United States

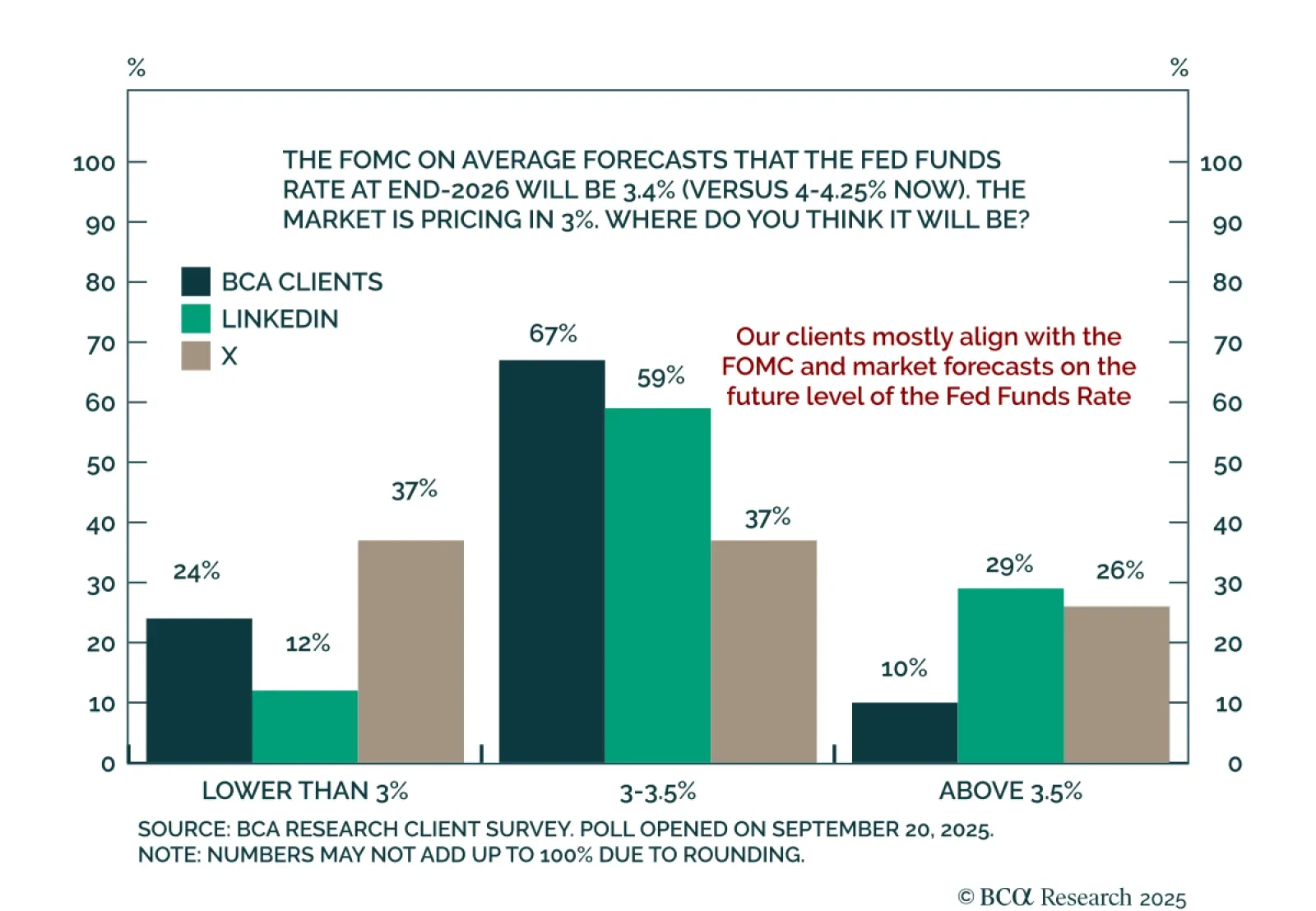

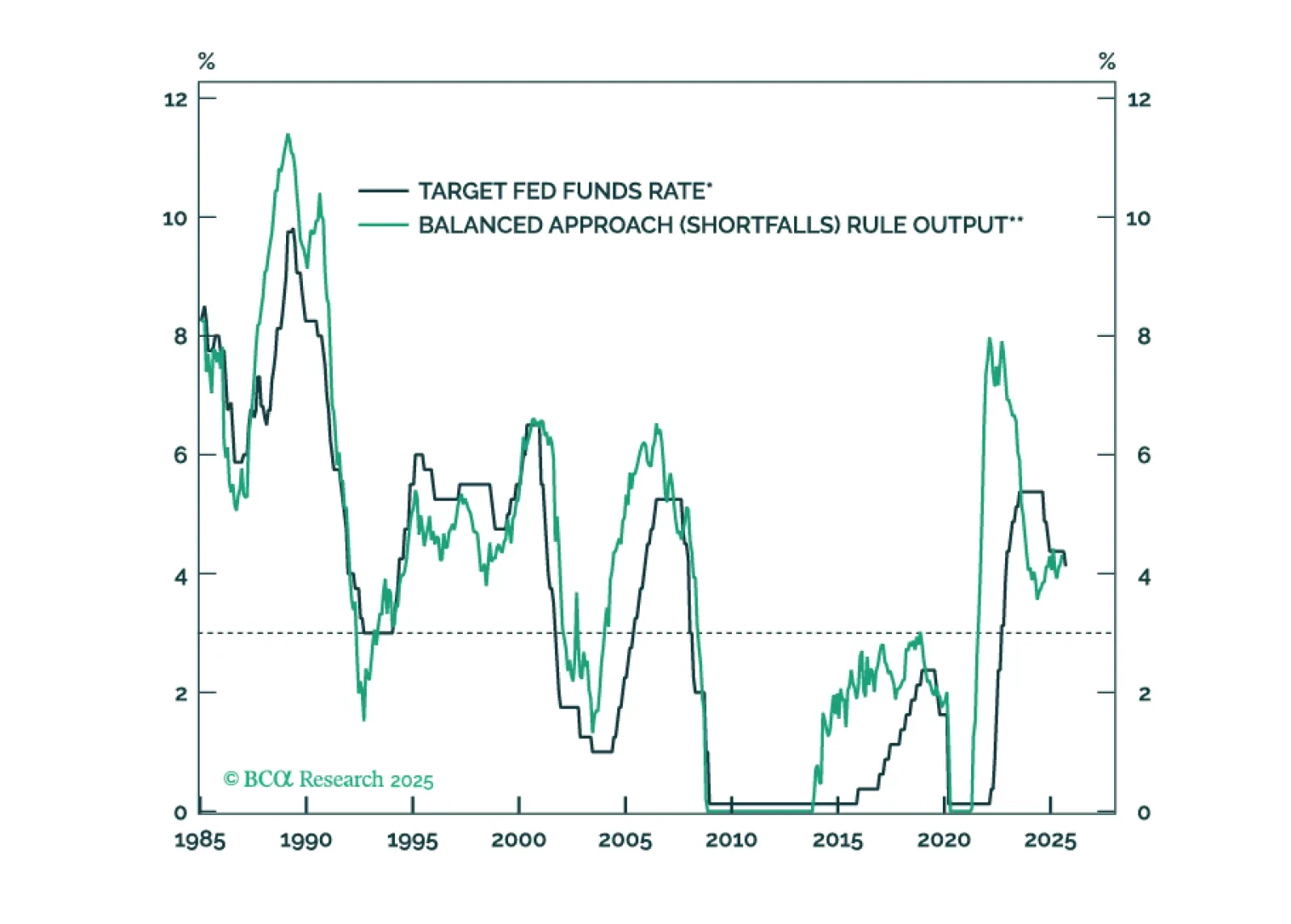

BCA clients see the FOMC cutting the fed funds rate to 3-3.5% by the end of next year, compared to 4-4.25% now, and the FOMC’s own median forecast of 3.4%. In the latest weekly edition of our Have Your Say client poll, 67% of respondents voted for…

