United States

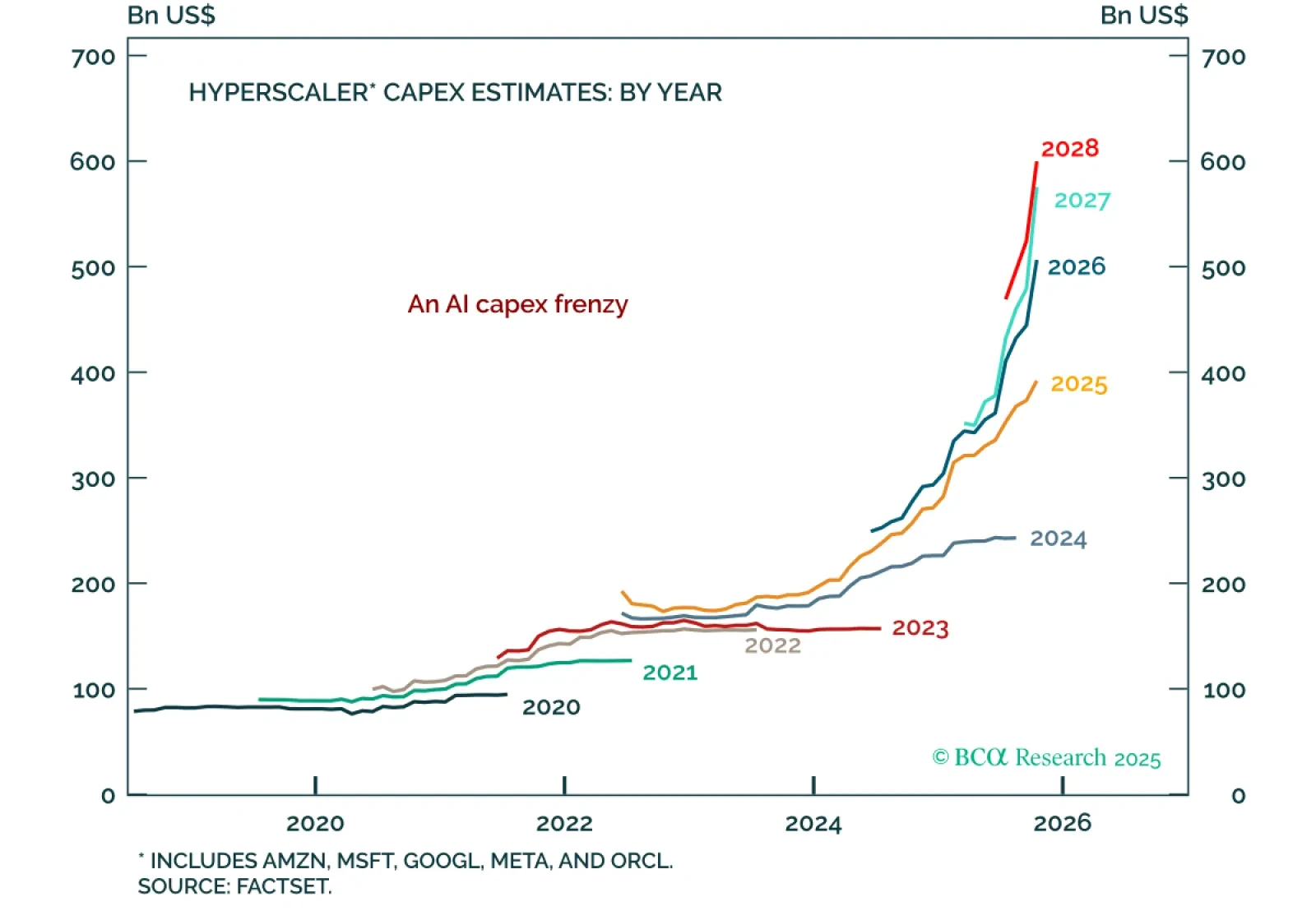

Our Global Investment strategists believe the risk of a “Metaverse Moment” in AI is rising and recommend increasing caution toward AI stocks and the broader S&P 500. This inflection occurs when markets begin penalizing companies for capex expansion, signs…

