US Labor Market

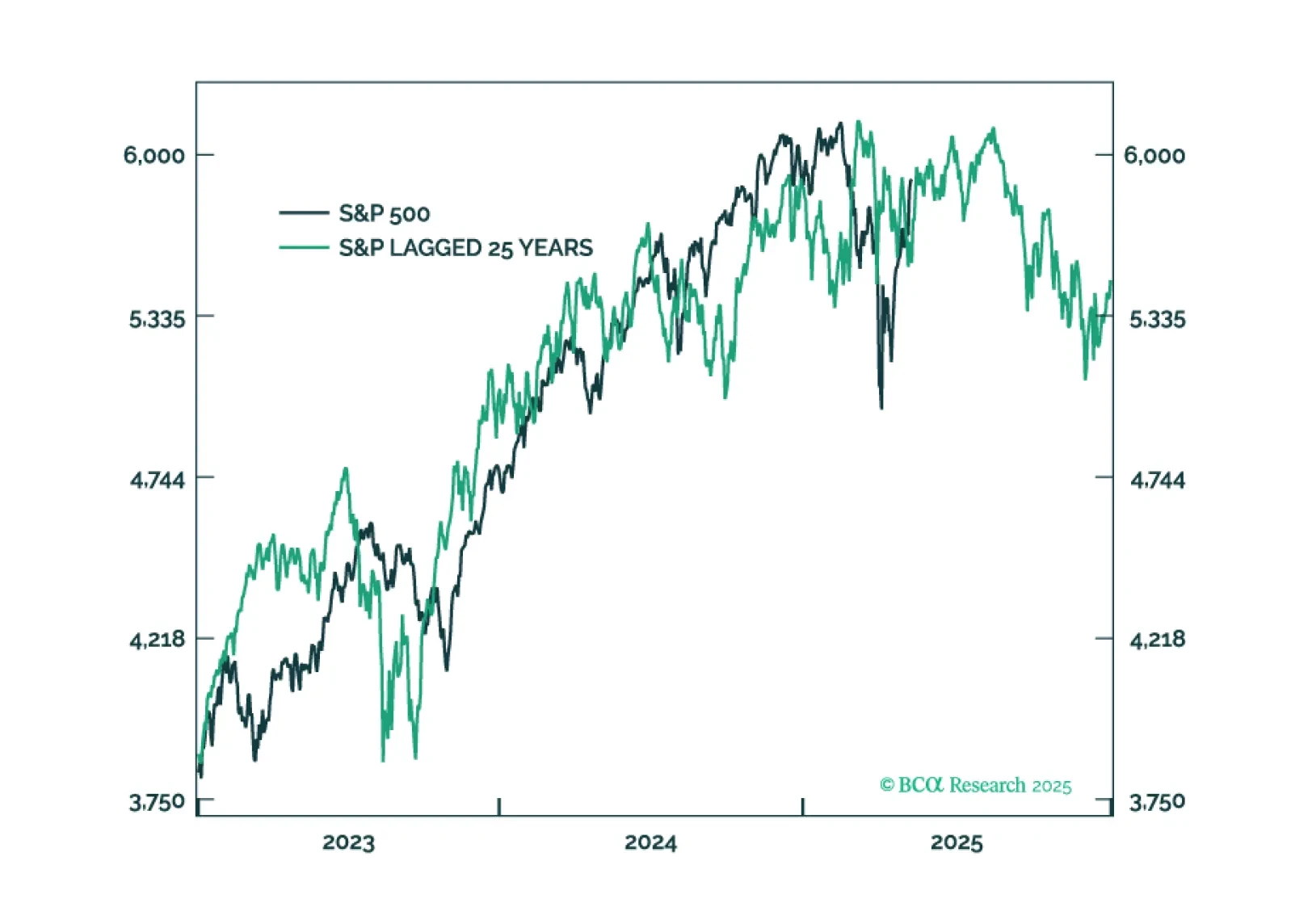

This year’s plunge in tech stocks followed by the recent strong countertrend rally is eerily reminiscent of 2000. But the market and economic parallels between 2025 and in 2000 run much deeper. This report lists 10 striking parallels between 2025 and 2020, then highlights some important differences, and ends by describing how the rest of 2025 might unfold based on a playbook that is: 2025 = ‘2000 with some tweaks.’