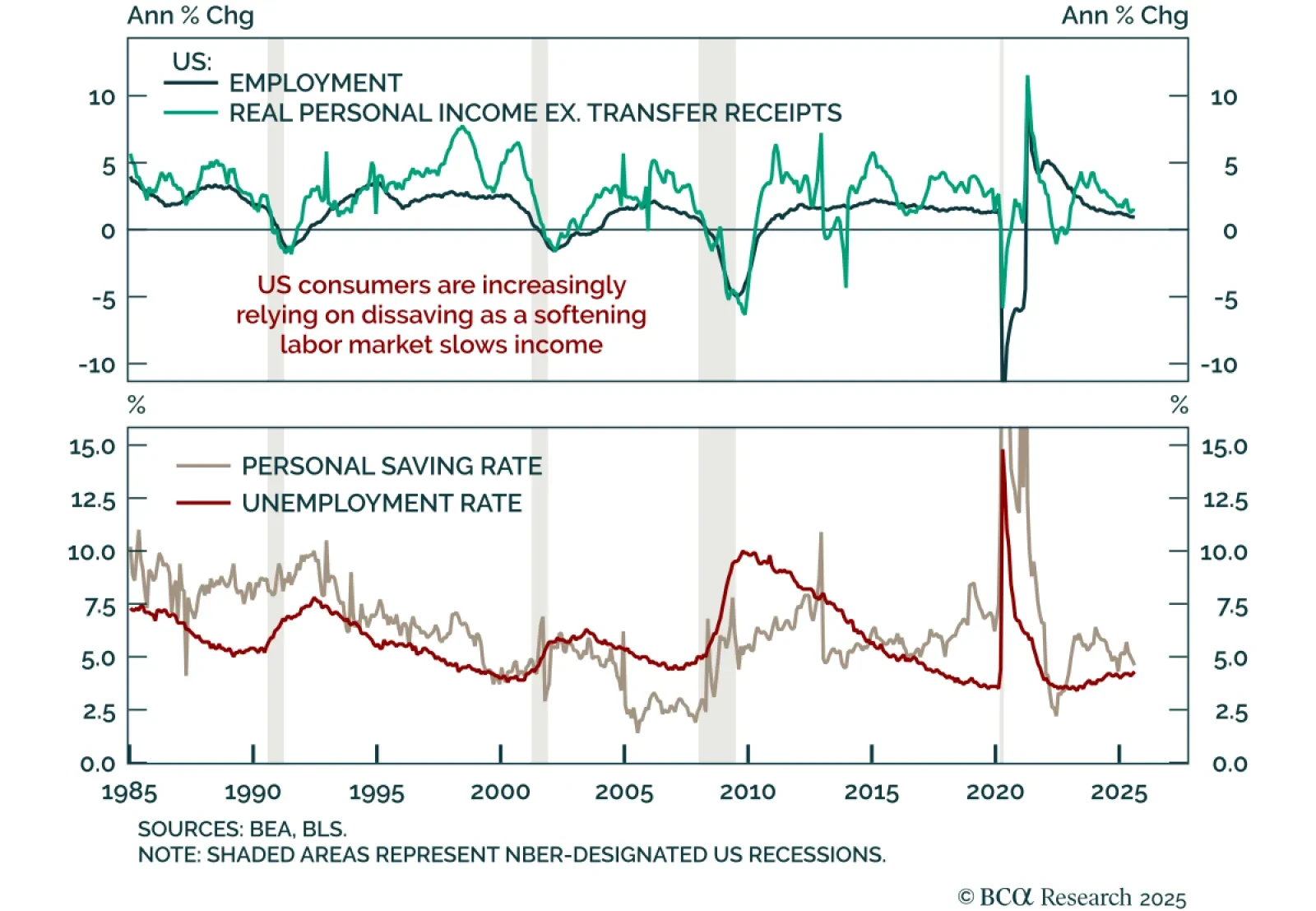

September consumption and income data beat estimates, showing a resilient US consumer but leaving the outlook fragile. Personal spending rose 0.6% m/m, outpacing income at 0.4%, pushing the saving rate down to 4.6%, its lowest level this year. Adjusted for…

