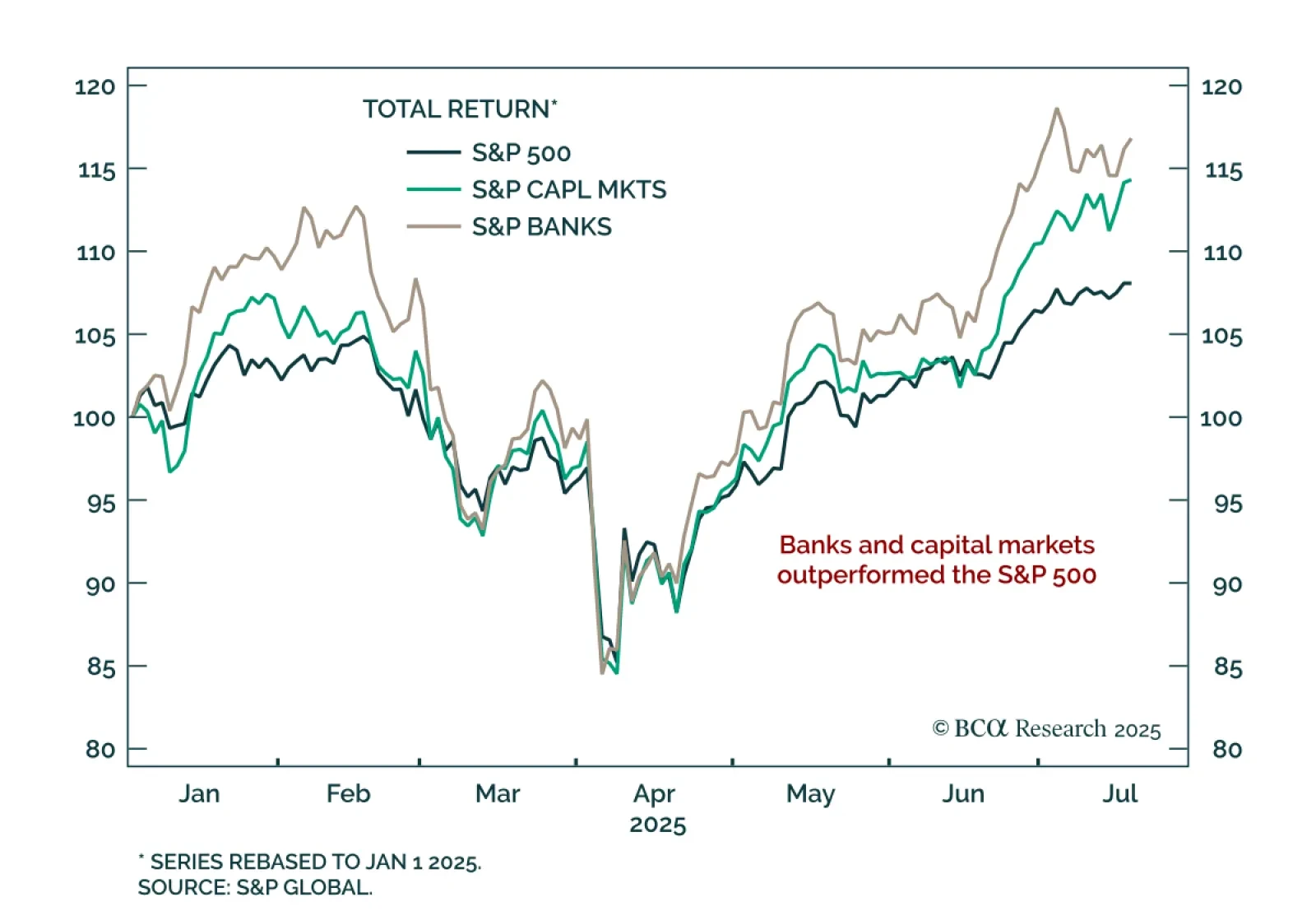

BCA’s US Equity strategists reiterate their overweight stance on Banks and Diversified Financials. Q2 results were solid, with resilient consumer strength and a rebound in capital markets activity. Net interest margins are stabilizing, and modest loan…

