United States

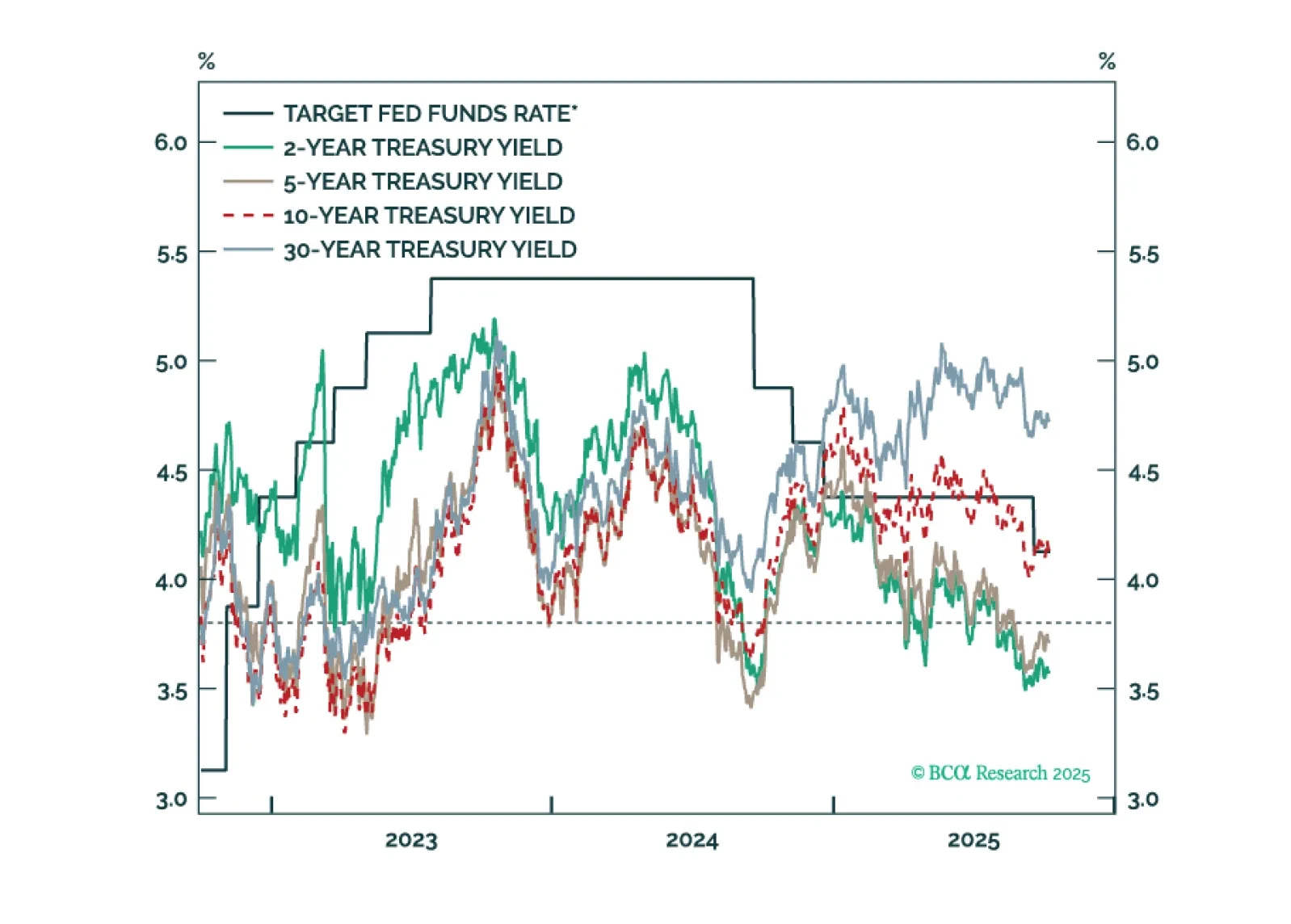

Treasury yields are generally following the pattern of past interest rate cycles, but with a larger term premium keeping the curve steeper than usual.

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.