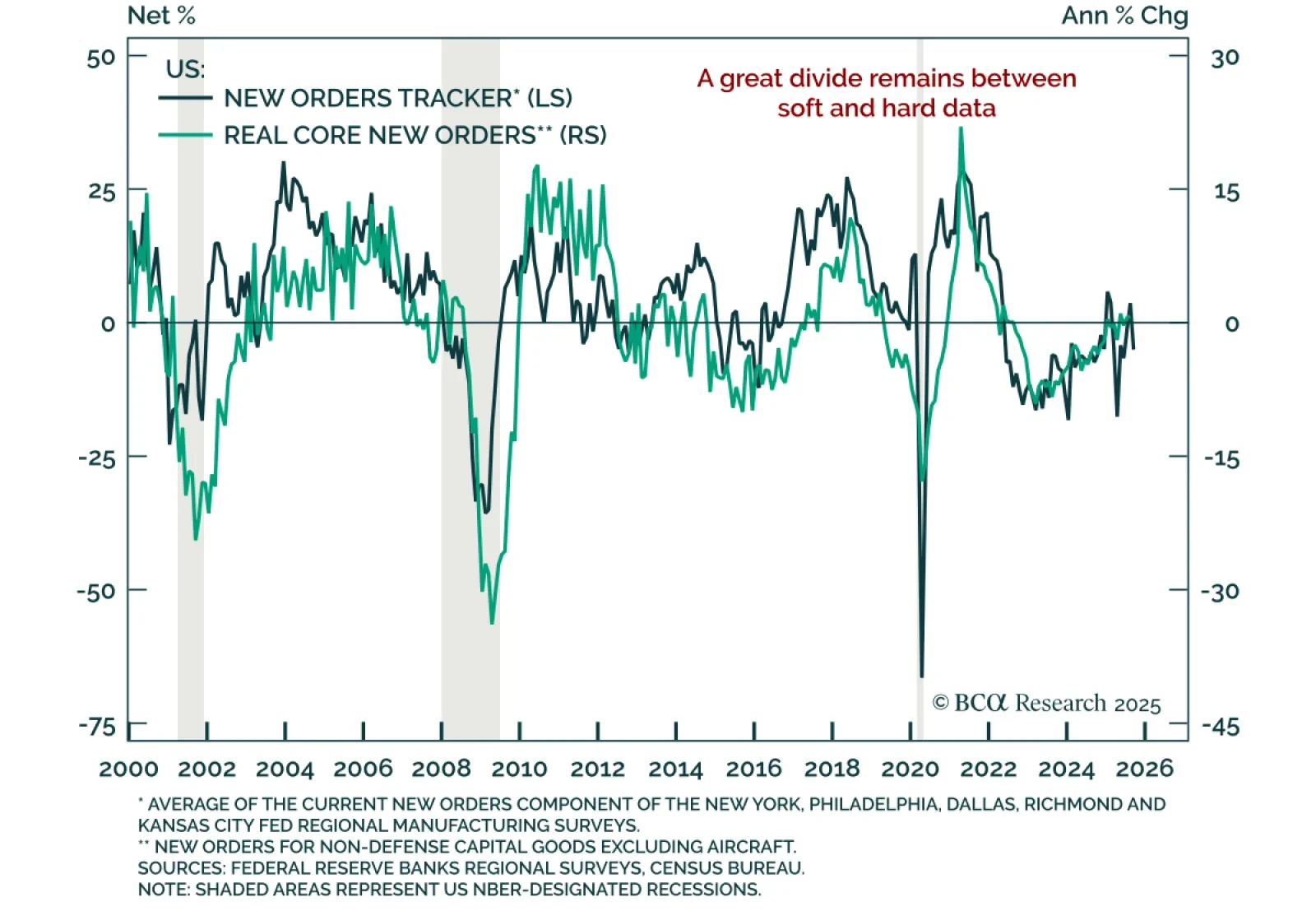

August core durable goods orders beat estimates, but weak shipments and survey data reinforce our modestly defensive stance. Core orders rose 0.6% m/m against expectations of a modest decline, though they decelerated from July’s downwardly revised 0.8% gain.…

Our tactical framework, which tracks the reflexive loop between financial conditions and economic surprises, points to stronger near-term growth, leaving equities vulnerable if inflation re-accelerates. Data surprises move markets, while bond yields and the…