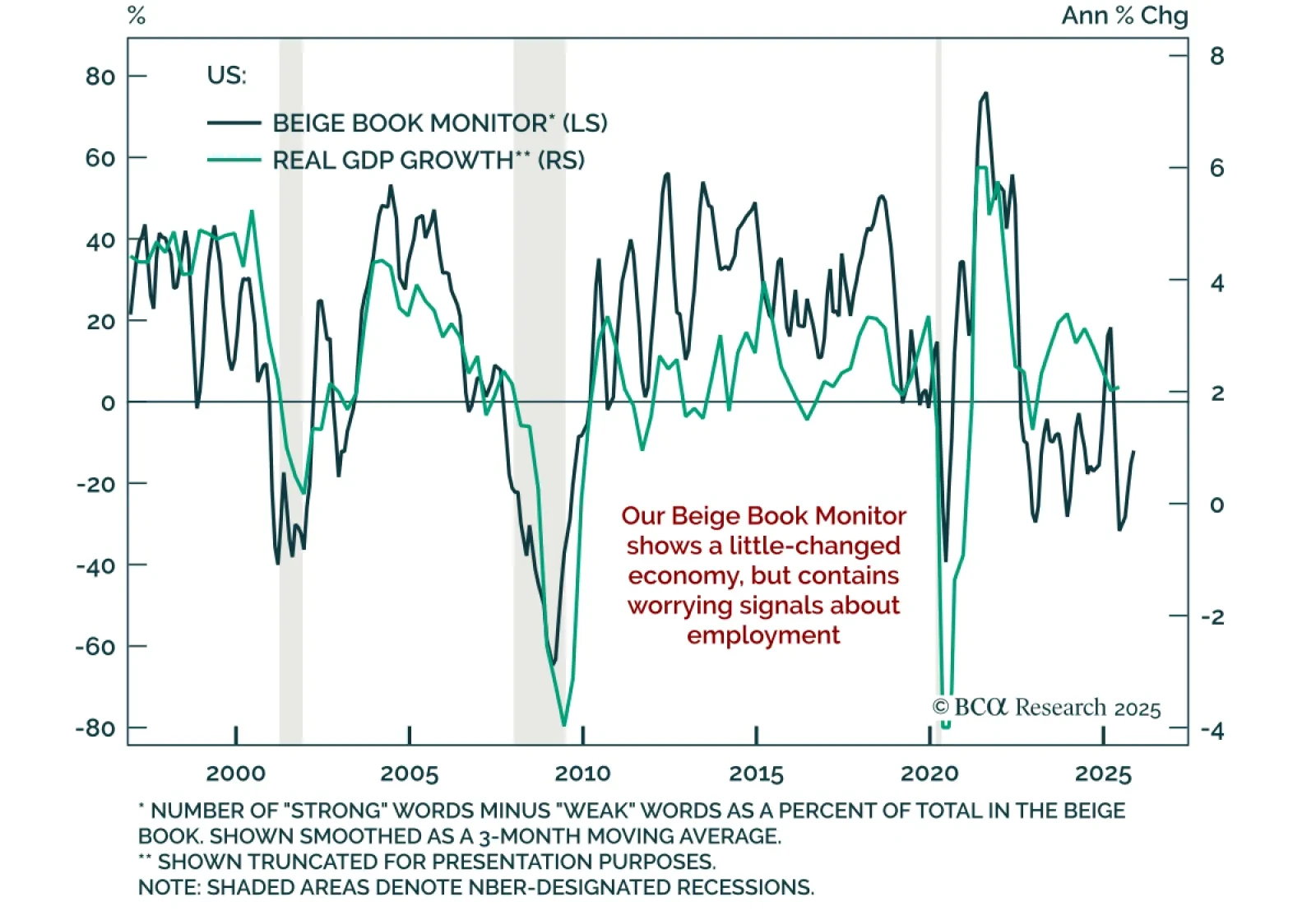

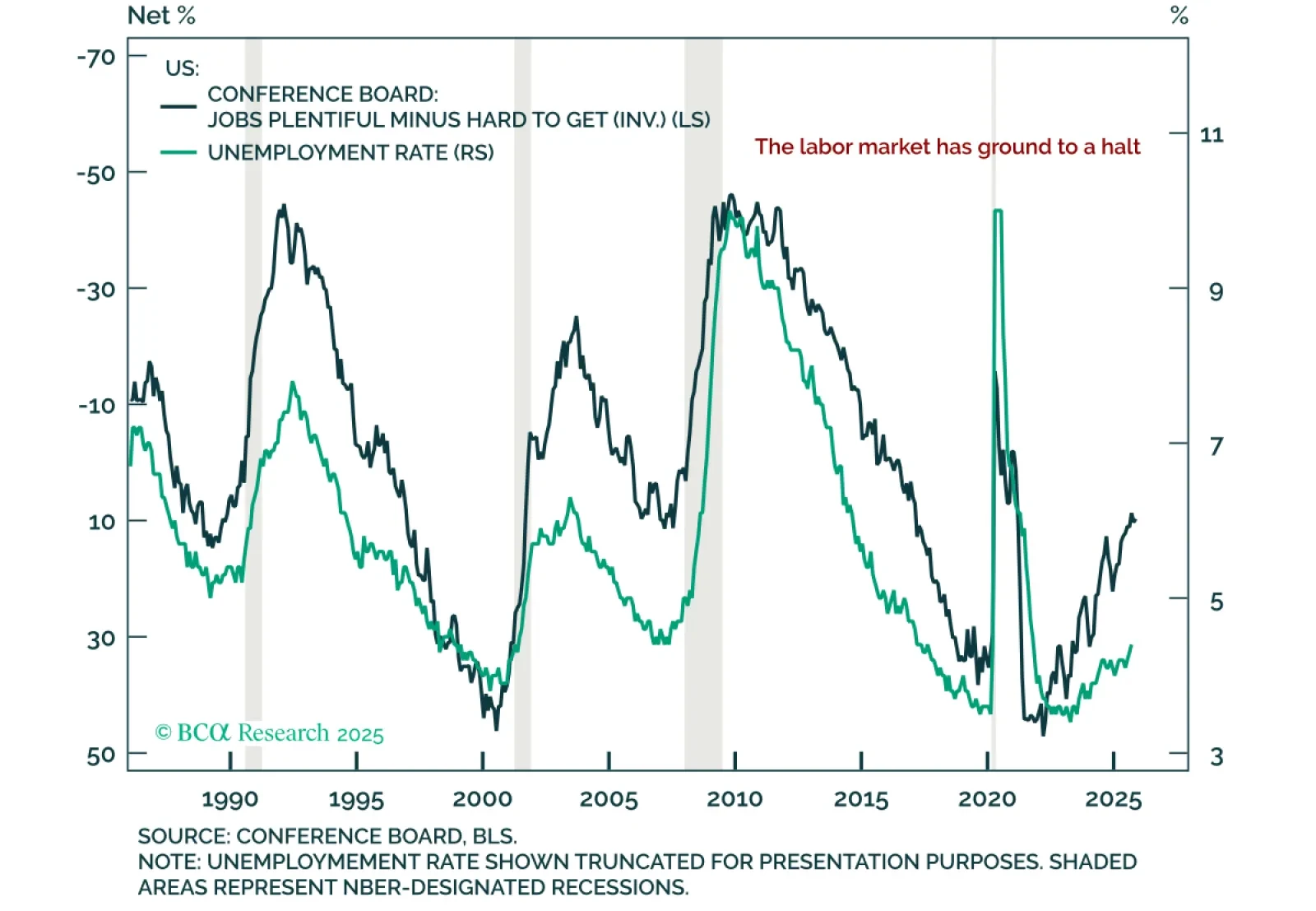

The Beige Book’s indicates that the risk of rising unemployment is greater than that of higher inflation. The November report showed a relatively unchanged US economy, with overall activity little changed. Consumer spending declined further, consistent with…

