United States

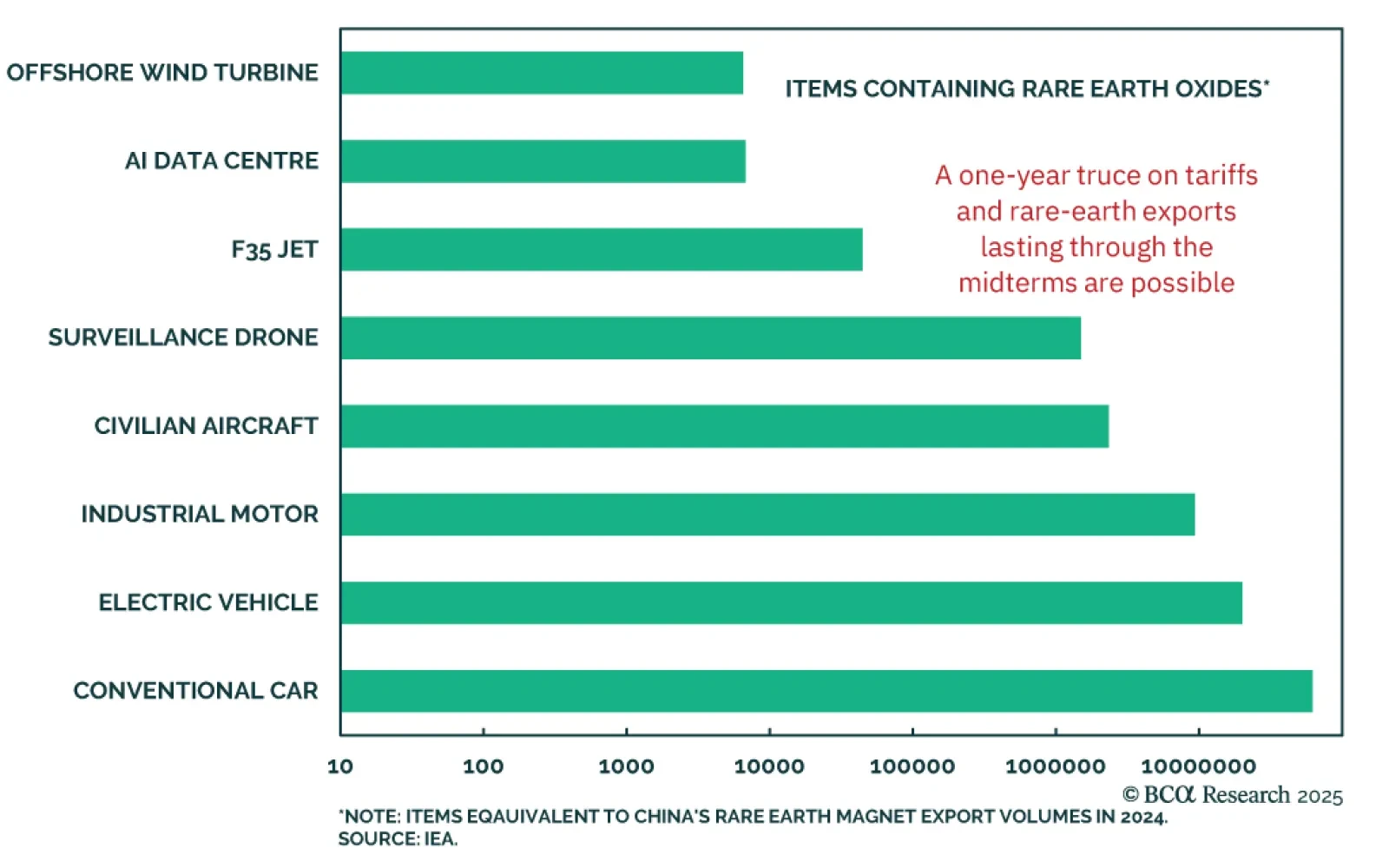

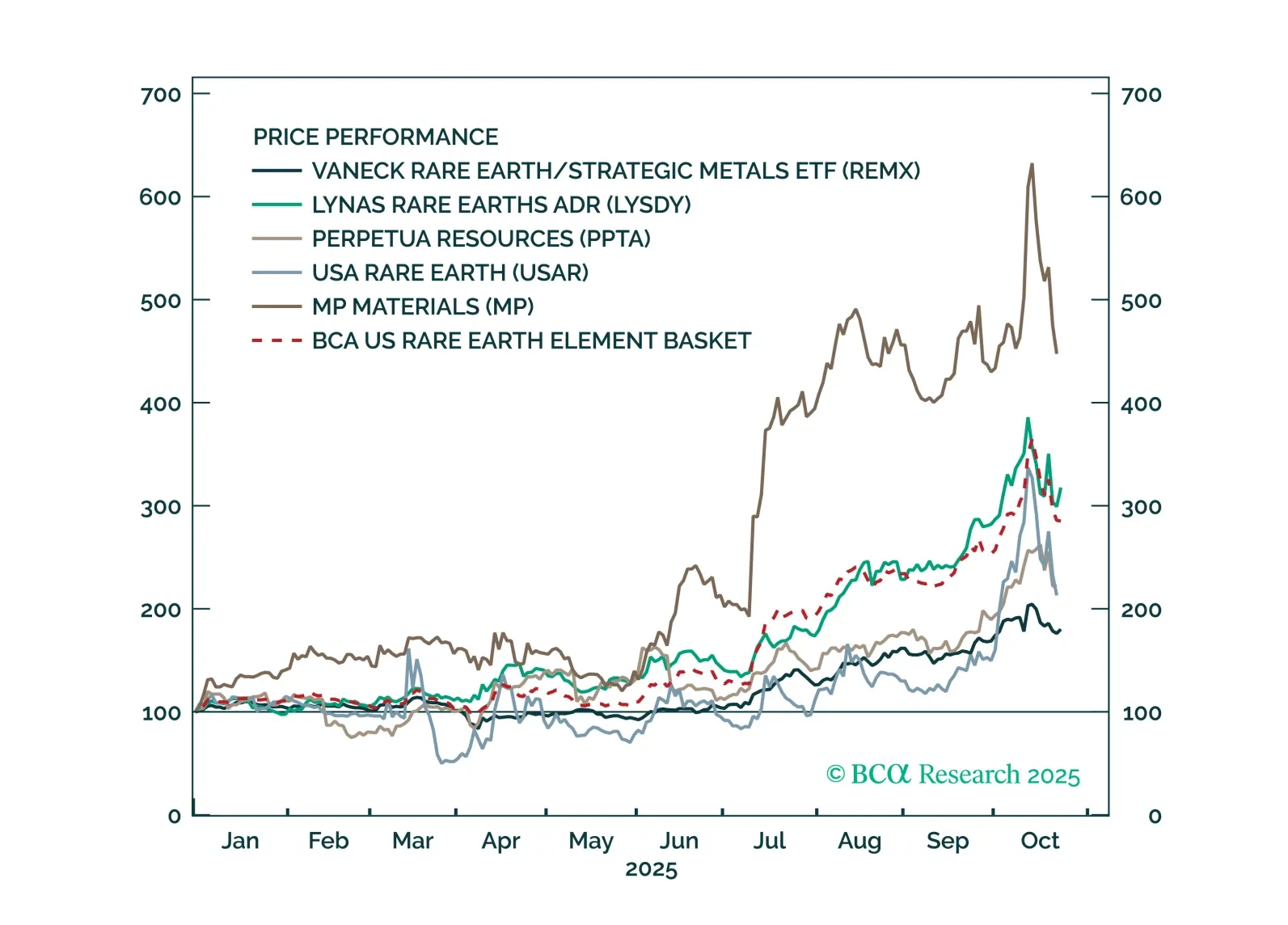

US-China decoupling and rare-earth supply disruptions created a unique opportunity for non-Chinese miners and refiners to scale production and achieve profitability. The build-out will be lengthy, costly, and fraught with challenges, but government support materially improves the odds. Rare-earth production outside China is a nascent investment theme; we are structurally bullish and recommend building a position by buying on dips by investing in a diversified basket of miners, presented in the report.