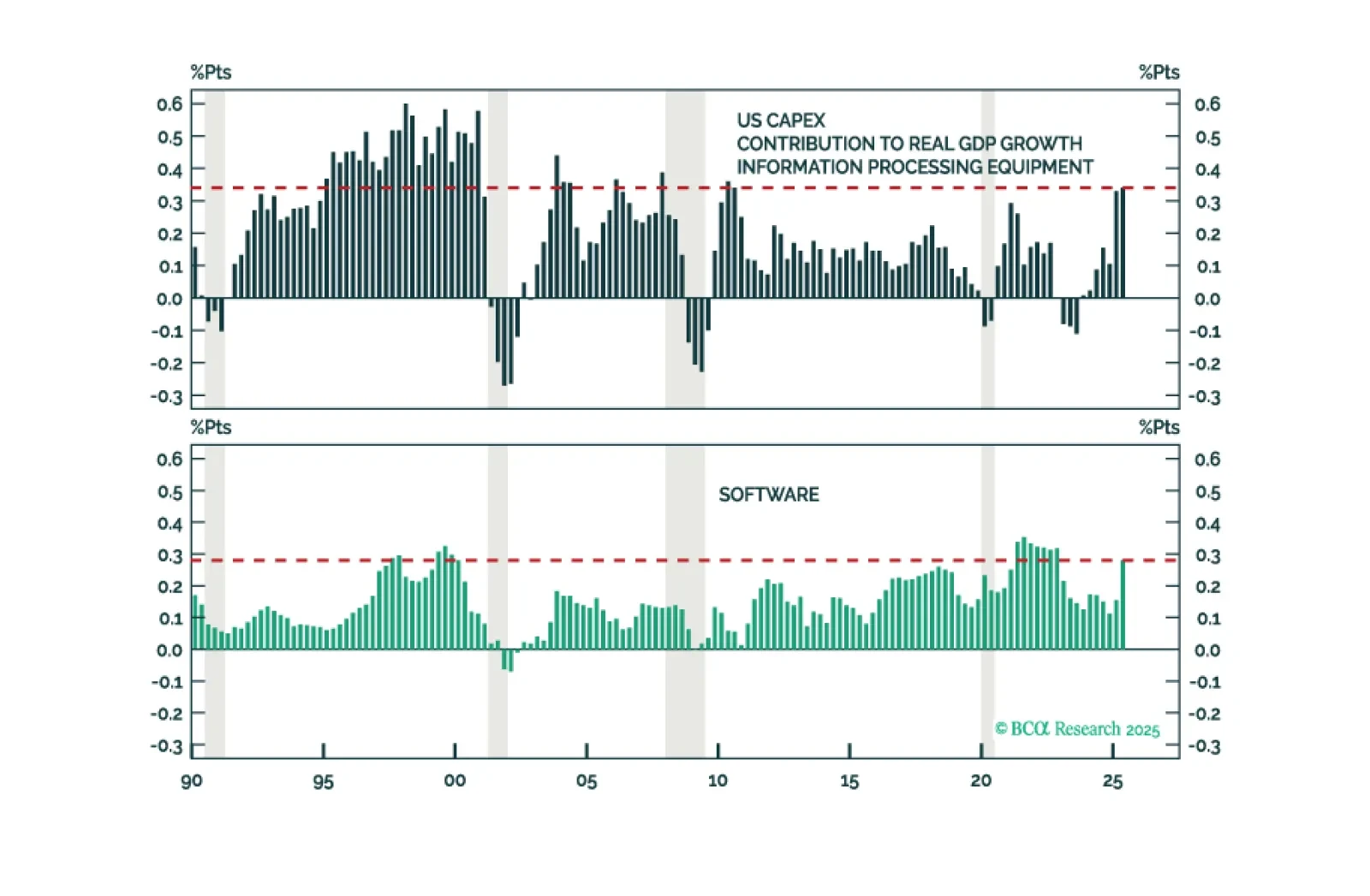

The AI capex boom is having a measurable impact on the economy but, so far, it is more muted than often cited.