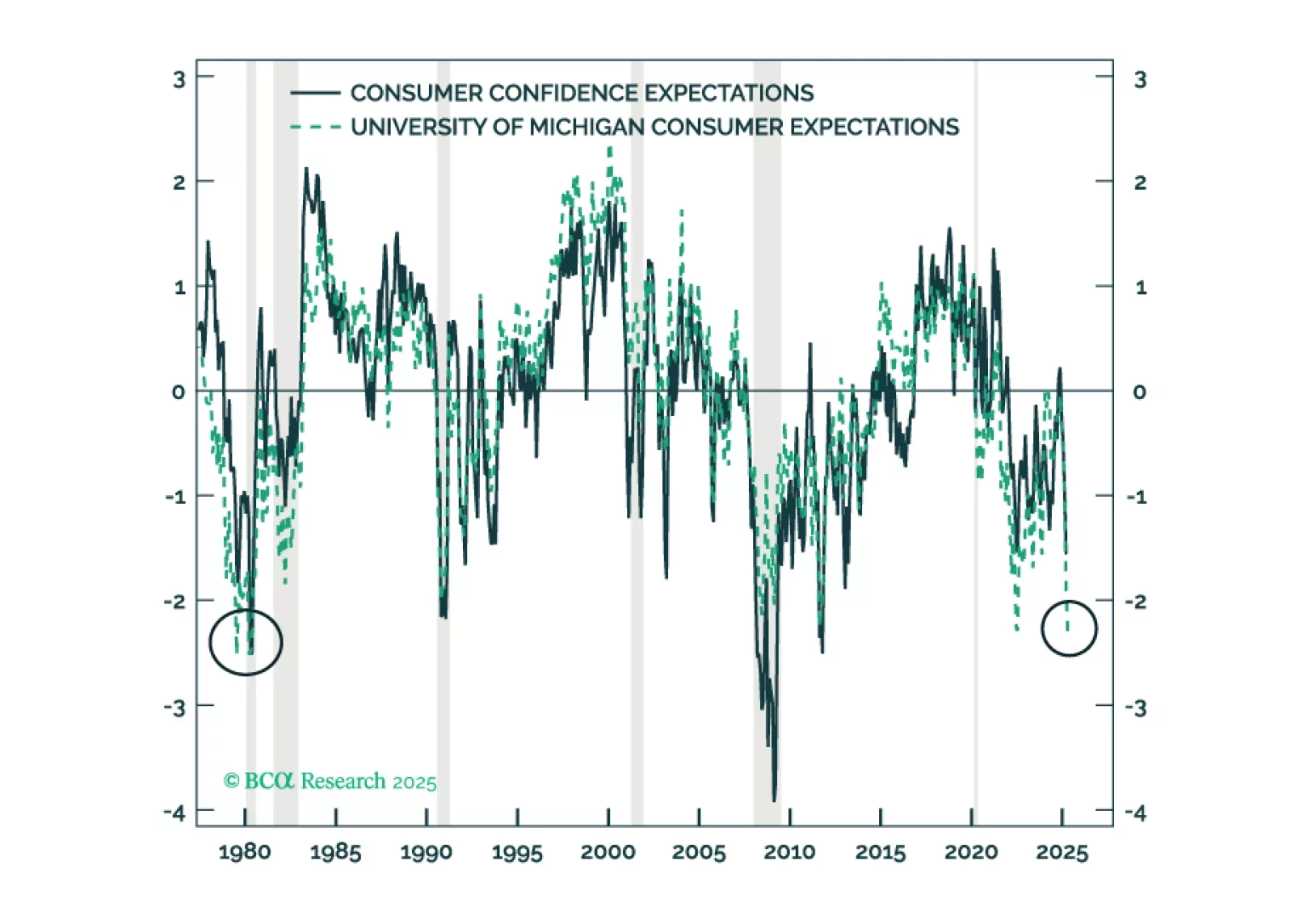

The policy-induced decline in consumer confidence has spread to businesses and investors, increasing the probability of a recession even if the administration reverses field on its aggressive tariff measures. We reiterate our defensive asset allocation recommendations.

Today, we publish our Quarterly Model Bond Portfolio report. We discuss how the trade war has further increased the global recession risk, but US Treasuries could underperform their global peers in the near term. We cover the fixed income investment implications in the short run and which bond markets are poised to outperform in a severe economic downturn.

