United States

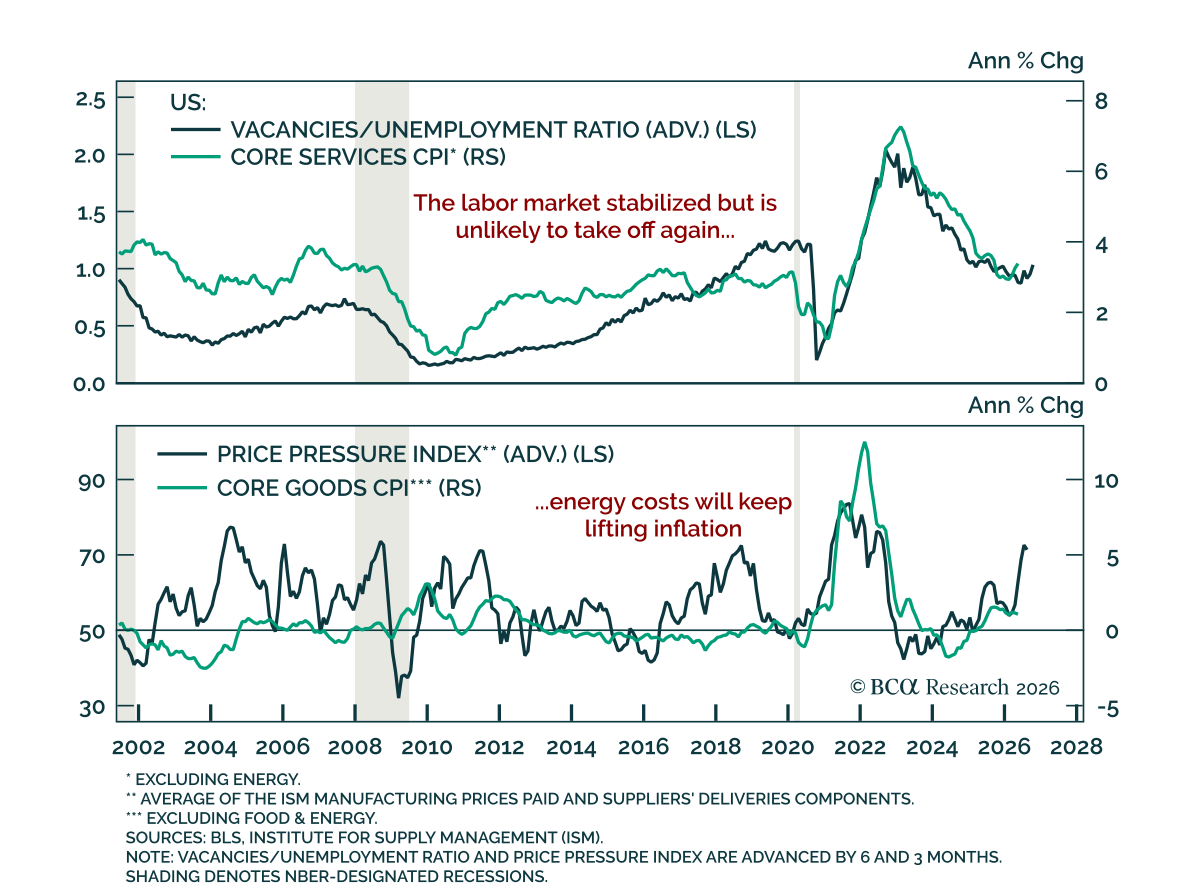

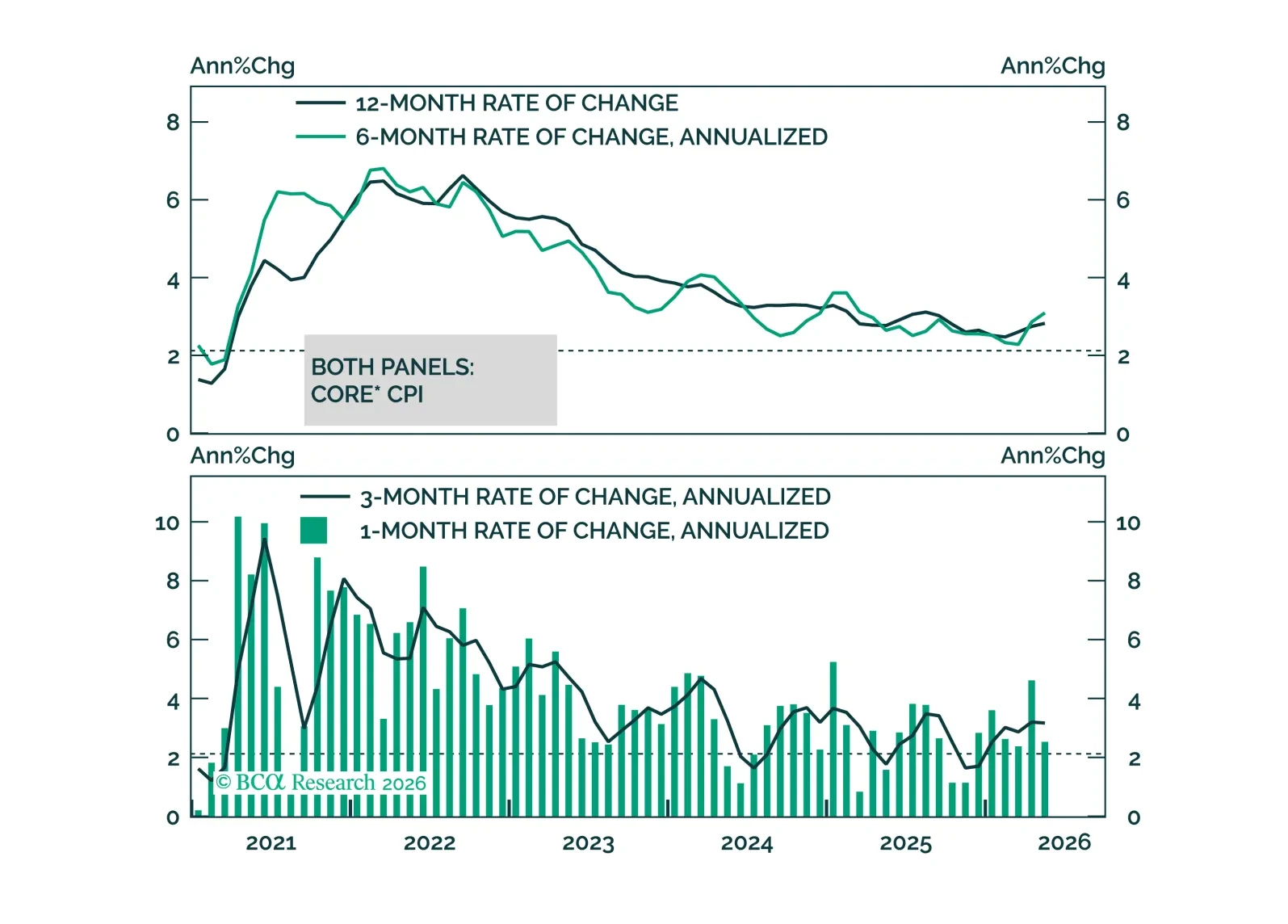

