United States

The president did not announce significant new tax cuts or economic stimulus.

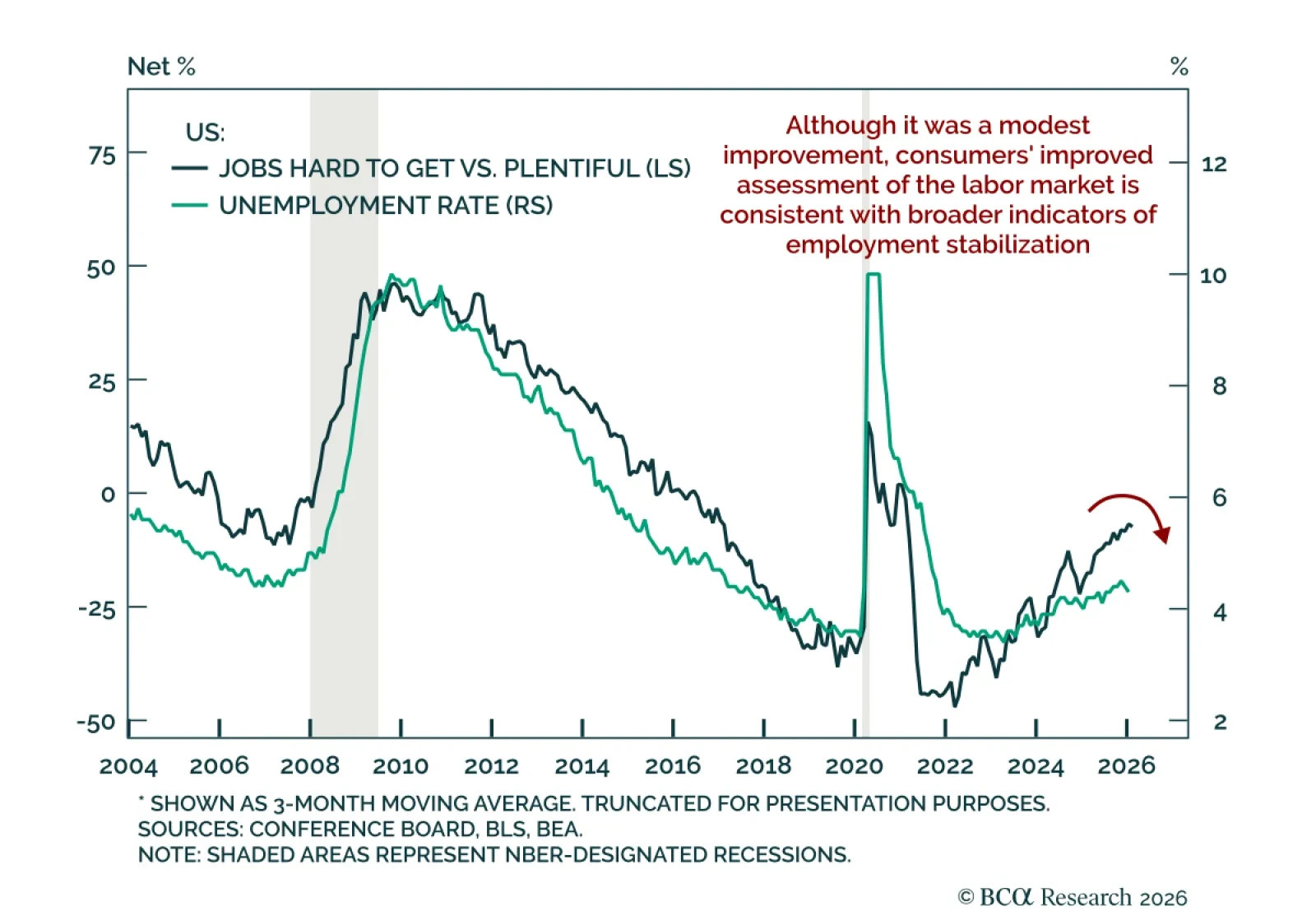

The February Conference Board survey suggests improving labor-market perceptions, consistent with stabilizing growth momentum. The headline index rose to 91.2 from an upwardly revised 89.0 in January, beating estimates. Both present conditions and…

