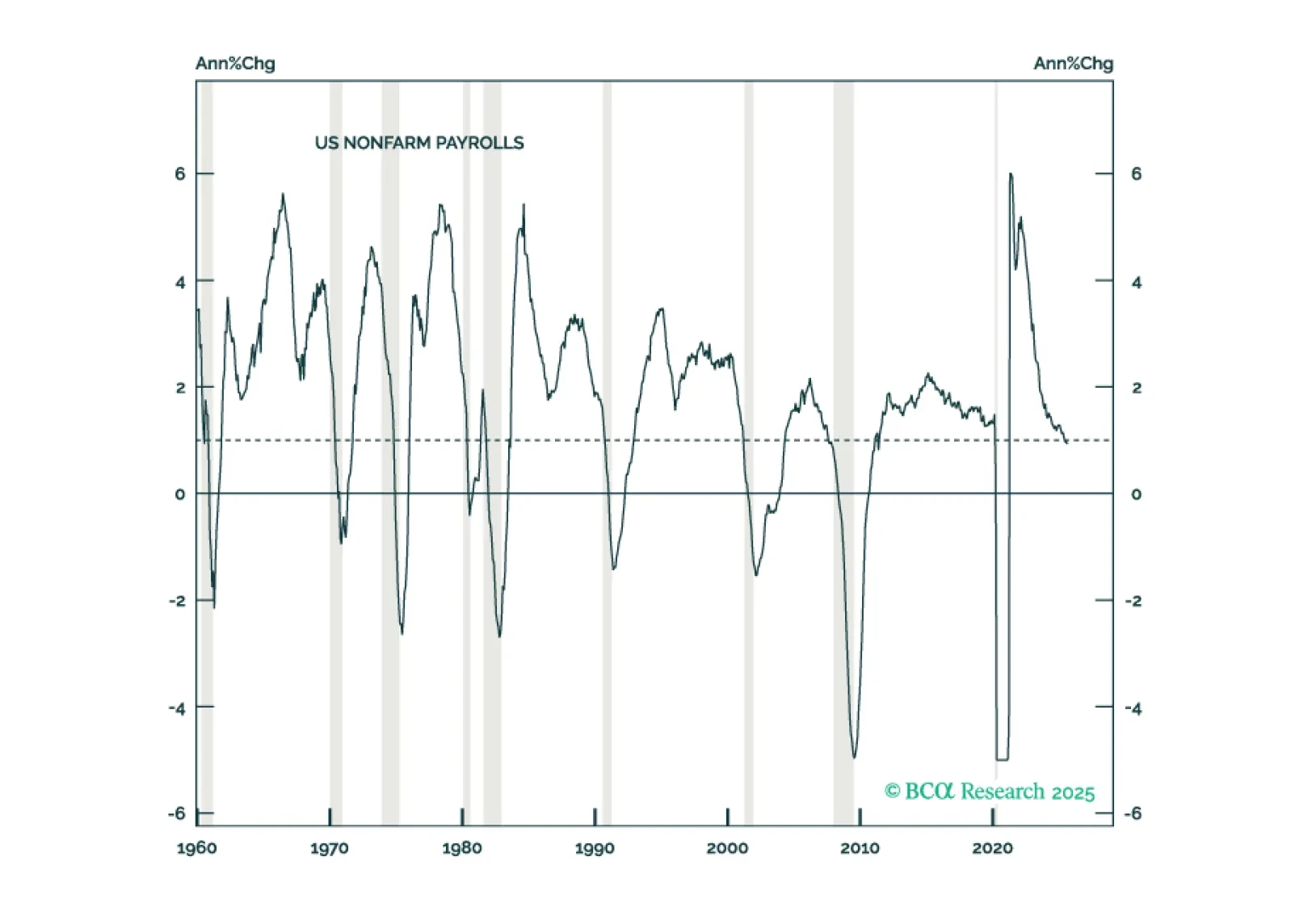

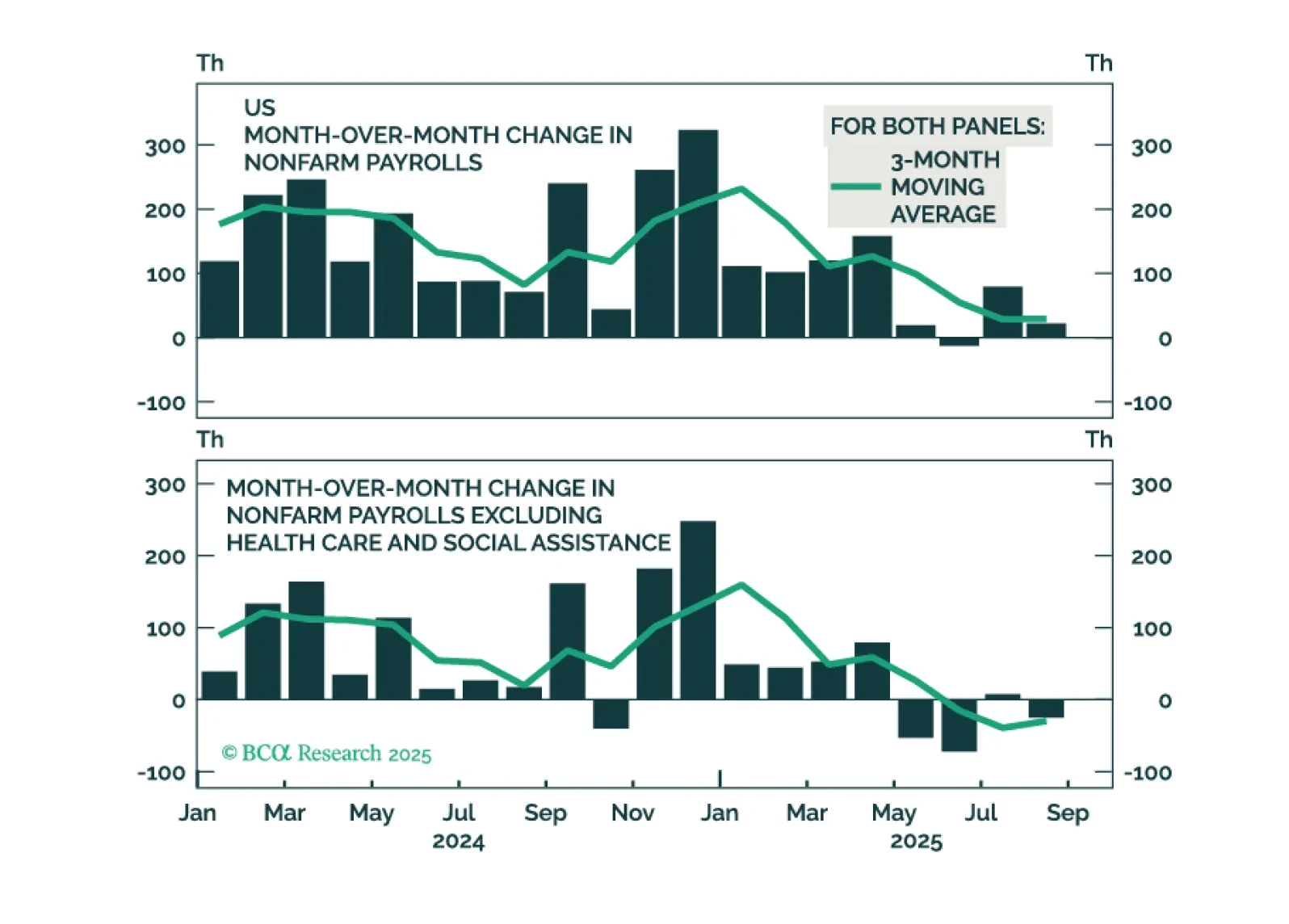

US Labor Market

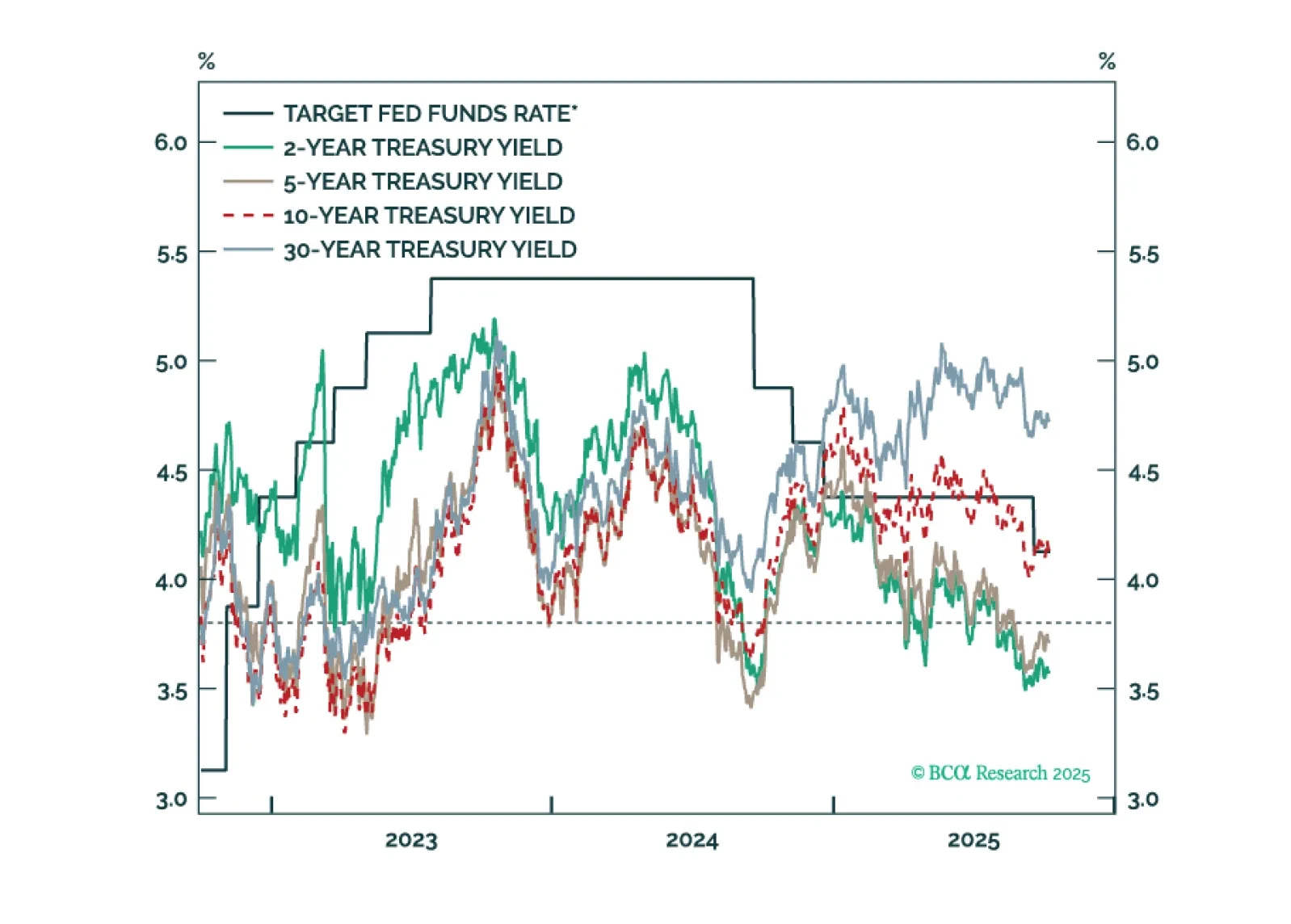

Treasury yields are generally following the pattern of past interest rate cycles, but with a larger term premium keeping the curve steeper than usual.

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.

The K-shaped economy aptly describes the bifurcation between low- and high-end households but it’s not something investors should celebrate if they want the expansion to continue.