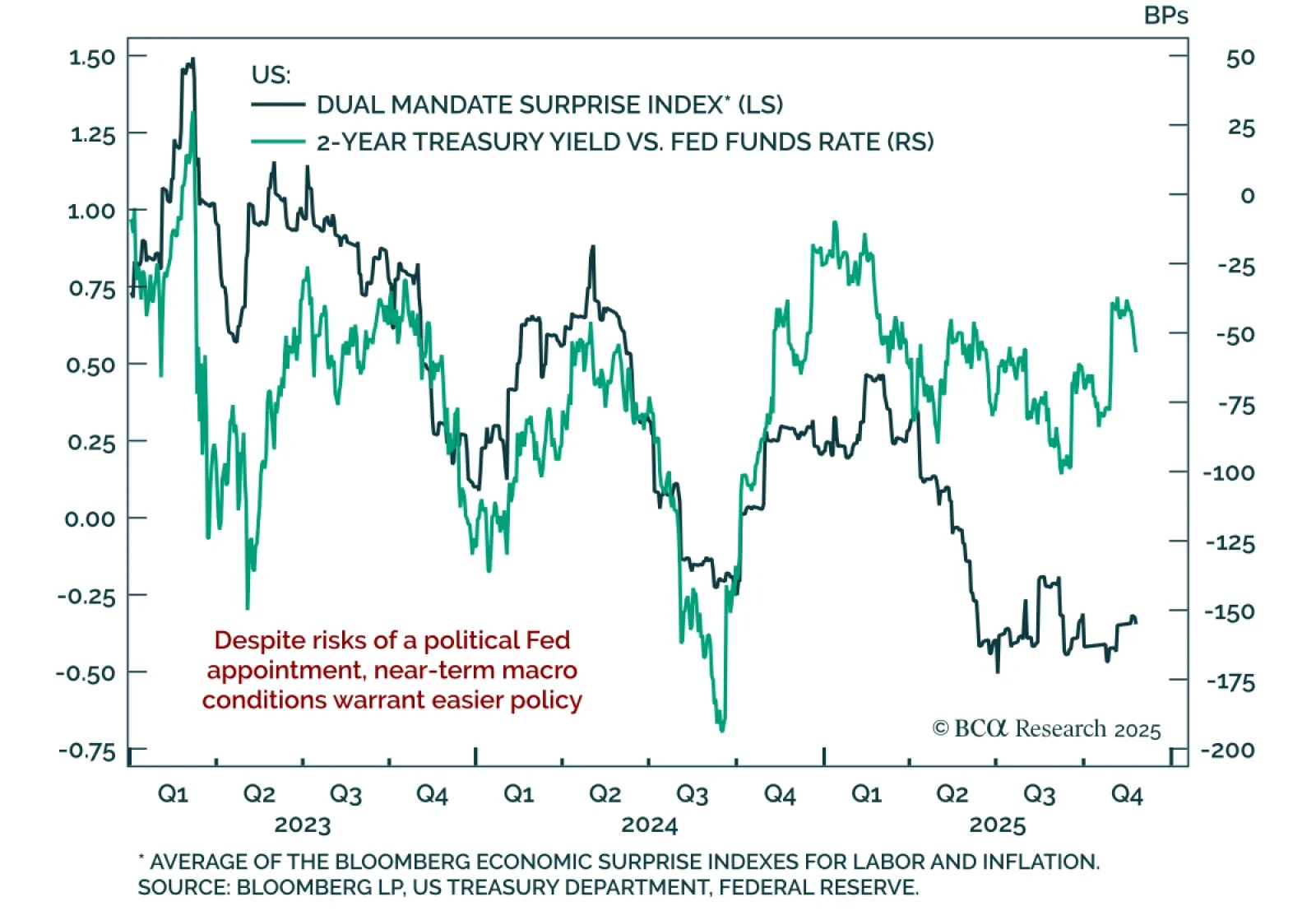

A politically aligned Fed nominee would likely receive a grace period, but investors should still add inflation hedges to their strategic allocation. New reporting indicates that current WH NEC Director Kevin Hassett is the frontrunner to succeed Chair…

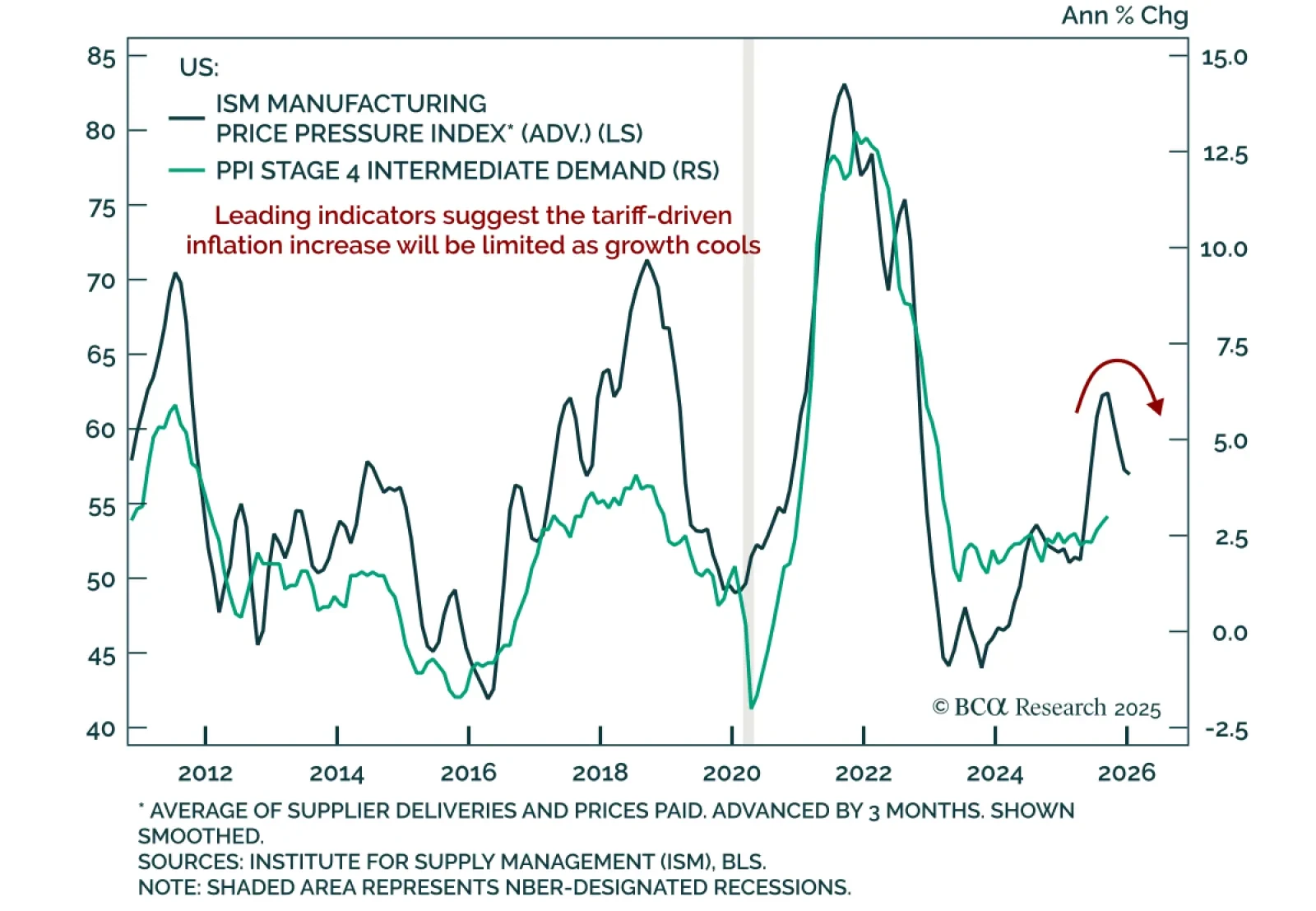

The September PPI report came in cooler than expected, reinforcing limited inflation pressures and supporting underweights in TIPS versus nominals Treasuries. Headline PPI rose 0.3% m/m after a 0.1% decline in August, while core PPI excluding food, energy,…

