United States

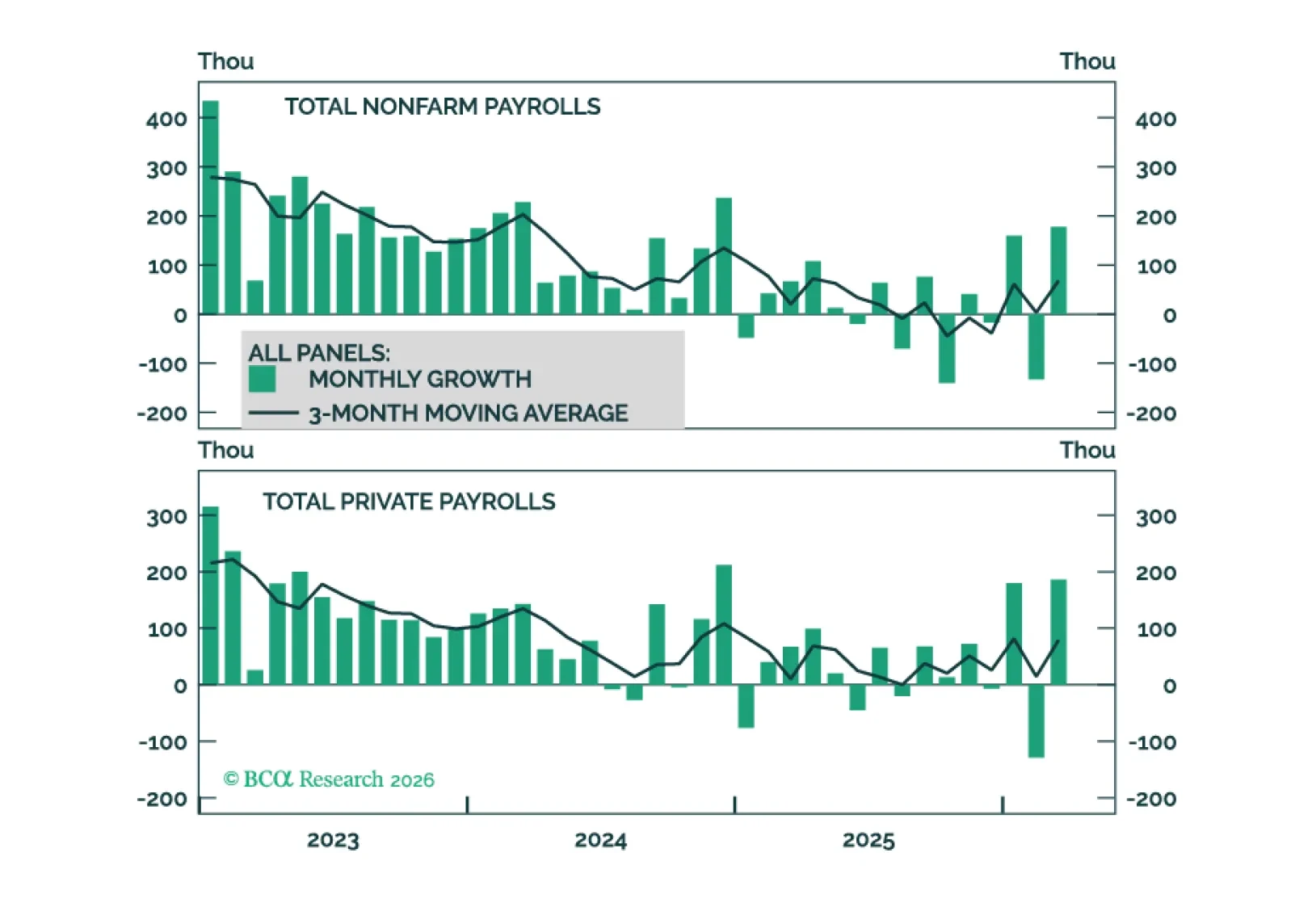

US employment data show some tentative signs of job growth acceleration and stable utilization. We see breakeven monthly job growth as closer to +30k per month than zero.