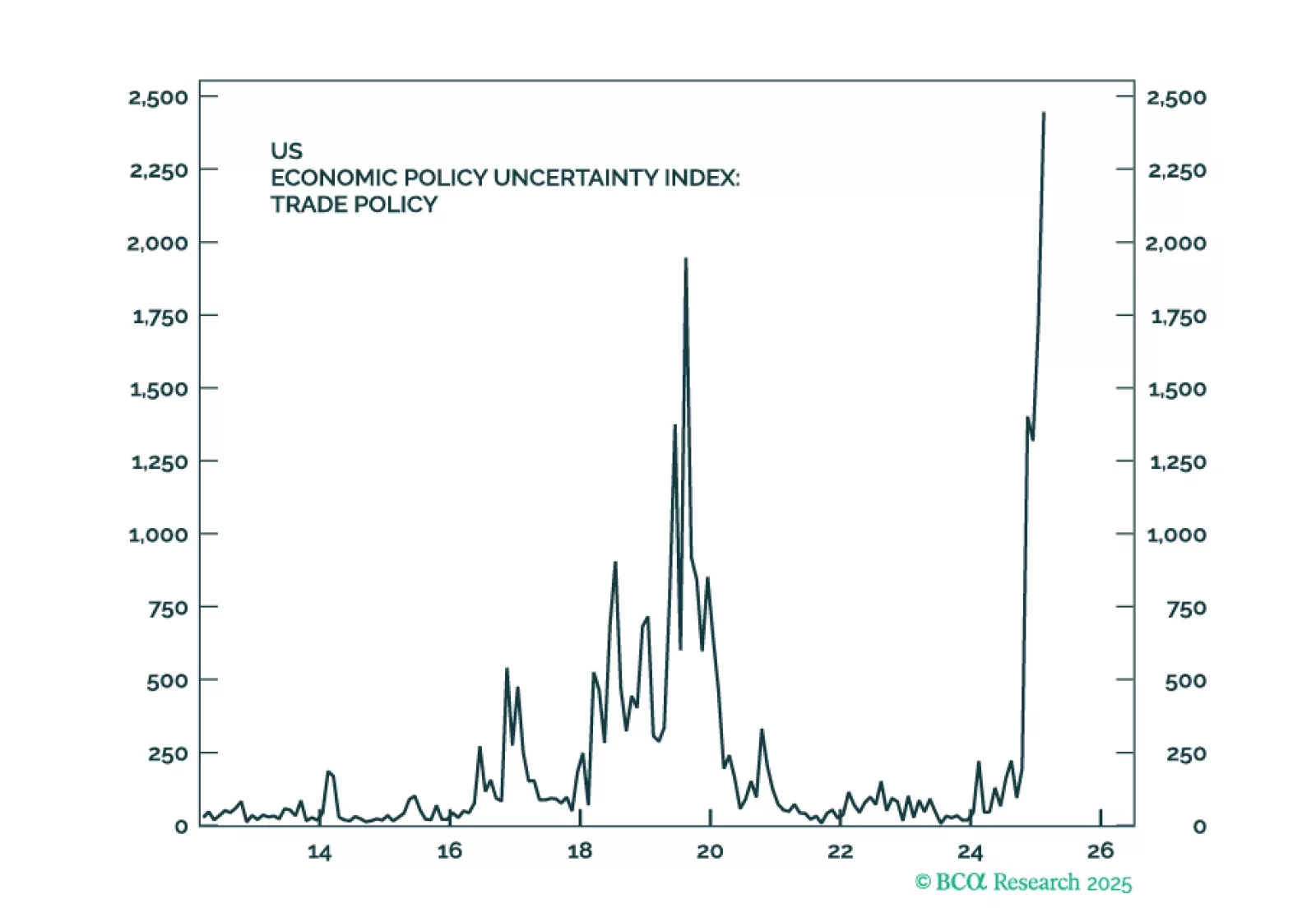

Although there may be a method to DOGE’s 100-mile-an-hour madness, we think the worries and uncertainty stoked by it and on-again, off-again tariff measures have increased the probability of a recession while bringing forward its start date. We are therefore tactically downgrading equities to underweight and upgrading fixed income and cash to overweight. Investors should pursue a defensive posture.