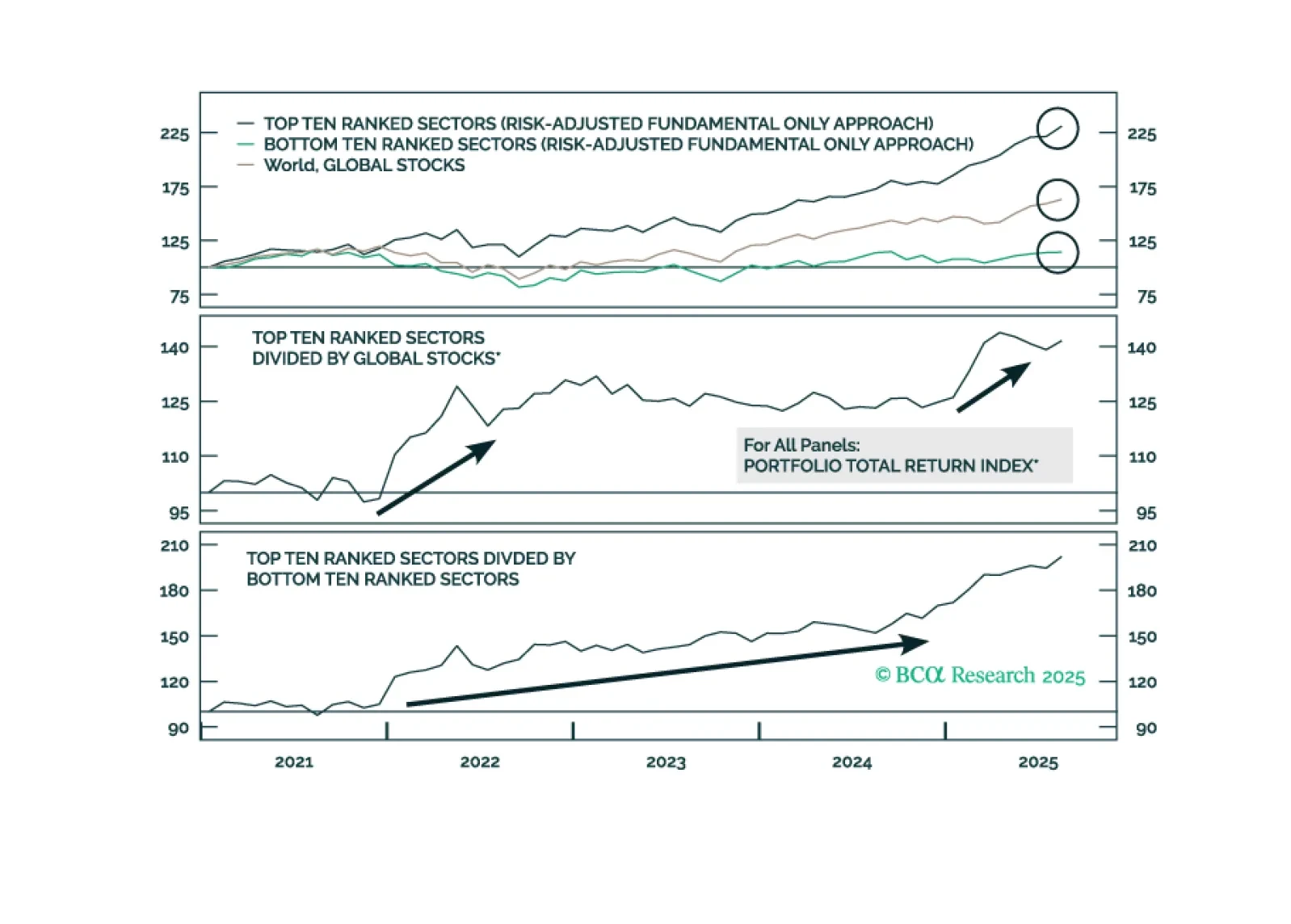

In Section I, Doug highlights that benchmark positioning in equities, fixed income and cash is now recommended. Still, the US macro situation warrants continual monitoring, given weakening labor market momentum. In Section II, Jonathan shows how valuation-adjusted fundamental momentum has been a successful tool for ranking global sectors.

In Section II, Jonathan shows how valuation-adjusted fundamental momentum has been a successful tool for ranking global sectors.