Easing US financial conditions reinforce near-term US data strength. US data has exceeded expectations since the start of the year, with positive economic surprises accelerating. At the same time, financial conditions have eased, as reflected in our proxy…

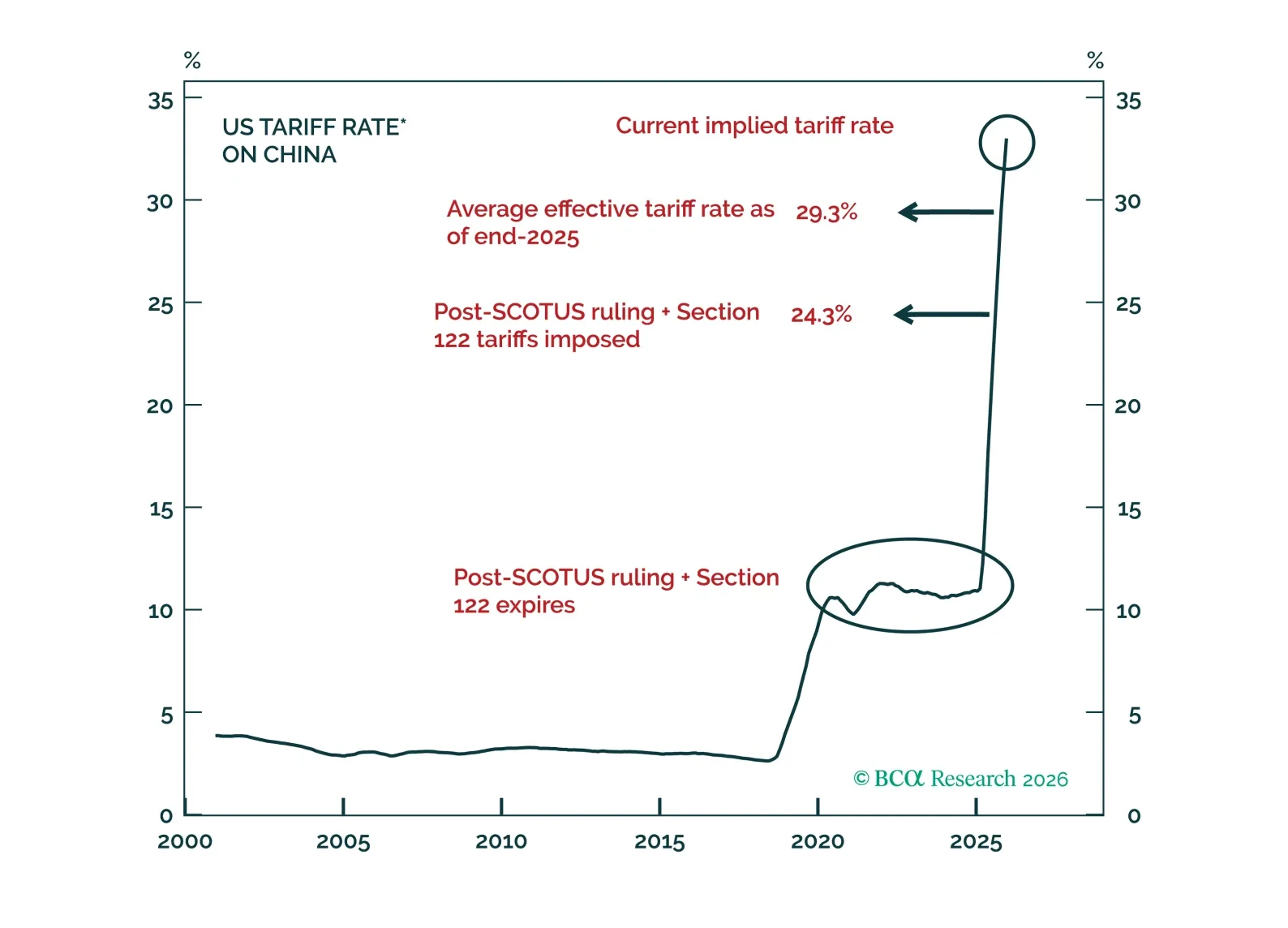

This report examines the implications for Chinese exports and global trade in light of the US Supreme Court’s ruling on tariffs.