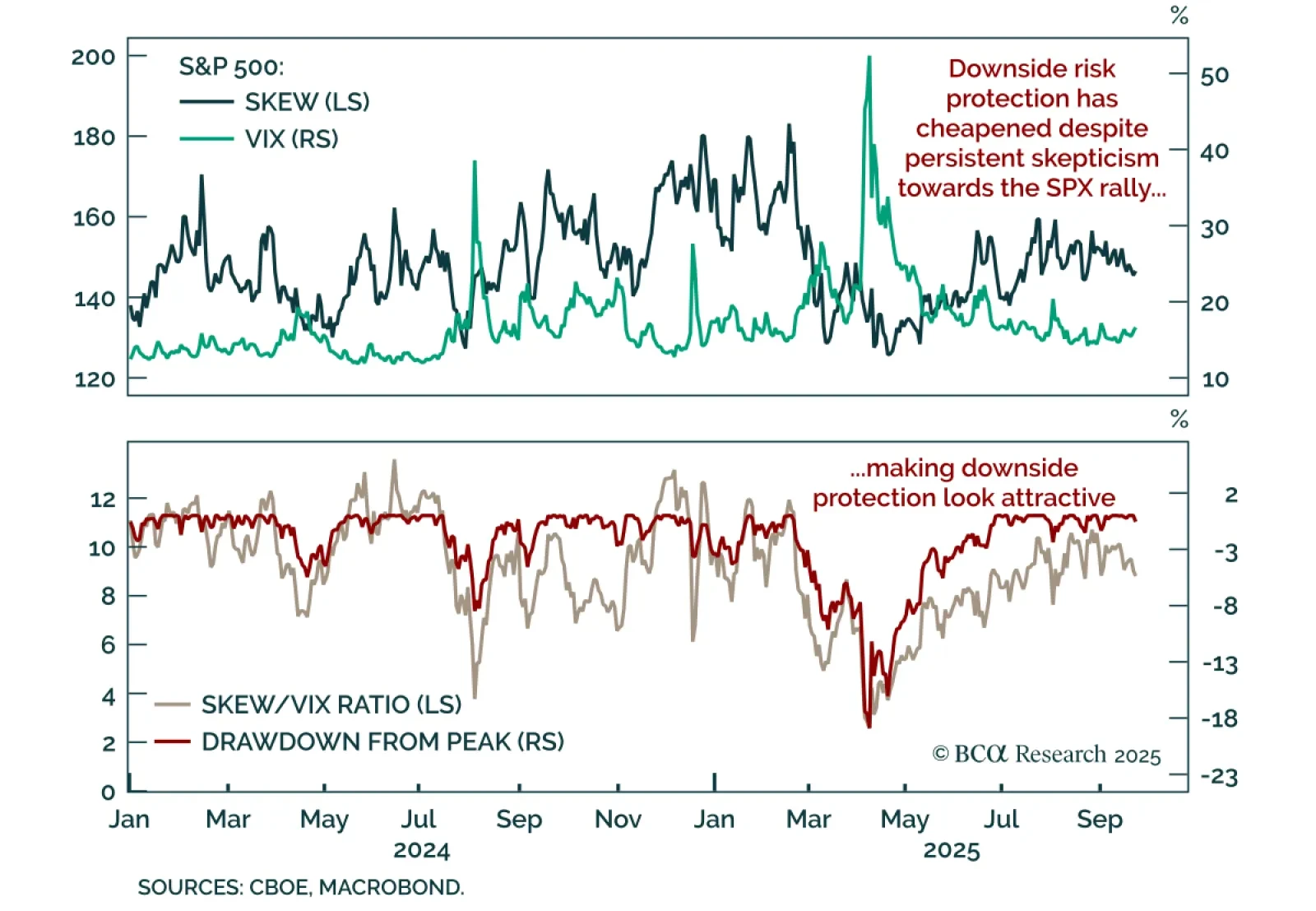

Despite talk of September seasonality, the S&P 500 has not pulled back, and the pain trade remains higher. The sell-off many expected failed to materialize. Positioning is not stretched, and in an environment where dip-buying remains instantaneous, any…

This week’s US Bond Strategy Special Report takes a look at the two most provocative papers presented at last month’s Jackson Hole conference.