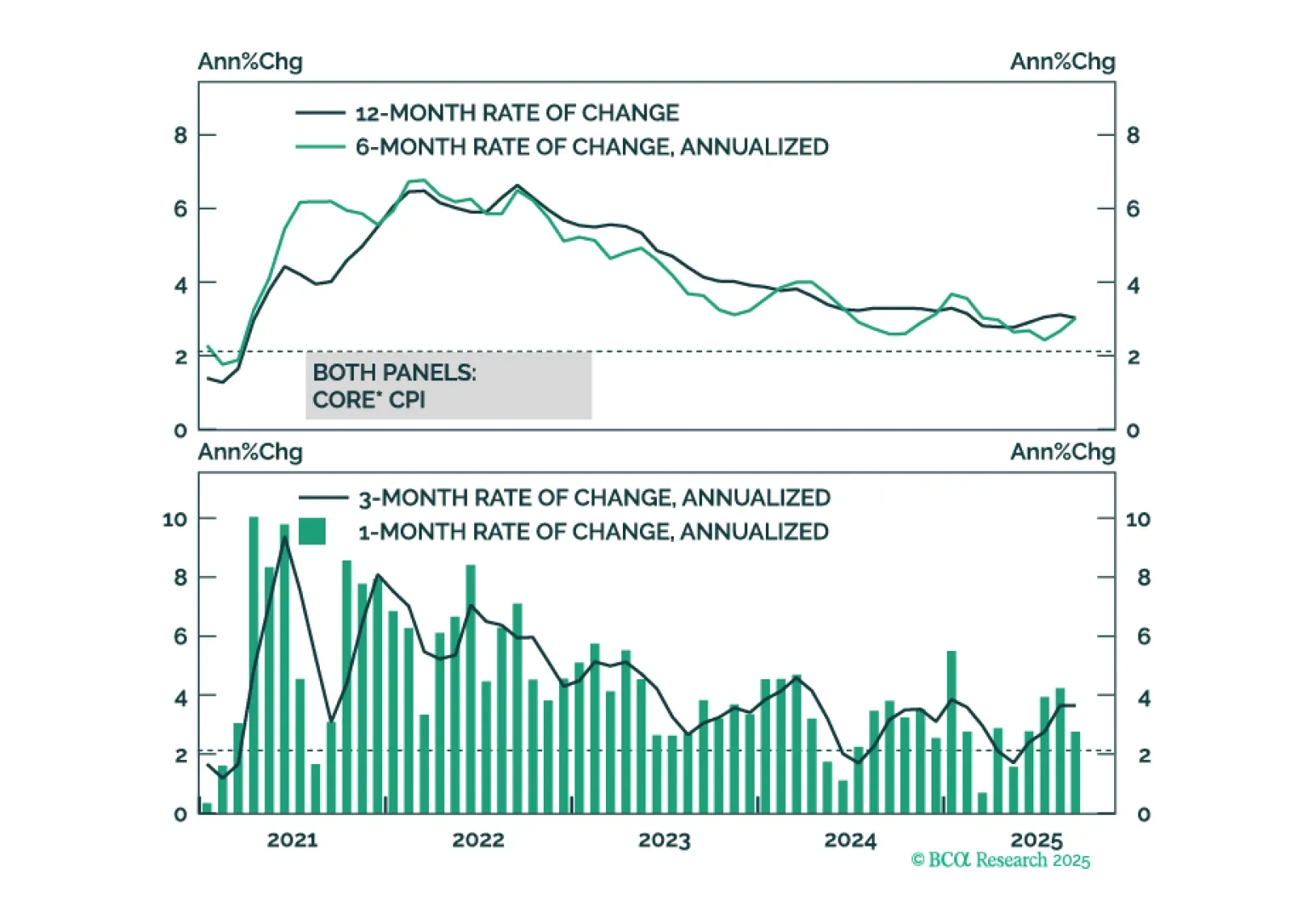

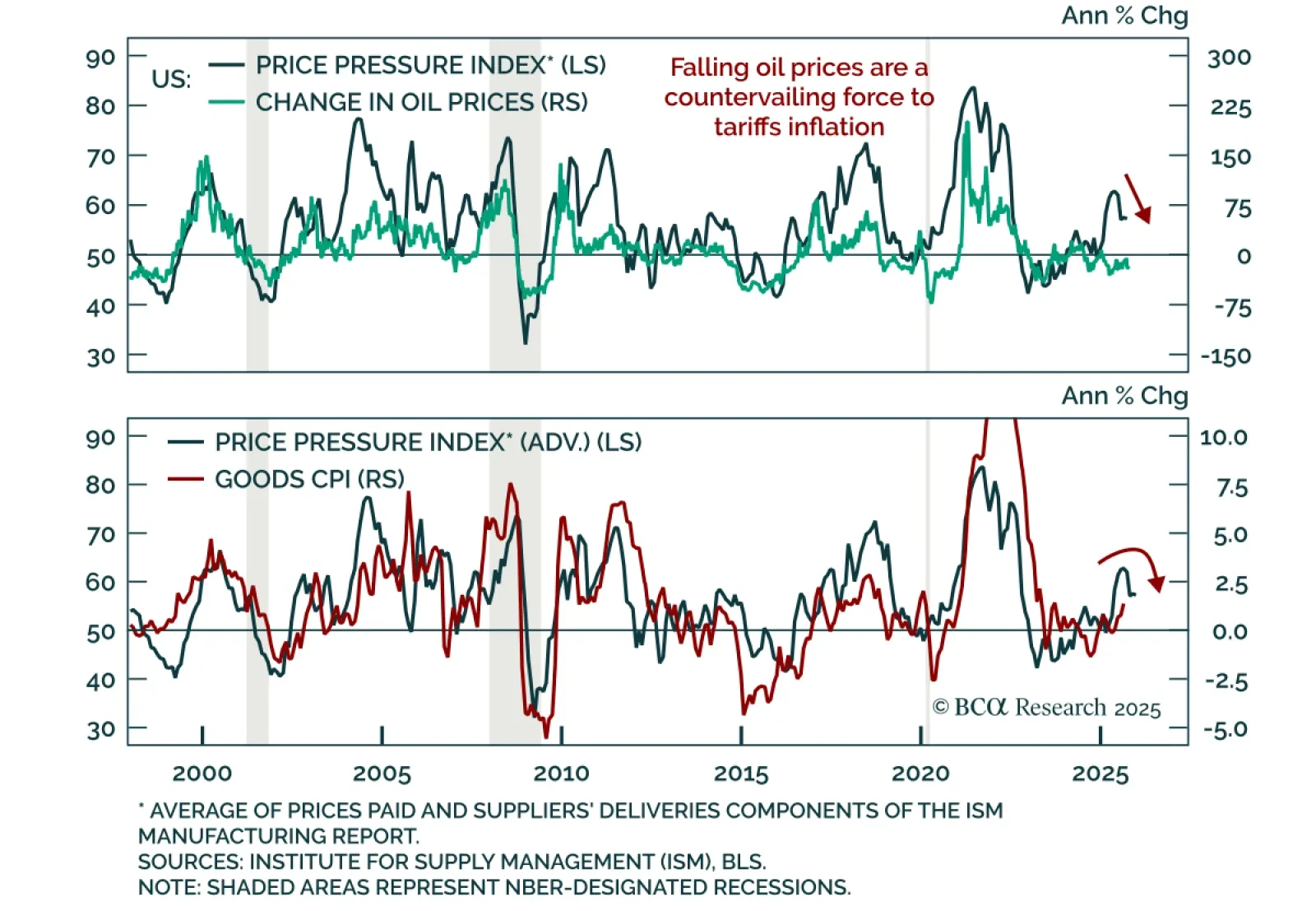

US inflation data continue to show no signs of price pressures beyond a near-term tariff effect.