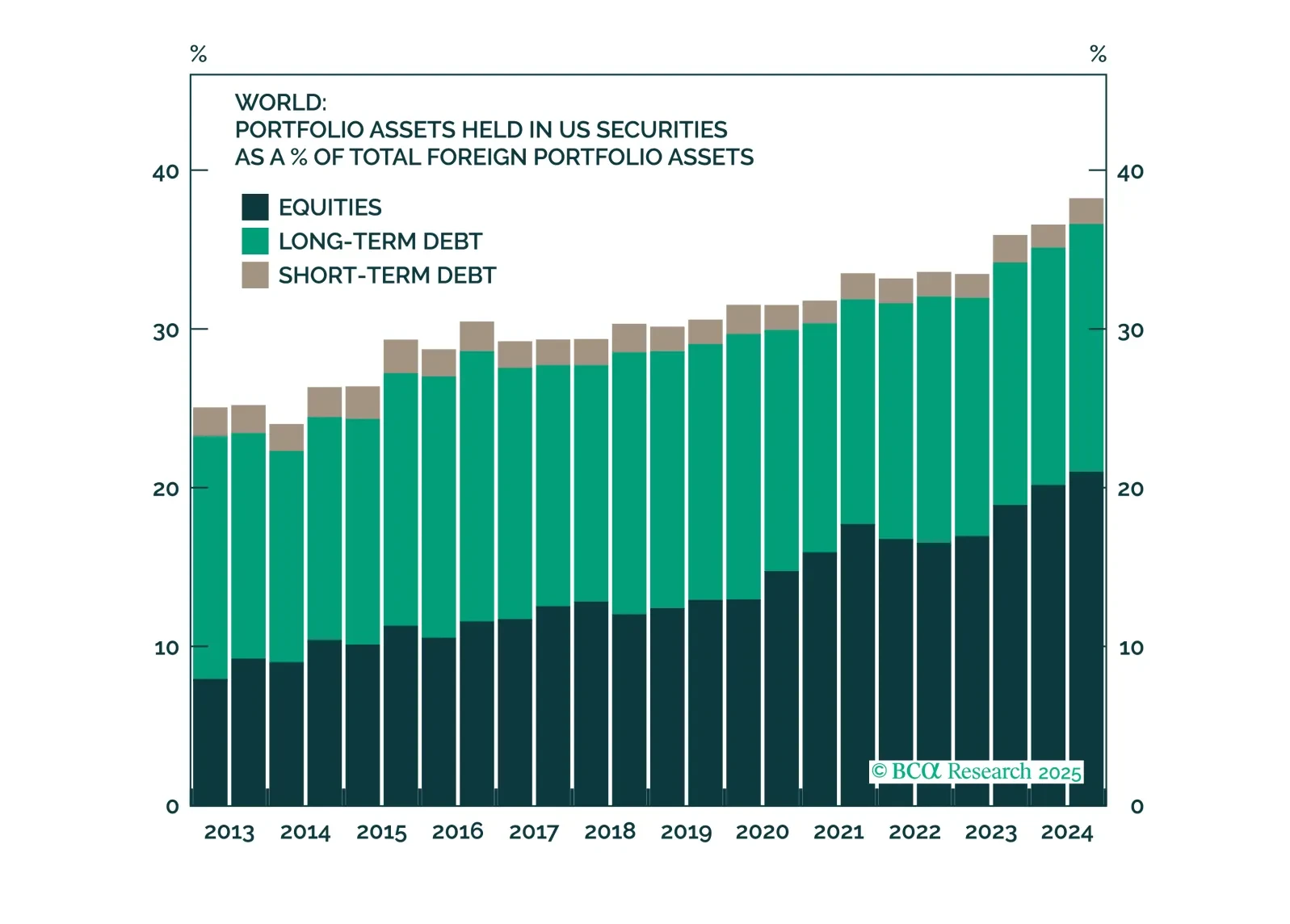

The dollar’s early 2025 decline was a reflection of a global rush to hedge accumulated USD exposure, not a mass exodus from US assets. With most hedging now complete, currency moves should again follow fundamentals, setting the stage for a tactical USD rebound in the months ahead.