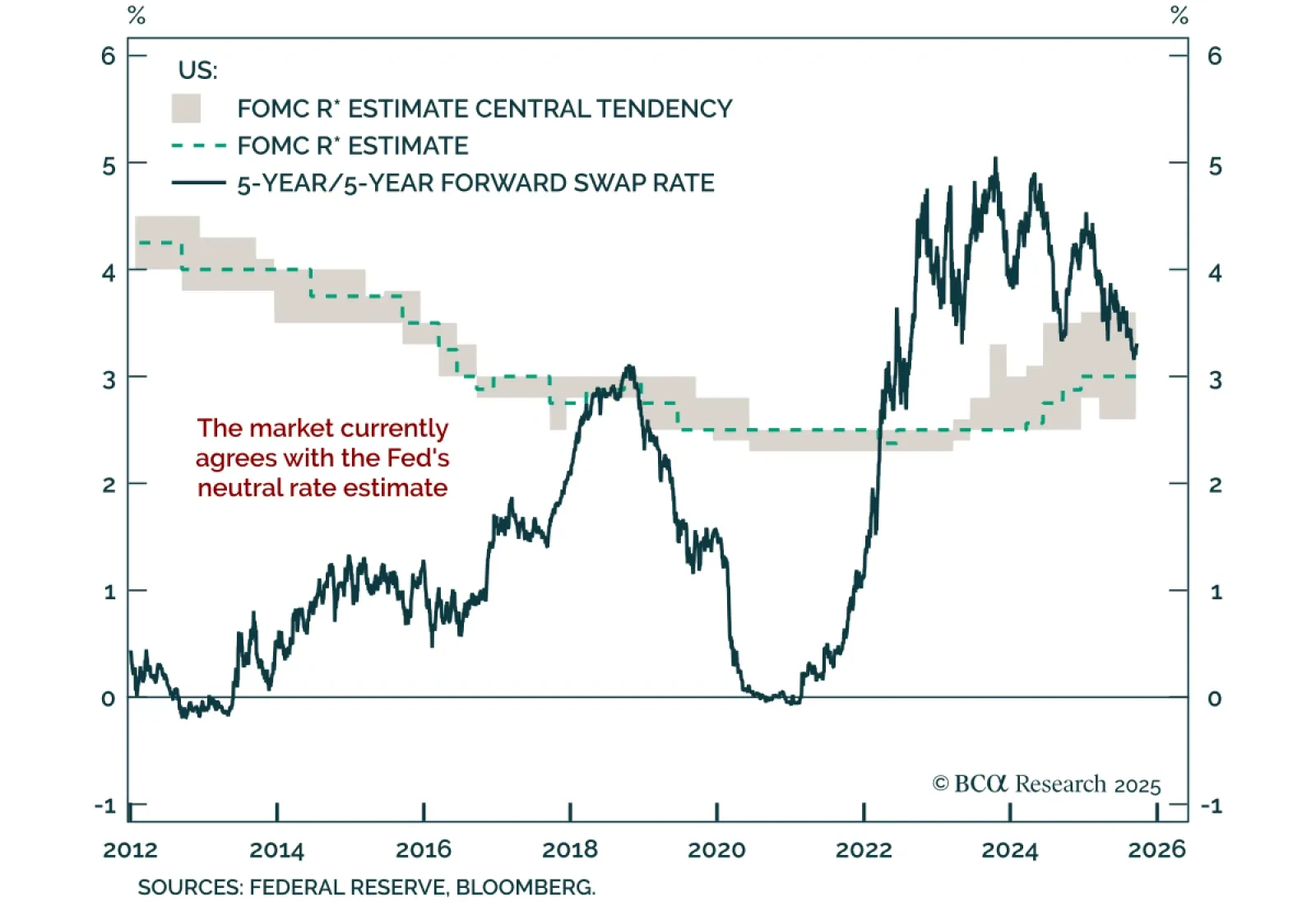

Post-FOMC speeches reveal divisions across the committee, reinforcing long duration as policy remains mildly restrictive. The September dots showed a split, with half of participants expecting at most one 25 bps cut and the rest seeing at least two. Gov.…

