United States

The Fed is on hold for now, but its 2026 economic projections are far too optimistic. The Fed will ease more next year than it currently anticipates.

Maintain a long duration stance and favor curve steepeners as the Fed’s outlook remains too optimistic relative to ongoing labor and growth deterioration. The Fed cut rates by 25 bps to 3.5%–3.75%. The decision again drew two-sided dissents: Governor Miran…

Maintain a modestly defensive stance as cooling wage growth reinforces labor-market weakness. The delayed Q3 Employment Cost Index missed estimates, slowing to 0.8% q/q. The “core” ECI measure, which excludes incentives-paid occupations and provides a clearer…

We are constructive on equities in 2026, as monetary easing, fiscal support, GenAI-related capex, and strong earnings growth are unequivocally positive for the asset class. Valuations are extended, but concerns about a bubble are overstated. Despite the favorable backdrop, we expect the S&P 500 to return only 5–10%, ending 2026 between 7,200 and 7,500.

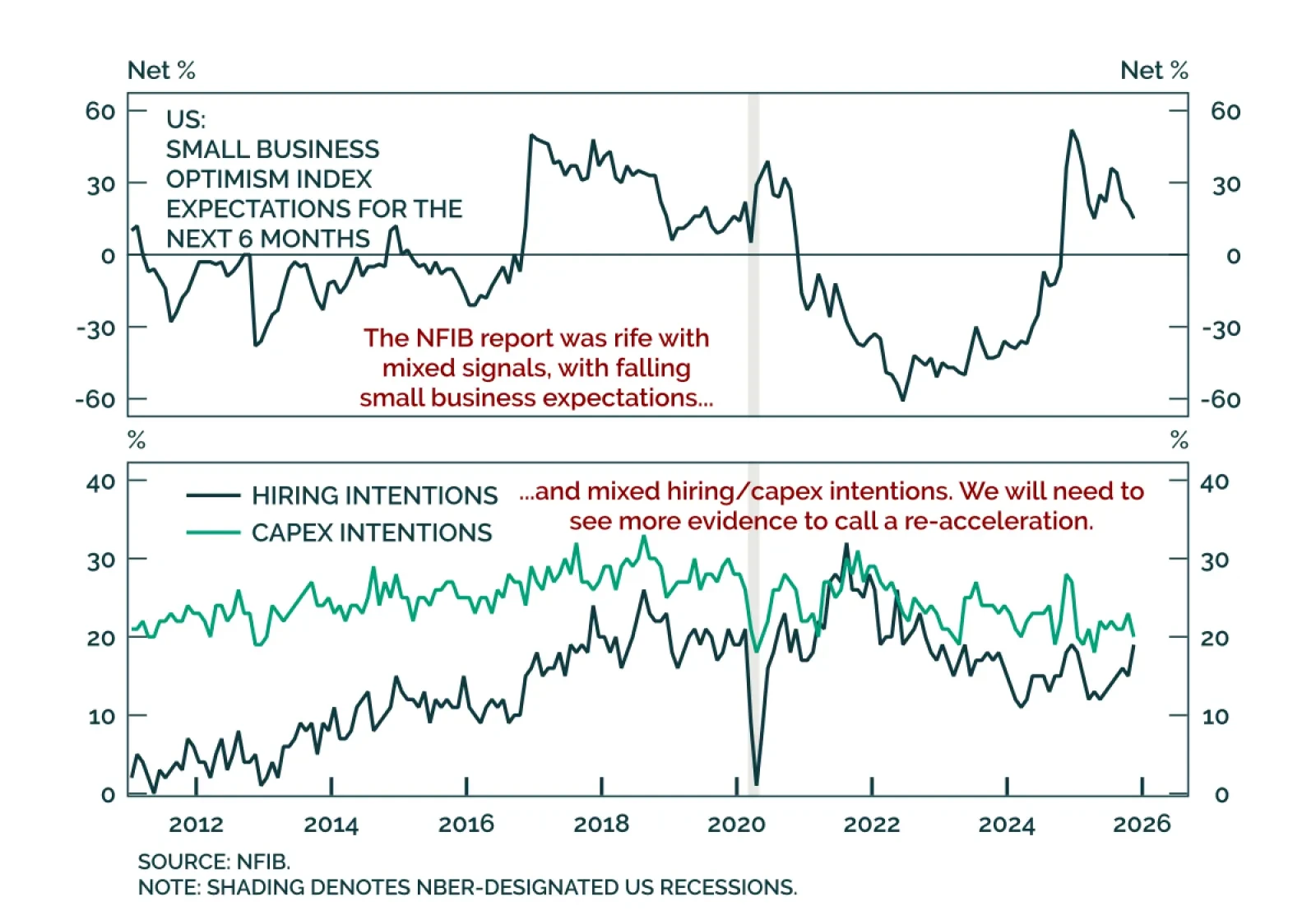

Maintain a modestly defensive stance as the NFIB shows no signs of a growth or labor-market re-acceleration. The November NFIB Small Business Optimism Index beat estimates, rising to 99.0 from 98.2 and slightly above its long-term average, but underlying…