Despite concerns about fiscal sustainability, a rise in term premia, and attacks on central bank independence, monetary policy remains the primary driver of bond markets. In our Q3 Review & Outlook, we update our views and identify opportunities in government bonds, short-term interest rate futures, global yield curves, inflation-linked bonds, and credit.

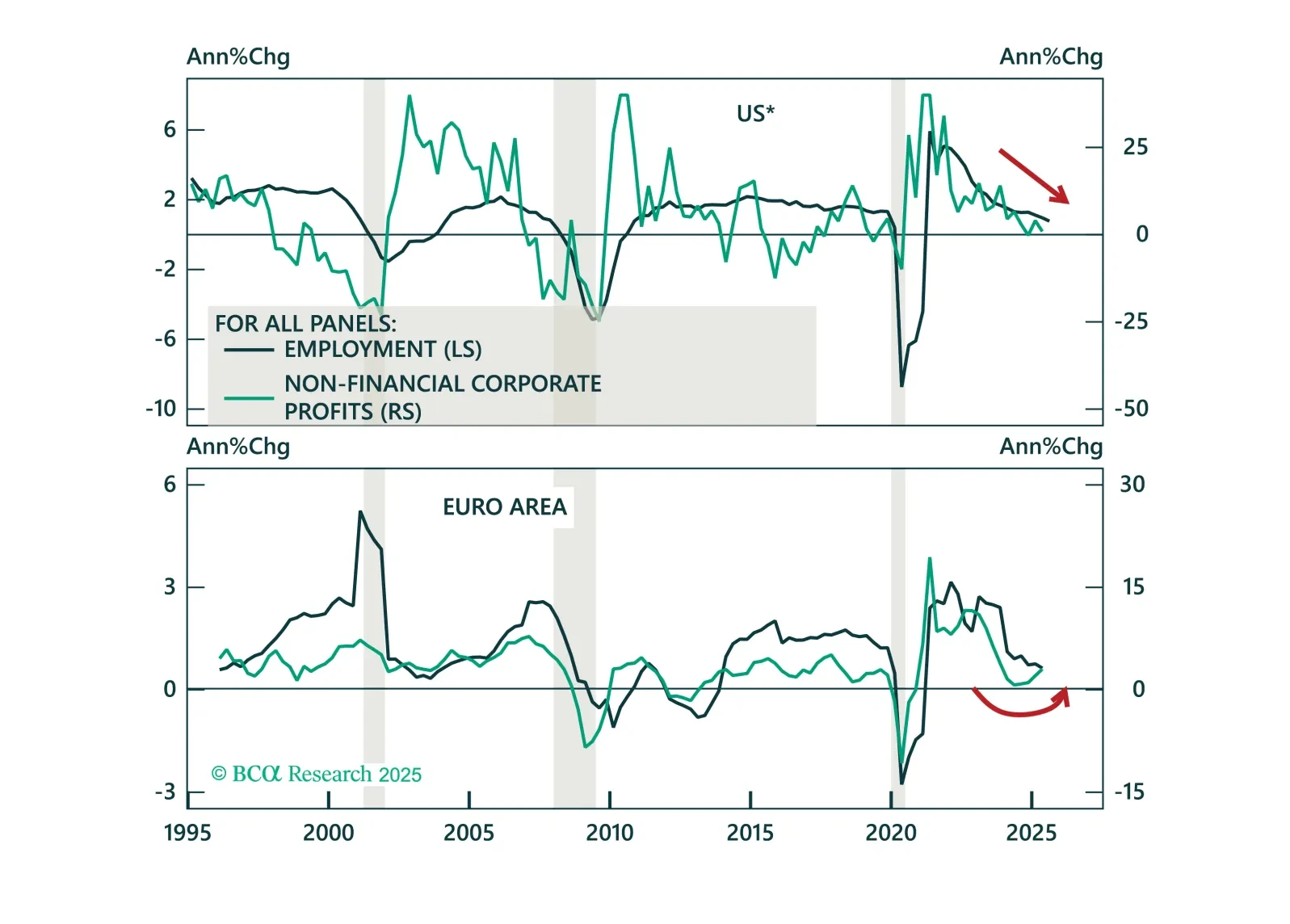

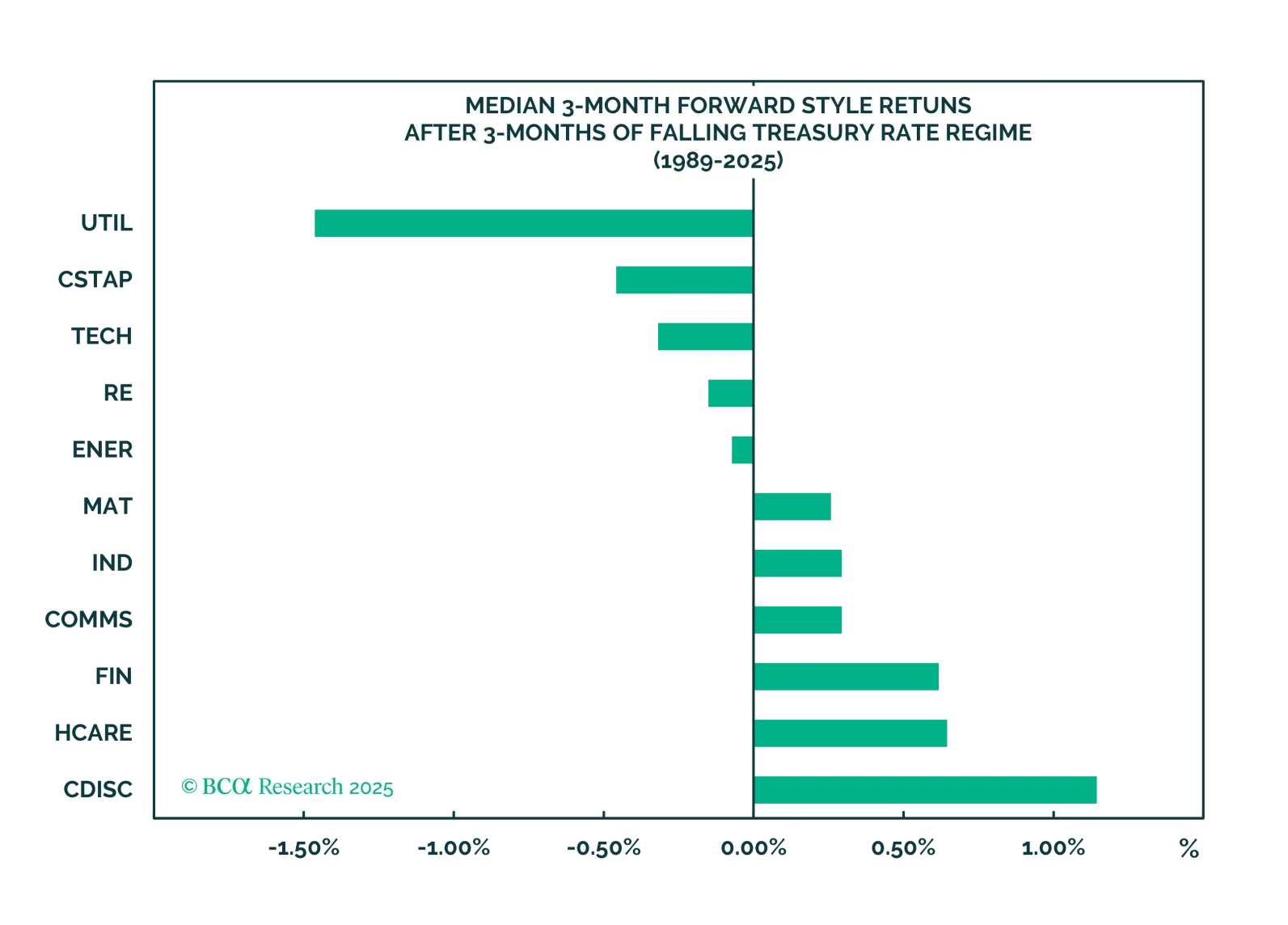