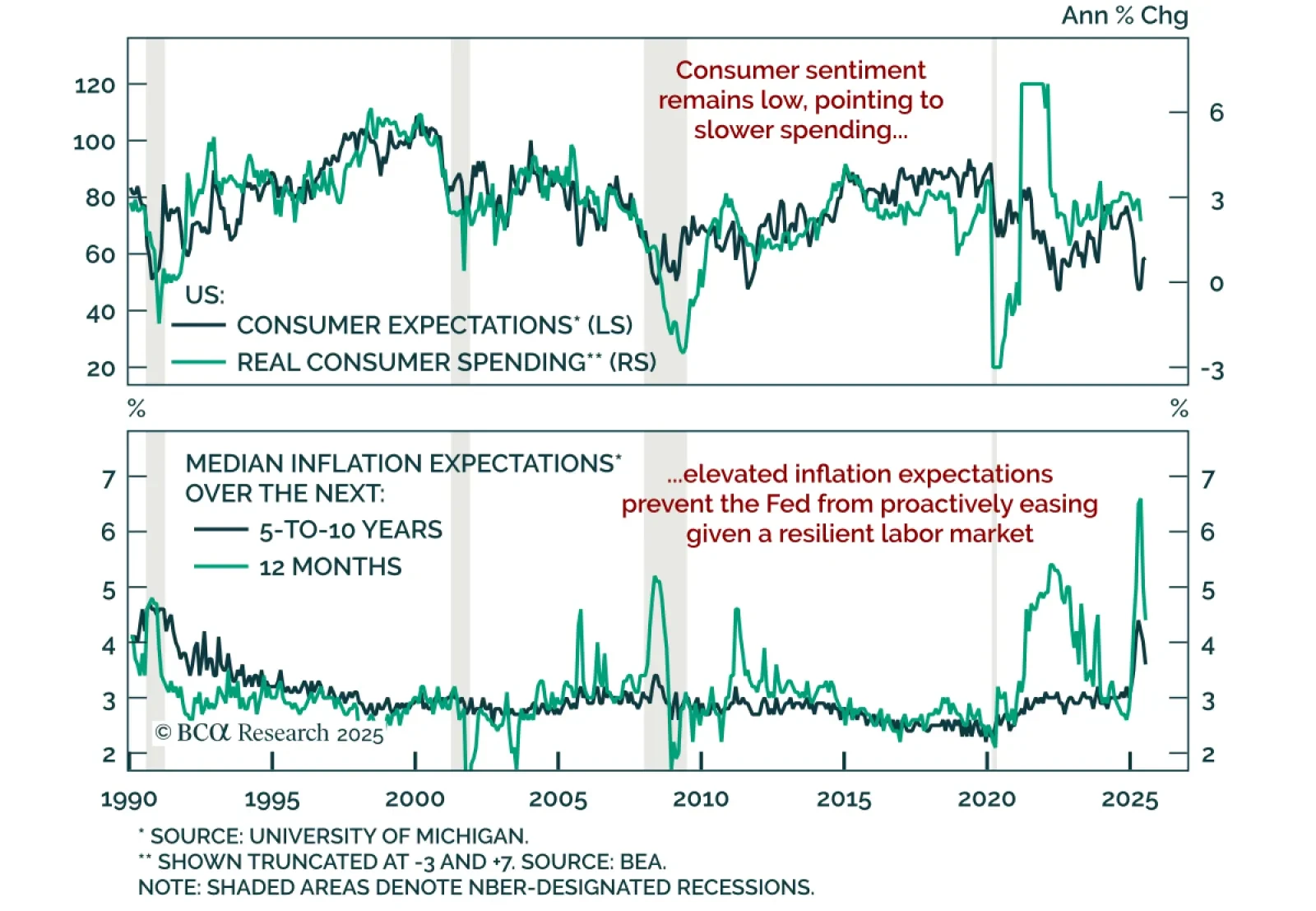

Consumer sentiment improved modestly in July, but remains at levels that still point to subdued spending, reinforcing our defensive stance. The preliminary University of Michigan index rose to 61.8 from 60.7 in June. Expectations edged up to 58.6, while…