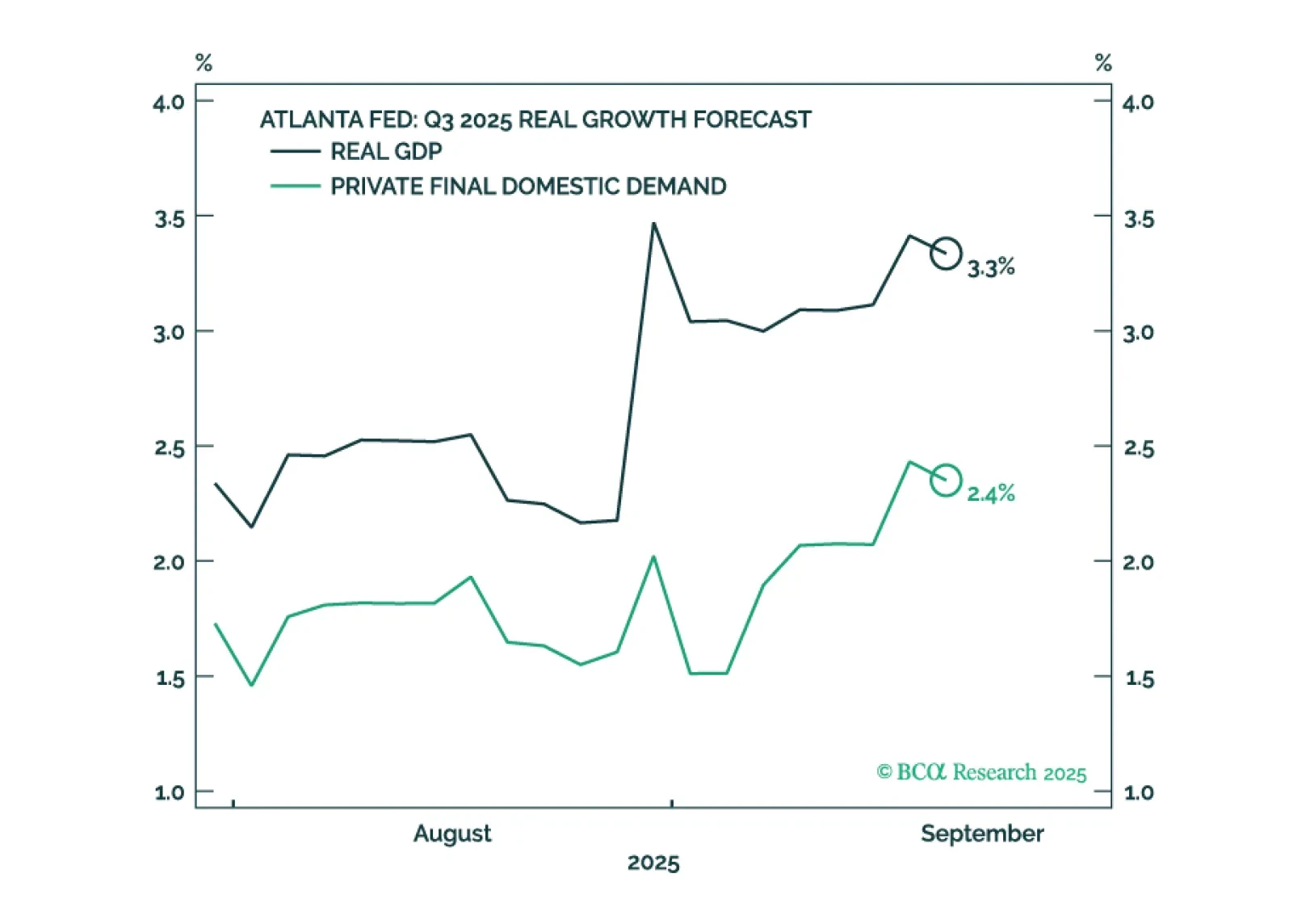

US GDP growth appears to have accelerated even as employment growth has faltered. We will make a final decision in early October when we publish our next Strategy Outlook, but most likely, we will cut our 12-month US recession probability to 40%-to-50% from 60% and turn tactically neutral on stocks, while still retaining a modest equity underweight over a 12-month horizon.