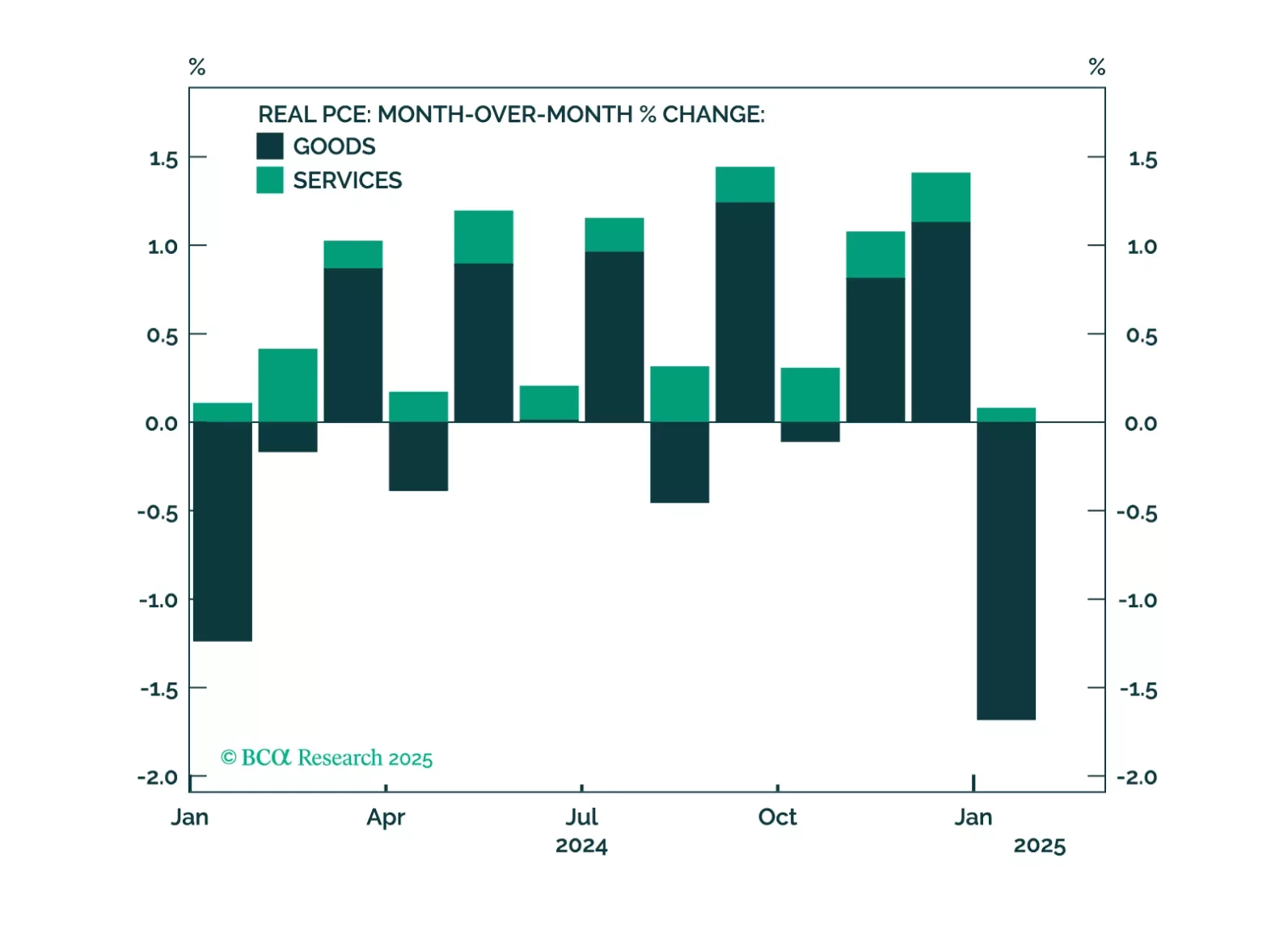

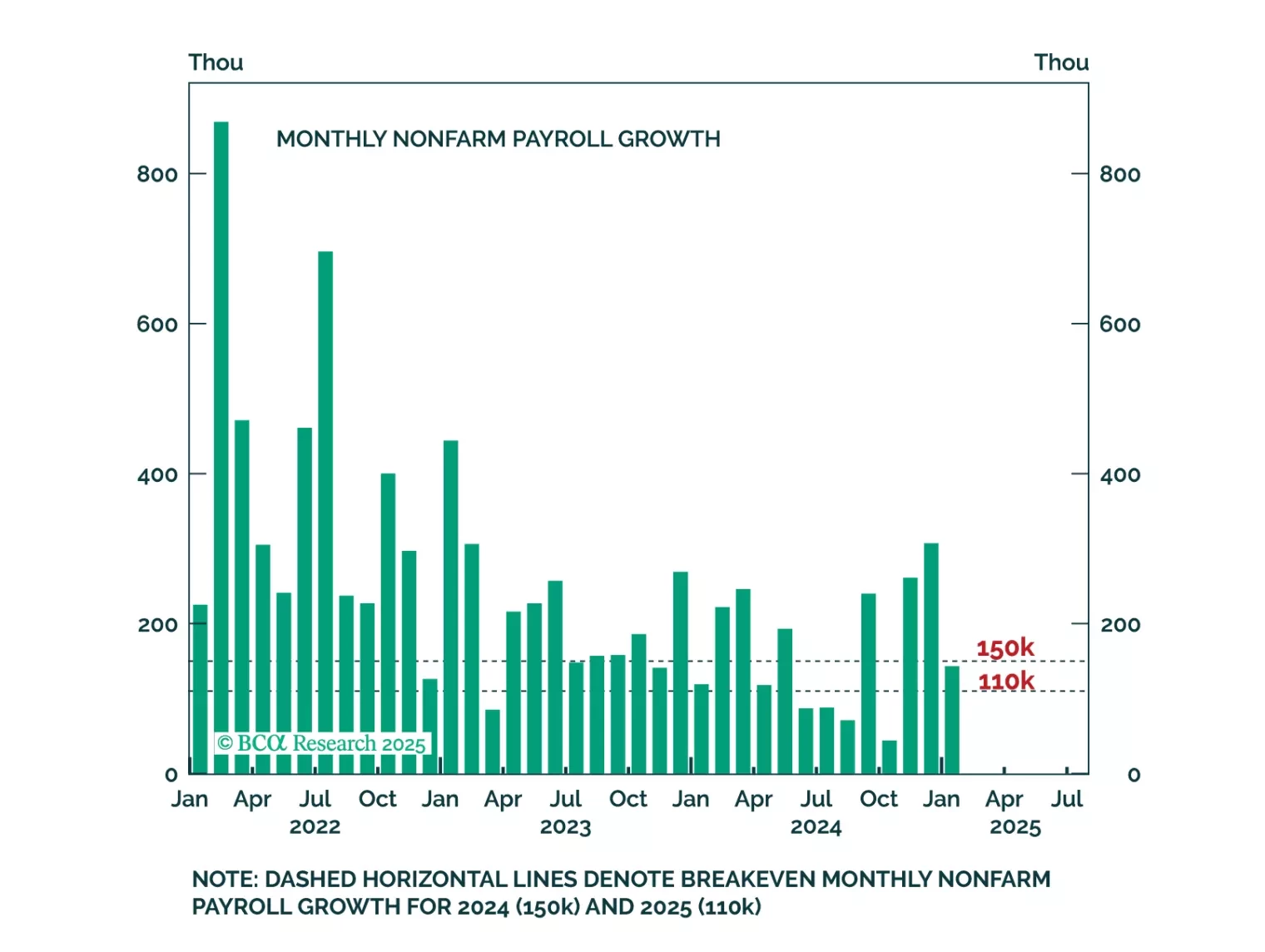

This morning’s employment report showed solid job growth, but recent consumer spending indicators are more concerning. The risk of recession starting within the next few months has increased. We suggest some important indicators for investors to track in the current environment.

The US economy is set to enter a recession within the next few months. Stay underweight equities and overweight cash. Look to increase fixed-income duration exposure over the coming months. The euro is likely to strengthen and European stocks should outperform US stocks over the next month or so, but these trends will reverse by the middle of this year.

Some thoughts on this morning's employment data and Treasury Secretary Bessent's recent attempts to talk down the 10-year Treasury yield.