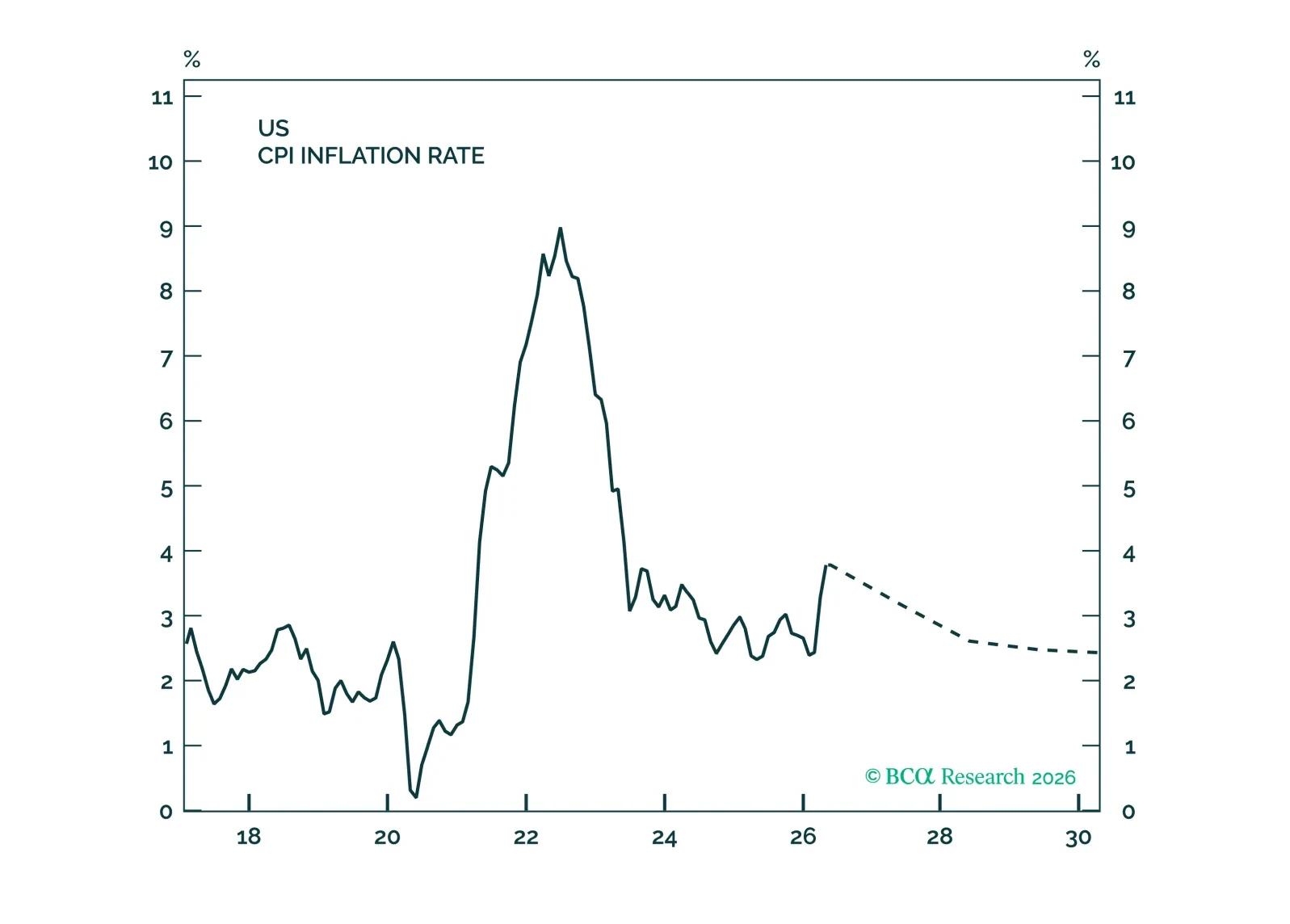

May CPI data show no evidence of passthrough from energy prices to core inflation. This will