United States

Job creation remains stalled, but consumers are carrying on and S&P 500 earnings have been growing by double digits. Although the repercussions from the war in the Middle East are not yet clear, the US economy was doing just fine before it began.

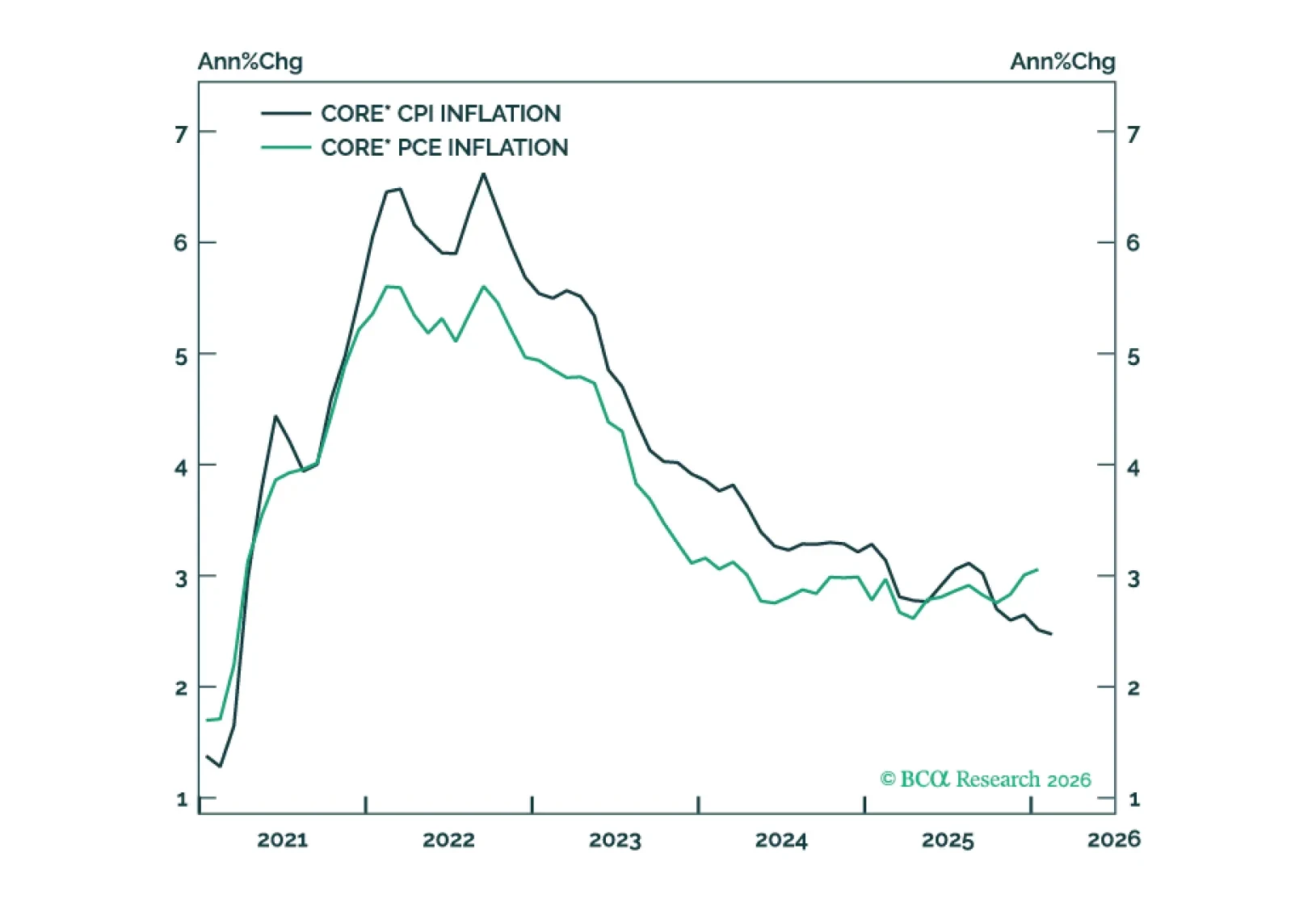

The gap between PCE and CPI inflation will narrow within the next few months, mostly driven by core PCE inflation converging toward its trimmed mean.

