US Labor Market

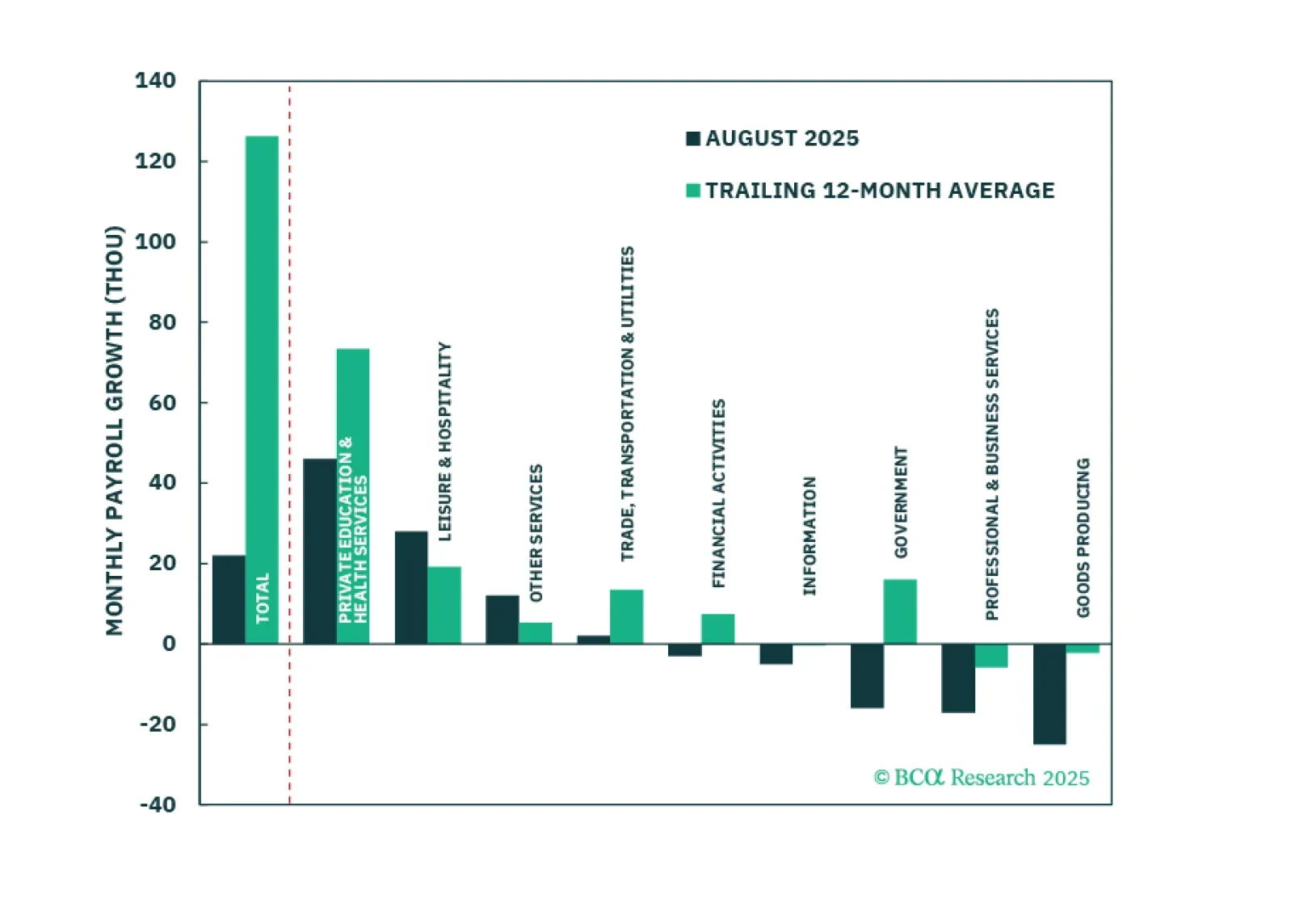

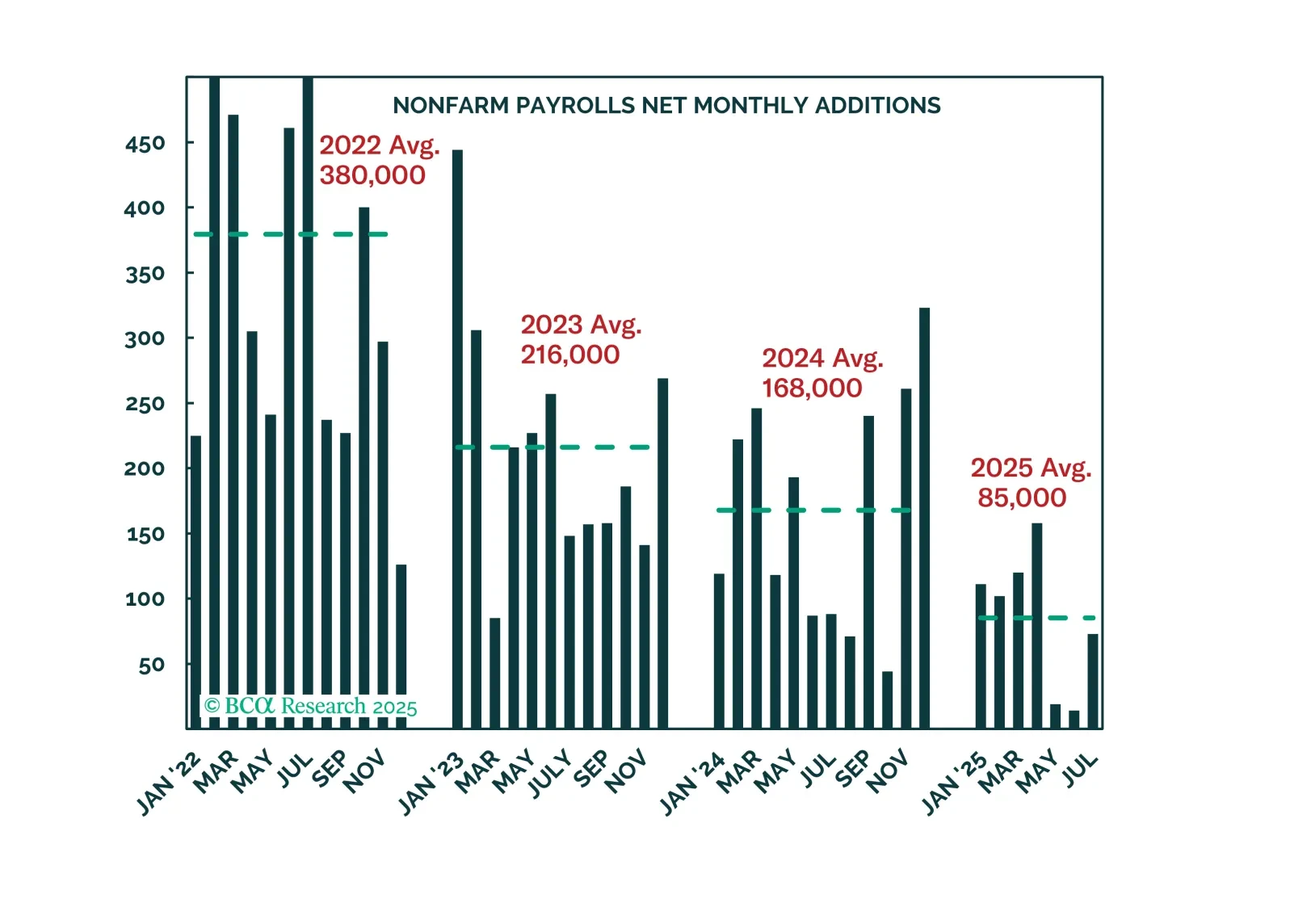

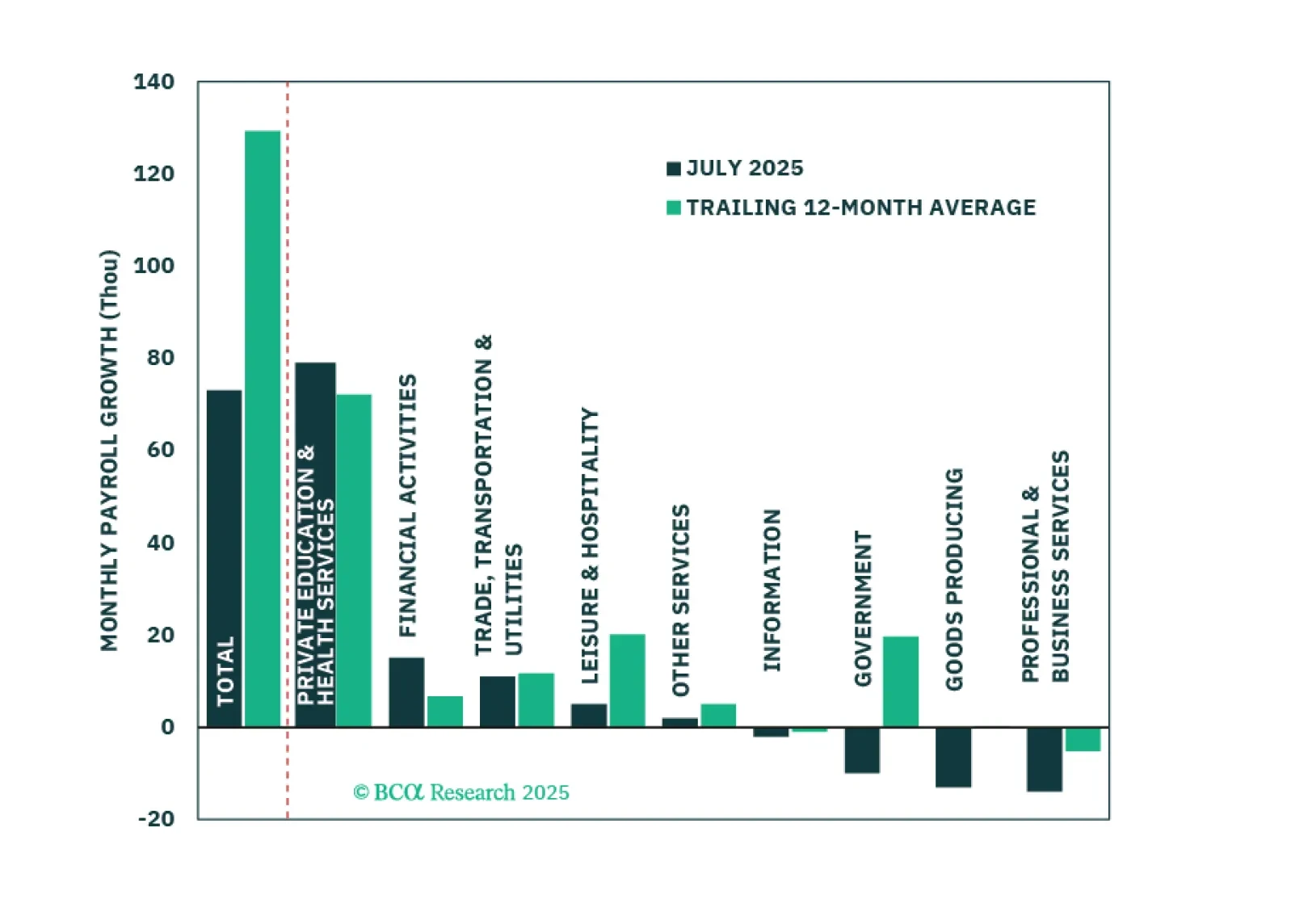

The August employment report showed a modest increase in labor market slack, enough to cement a 25-basis-point rate cut this month.