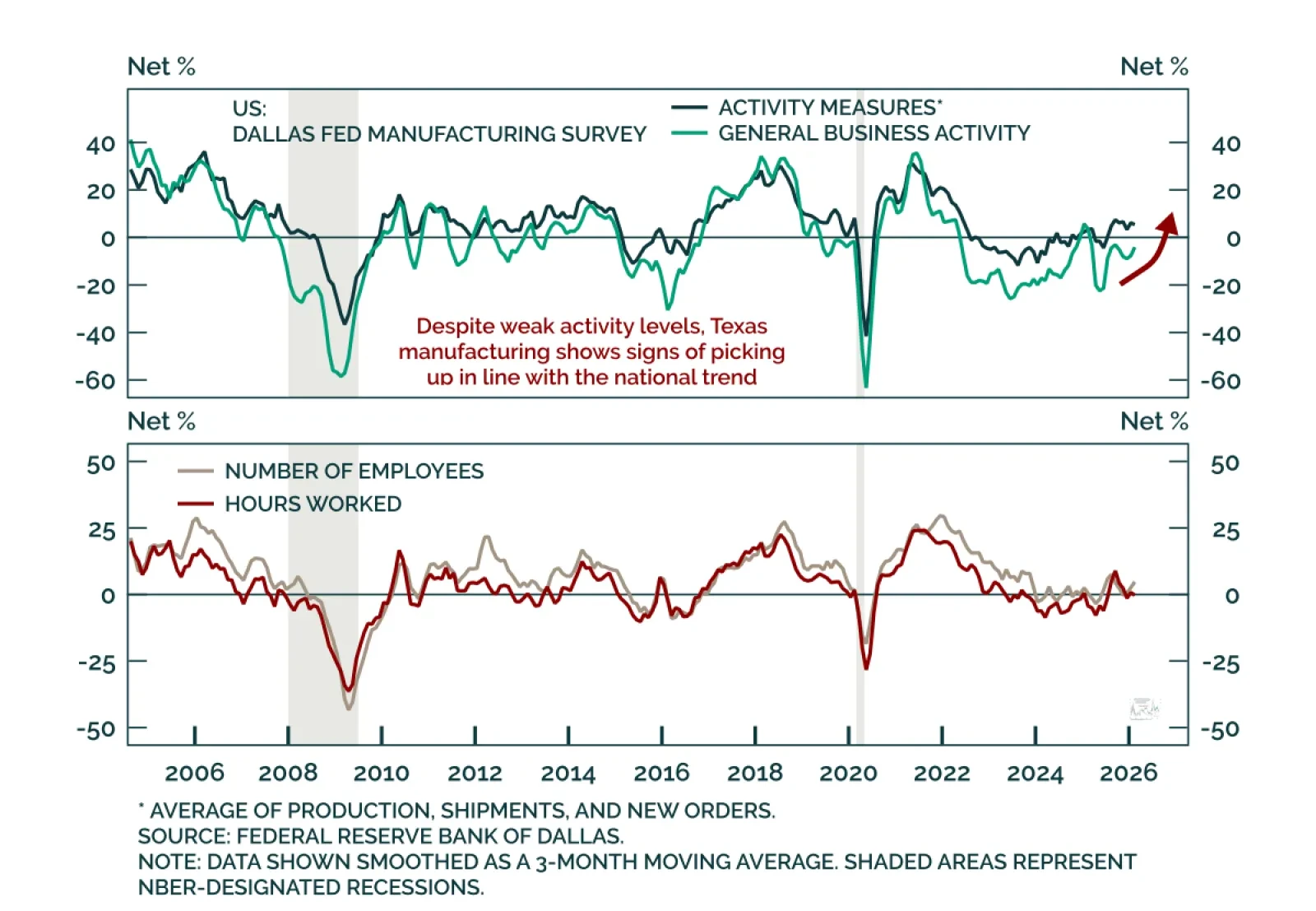

The Dallas Fed survey points to strengthening manufacturing activity alongside moderating price pressures. The headline index rose to 0.2 from -1.2, beating estimates and marking the strongest reading since July 2025, though still at a low level. The index…