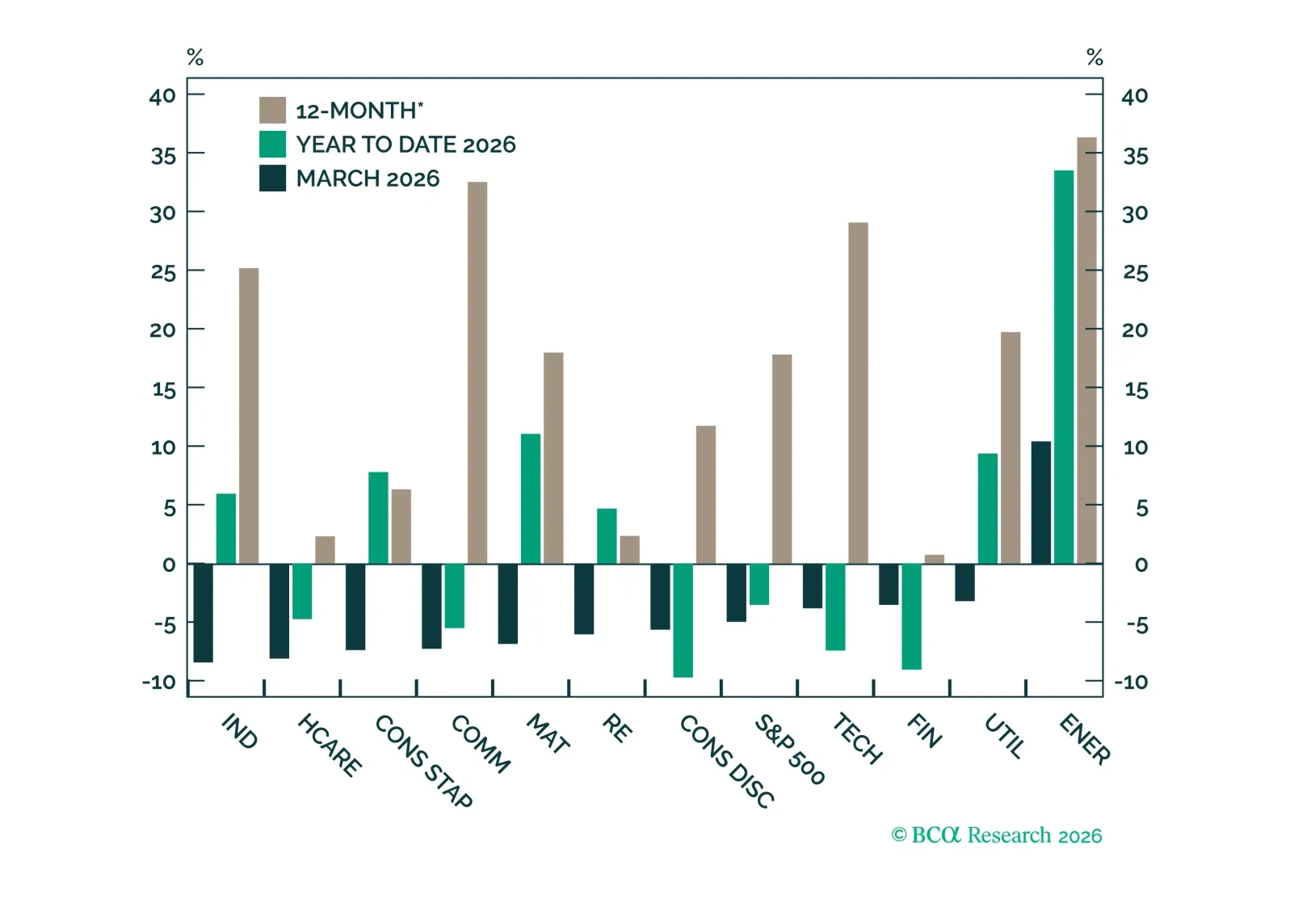

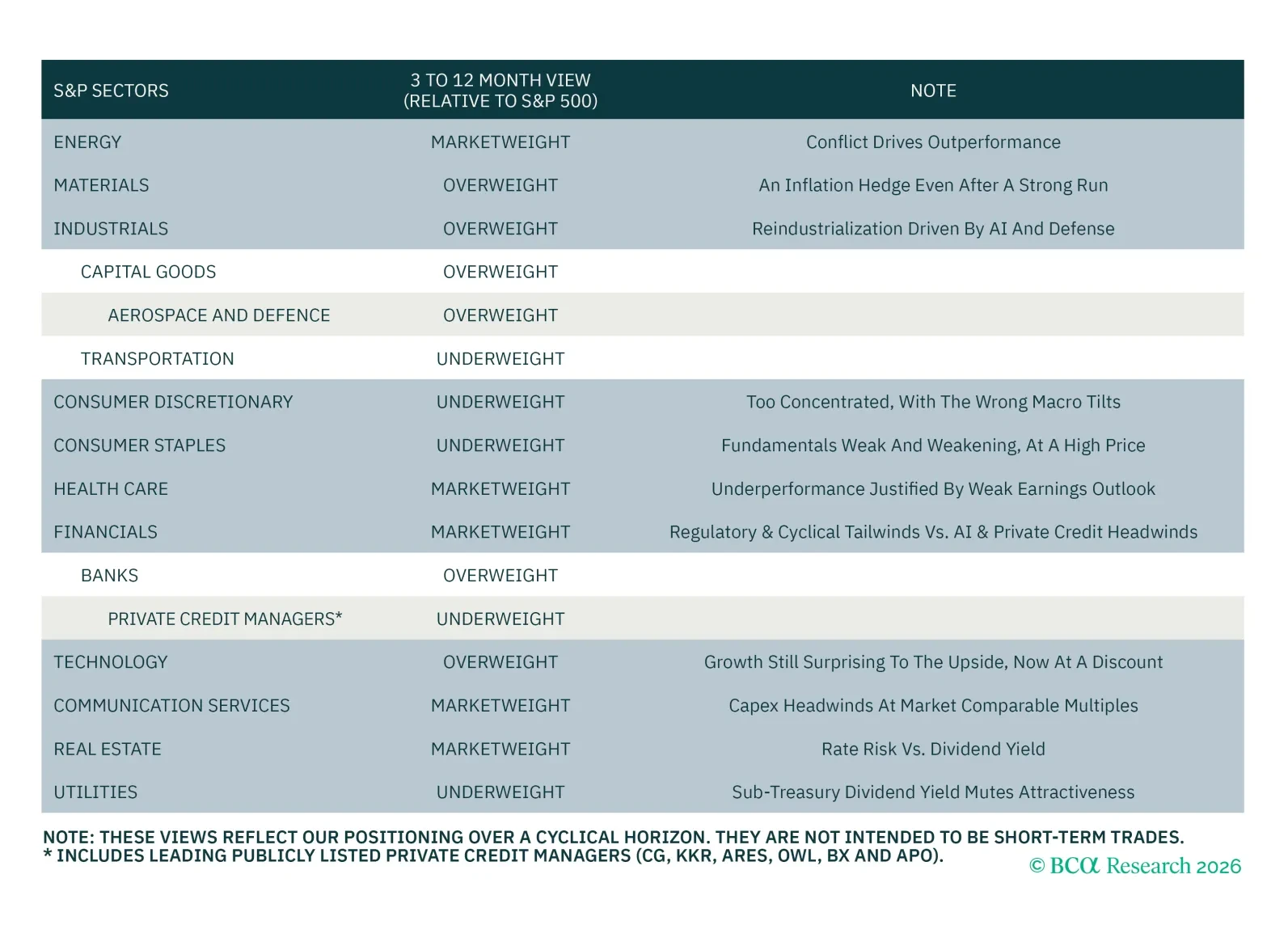

We expect the S&P 500 to deliver $308 of EPS in 2026, with a year-end target of 7700. Revenue growth drives upside, with little margin or multiple expansion. With economic growth tilted toward investment, we are overweight Technology, Industrials, and Materials, market-weight Financials, Energy, Health Care, Communication Services, and Real Estate, and underweight Consumer Staples, Consumer Discretionary, and Utilities.