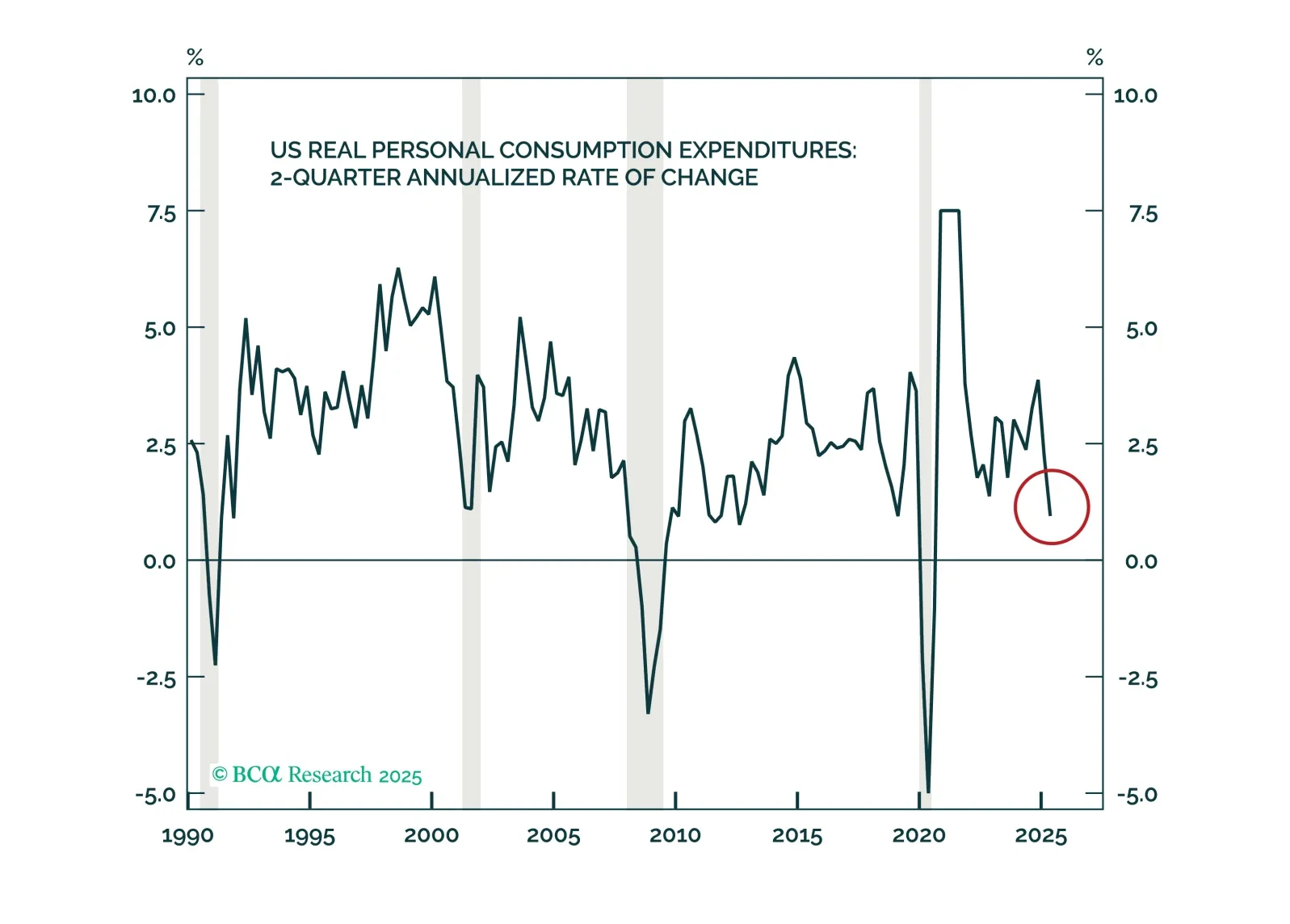

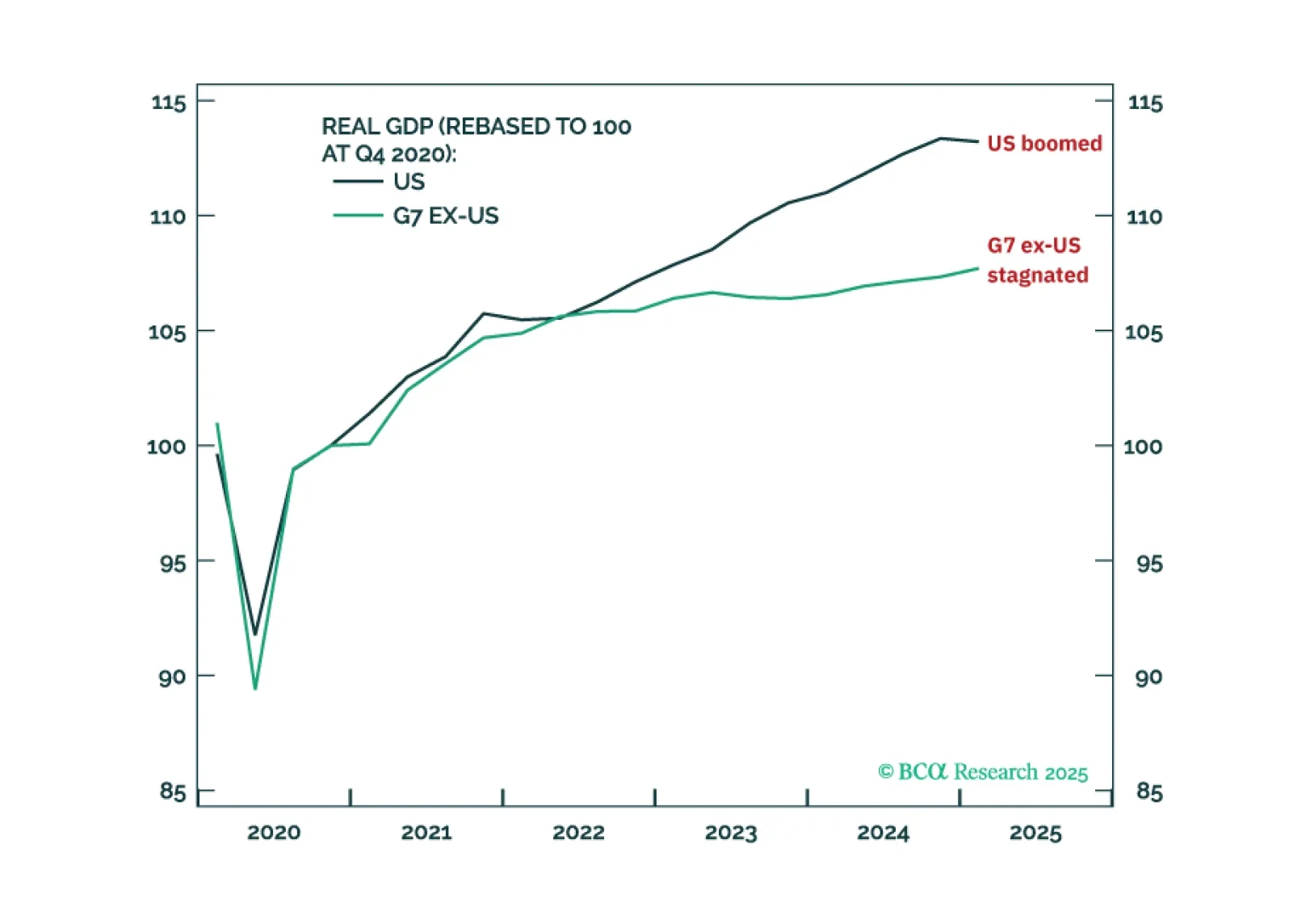

Economic activity plainly slowed in the first half, led by decelerating consumption and payrolls growth, but financial markets didn’t care. If the next two weeks of data don’t indicate that the May-June slowdown stretched into July and August, we will likely drop our defensive recommendations.

Data received since we began reassessing our bearish stance supported our notion that the economy is not as strong as the investor consensus perceives. But the softness will likely have to intensify in July and August to preserve our defensive recommendations.

Economic activity and hiring cooled significantly in the first half of the year. The most important question for investors is whether this signals an imminent increase in labor market slack.