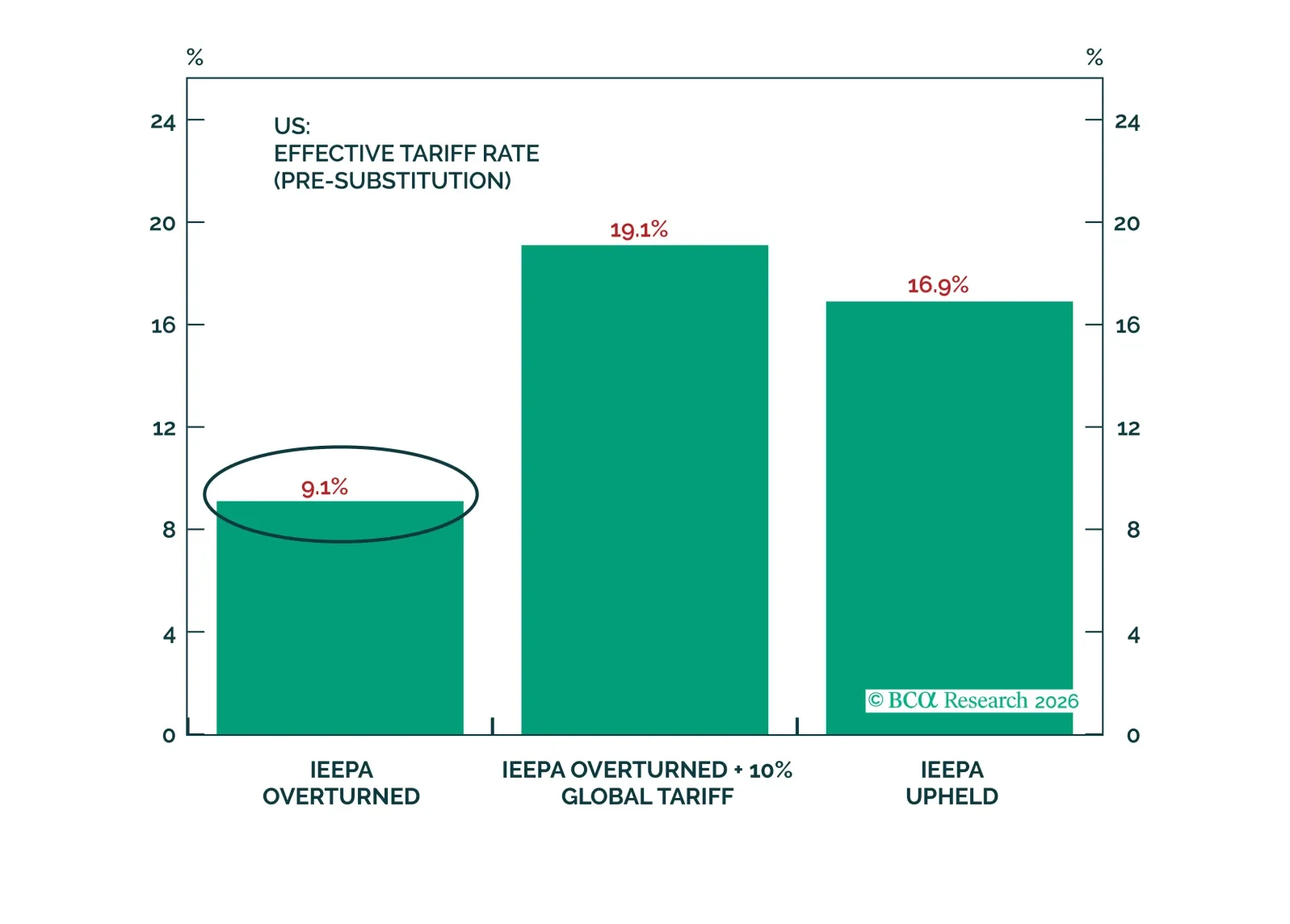

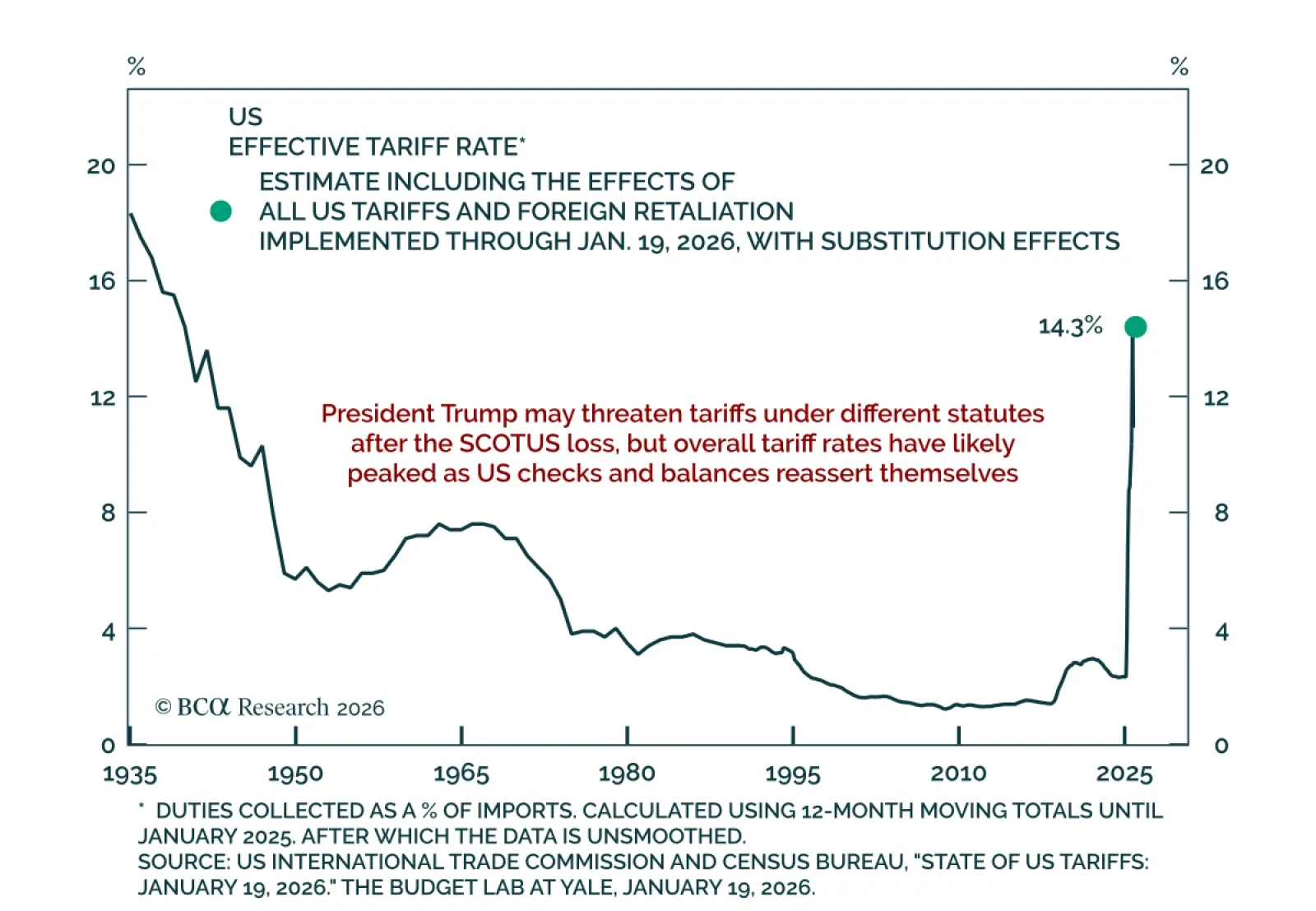

President Trump announced a new 15% tariff under Section 122 following the Supreme Court’s strike-down of tariffs imposed under the IEEPA statute. Despite the ruling, Sections 232 and 301 remain available and are not time-limited, preserving significant…