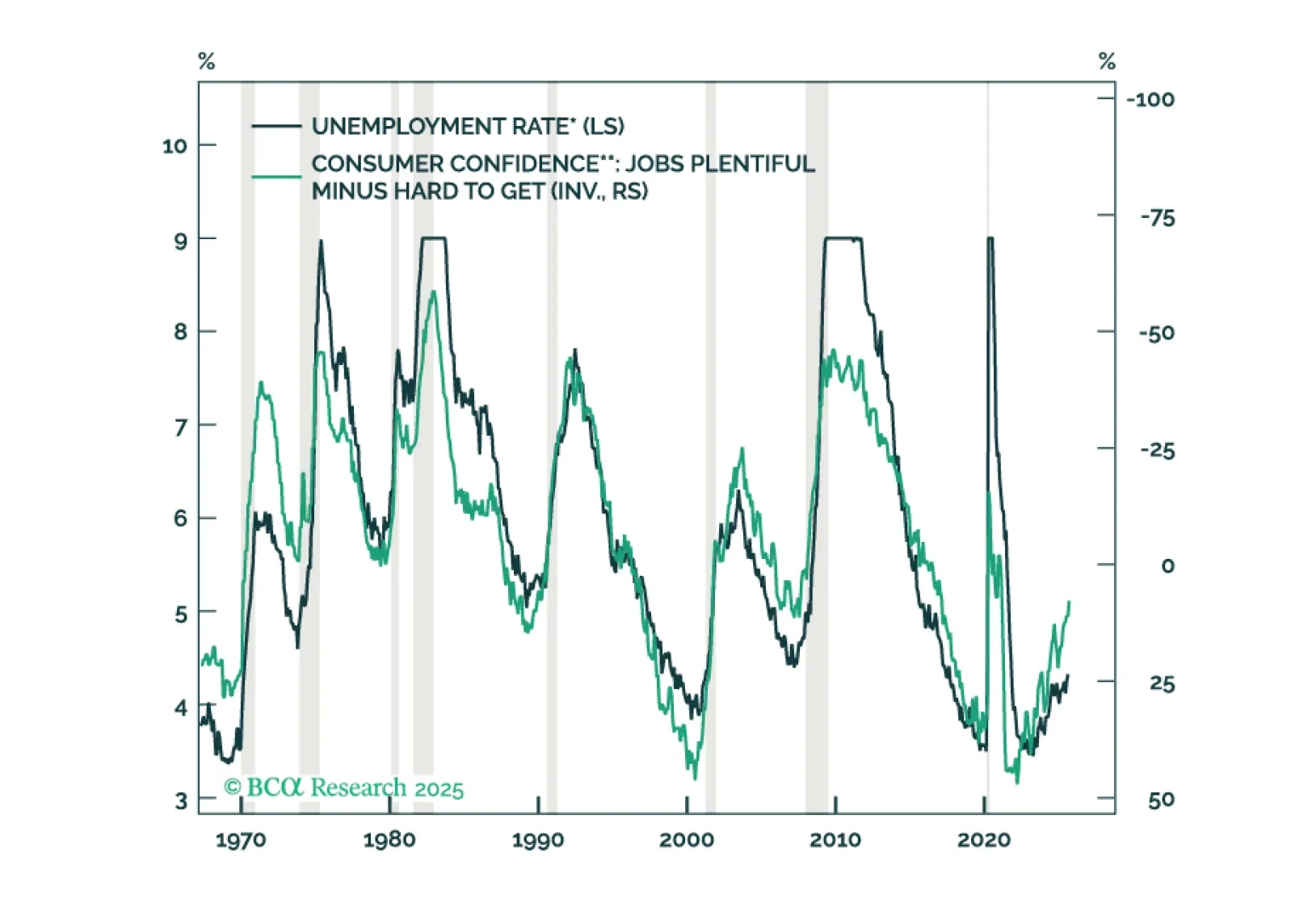

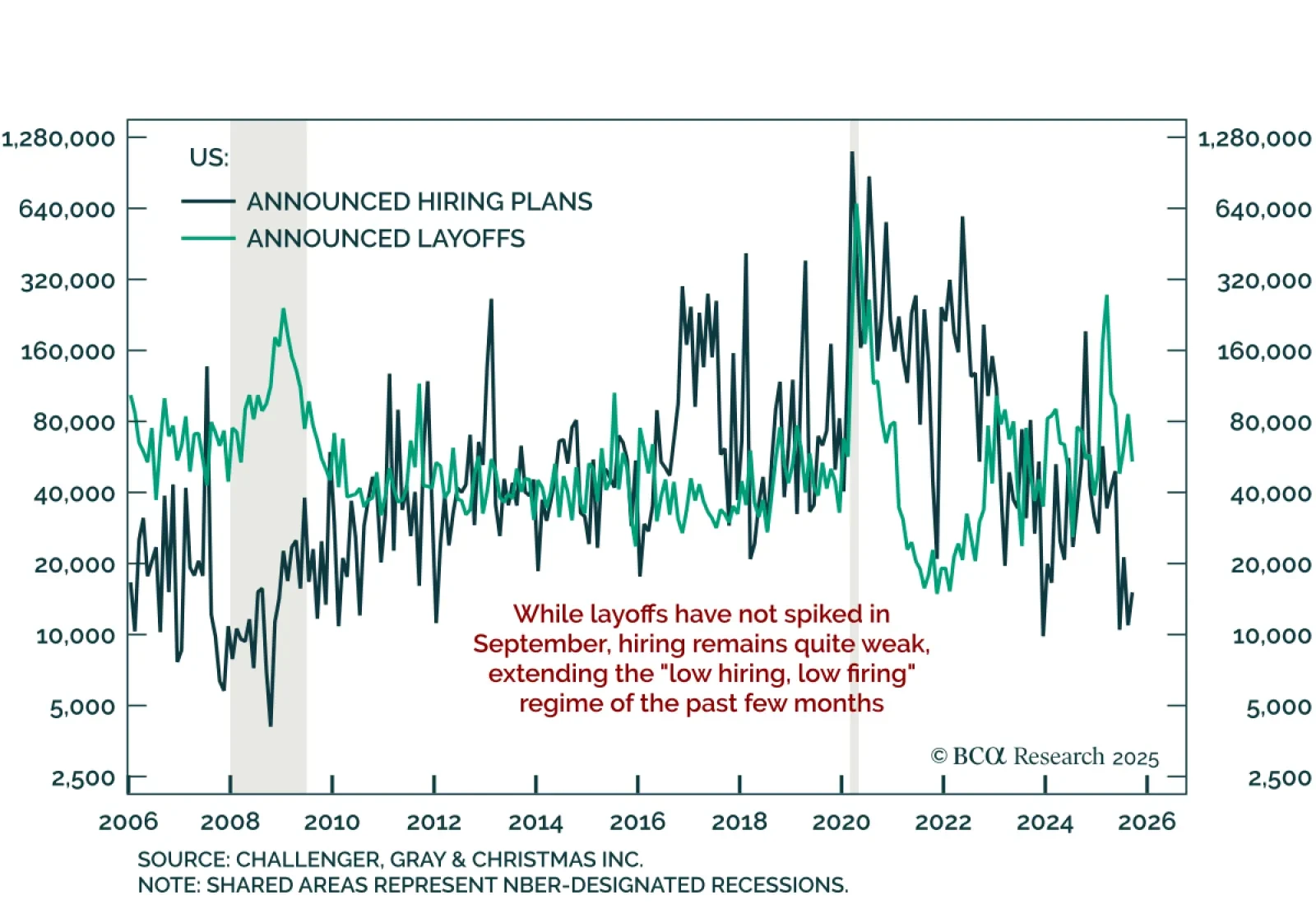

The economy remains resilient despite a softening labor market. As the economy shifts from labor toward capital, we may be in the early stages of a “jobless boom.” Our bull case for equities rests on strong earnings growth, accelerating GenAI adoption, monetary easing, and stimulus from OBBBA. Key risks we continue to monitor are rising bond yields and the threat of stagflation.