keep the Fed on hold for the time being.

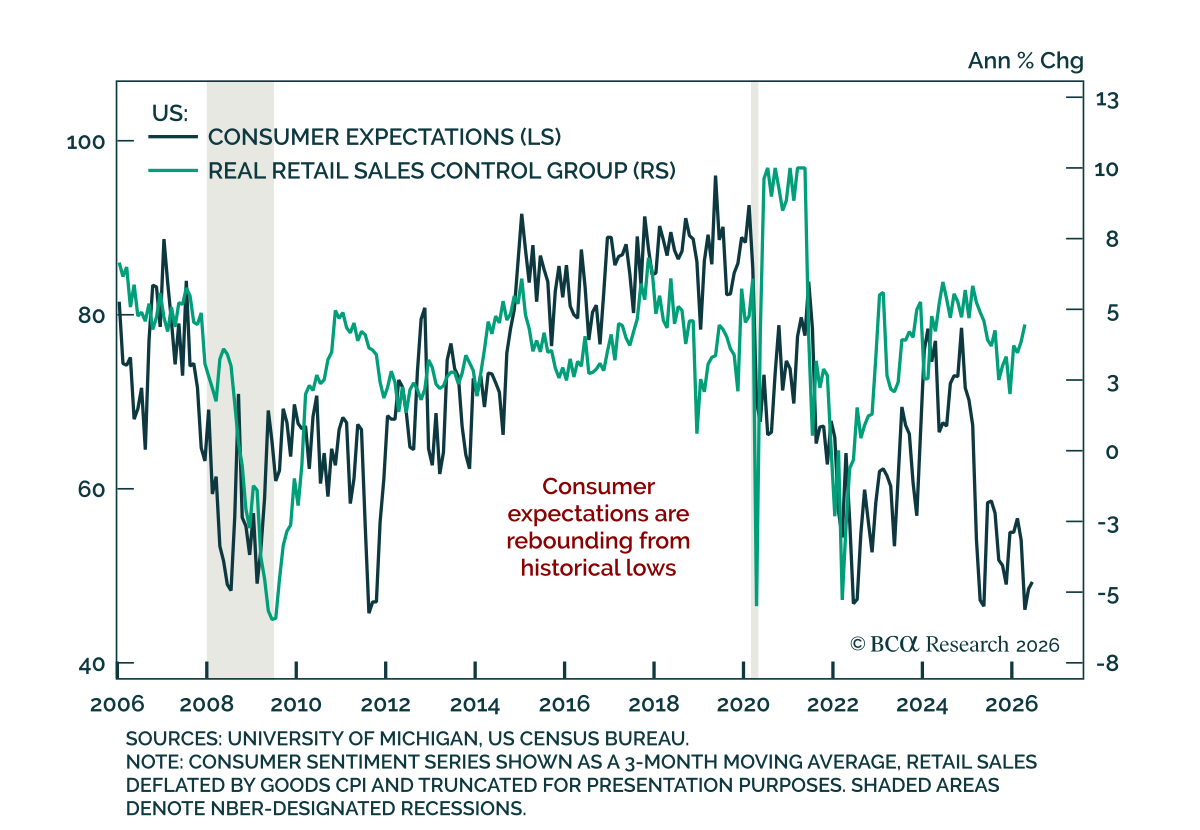

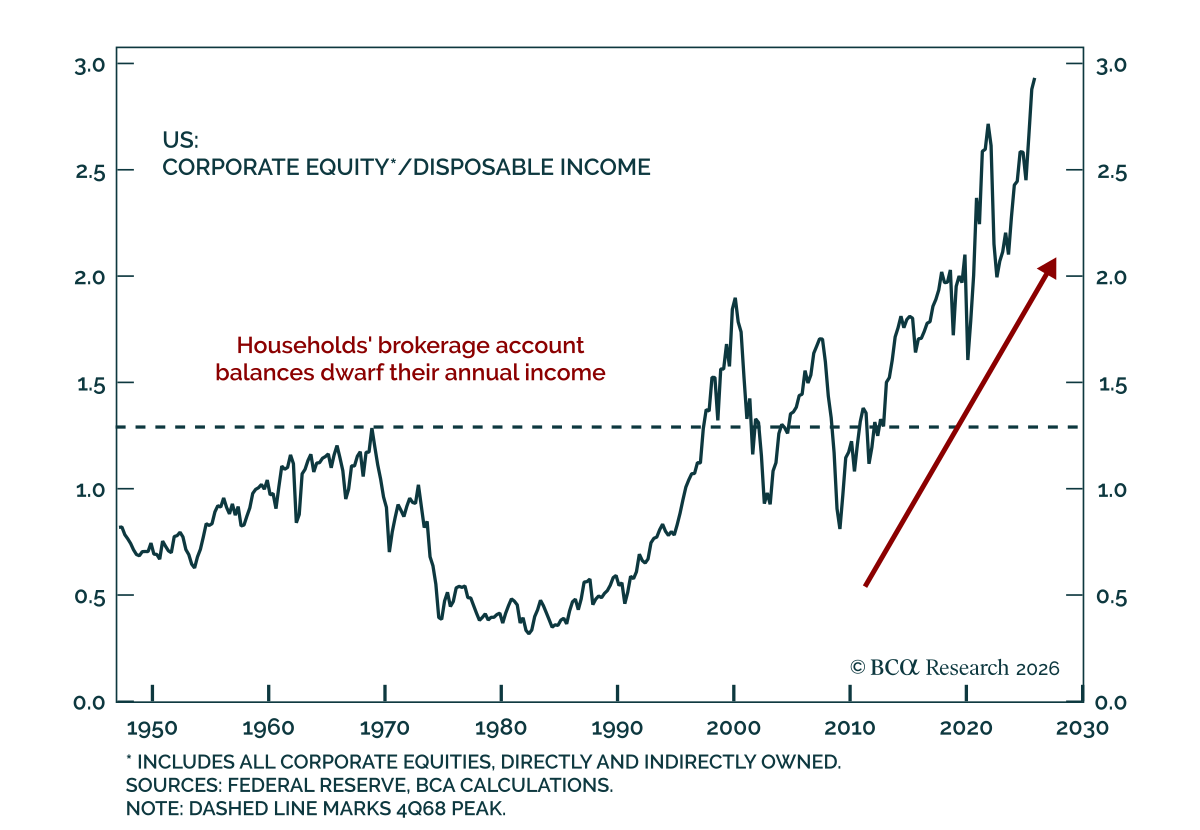