The recent oil price shock reinforces our view that inflation will surprise to the upside during the next few months but fall rapidly in H2 2026.

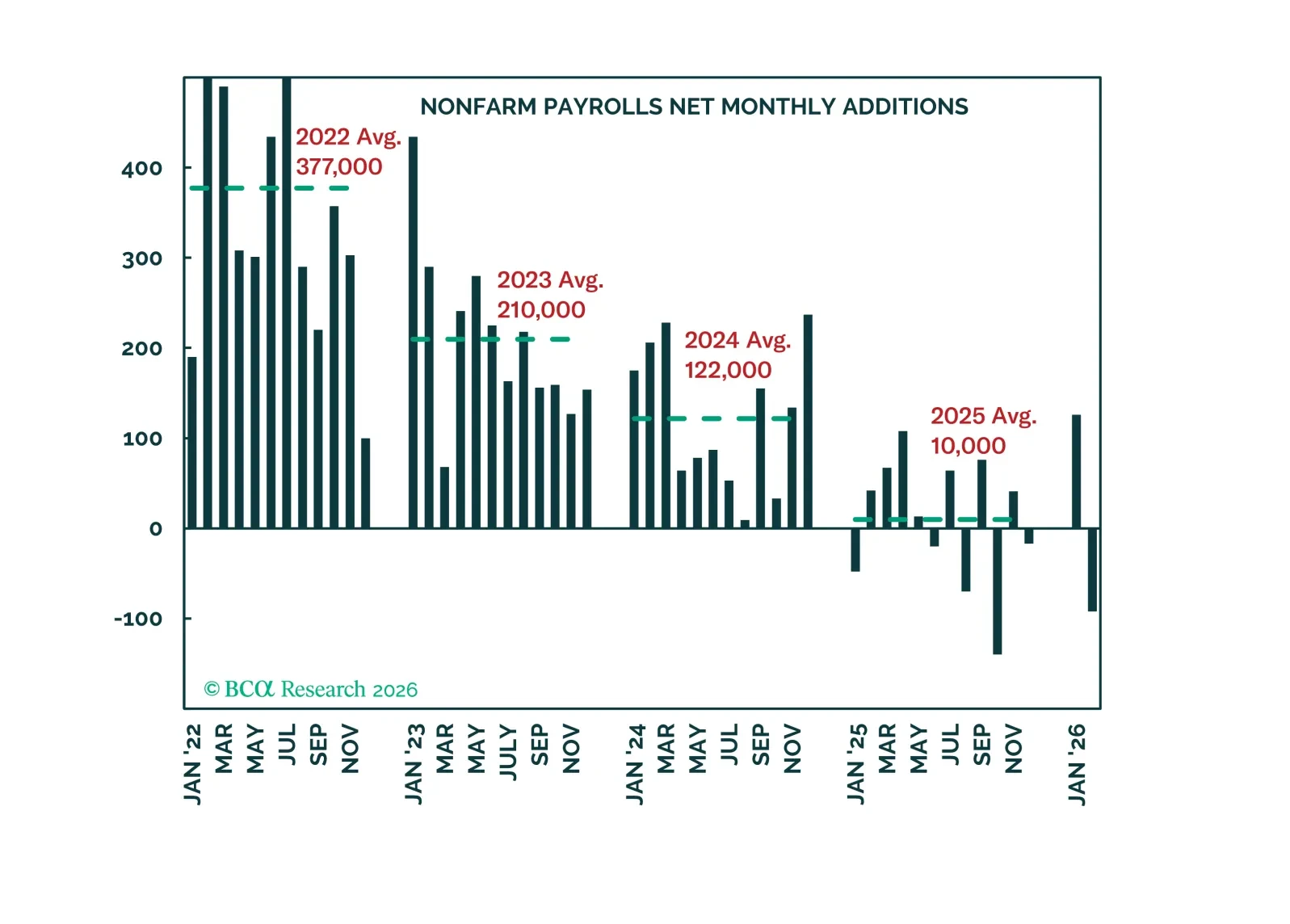

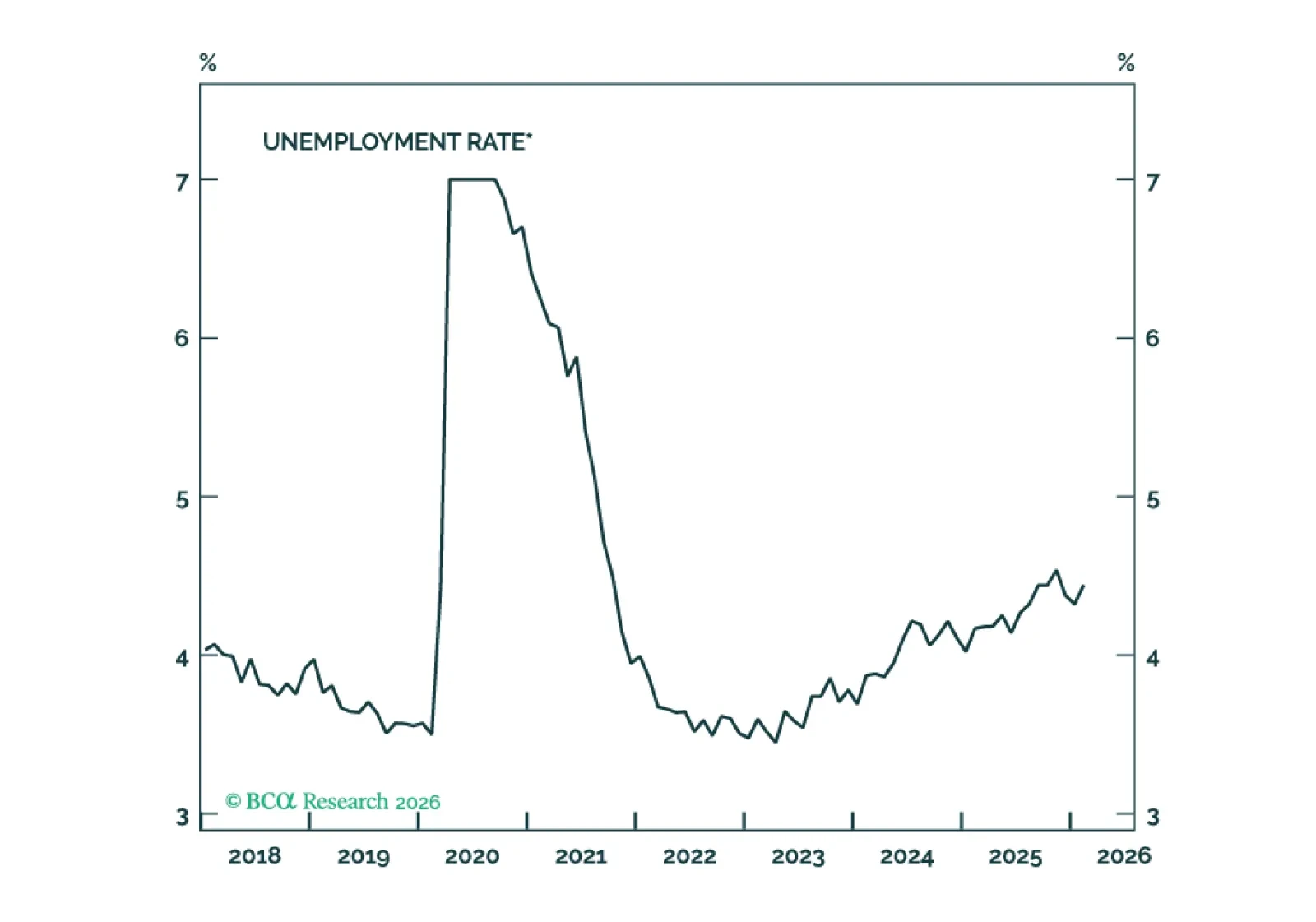

Looking through month-to-month volatility, job growth’s underlying trend is stable and consistent with a flat-to-slightly higher unemployment rate.

An energy price spike caused by a Middle Eastern war almost guarantees that Republicans will lose control of the House, and the chance of a Democratic Senate victory increases from 35% to 40%.