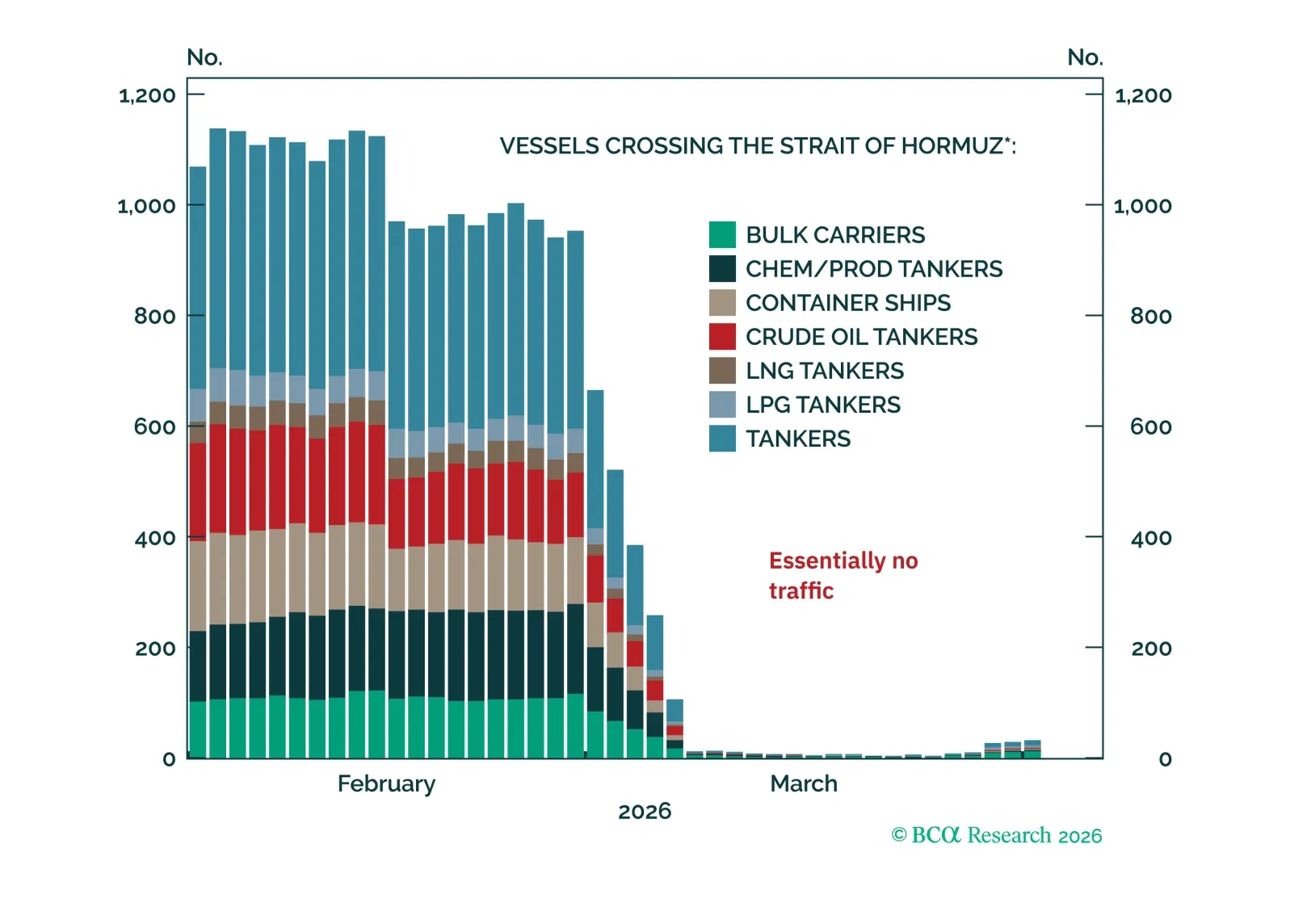

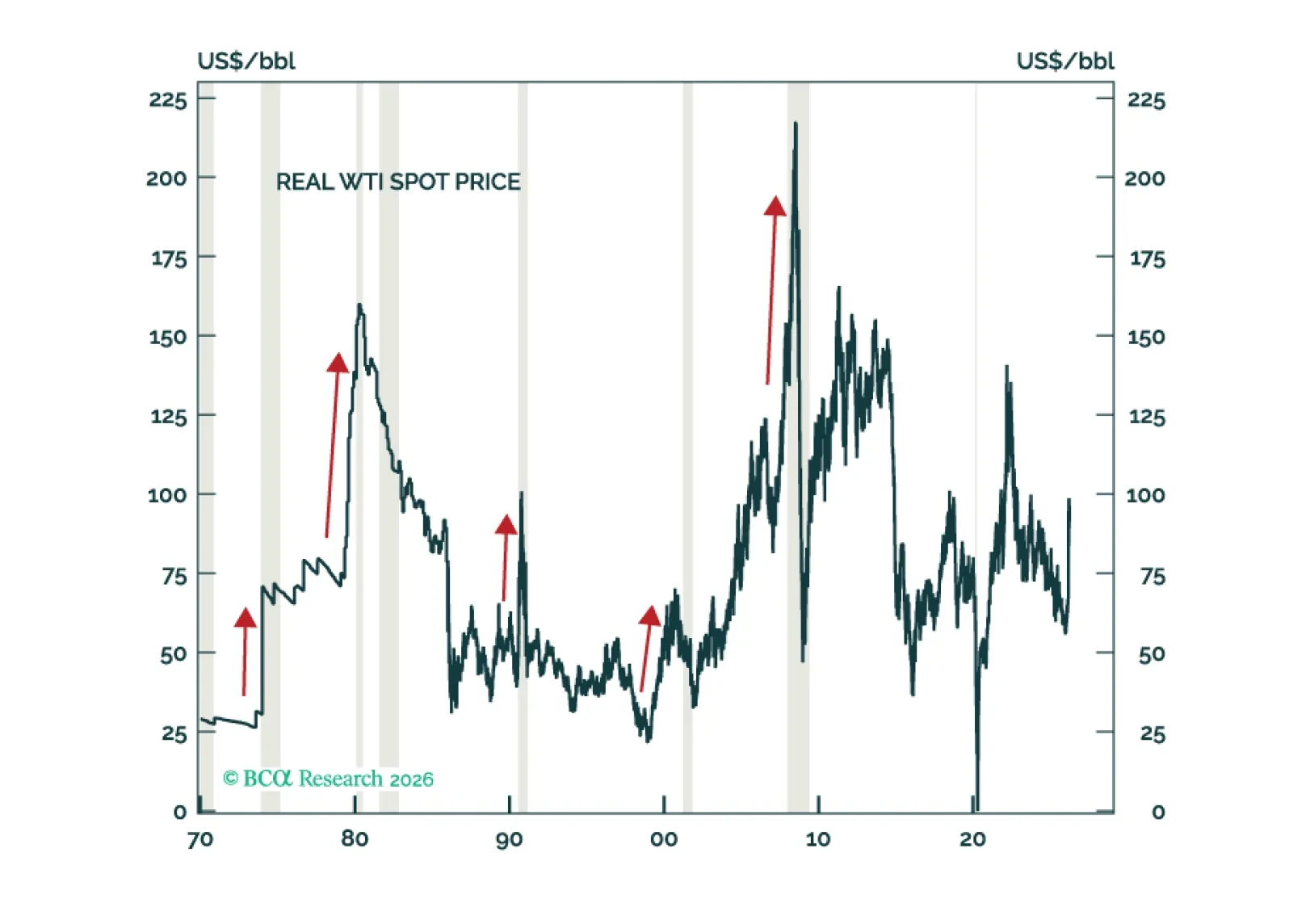

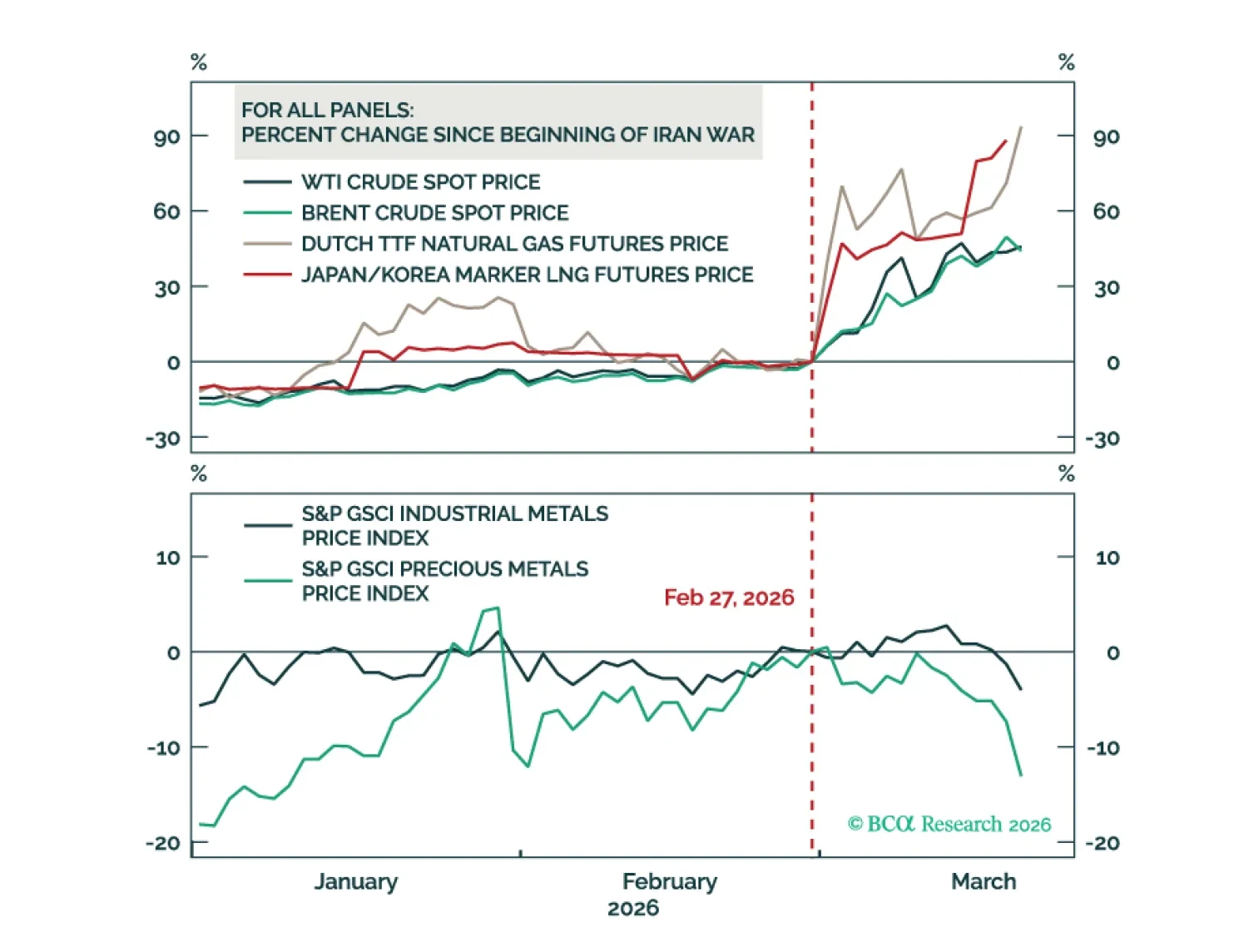

Our "miniature stagflation" episode is coming together on the back of the Iran shock, China slowdown, and American political division.

Our Portfolio Allocation Summary for April 2026.