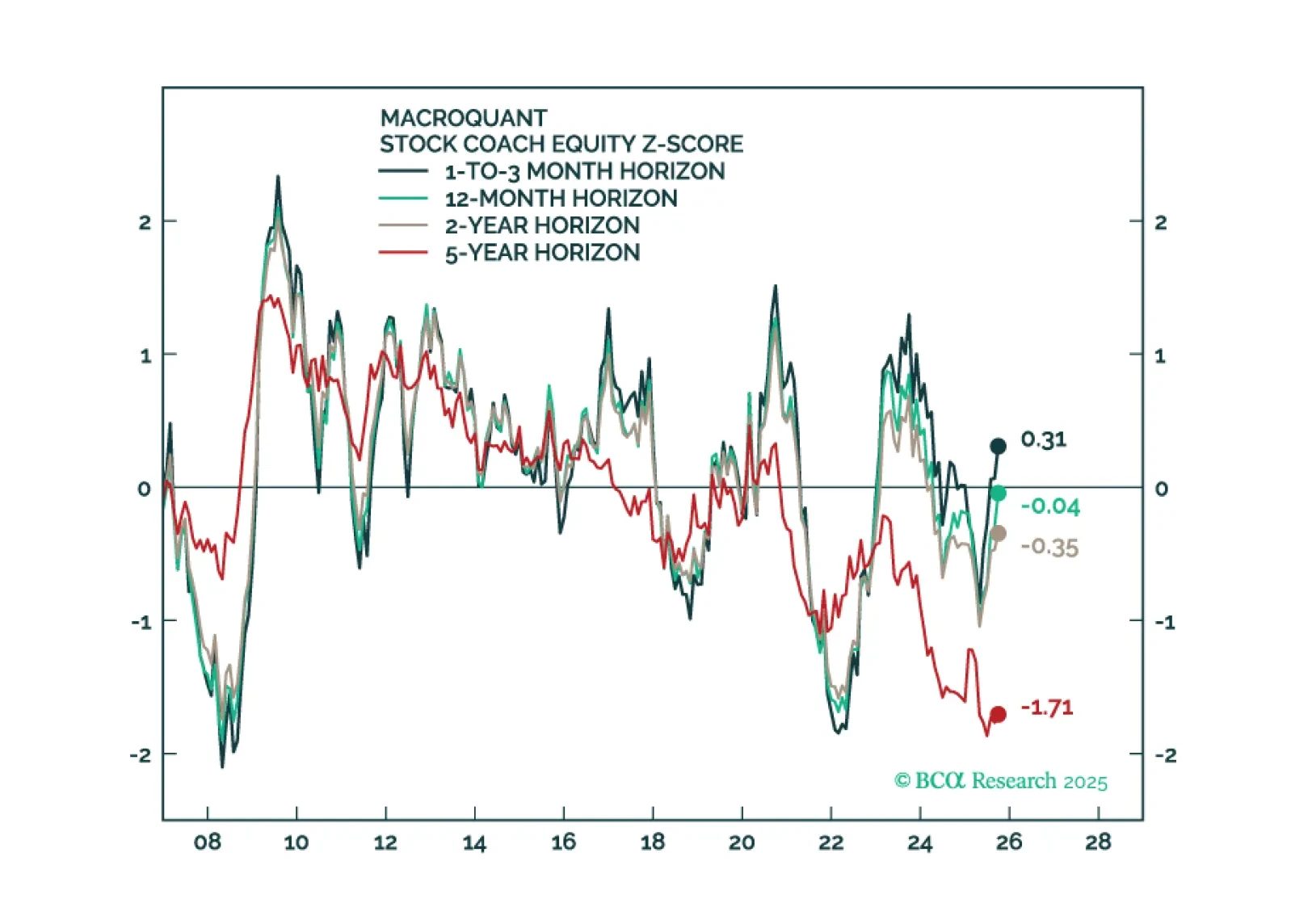

Our Portfolio Allocation Summary for October 2025.

A short guide on how best to use and interpret our real-time fractal heatmap for asset allocation.