Our Portfolio Allocation Summary for March 2026.

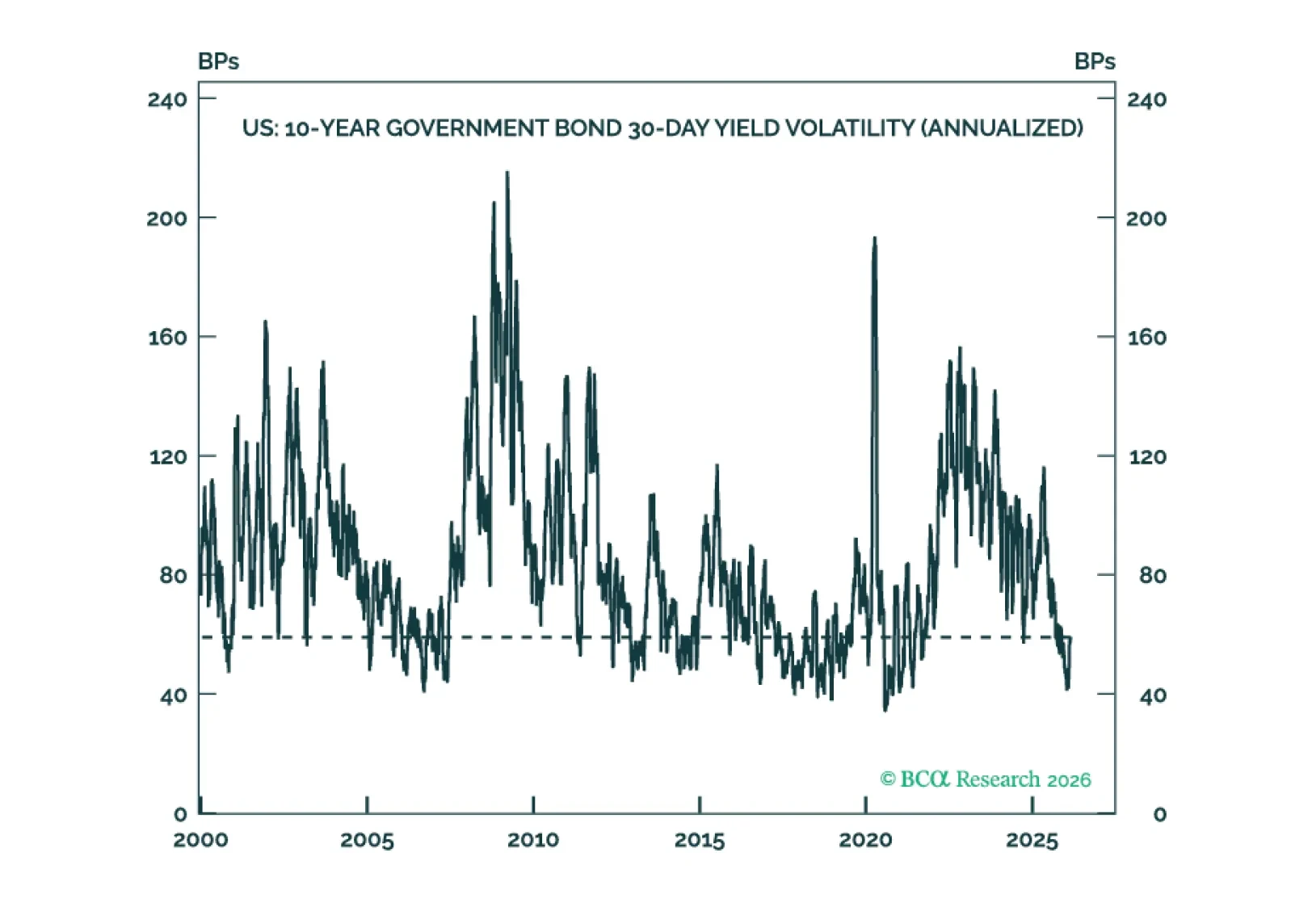

Interest rate volatility is very low across developed market fixed income. Investors should maximize the carry in their portfolios to outperform in a low rate vol environment.