Maintain long duration and favor tactical steepeners as the JOLTS data show no evidence of a labor-market re-acceleration. The delayed October JOLTS report showed job openings rising slightly to 7.67m from 7.66m, but underlying details do not point to renewed…

Watch the shift in correlation between equities and the USD; a positive co-movement will carry major implications for asset allocation and hedging. Shifting correlations have been a defining theme of the year. They often signal regime change. Correlations…

Our US and Geopolitical strategists delivered accurate calls on Trump’s tariff shock and Israel’s strike on Iran in 2025 but missed the China equity rally and overestimated near-term prospects for a Ukraine ceasefire. Their 2025 outlook correctly anticipated…

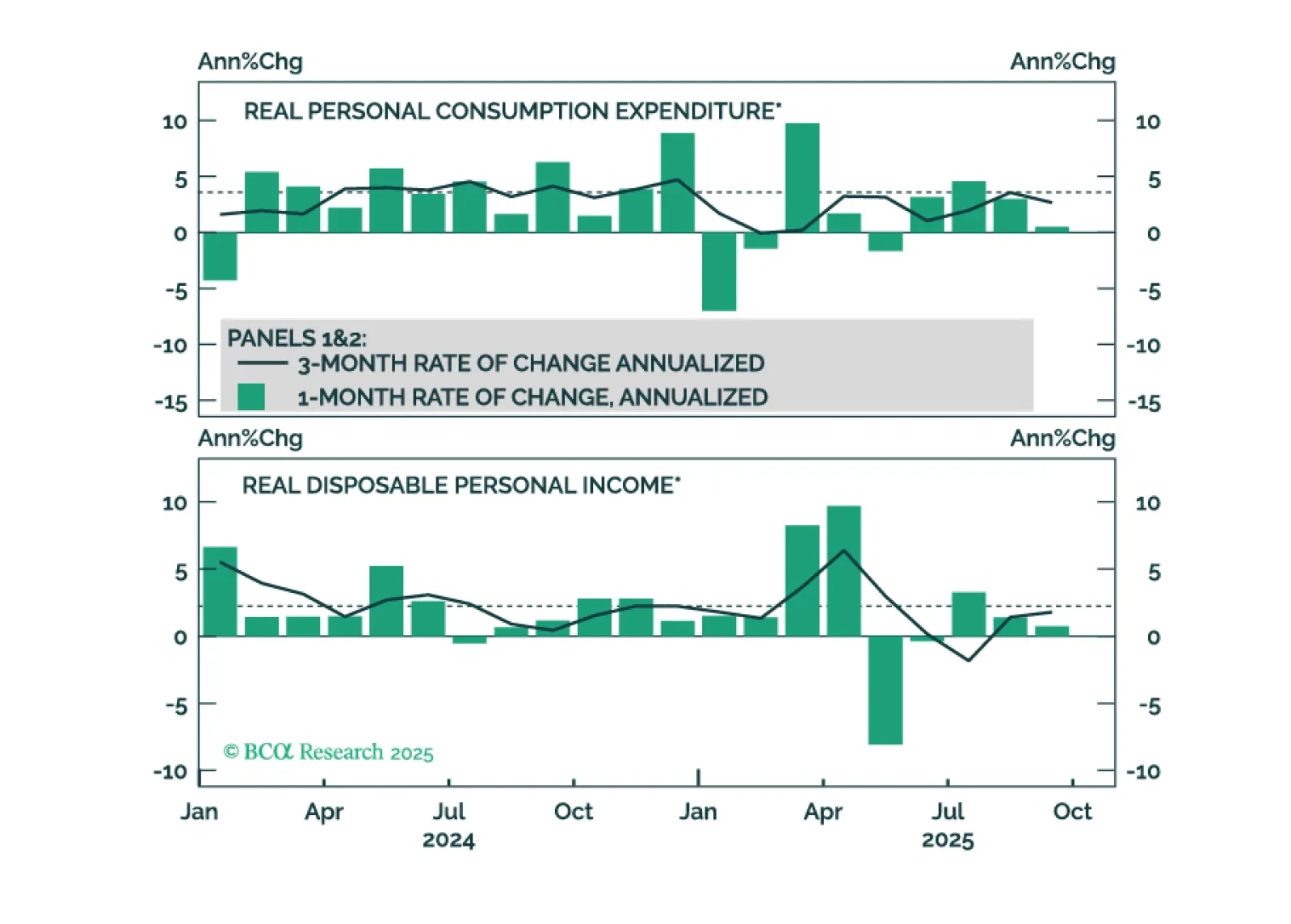

Expect more Fed easing than priced as stalled labor momentum and fragile consumption limit inflation pressure. The delayed September Personal Income & Outlays report showed a weaker picture than expected. Nominal income and spending beat estimates, but…

September’s weak consumer spending data challenge the K-shaped recovery narrative and suggest that spending will slow to match already-weak employment growth.