US Dollar

Collapsed complexity, plus the unwinding of favourable base effects and favourable seasonal adjustments to the inflation and jobs numbers, all pose a danger to the Goldilocks market.

The DXY will continue to have near-term upside, as economic growth holds up in the US, while it deteriorates in other parts of the world. Remain constructive on the DXY at current levels, but pivot to a short position on evidence US growth is boosting the rest of the world.

The US is not out of the woods when it comes to inflation, which means that it is too early to conclude that the Fed can stop raising rates. Any further increase in inflation risk would prompt us to turn more cautious on stocks.

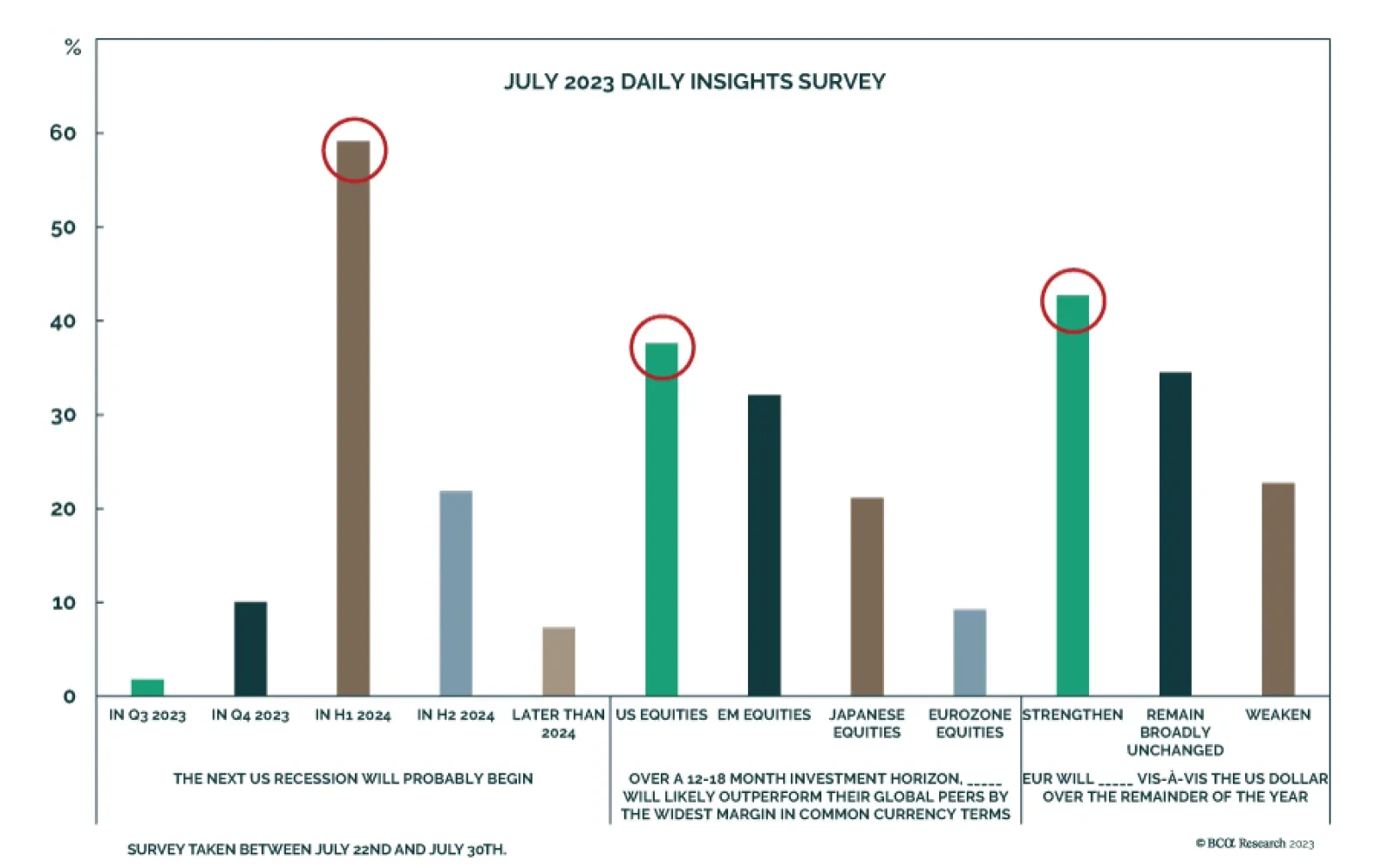

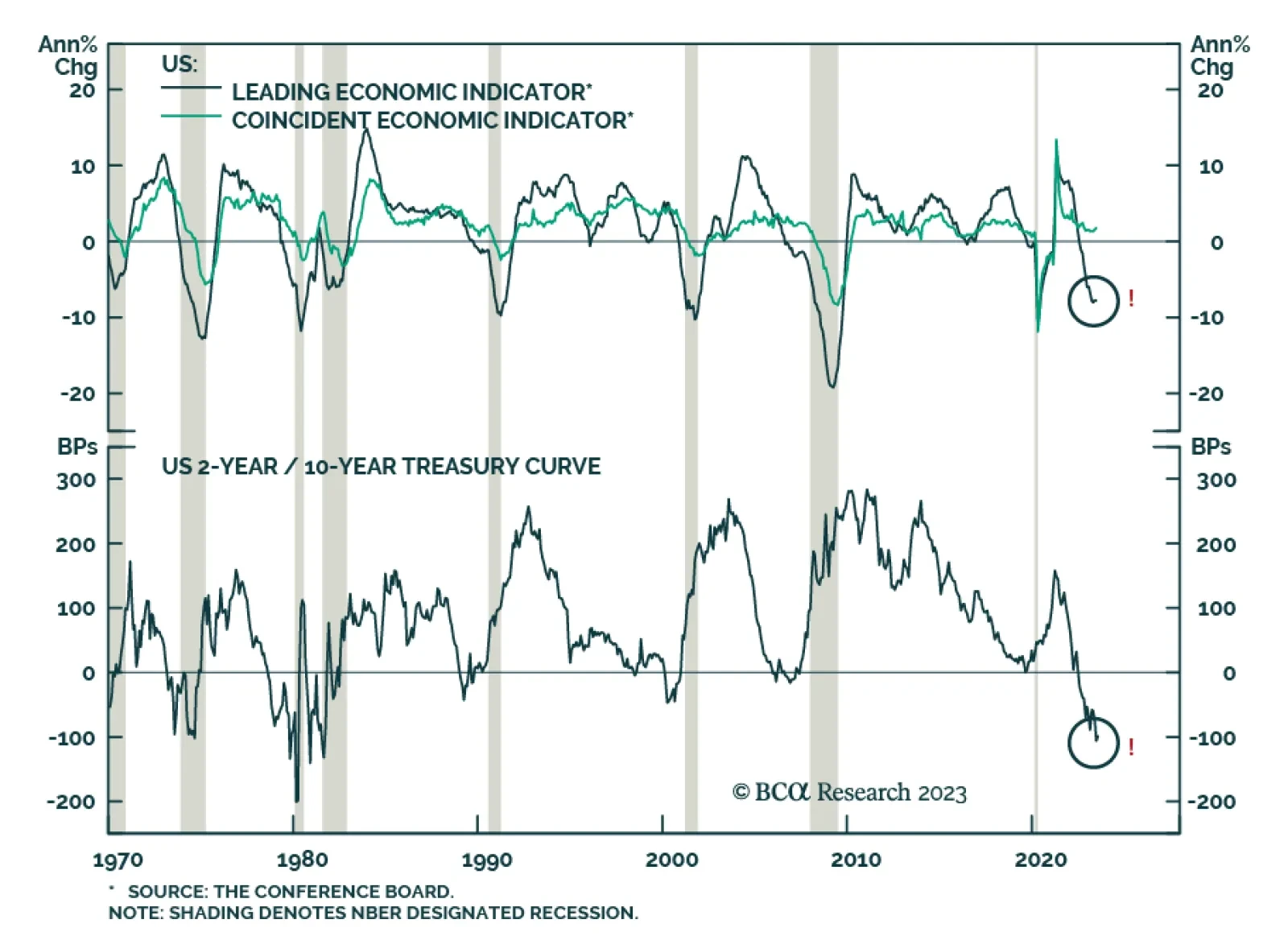

In Section I, we audit the market’s “soft landing” narrative in response to a meaningful challenge to our cautious stance from recent financial market developments. We acknowledge that US economic growth was stronger in the first half of the year than many investors expected, but we are unmoved by the recent uptick in “soft landing” hopes. A “soft landing” outcome very likely necessitates interest rate cuts before recessionary dynamics emerge, and it is far from clear that rate cuts or (especially) an easy monetary policy stance are likely to materialize over the coming year. As such, we continue to believe that conservative portfolio positioning is appropriate. In Section II, we discuss some simple approaches that we use when valuing the major asset classes that we cover. We conclude that global ex-US equities and ex-US developed market currencies are the main assets that can be considered “cheap” today.