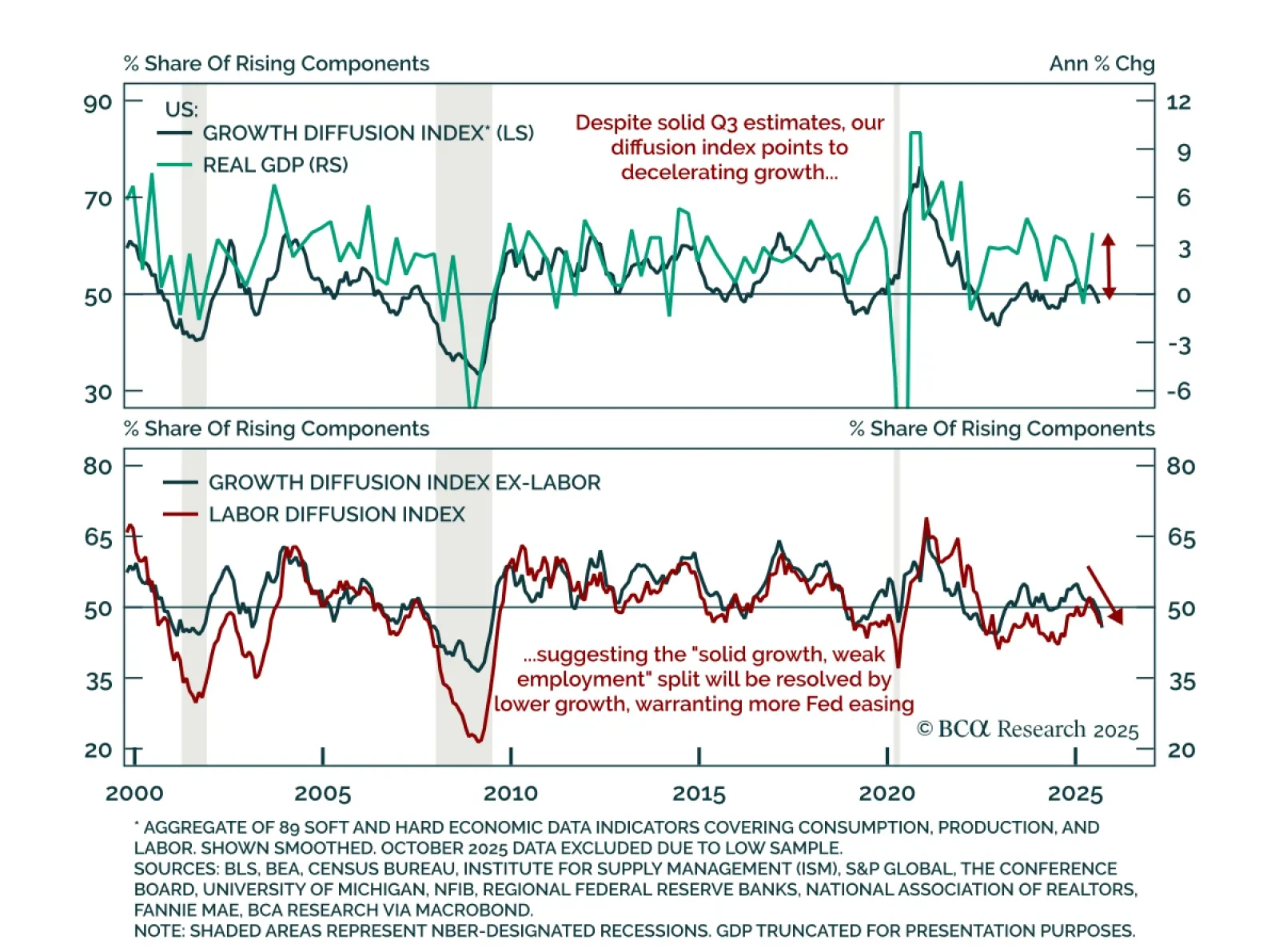

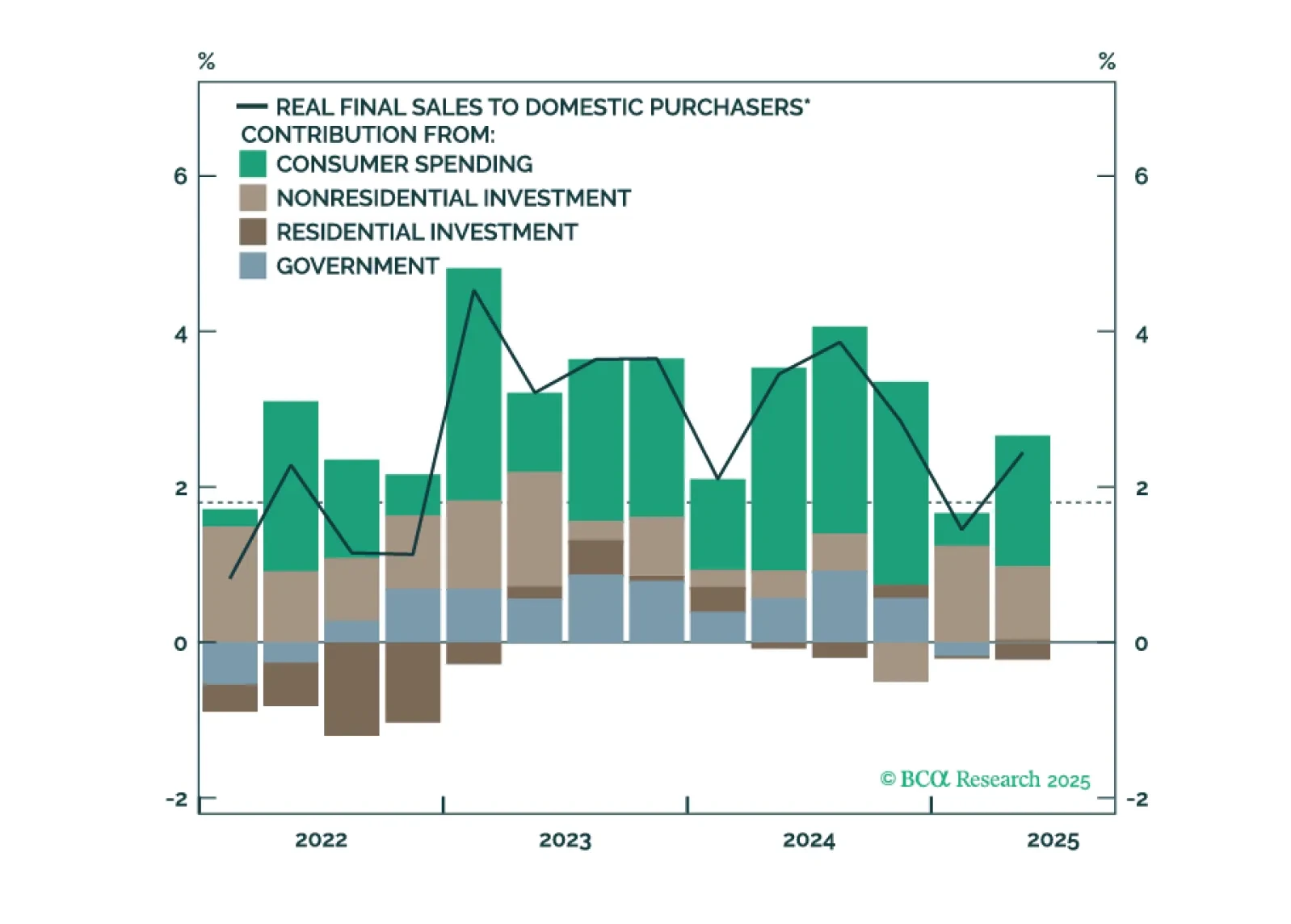

The Fed is poised to deliver a 25-basis-point rate cut this month, but