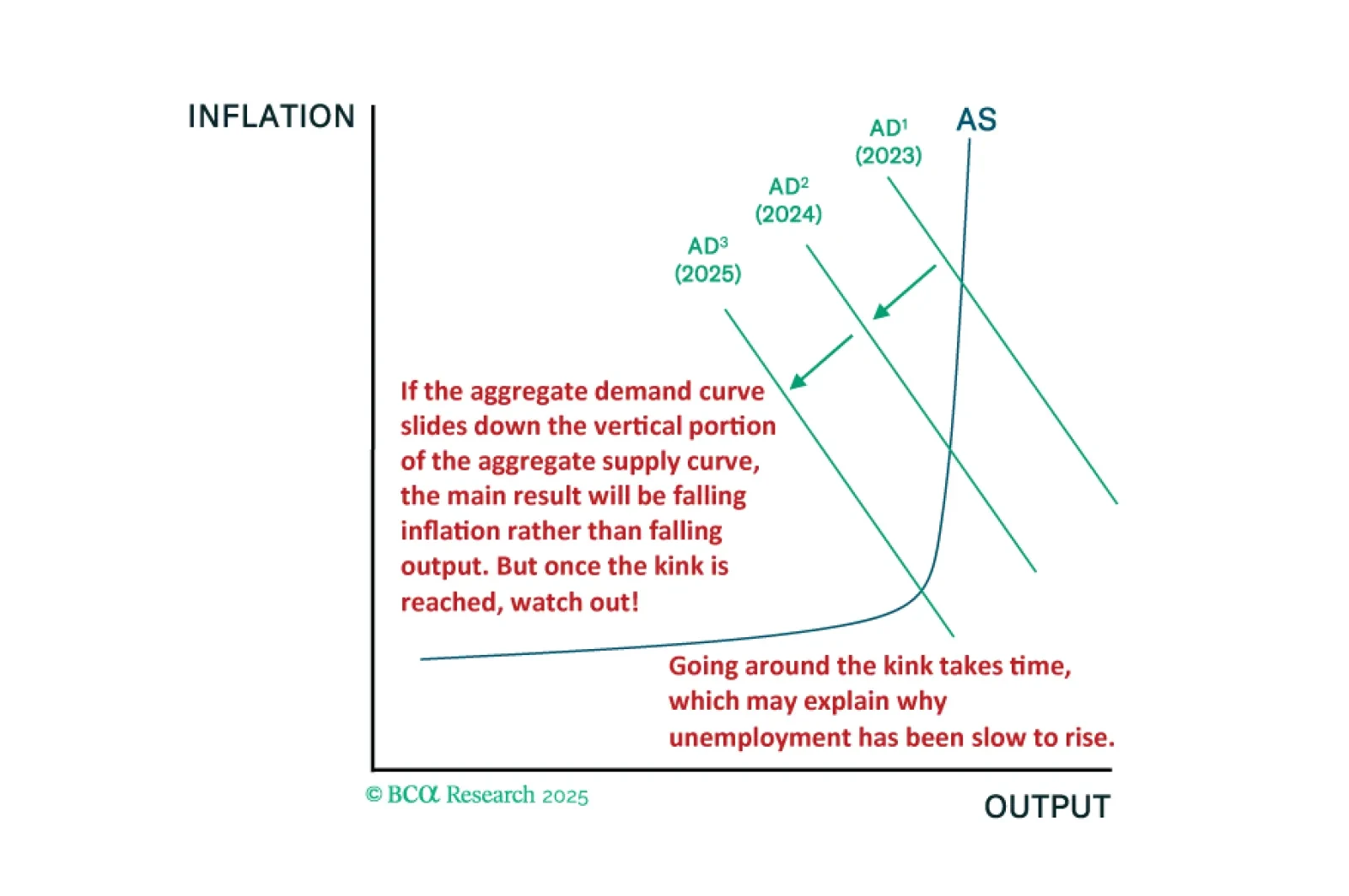

The fact that the US economy has been slower to deteriorate than in past cycles is entirely consistent with our kinked Phillips curve framework. We will be looking to our MacroQuant model for guidance on when to turn fully defensive.

Euro area and Chinese interest rates must fall much further to prevent monetary policy from becoming ultra-restrictive. But Trump’s attempts to force unwarranted rate cuts from the Fed risks a vicious backlash from the bond vigilantes.