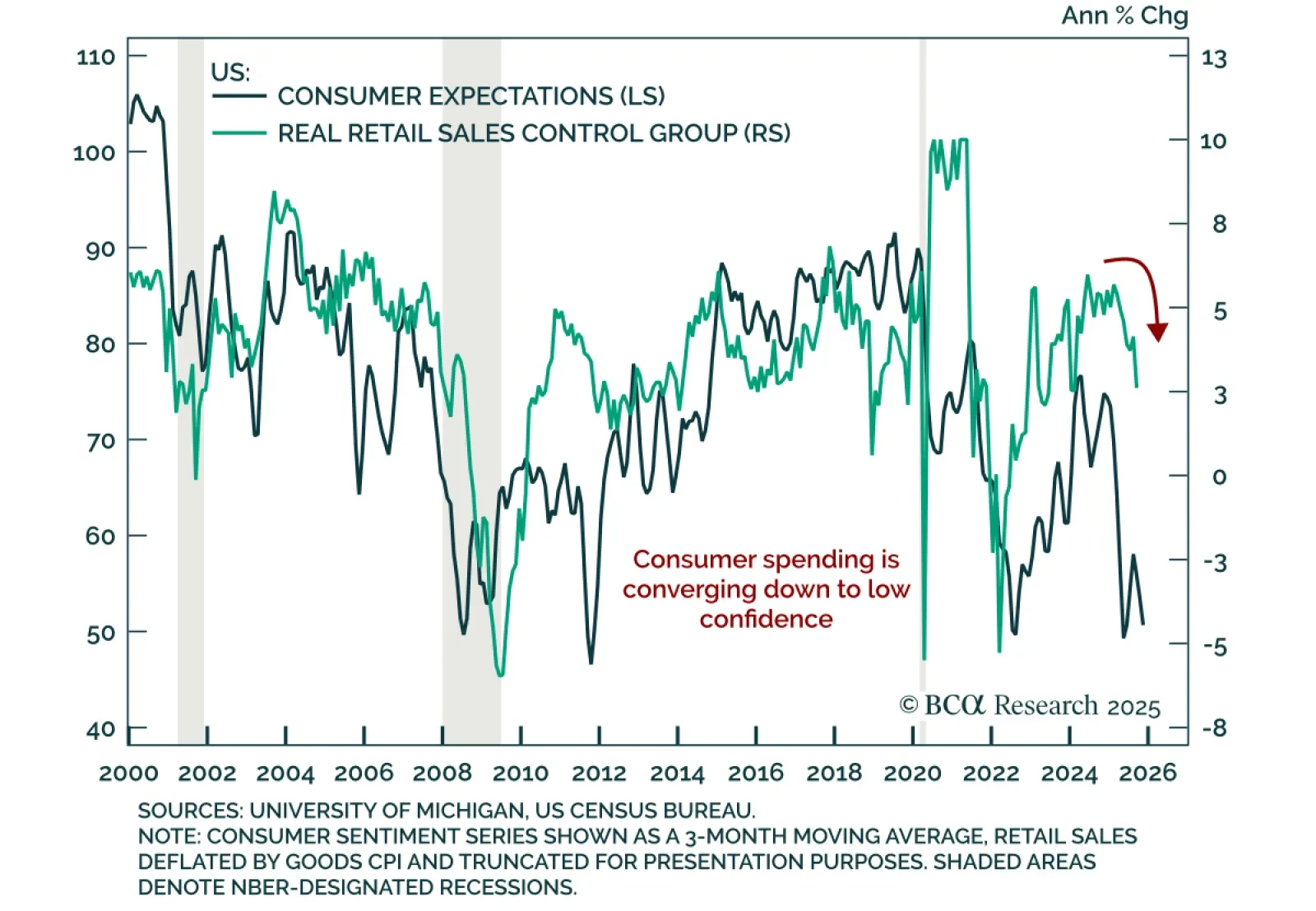

US September retail sales disappointed, reinforcing signs of slowing consumption and warranting a modestly defensive positioning. Headline sales rose 0.2% m/m, down from 0.6% in August, while core sales excluding autos and gas grew just 0.1%, down from a…

The November Conference Board Consumer Confidence Index fell again, underscoring a weak but not collapsing economy that keeps the Fed on track to ease. The index dropped to 88.7 from 95.5, with both the present situation (126.9 from 131.2) and expectations…