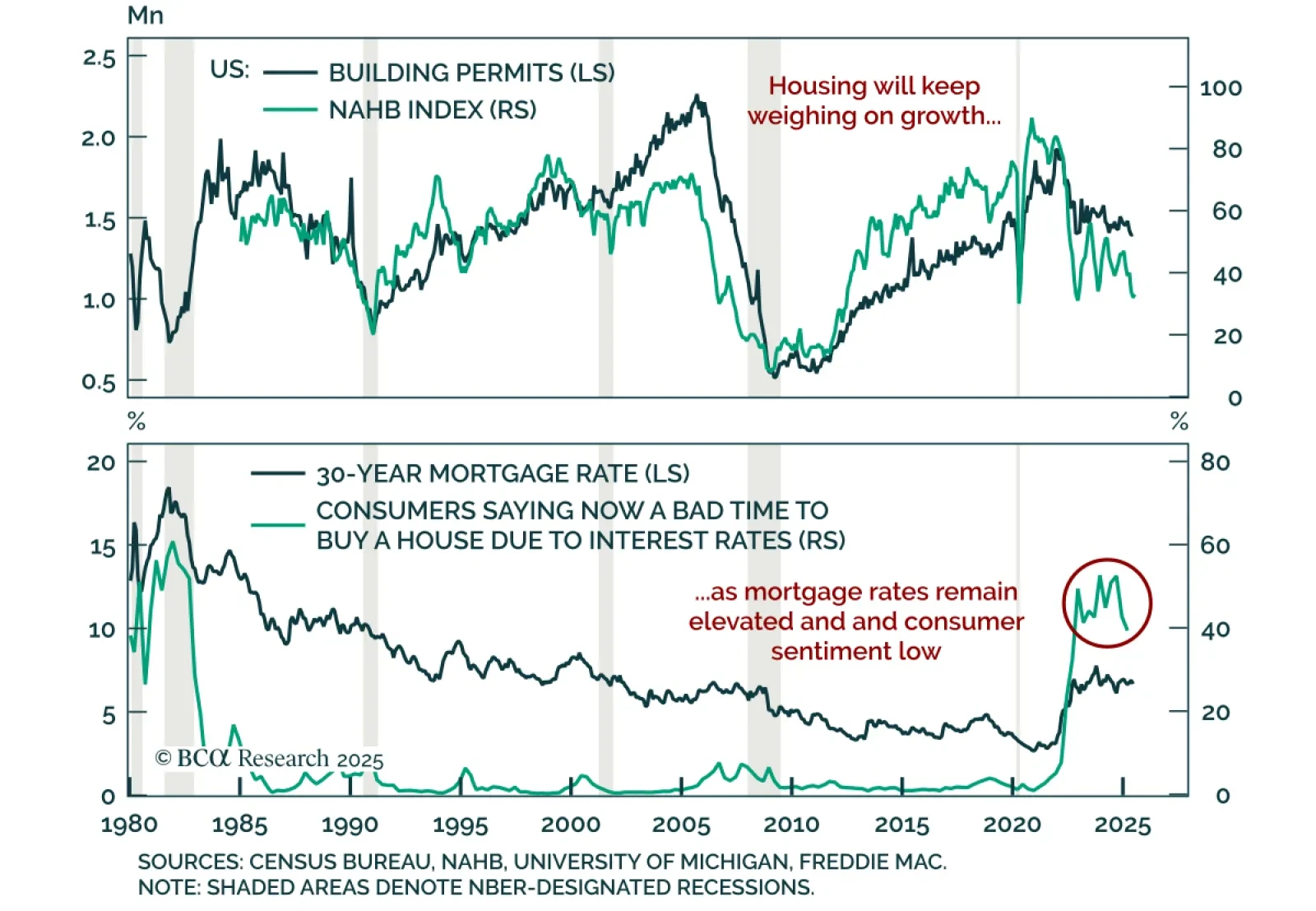

June US housing data surprised to the upside, but the broader sector is still weak, reinforcing our modest underweight on equities. Housing starts rose an annualized 4.6% m/m, and building permits ticked up 0.2% after a 2.0% decline in May. Gains were…