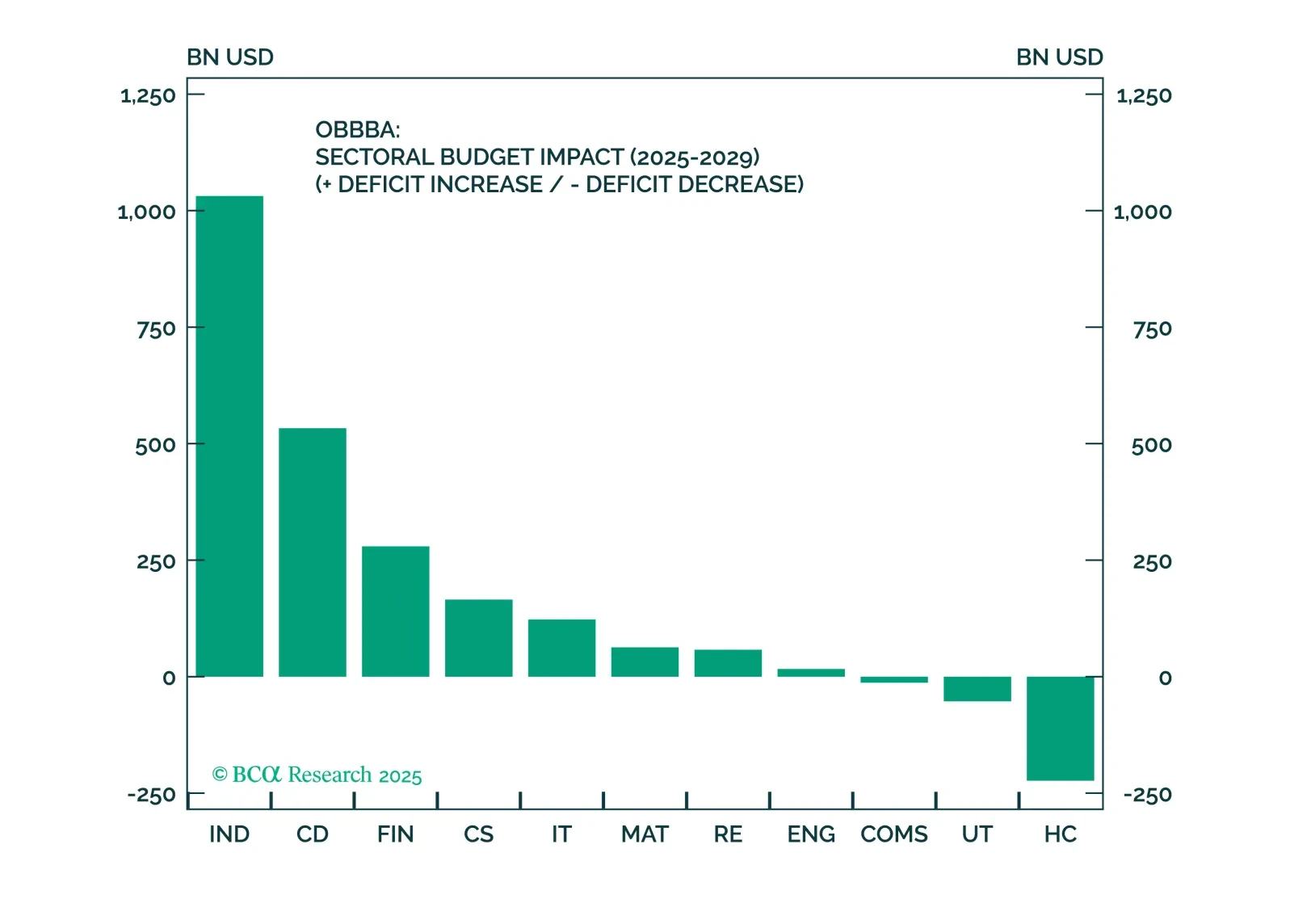

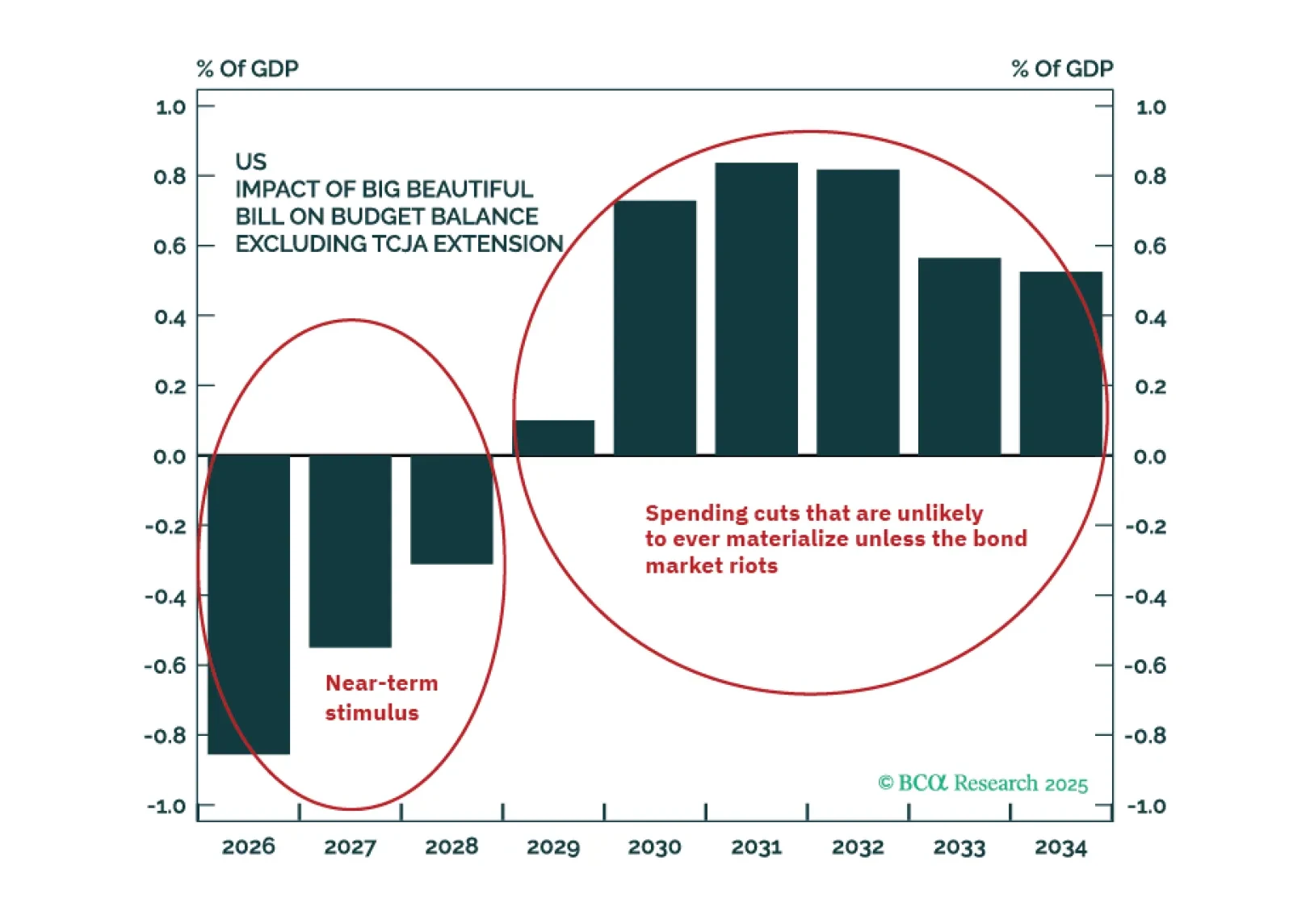

Despite macro headwinds, the OBBBA clearly favors Industrials, Financials, and Consumer Discretionary equity sectors. A carefully constructed, factor-aware basket in these sectors is well positioned to outperform