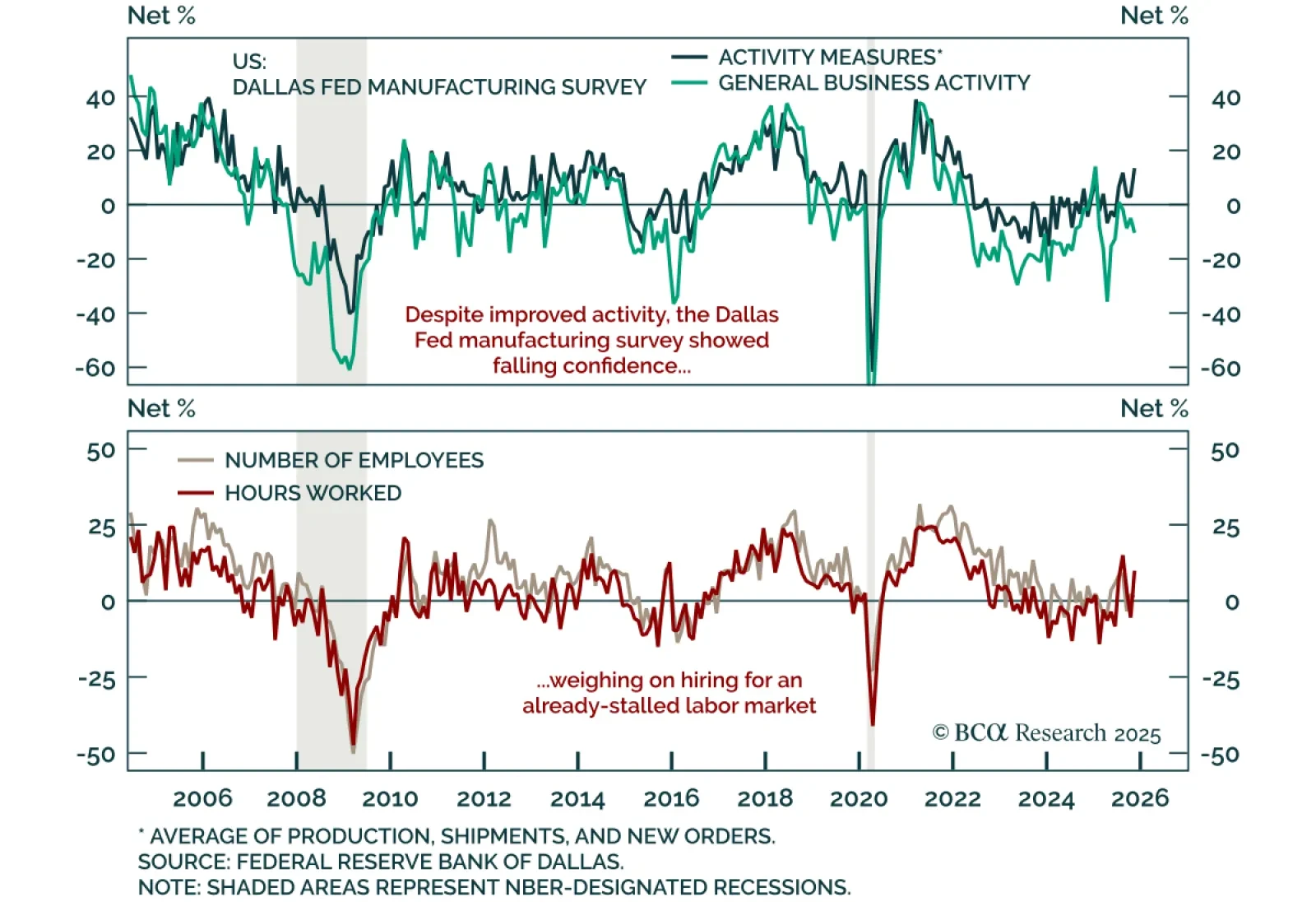

The November Dallas Fed manufacturing survey painted a mixed picture, with softer business sentiment but improving production and stable employment. The headline index fell to -10.4 from -5.0, while the production component jumped 15 points to 20.5, showing…