a follow-up rate cut in December will depend on how the divergence between strong consumer spending and weak employment growth is resolved.

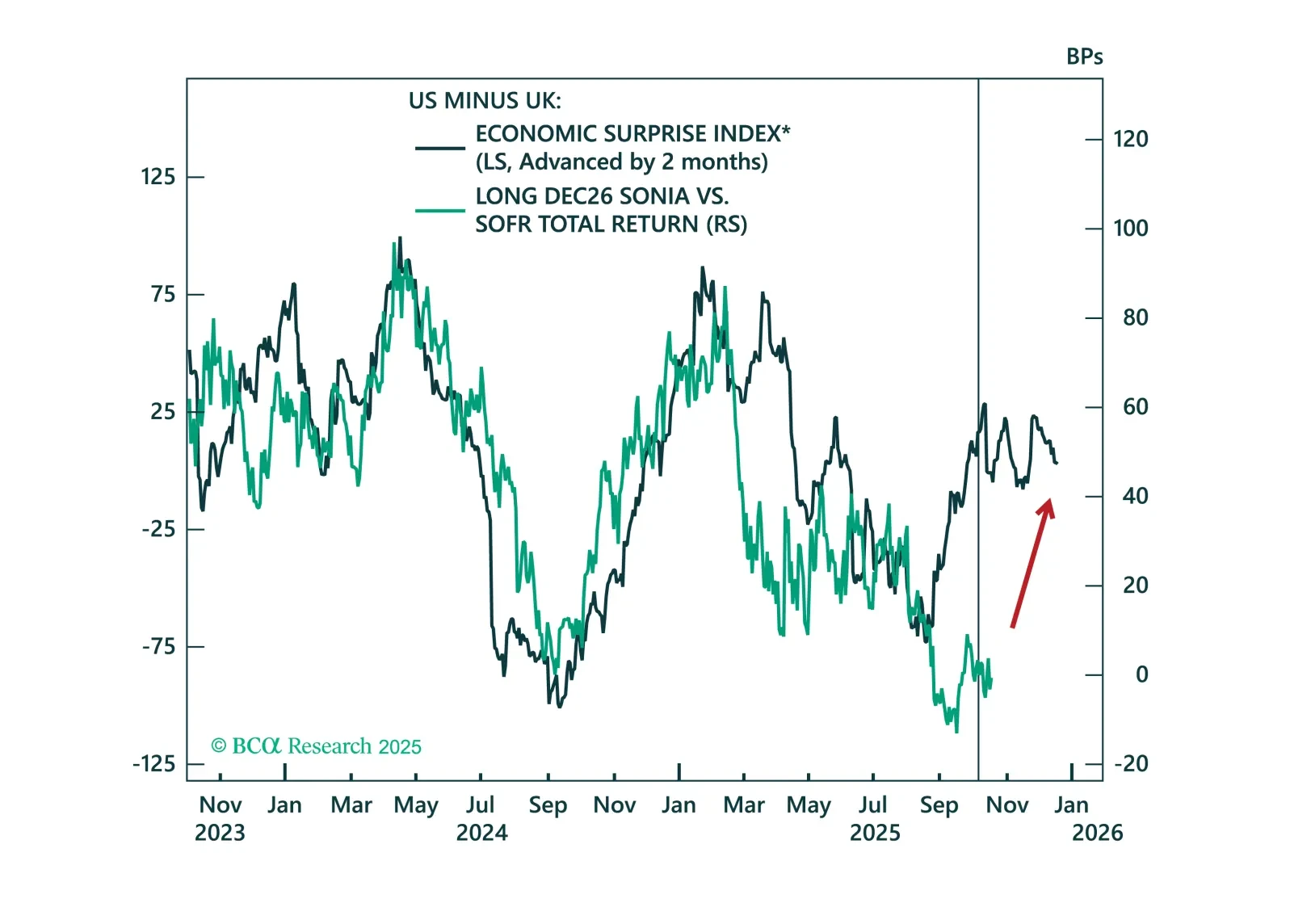

Same policy rate, very different expectations. We break down why policy convergence between the Fed and BoE is THE fixed income trade for year-end.