in a fiscal-driven, uncertain environment.

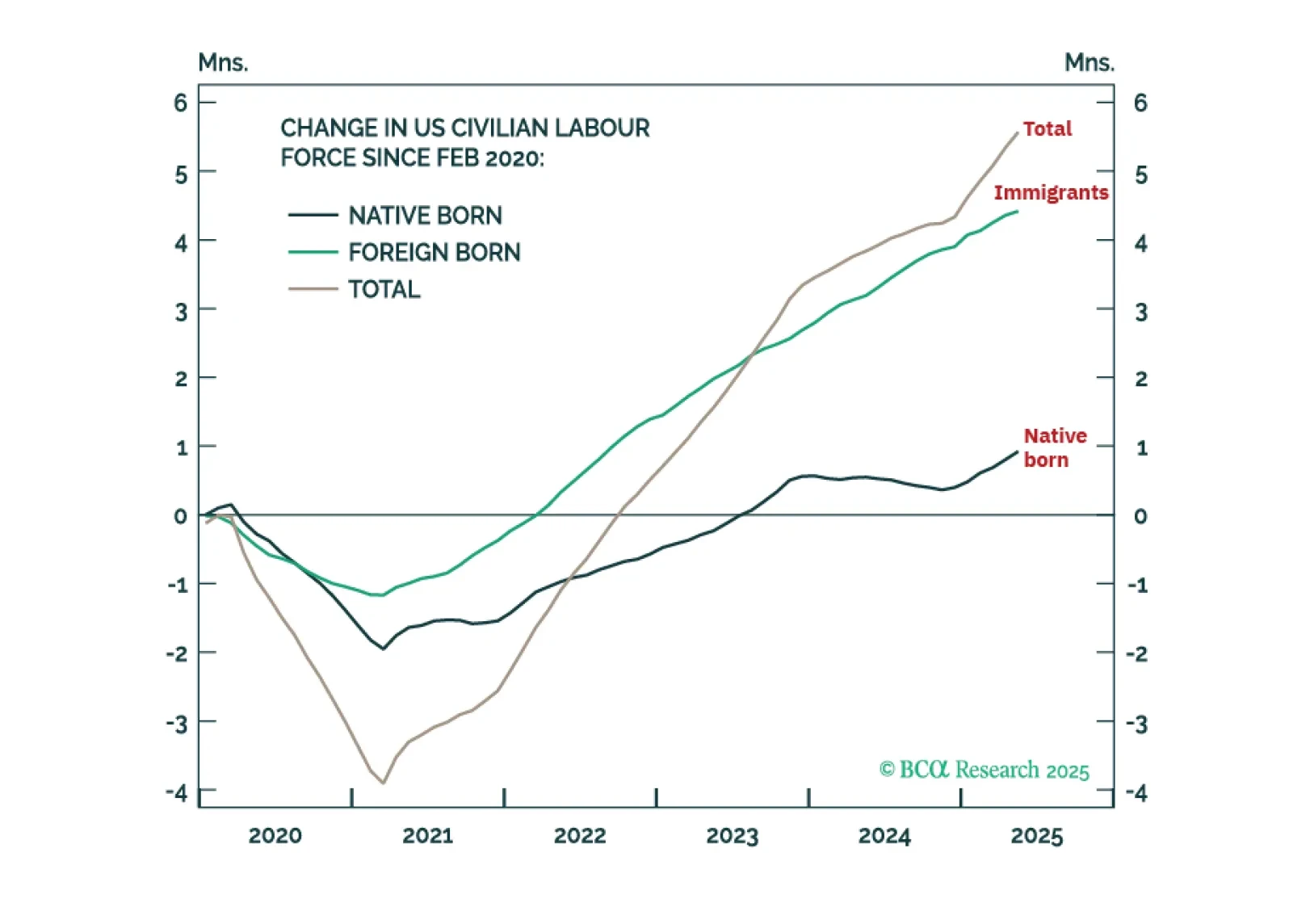

Trump’s immigration policies are protecting the US economy from a sharp rise in unemployment but steering it into a ‘mini stagflation’. Plus: a new tactical trade is to underweight global technology (IXN).