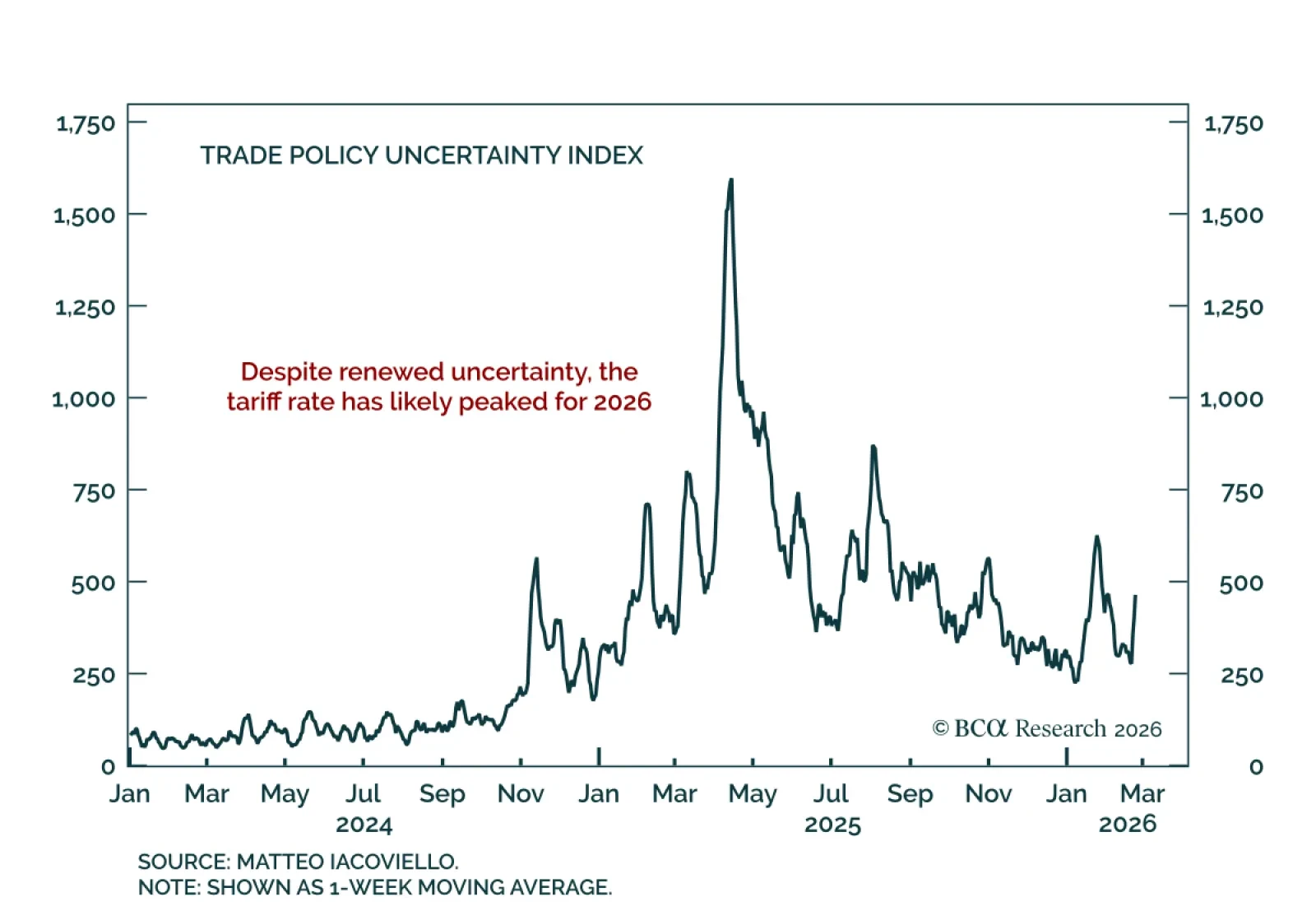

Trump is saving face with new tariffs but will avoid any major new tariff shock until 2027. For now, Iran risk will overshadow tariff volatility.