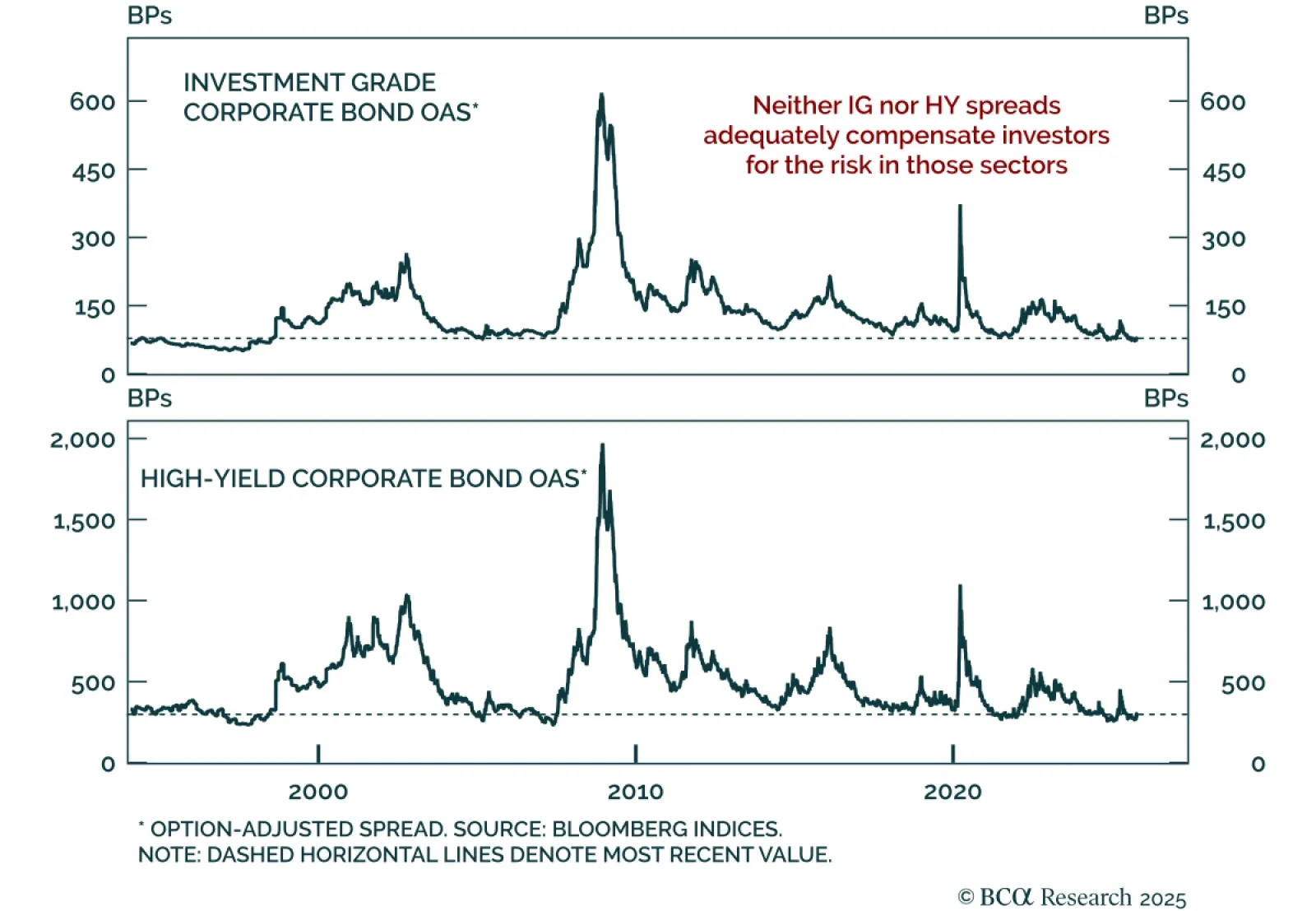

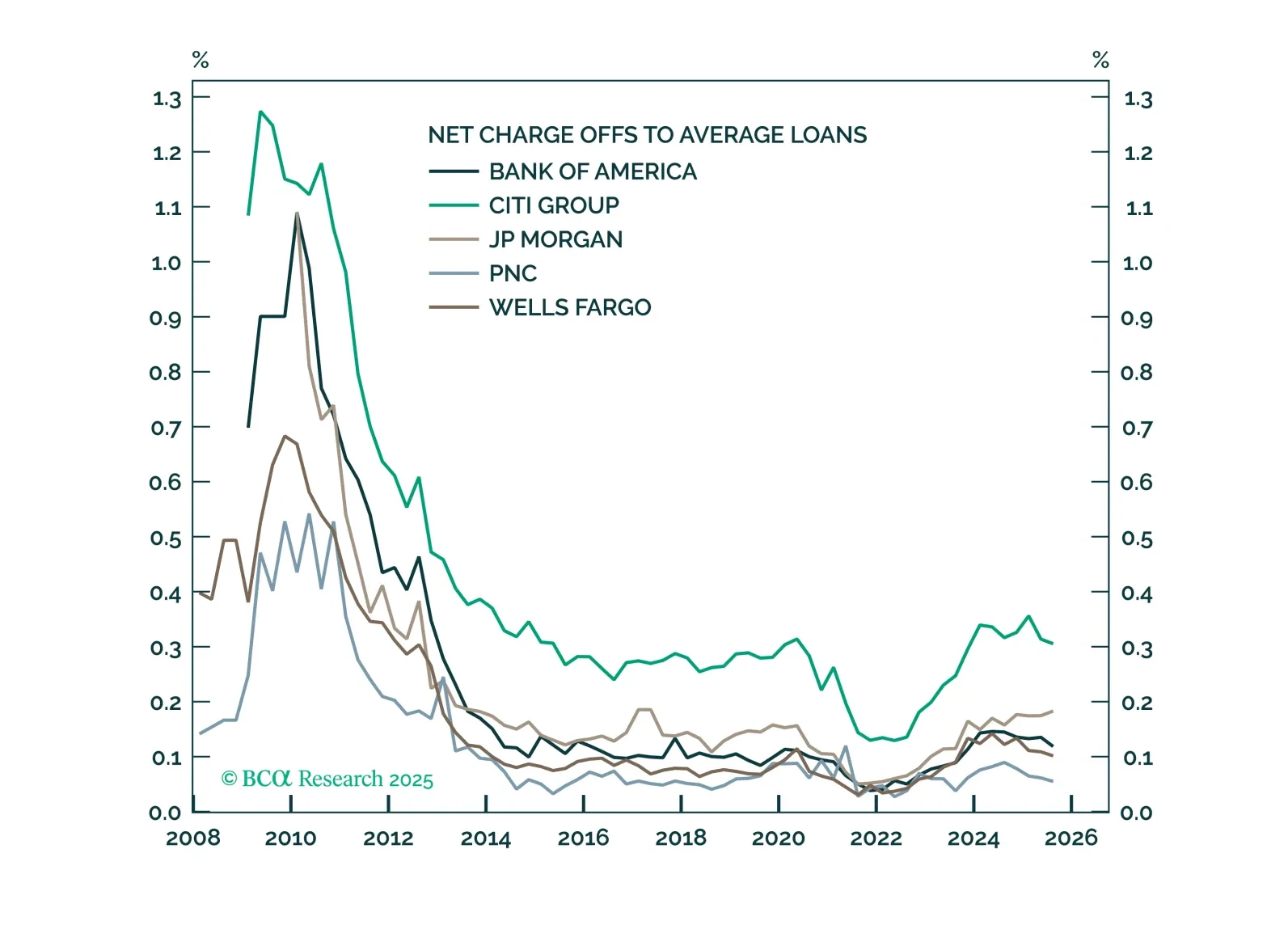

Strong results and constructive commentary from the US’s largest banks are encouraging: Consumers remain in solid shape, and the macro backdrop continues to favor equities. The outlook for the largest banks is positive, and they are unlikely to be affected by isolated credit events.