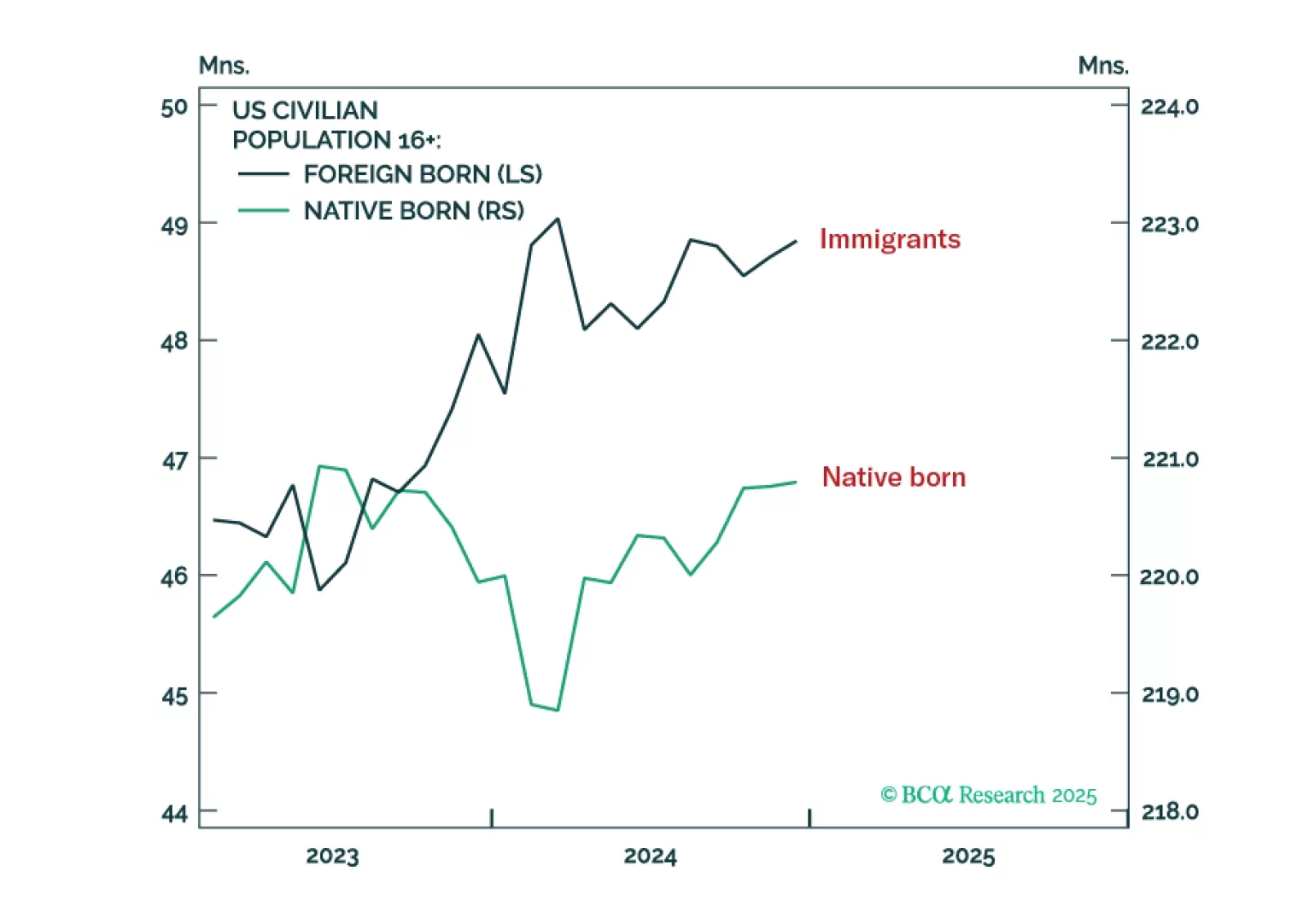

All the growth in the US labour supply since mid-2023 has come from immigration. This means if net immigration comes to a grinding halt, as Trump wants, it will hurt economic growth as well as keep the labour market supply-constrained. An increase in productivity growth could save the day, both to maintain growth and to kill inflation. Yet hopes that AI is about to usher an imminent and sustained boost to productivity growth are misplaced. Hence, expect a slowdown in US growth combined with inflation stuck close to 3 percent, a combination that I call a ‘mini stagflation’. We go through the investment implications. Plus: Tactically overweight Portugal versus Europe.