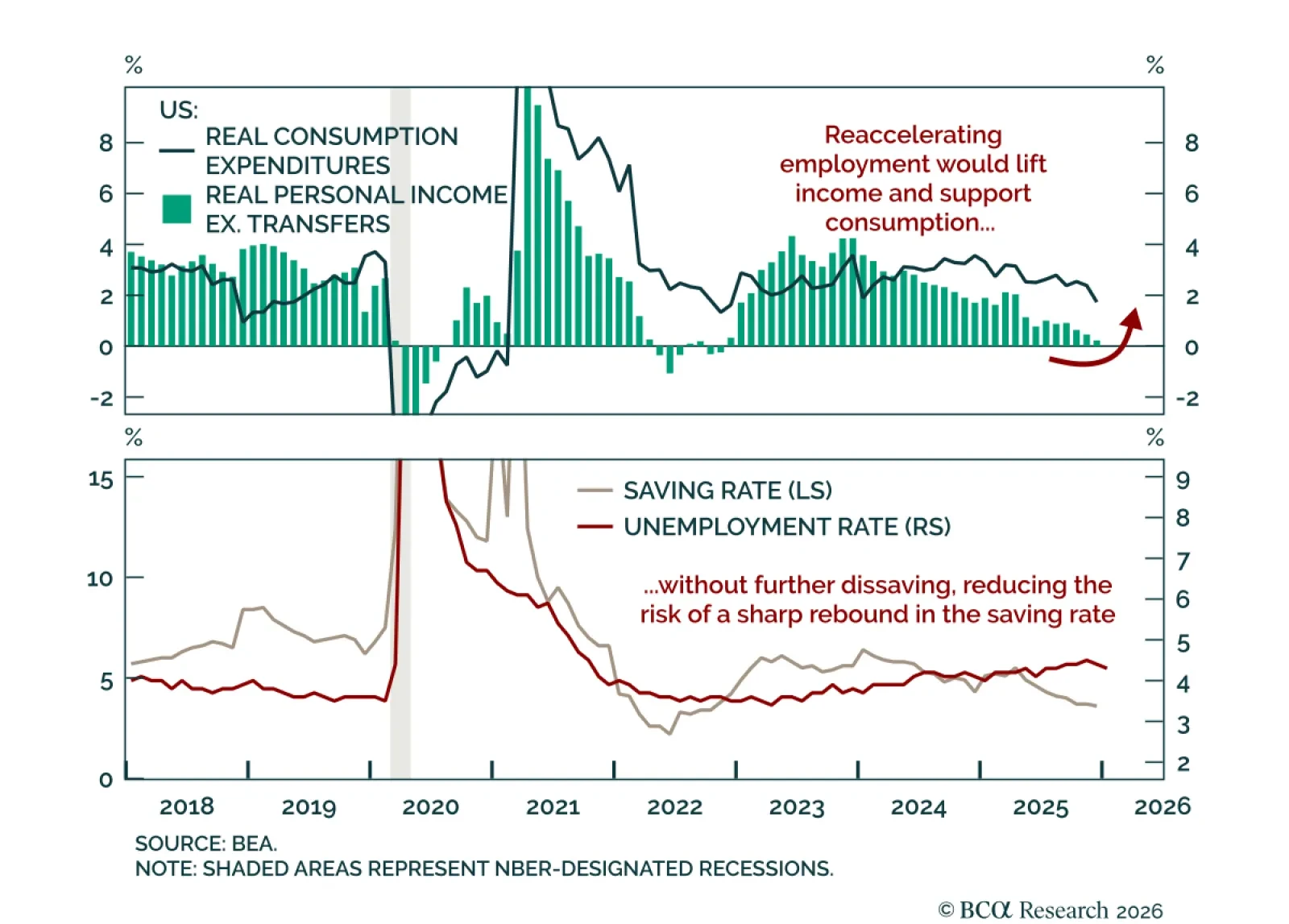

The December US Personal Income and Outlays report sent mixed signals. Real consumption slowed to 0.1% m/m from 0.2% in November, in line with expectations, while real income excluding transfers fell 0.1%. Spending was supported by dissaving, with the saving…