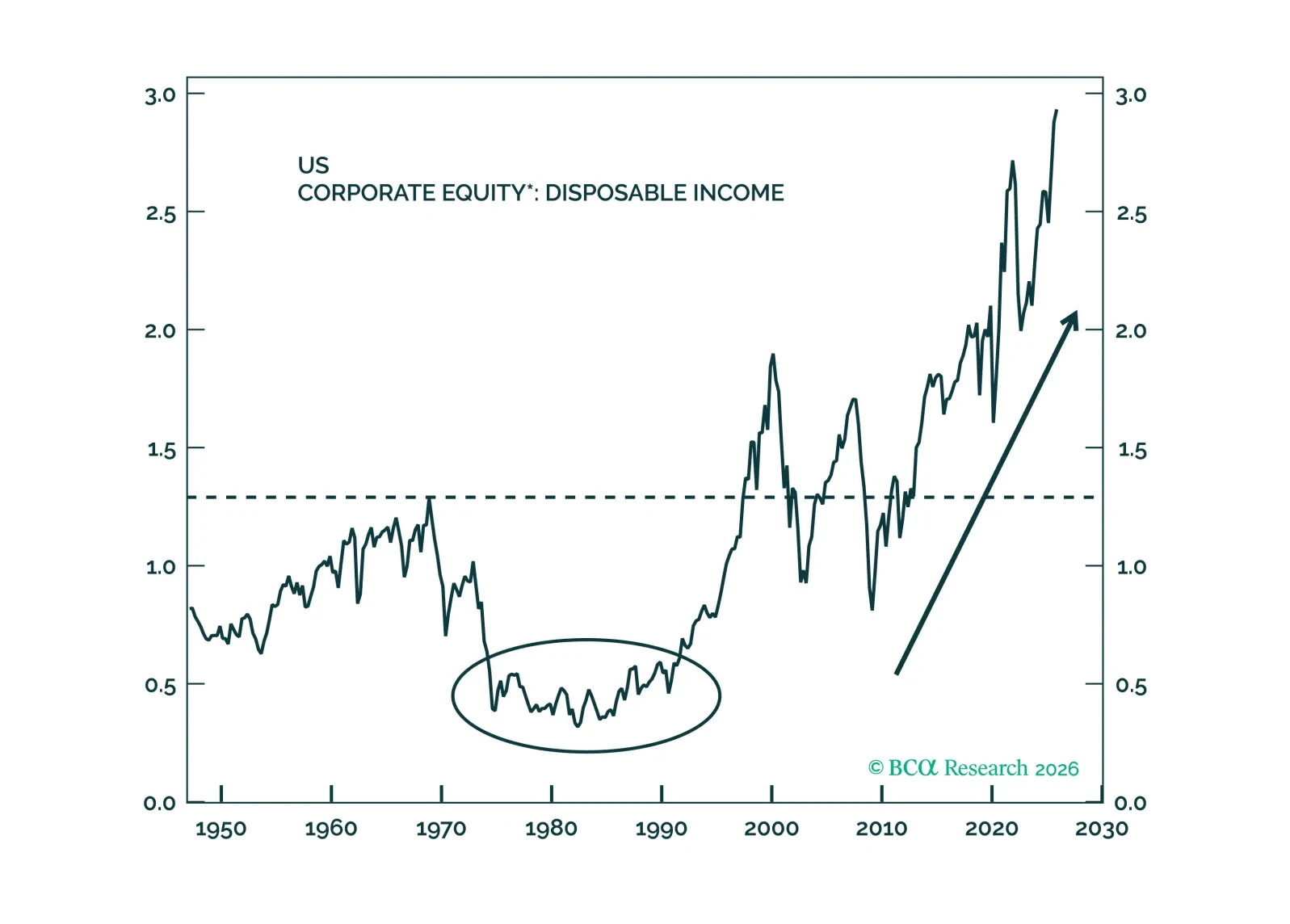

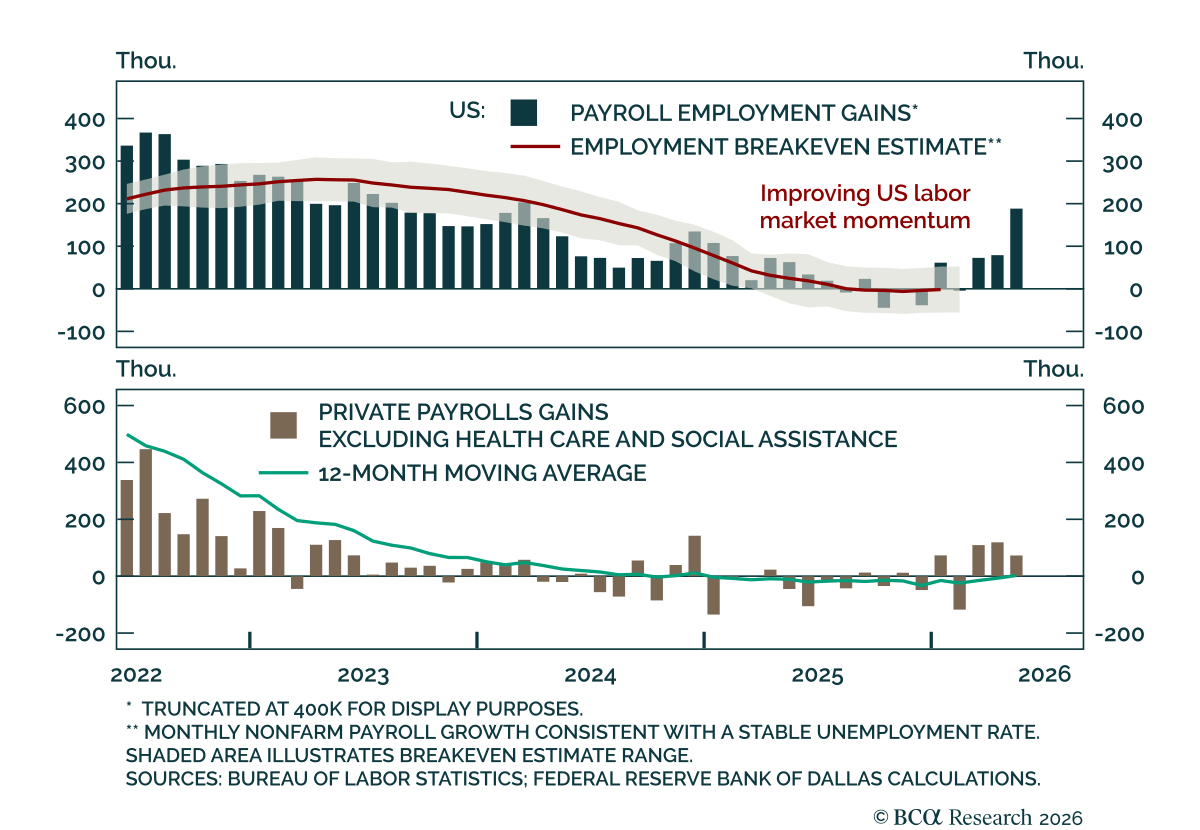

Although the multi-decade surge in the value of households’ equity holdings has made US activity more vulnerable to a stock selloff, the latest income, spending and employment data suggest that consumption growth can carry on at a 2% inflation-adjusted pace.