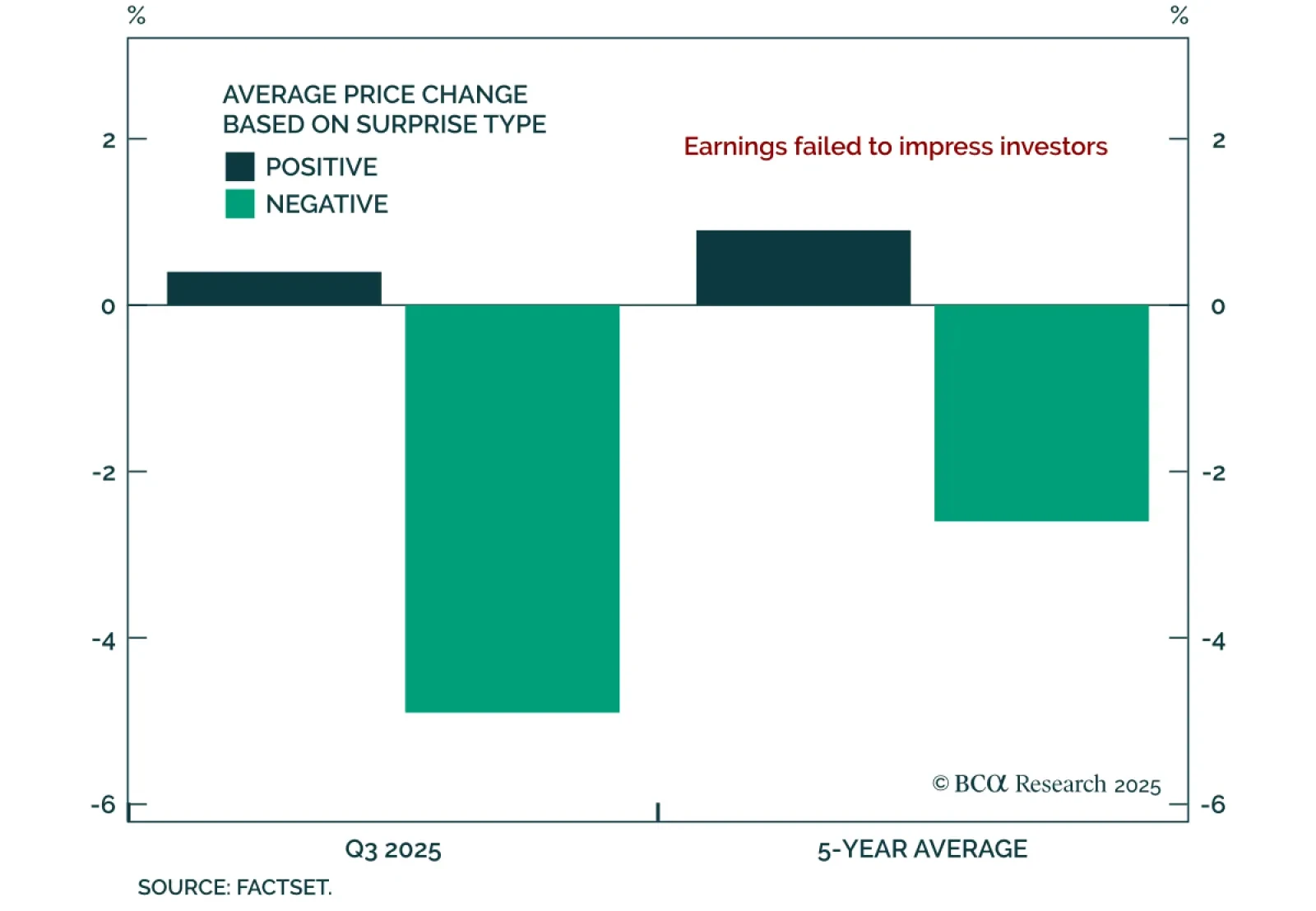

Our US Equity strategists remain equal weight Consumer Services and underweight Consumer Staples, as Q3 earnings revealed widening performance gaps across income segments. Results were solid on both revenue and earnings, but with valuations already stretched,…