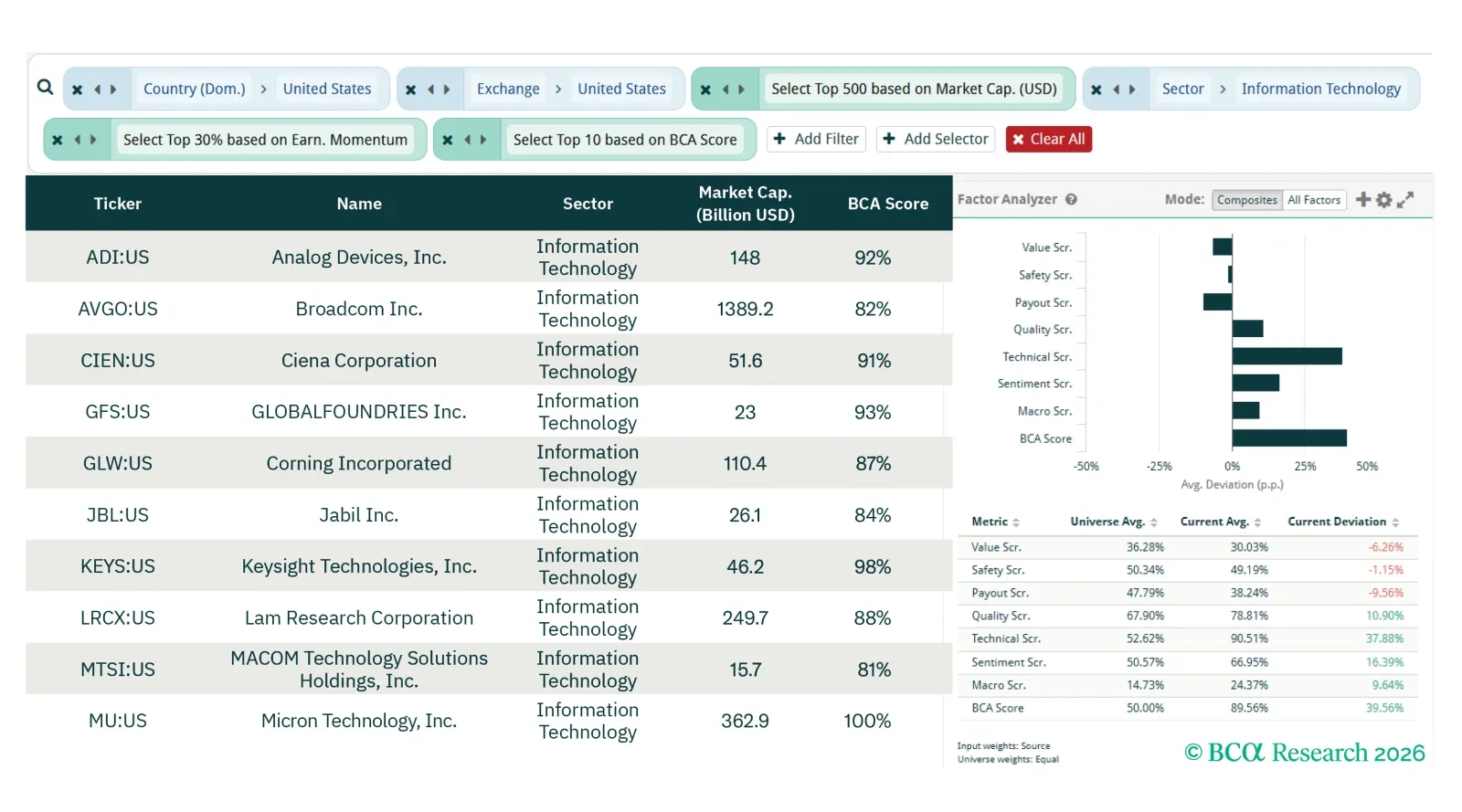

This screener report builds on the US Equity Strategy team's sector view published on 30 March 2026, where the team overweights Information Technology, Industrials, and Materials on a 3- to 12-month horizon. Here we utilize our screening tools to layer bottom-up stock selection onto their top-down sector views.

We continue to expect the S&P 500 to gain ground in 2026, driven by revenue growth, with limited scope for margin or multiple expansion. With cyclical upside tilted toward the investment side of the economy, we favor sectors with high-quality, revenue-driven earnings growth, leverage capex, and valuations that leave room for catch-up.

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

Higher oil prices threaten the global economy, warranting an underweight stance on equities. Over the long haul, industrial metals will fare better than crude.

