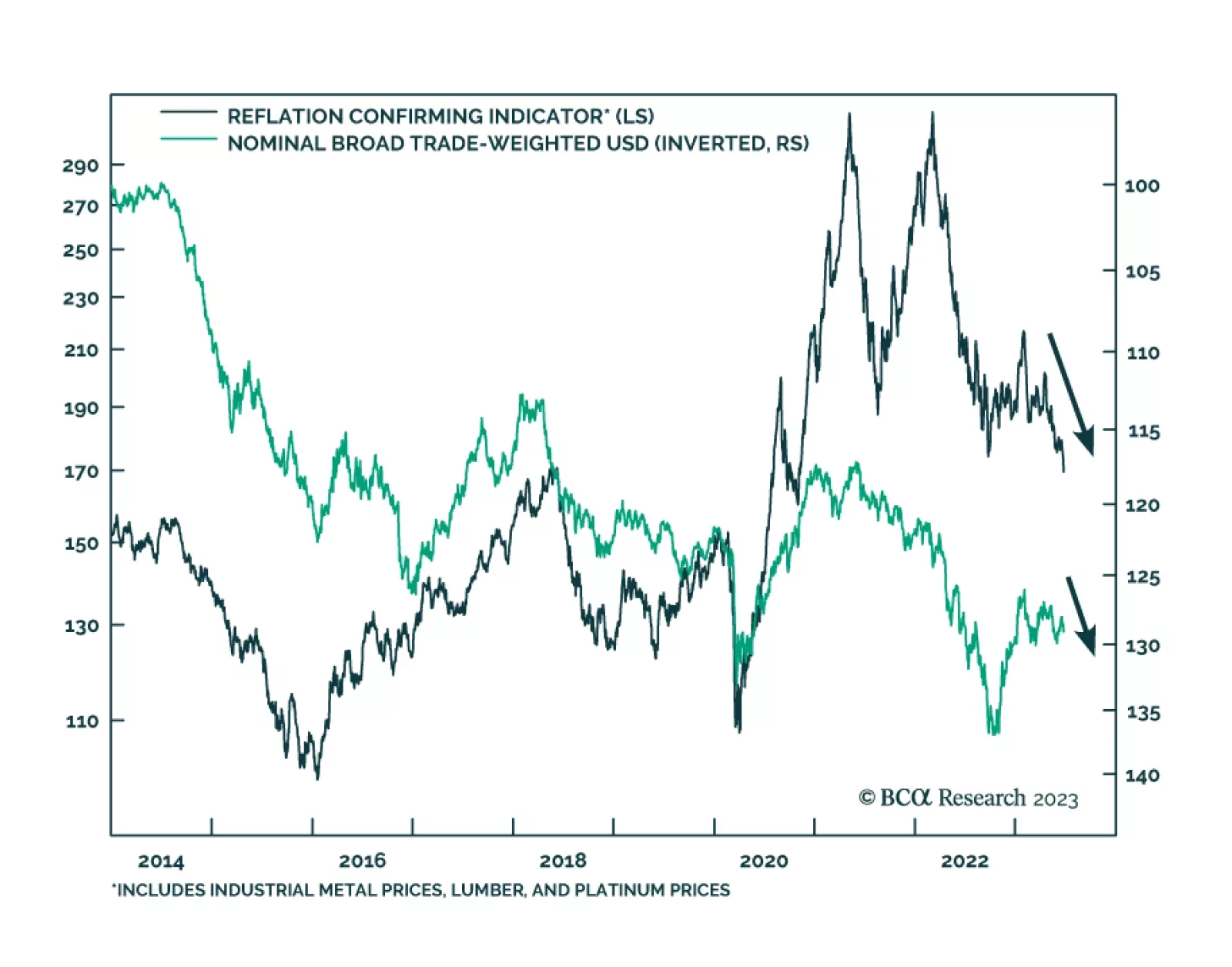

US Dollar

Recession is on track to start around year-end. Stocks usually peak shortly before recession begins. So, position defensively but be prepared for a few more months of the rally.

This report reviews our key calls for major currencies, in light of recent data releases.

In this Strategy Outlook, we present the major investment themes and views we see playing out for the rest of 2023 and beyond.

The market does not grasp the implied depths of recessions that will be needed to prevent inflation expectations from un-anchoring. Among the major economies, the most vulnerable to a deep recession is the UK. We explain why, and some investment implications. Plus: the yen is a rebound candidate, while Japanese equities are a reversal candidate.

This Strategy Insight discusses the bond market and currency implications of the Fed’s “hawkish pause”.

As the major central banks once again mull their policy options, they face a daunting task. They must phase-transition inflation back to imperceptible, without phase-transitioning unemployment to perceptible. This report explains why this will prove impossible, and what central banks will likely prioritise. Plus: the collapsed complexity of the recent stock market rally signals excessive trend-following. Until the complexity normalises, we are reluctant to chase the rally.

This Strategy Insight discusses the bond market and currency implications of the Fed’s “hawkish pause”.

A benign disinflation will support equities over the next few quarters. Stocks will fall next year as a recession begins when investors least expect it.

What’s going on? The market-weighted stock market is up. But the equally-weighted stock market is not up. Neither is credit. Neither are industrial metal prices. Neither is the oil price, despite two waves of OPEC output cuts. We explain the dichotomy. Plus: European basic resources stocks can rebound, but Netherlands is likely to reverse.