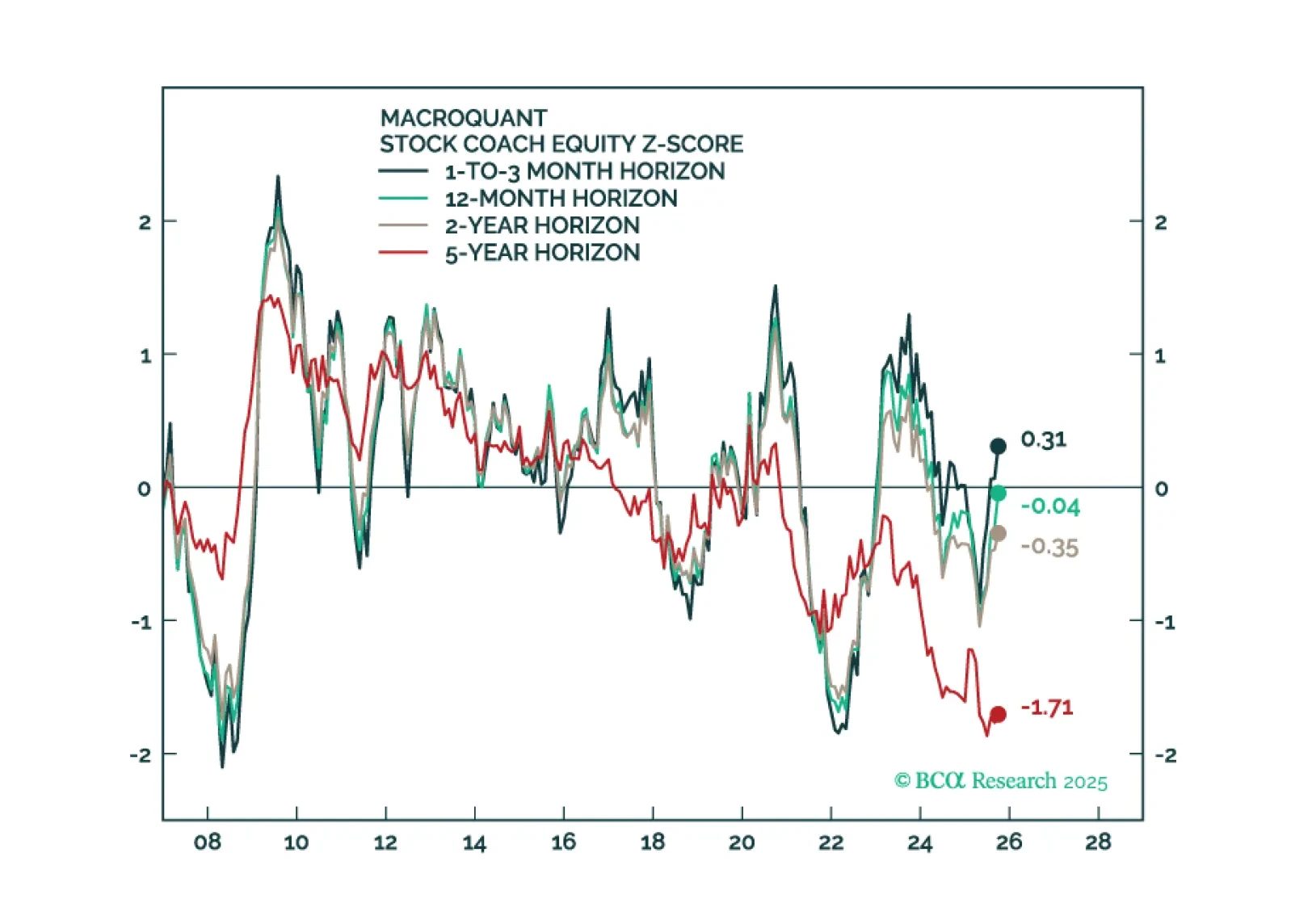

While it is impossible to know exactly when global equities will peak, there are now enough vulnerabilities to justify keeping one’s finger near the eject button.