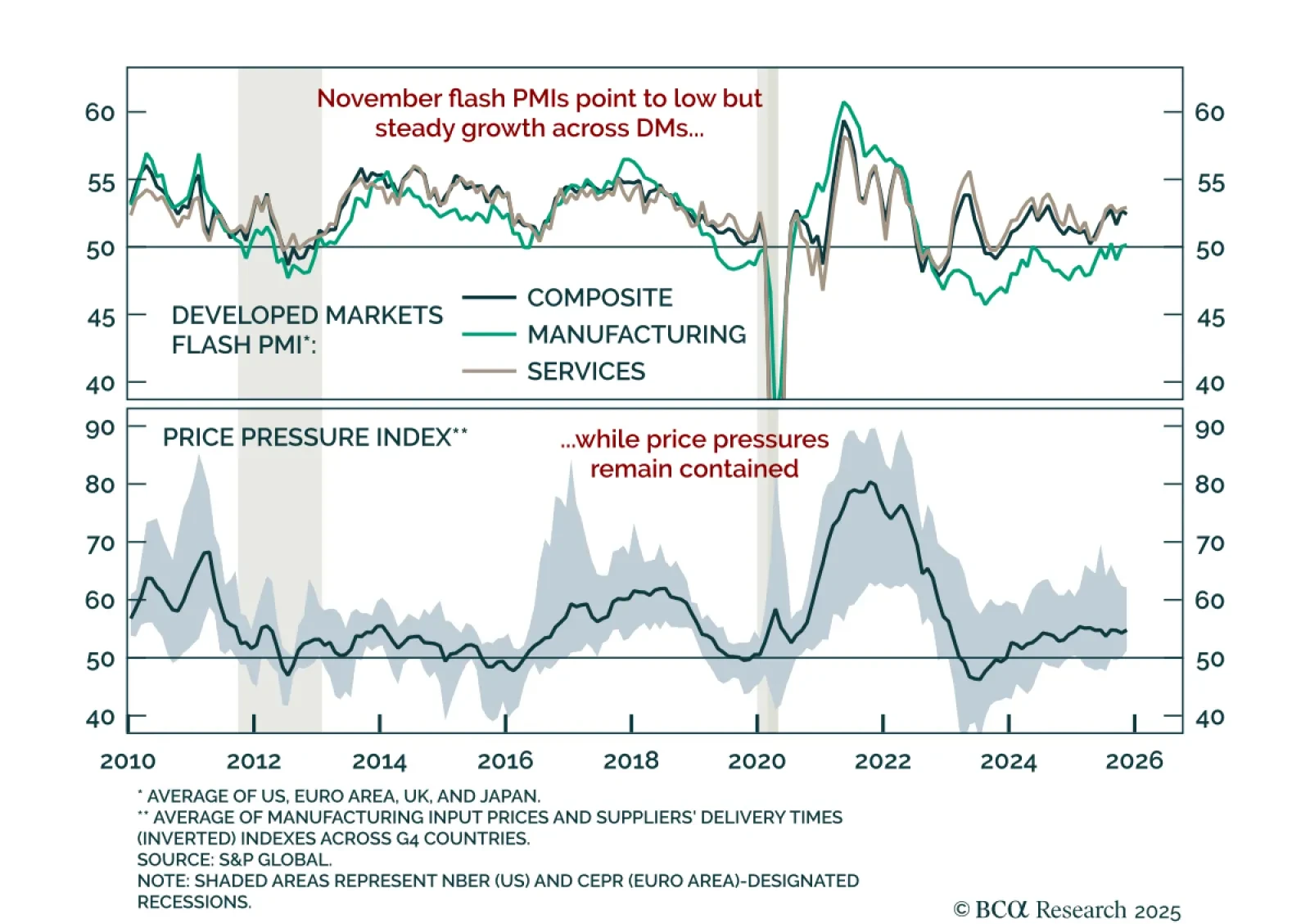

November flash PMIs confirmed sluggish global momentum, reinforcing a defensive stance with tactical support for the USD. The US composite PMI rose to 54.8, driven by stronger services but weaker manufacturing. The Euro area showed a similar pattern, with…