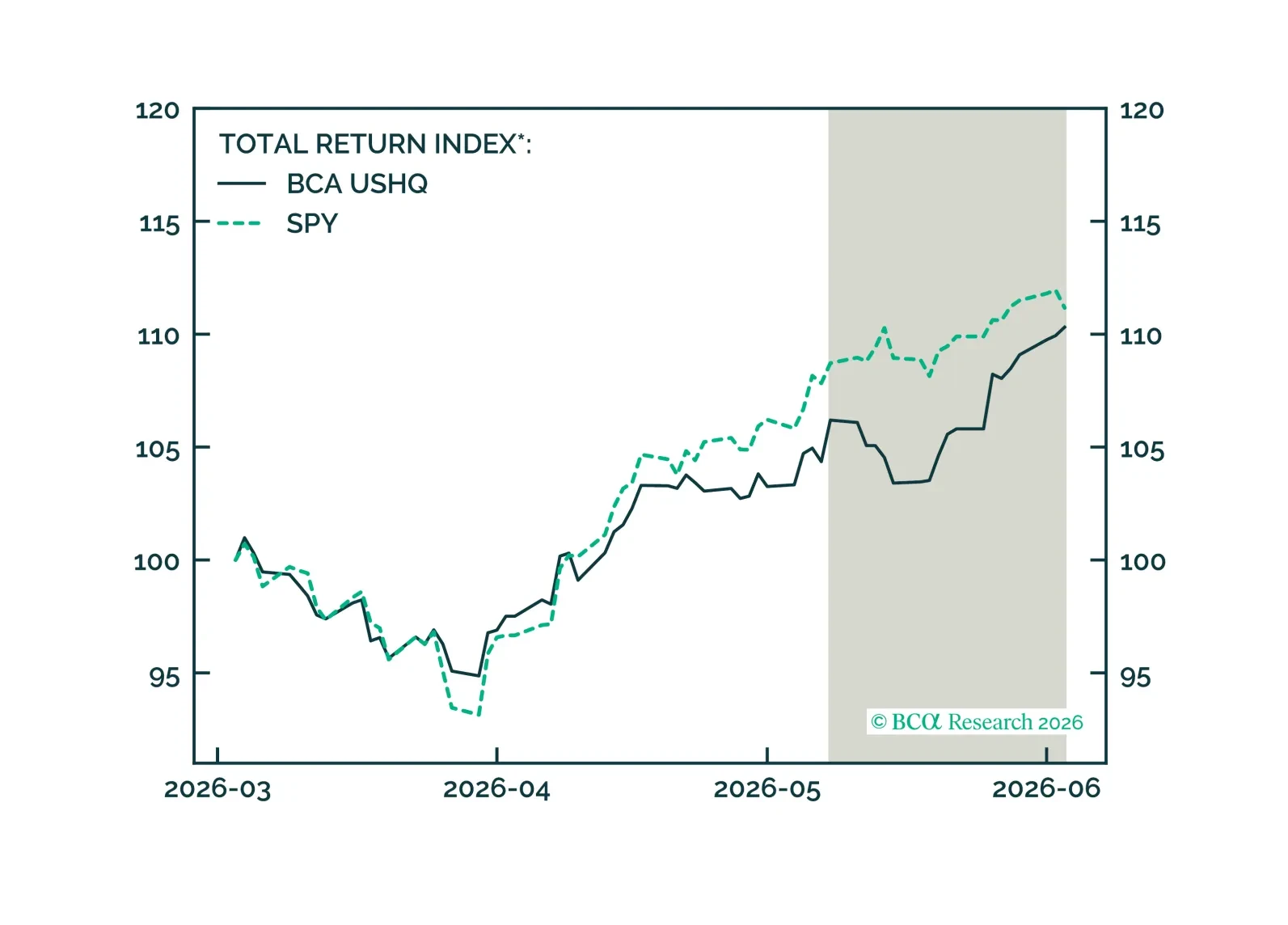

The US High Quality (USHQ) portfolio outperformed its benchmark through May, returning 3.88%, while its SPY benchmark returned 2.25%. On a trailing three-month basis, the USHQ portfolio’s performance was weaker than the benchmark, with USHQ underperforming by approx. 86bps.

The AI boom will increase inflation in the near term and could also raise it over the long term. The Fed’s reluctance to hike rates is understandable, but it risks amplifying what may already be a brewing stock market bubble.