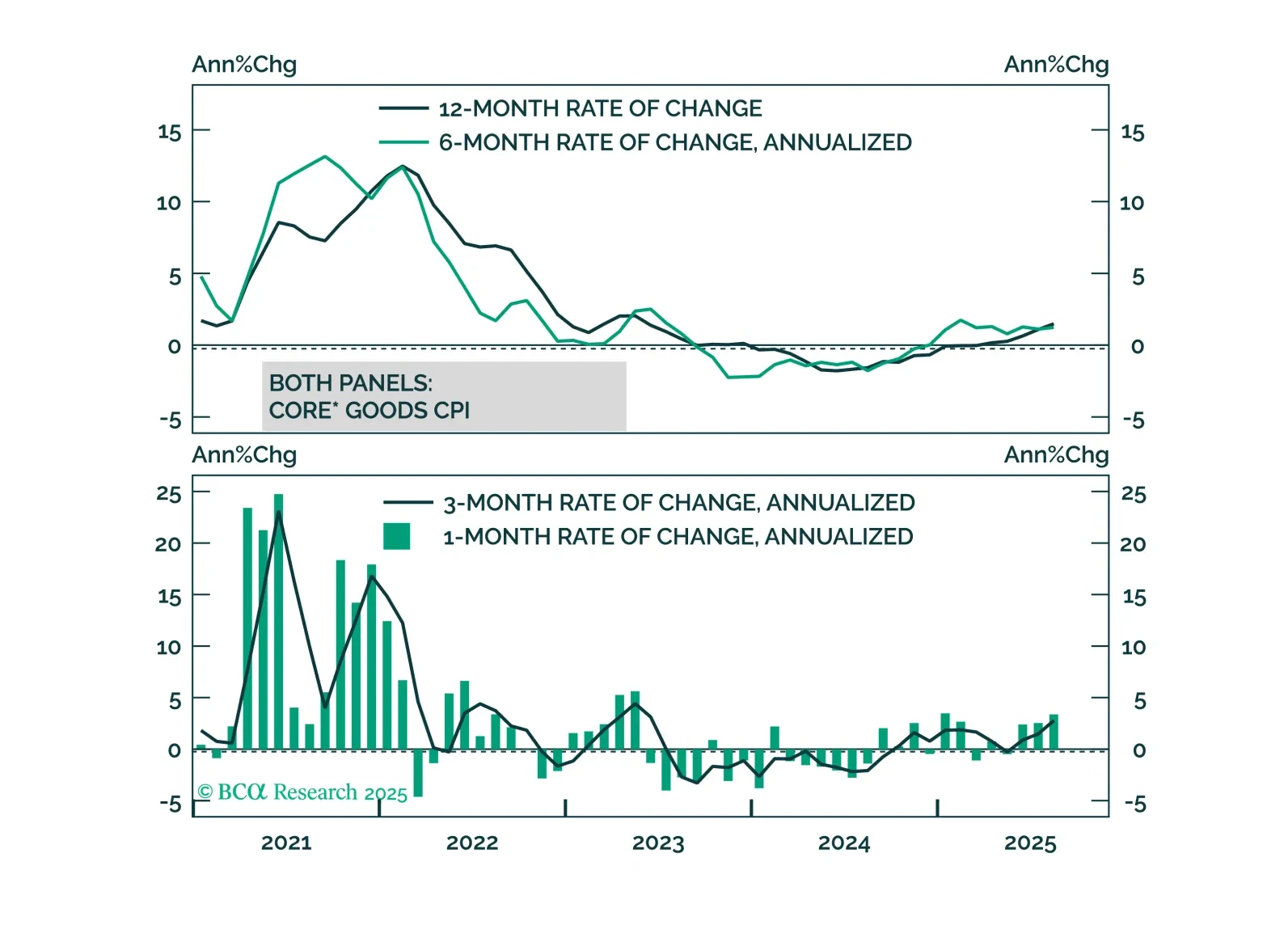

High US inflation is being driven by tariffs, not domestic inflationary pressure. This argues for Fed easing and a bull-steepening of the Treasury curve.