The US economy has held up better so far this year than we had expected. For the time being, investors should remain modestly underweight equities. A more aggressive underweight would be justified only once the “whites of the recession’s eyes” are visible.

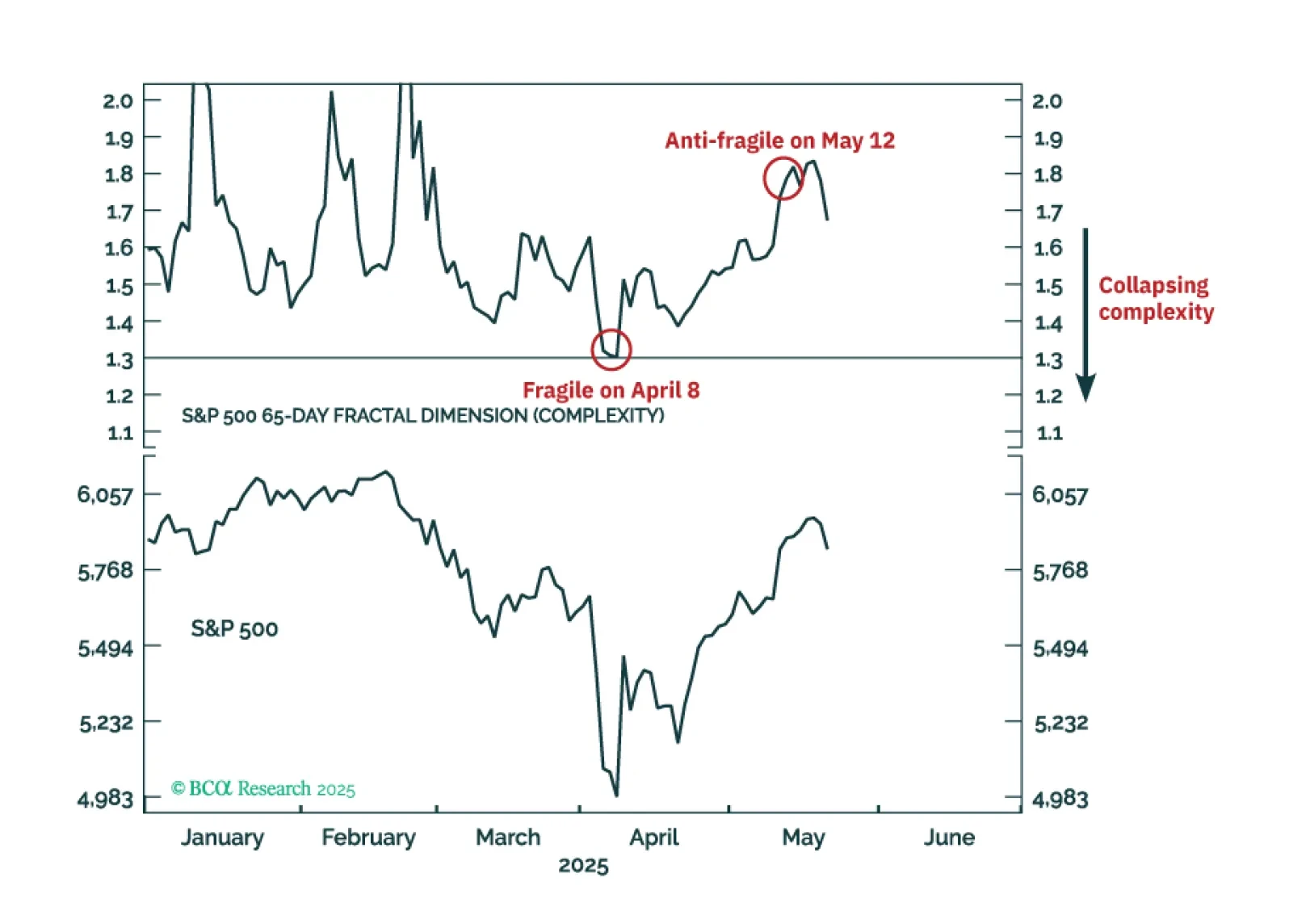

Right now, the major stock and bond markets are more ‘anti-fragile’ than fragile, and the Joshi rule recession indicators signal that a US recession is not imminent. This justifies a neutral, or default, tactical weighting to both stocks and bonds until a major market does become fragile, or until recession risk elevates. The one major price trend that is fragile is the 65-day selloff in the US dollar, which justifies a tactical overweighting to the dollar.