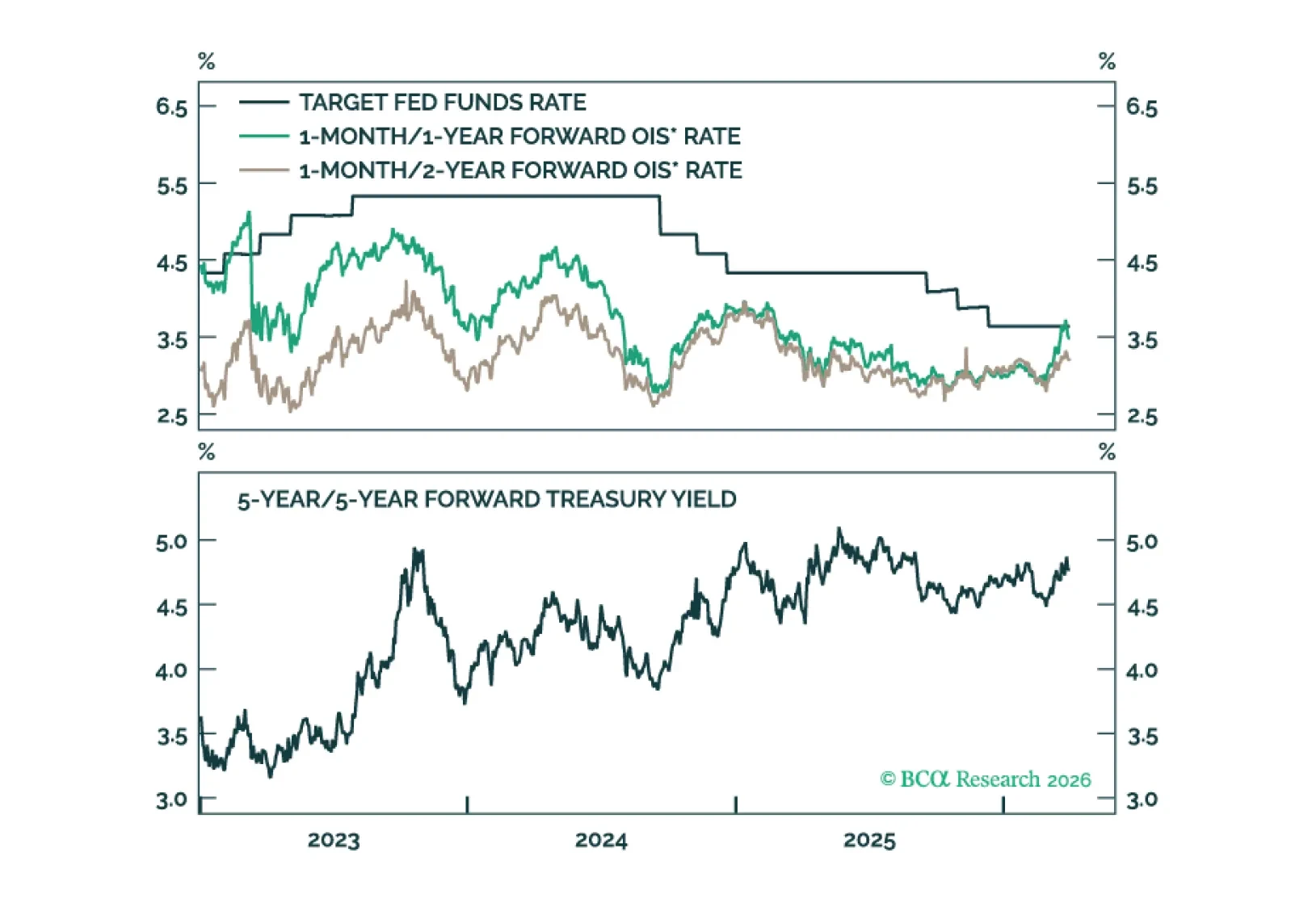

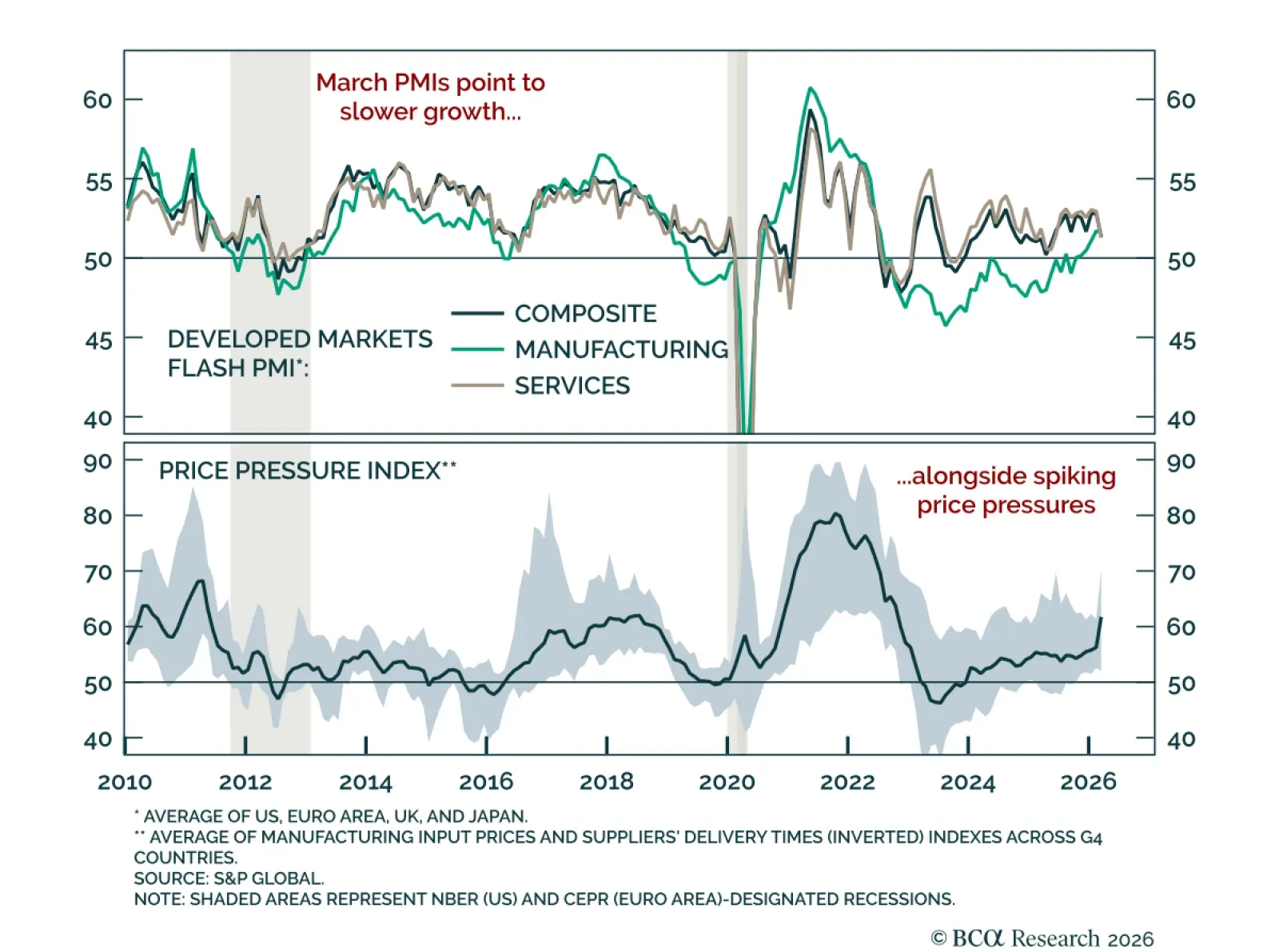

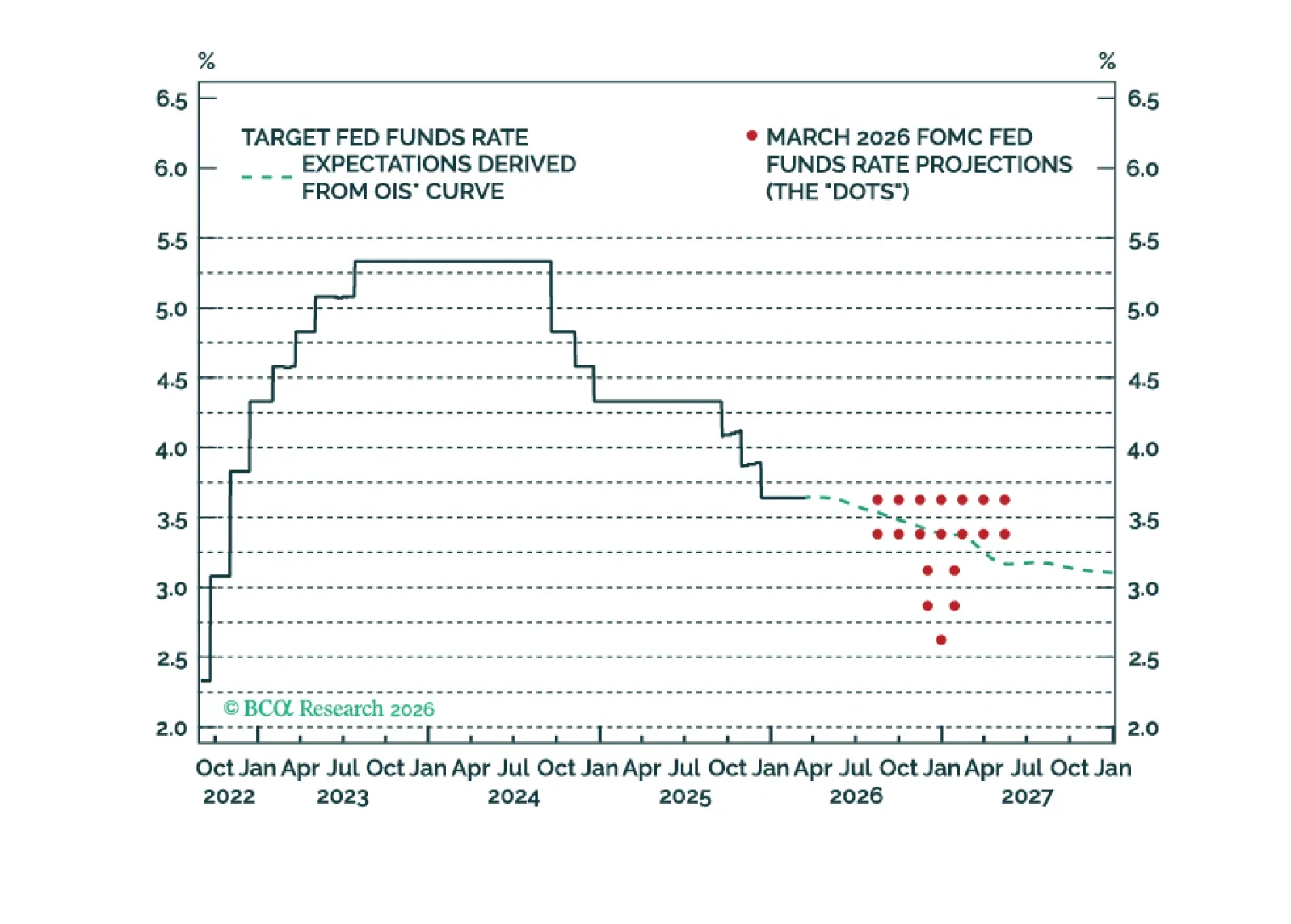

The Fed will not cut rates again until core inflation trends lower. This remains likely as the tariff impact on goods inflation wanes, but the recent energy price shock could delay any meaningful downtrend.