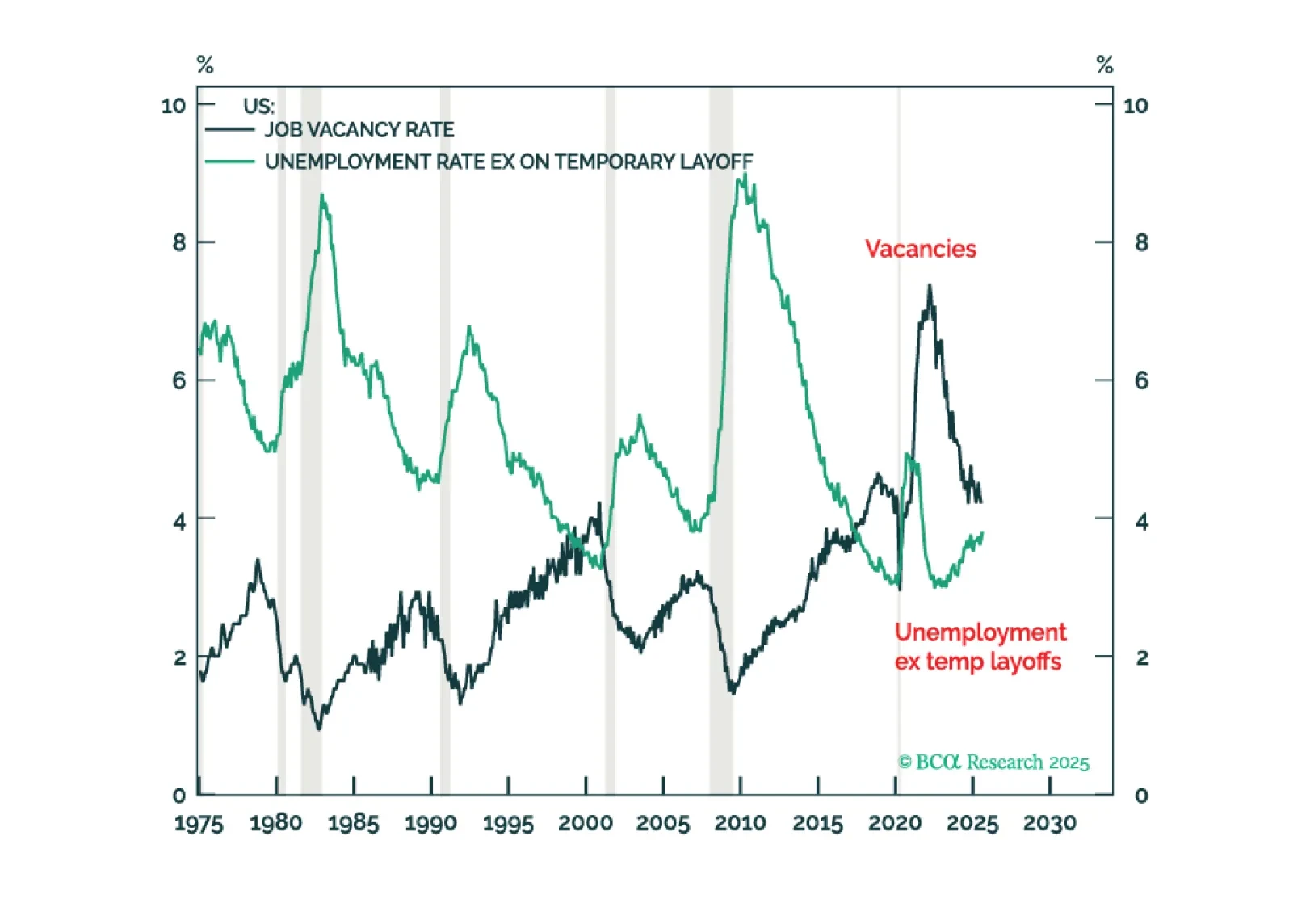

For the next few months at least, inflation risk trumps recession risk for both US markets and world markets. This because, correctly gauged, the US jobs market is still supply-constrained with ‘jobs looking for a worker’ exceeding ‘workers looking for a job’ by 0.4 percent. A still supply-constrained US jobs market cannot enter a demand-driven recession until it flips back to demand-constrained, so bond investors should underweight duration. Plus: a new tactical trade is overweight India (INDA).

Although our recession conviction has risen, we conclude our strategy review by closing our equity underweight and our fixed income and cash overweights. AI momentum is too strong to have anything more than modest exposure to an equity decline via a small SPY put position.