We see challenges ahead for Global Buyout across geographies as valuations need further resetting. While we are concerned with capital controls and flight risk in Asia-Pacific Venture Capital, the upside potential from AI may be worth a look. The current entry point for Private Credit is opportune across North America and Europe with the distressed pipeline building. Real Estate does not look appealing with the macro and relative opportunity set driving our underweight. Hedge Funds have a favorable backdrop in the near-term, although prospects differ across Directional, Diversifier, and Crisis Risk Offset strategies.

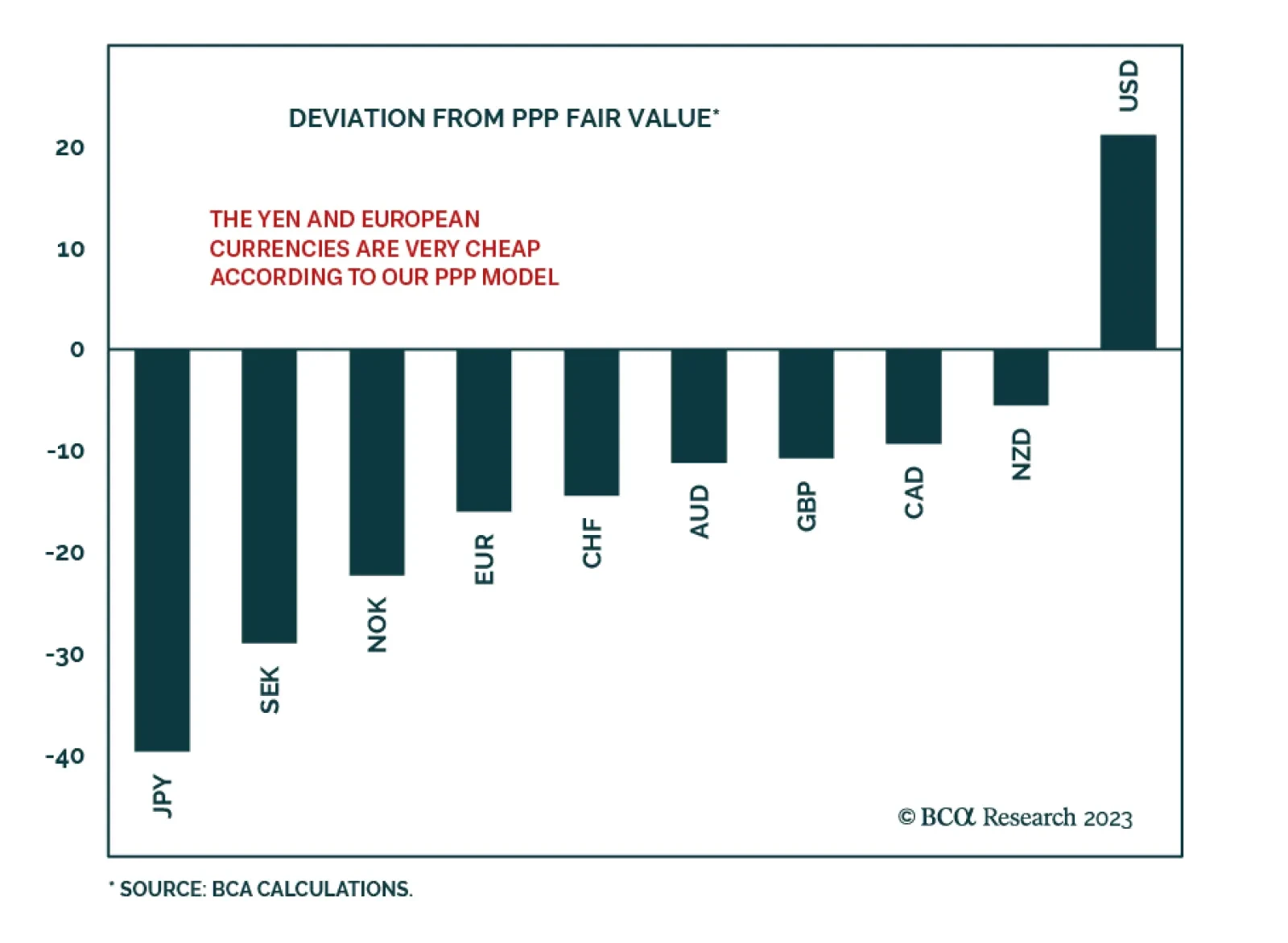

In this report, we evaluate the breakdown in the dollar and next moves in the DXY, based on fundamentals, historical precedents, and technical patterns over the last few years.

In this report, we evaluate the breakdown in the dollar and next moves in the DXY, based on fundamentals, historical precedents, and technical patterns over the last few years.