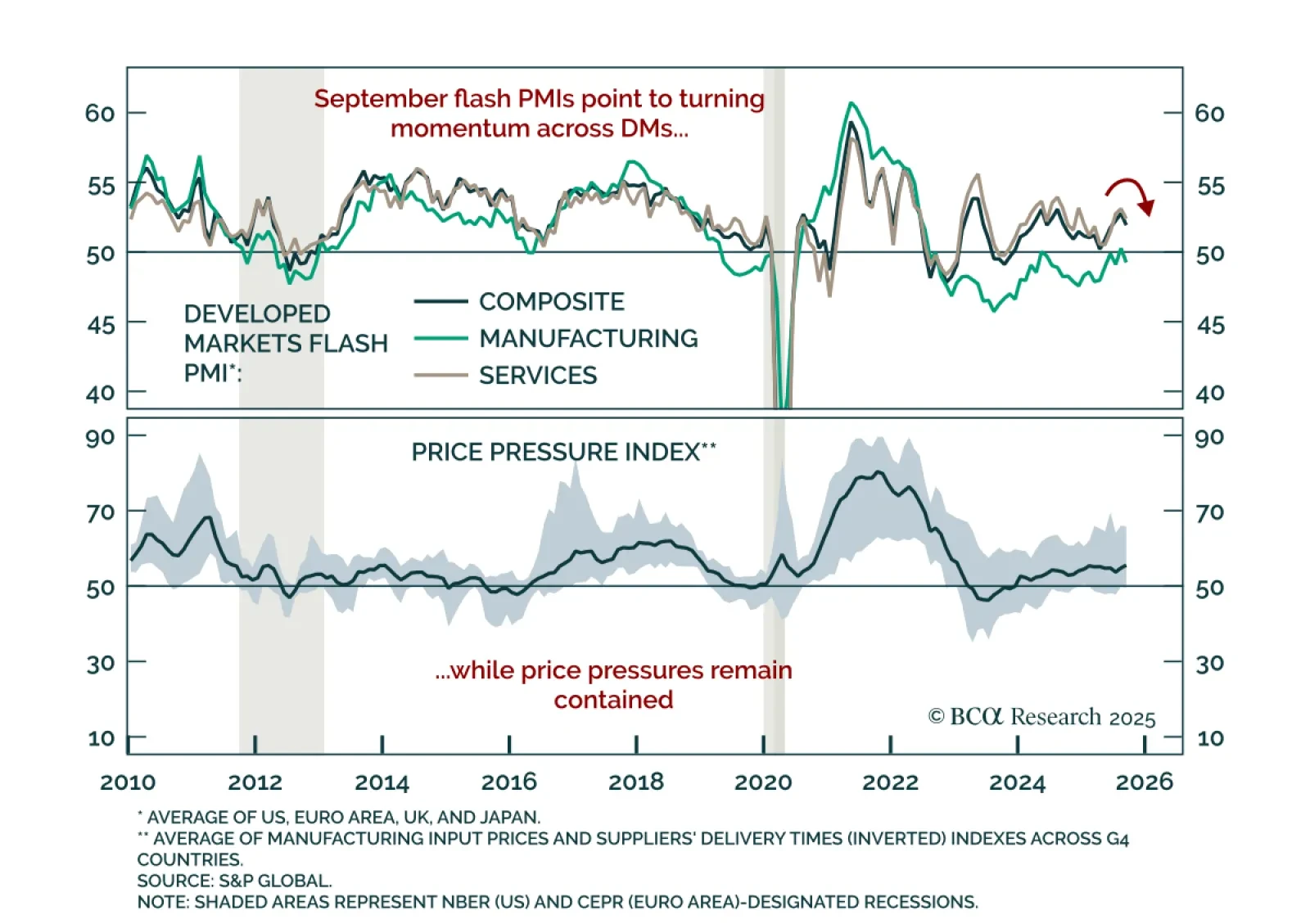

September flash PMIs show slowing global momentum, reinforcing US equity outperformance and underweights in industrial metals. The US composite slipped to 53.6 from 54.6, led by weaker manufacturing. Europe was mixed: Services strengthened modestly but…

Low rates volatility has been a key tailwind for equities, but the fragile equilibrium leaves markets exposed to AI sentiment and inflation risks. Rates volatility, measured by the MOVE index, has drifted to multi-year lows and sits below its 20th percentile…