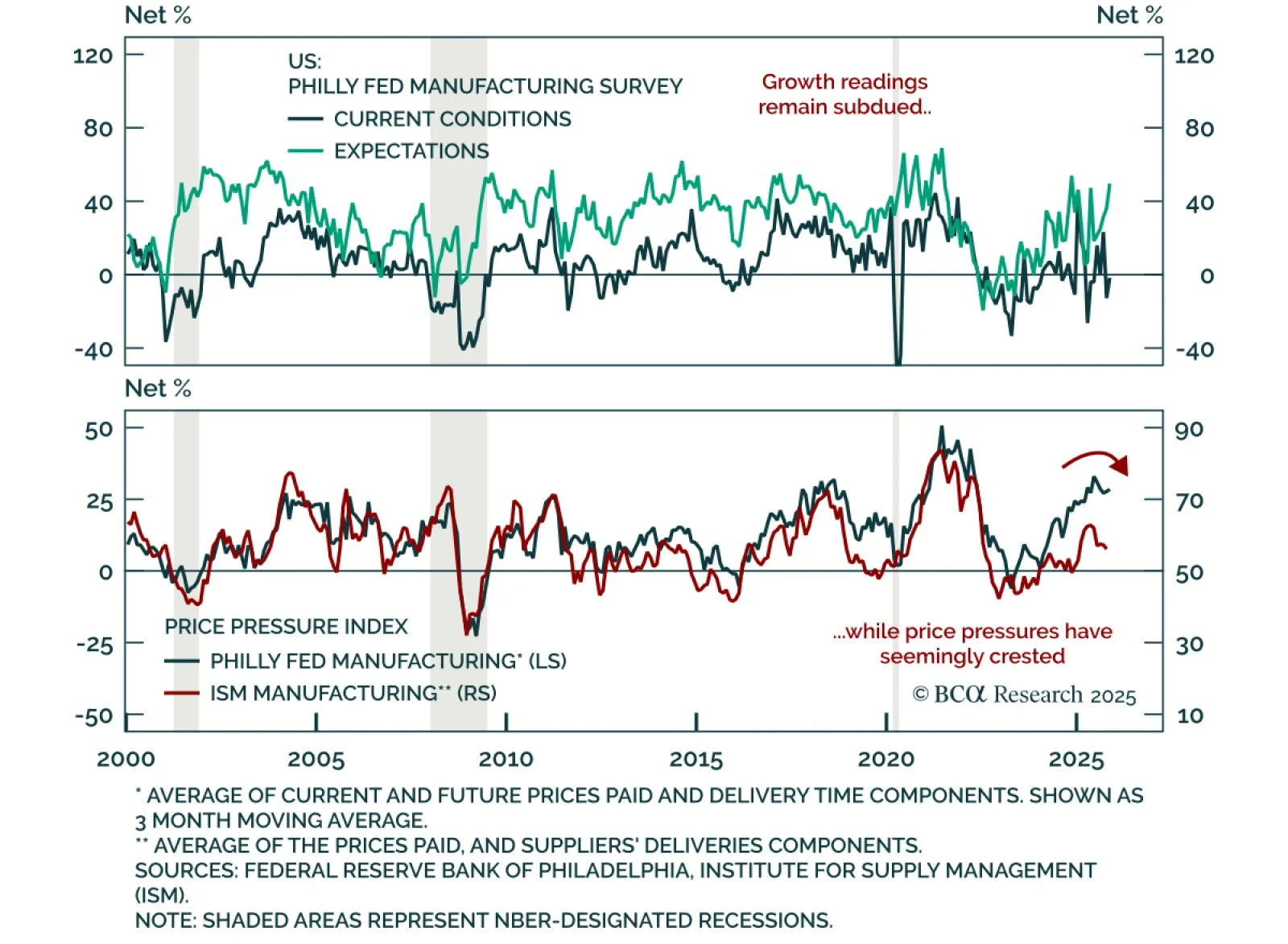

The November Philadelphia Fed survey missed expectations, showing manufacturing activity remains subdued with little momentum. Although the headline index rose to -1.7 from -12.8, new orders and shipments both slipped into contraction. Employment and hours…