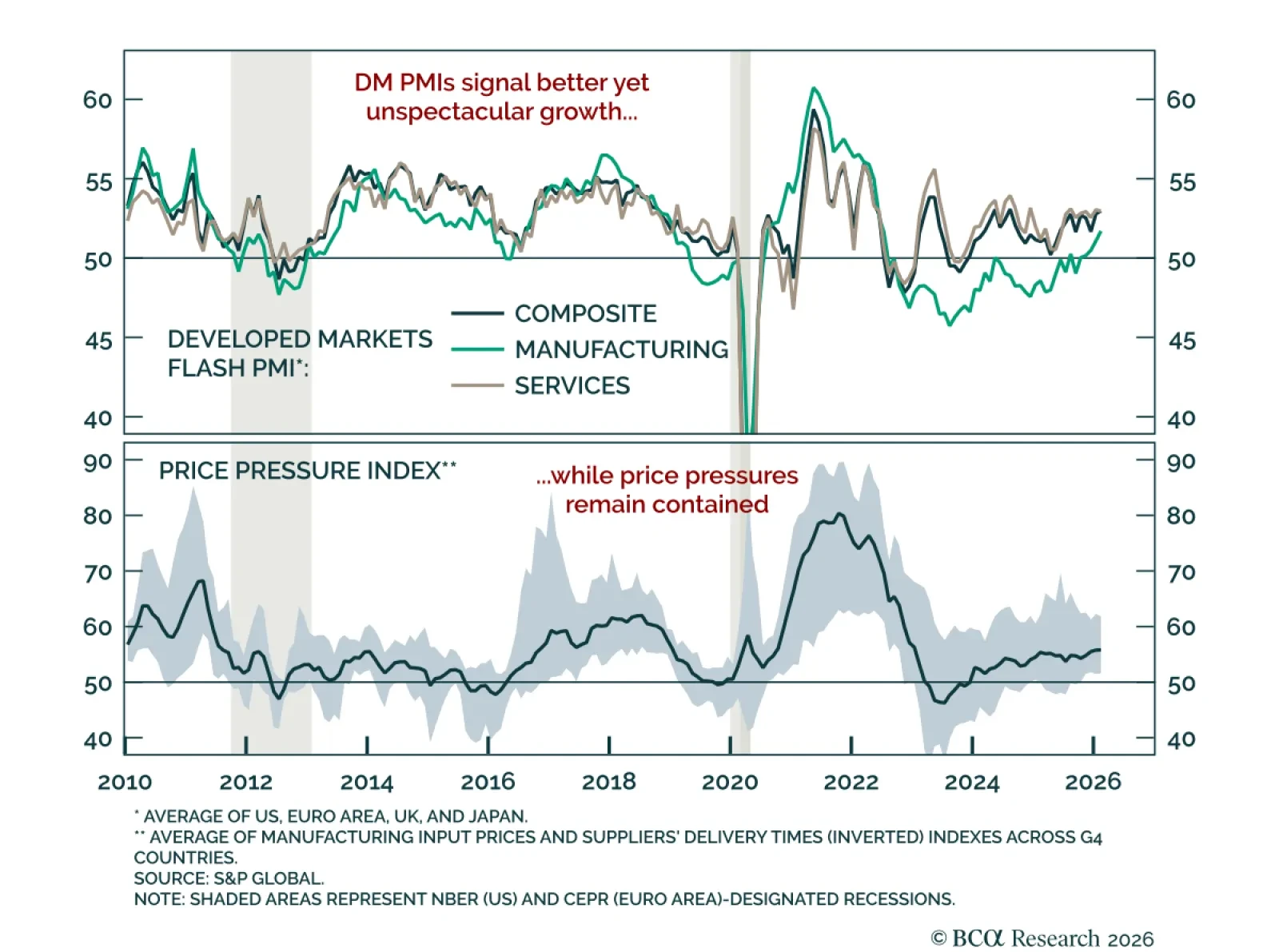

February flash PMIs edged higher, pointing to gradual improvement in global growth. After moving mostly sideways through 2025, developed markets PMIs are picking up. Manufacturing is showing decent momentum, rebounding after being weighed down by trade…

US checks and balances are still in place. The Supreme Court ruled against the Trump administration's use of sweeping tariffs under the International Emergency Economic Powers Act (IEEPA). Our US and Geopolitical strategists see different implications for the…